Basal Cell Carcinoma Treatment Market Size Analysis:

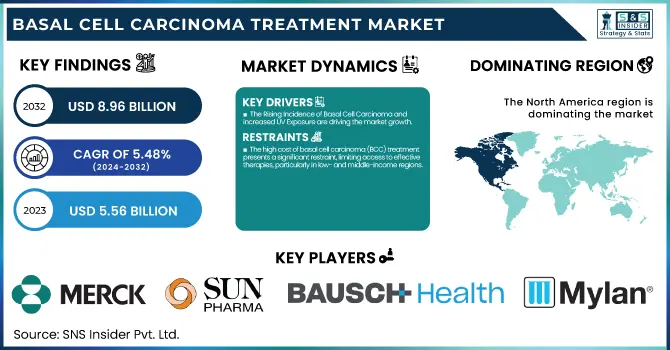

The Basal Cell Carcinoma Treatment Market size was estimated at USD 5.56 billion in 2023 and is projected to reach USD 8.96 billion by 2032, growing at a CAGR of 5.48% from 2024 to 2032.

The Basal Cell Carcinoma (BCC) Treatment Market report provides innovative insights through in-depth incidence and prevalence analysis, emphasizing trends in age, gender, and regional distribution. It comprises treatment adoption trends by region, illustrating differences in the application of surgery, radiation, and targeted therapies according to healthcare infrastructure.

To Get more information on Basal Cell Carcinoma Treatment Market - Request Free Sample Report

The report also contains patient volume trends, which forecast future demand for BCC treatments. A detailed breakdown of healthcare expenditures includes government, commercial, private, and out-of-pocket spending and gives clear insights into financial trends. These in-depth insights provide a fact-based point of view on treatment dynamics, access, and economic effects in the BCC market.

Basal Cell Carcinoma Treatment Market Dynamics

Drivers

-

The Rising Incidence of Basal Cell Carcinoma and increased UV Exposure are driving the market growth.

The rising incidence of basal cell carcinoma (BCC) is a major growth driver for the market, with increasing cases attributed to long-term ultraviolet (UV) radiation exposure. The Skin Cancer Foundation estimates that about 3.6 million cases of BCC are diagnosed each year in the United States alone. Climate change, ozone depletion, and lifestyle changes have all led to increased UV exposure, raising the risk of skin cancers worldwide. Also, aging and fair-skinned populations are especially susceptible, which is propelling the need for new treatment solutions. To meet this, pharmaceutical firms are creating novel therapies, including Sun Pharmaceuticals' Odomzo (sonidegib) and Roche's Erivedge (vismodegib), that act on the Hedgehog signaling pathway. These developments, along with early detection programs, are heavily driving the BCC treatment market growth.

-

Advancements in targeted and immunotherapy treatments are driving the basal cell carcinoma treatment market.

The basal cell carcinoma treatment market is fueled by ongoing progress made in targeted treatment and immunotherapy, offering patients less invasive and more effective treatment options. The approval of Hedgehog pathway inhibitors such as vismodegib (Erivedge) and sonidegib (Odomzo) has greatly changed the treatment of BCC, especially locally advanced and metastatic disease. Also, immunotherapies like PD-1 inhibitors are on the rise, with Sanofi and Regeneron's Libtayo (cemiplimab-rwlc) gaining FDA approval for advanced BCC in 2021. These new treatments provide options to surgery and radiation, lessening the reliance on invasive interventions. Also, clinical trials continue to investigate new biologics and combination treatments, increasing the effectiveness of treatments. The increasing uptake of personalized medicine, combined with growing research activities in oncology drug development, is fueling the market's growth.

Restraint

-

The high cost of basal cell carcinoma (BCC) treatment presents a significant restraint, limiting access to effective therapies, particularly in low- and middle-income regions.

Newer treatment methods, including targeted therapies (for example, Hedgehog pathway inhibitors vismodegib and sonidegib) and immunotherapies, are highly expensive and cannot be afforded by most patients unless they have good insurance coverage. Even surgical treatments, such as Mohs micrographic surgery, are expensive in terms of the specialized skills needed. Cancer therapies occupy a major chunk of out-of-pocket spending across various areas, according to reports of healthcare spending. Additionally, reimbursement policies between nations are different, creating inequalities regarding the accessibility of treatment. These cost-related barriers tend to delay diagnosis and treatment, further risking the advancement of the disease. Removing cost-related barriers by policy interventions and extending insurance coverage is still a pivotal step towards better patient outcomes.

Opportunities

-

The rising geriatric population and growing awareness of skin cancer represent a significant opportunity for the basal cell carcinoma (BCC) treatment market.

The increasing geriatric population and increased awareness of skin cancer are a major opportunity for the basal cell carcinoma (BCC) treatment market. Aging is a major risk factor for BCC, with a large majority of cases found in people aged over 60. With increasing global life expectancy, the number of older people at risk for BCC will increase, propelling demand for effective treatments. Further, public health programs and dermatological examinations are raising early detection levels, resulting in timely interventions and better patient outcomes. Governments and healthcare providers are raising skin cancer awareness, persuading people to visit doctors in case of suspect lesions. Higher awareness, together with improvements in non-invasive diagnostic equipment, is likely to increase the pool of patients and drive market growth in the forecast years.

Challenges

-

One of the major challenges in the basal cell carcinoma (BCC) treatment market is the risk of recurrence and treatment resistance.

One of the primary issues in the basal cell carcinoma (BCC) treatment market is recurrence and treatment resistance risk. Even with effective treatments like surgery, radiotherapy, and targeted therapy, a high proportion of patients relapse, especially those with aggressive or high-risk BCC subtypes. Recurrence rates among high-risk BCC can be as high as 50% over five years if not managed effectively. In addition, long-term use of Hedgehog pathway inhibitors such as vismodegib and sonidegib has been linked with resistance, making their long-term efficacy questionable. This issue calls for ongoing developments in drug therapy and other treatment modalities. Moreover, the absence of a standardized follow-up regimen and post-treatment surveillance enhances the risk of recurrence, further hampering disease control. Overcoming this issue is essential by addressing resistance mechanisms and enhancing long-term surveillance strategies.

Basal Cell Carcinoma Treatment Market Segmentation Analysis

By Type

The surgery segment dominated the basal cell carcinoma (bcc) treatment market with around 36.15% market share in 2023 because of its high effectiveness, widespread use, and capacity to remove cancerous tissues entirely. Surgical interventions like Mohs micrographic surgery (MMS) and excisional surgery are the gold standard for BCC treatment, particularly for recurrent or high-risk cases. Mohs surgery, specifically, offers greater accuracy through the removal of minimal tissue while guaranteeing total cancer removal, lowering recurrence rates. Greater access to advanced surgical methods, experienced dermatologic surgeons, and specialized treatment facilities also added to this segment's leadership. Moreover, the growing prevalence of BCC, combined with a preference for curative and definitive treatments, supported the demand for surgical procedures, especially in developed countries with well-established healthcare infrastructure.

The intralesional injections segment is expected to show the fastest growth rate in the forecast period, owing to the increasing need for non-surgical and minimally invasive BCC treatment. Intralesional treatments are based on the direct injection of chemotherapeutic or immunomodulatory drugs into the tumor, which causes localized regression of the tumor with fewer systemic side effects. Advancements in biologic therapies, such as immune checkpoint inhibitors and targeted drug delivery systems, have made this method more effective. This technique is especially advantageous for patients ineligible for surgery because of age, comorbidities, or lesion location in cosmetically sensitive regions like the face. Furthermore, the growing availability of new and emerging intralesional drugs and active clinical trials to test their efficacy are anticipated to fuel adoption, thus forming a central driver of market growth during the forecast years.

By Treatment providers

The hospital segment dominated the basal cell carcinoma (bcc) treatment market in 2023, driven mainly by the presence of sophisticated treatment centers, specialized oncology units, and multidisciplinary care strategies. Hospitals offer a wide array of BCC treatments, such as Mohs micrographic surgery, radiation therapy, and systemic therapies, and are thus the most sought-after option for patients with advanced-stage or high-risk BCC. Besides, hospitals have access to advanced technologies, clinical trials, and well-trained oncologists and dermatologists, which further put them in a strong position. The rise in the incidence of BCC, coupled with increased patient flow for surgical and combination treatments, has further placed the hospitals as the major treatment platform. In addition, generous reimbursement policies and the availability of specialized cancer centers within hospital chains have helped the segment capture the global market.

The dermatology clinics segment is also expected to be the fastest-growing in the forecast period because of the growing trend for outpatient procedures, enhanced access to dermatologists, and improvement in minimally invasive procedures. Early-stage BCC or low-risk lesion patients increasingly opt for dermatology clinics for treatments such as cryotherapy, photodynamic therapy, topical chemotherapy, and intralesional injections. Such clinics provide quicker waiting periods, affordable treatment, and advanced dermatologic skills, making them a quick option compared to hospitals. Moreover, the increased use of teledermatology and AI-based diagnostic equipment by dermatology clinics will soon enhance early detection and treatment rates. As knowledge about skin cancer screening and preventive dermatology care increases, dermatology clinics will keep growing at a fast pace, particularly in urban and highly developed healthcare economies.

Basal Cell Carcinoma Treatment Market Regional Insights

North America dominated the basal cell carcinoma (bcc) treatment market with around 58.46% market share in 2023 because of its well-developed healthcare infrastructure, high incidence of skin cancer, and strong presence of major pharma companies. The North American region has a high rate of incidence of BCC, which is influenced by high exposure to ultraviolet (UV) radiation, especially in the United States. High diagnostic capacity and extensive awareness regarding skin cancer have resulted in early detection and timely intervention. Also, the area is supported by strong research and development efforts with ongoing innovations in targeted therapies, immunotherapies, and topical treatments. Supportive reimbursement policies and the availability of regulatory organizations such as the FDA also sustain market growth and make North America the top BCC treatment region.

Asia Pacific is the fastest growing region in the basal cell carcinoma treatment market with a 6.18% CAGR throughout the forecast period, with growing incidences of skin cancer, growing healthcare expenditure, and rising access to expensive treatments. Nations such as China, India, and Japan are seeing a hike in BCC incidence because of altered environmental patterns, more outdoor exposure, and population aging. Moreover, rising awareness regarding skin cancer and early detection, combined with a growing healthcare infrastructure, are driving demand for efficient treatment solutions. The region is also witnessing rising investments from pharmaceutical players seeking to strengthen their market foothold. With continuous clinical trials, the launch of novel therapies, and government support, Asia Pacific is expected to see remarkable market growth in the future.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players in the Basal Cell Carcinoma Treatment Market

-

Merck & Co., Inc. (Erivedge, Keytruda)

-

F. Hoffmann-La Roche Ltd. (Erivedge, Tecentriq)

-

Sun Pharmaceuticals Ltd. (Odomzo, Tazorac)

-

Bausch Health Companies Inc. (Efudex, Solage)

-

Mylan N.V. (Fluorouracil Cream, Imiquimod Cream)

-

Allergan plc (Zyclara, Tretinoin Cream)

-

Perrigo Company plc (Imiquimod Cream, Fluorouracil Cream)

-

Strides Pharma Science Limited (Fluorouracil Cream, Imiquimod Cream)

-

Amgen Inc. (Imlygic, Enbrel)

-

Almirall, LLC (Fluorouracil Cream, Imiquimod Cream)

-

AiViva BioPharma (AIV001, AIV007)

-

3M Pharmaceuticals (Aldara, Fluorouracil Cream)

-

Pfizer Inc. (Daurismo, Xalkori)

-

Novartis International AG (Odomzo, Tafinlar)

-

Sanofi S.A. (Libtayo, Jevtana)

-

Regeneron Pharmaceuticals, Inc. (Libtayo, Zaltrap)

-

Glenmark Pharmaceuticals (Fluorouracil Cream, Imiquimod Cream)

-

Teva Pharmaceutical Industries Ltd. (Fluorouracil Cream, Imiquimod Cream)

-

Dr. Reddy's Laboratories (Fluorouracil Cream, Imiquimod Cream)

-

Cipla Limited (Fluorouracil Cream, Imiquimod Cream)

Recent Development in the Basal Cell Carcinoma Treatment Market

-

July 2024 – Samsung Bioepis Co., Ltd. announced that the U.S. Food and Drug Administration (FDA) has approved the Biologics License Application (BLA) for PYZCHIVA (ustekinumab-ttwe), both subcutaneous injection and intravenous infusion. PYZCHIVA is approved as a biosimilar for Stelara (ustekinumab) and as a treatment of moderate to severe plaque psoriasis in patients qualifying for phototherapy or systemic treatment, active psoriatic arthritis, moderately to severely active Crohn's disease, and moderately to severely active ulcerative colitis. Further, PYZCHIVA received a provisional interchangeability determination.

-

September 2024 – Sonidegib phosphate, a product of Sun Pharma Advanced Research, is under Phase I clinical trials for Non-Small Cell Lung Cancer. GlobalData reports that Phase I drugs for this indication have an 80% Phase Transition Success Rate (PTSR) for progressing to Phase II. GlobalData's analysis compares Sonidegib phosphate's drug-specific PTSR and Likelihood of Approval (LoA) against established benchmarks for Non-Small Cell Lung Cancer drugs.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 5.56 billion |

| Market Size by 2032 | US$ 8.96 billion |

| CAGR | CAGR of 5.48 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Surgery, Radiotherapy (RT), Intralesional Injections, Topical Chemotherapy, Oral Medications, Intravenous Medications, Chemical Peeling Treatment) • By Treatment Providers (Hospitals, Dermatology Clinics, Cancer Treatment Centers, Other Treatment Providers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Merck & Co., Inc., F. Hoffmann-La Roche Ltd., Sun Pharmaceuticals Ltd., Bausch Health Companies Inc., Mylan N.V., Allergan plc, Perrigo Company plc, Strides Pharma Science Limited, Amgen Inc., Almirall, LLC, AiViva BioPharma, 3M Pharmaceuticals, Pfizer Inc., Novartis International AG, Sanofi S.A., Regeneron Pharmaceuticals, Inc., Glenmark Pharmaceuticals, Teva Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories, Cipla Limited, and other players. |

Frequently Asked Questions

Ans: North America dominated the Basal Cell Carcinoma Treatment Market in 2023.

Ans: The “Surgery” segment dominated the Basal Cell Carcinoma Treatment Market.

Ans: The Rising Incidence of Basal Cell Carcinoma and increased UV Exposure are driving the market growth.

Ans: The Basal Cell Carcinoma Treatment Market was USD 5.56 billion in 2023 and is expected to reach USD 8.96 billion by 2032.

Ans: The Basal Cell Carcinoma Treatment Market is expected to grow at a CAGR of 5.48% during 2024-2032.

Get in Touch