Battery Production Machine Market Report Scope & Overview:

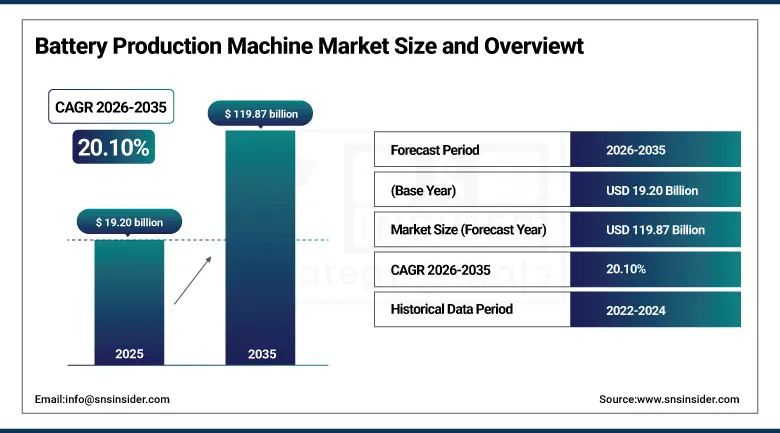

The Battery Production Machine Market size was valued at USD 19.20 billion in 2025 and is expected to reach USD 119.87 billion by 2035, growing at a CAGR of 20.10% from 2026-2035.

Growth in the Battery Production Machine Market is attributed to the increased demand for electric vehicles, energy storage systems, and portable electronics. The increasing emphasis of the global community on energy transition towards clean sources is leading to investments in battery production. Innovation in lithium-ion batteries and next-generation batteries is contributing to higher productivity in battery production machines. The growing trend of developing gigafactories, initiatives to encourage EV adoption, and robust investment in energy storage facilities are also fueling market growth.

Market Size and Forecast

-

Market Size in 2025: USD 19.20 Billion

-

Market Size by 2035: USD 119.87 Billion

-

CAGR: 20.10% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Battery Production Machine Market - Request Free Sample Report

Battery Production Machine Market Trends

-

Rising demand for electric vehicles and energy storage systems is driving the battery production machine market.

-

Growing expansion of lithium-ion battery manufacturing facilities is boosting equipment demand.

-

Increasing focus on large-scale gigafactories and automated production lines is fueling market growth.

-

Expansion of renewable energy storage and consumer electronics manufacturing is supporting deployment.

-

Advancements in electrode coating, cell assembly, formation, and testing equipment are improving efficiency and precision.

-

Rising emphasis on automation, quality control, and high-throughput production is shaping adoption trends.

-

Collaborations between battery manufacturers, machinery providers, and automation companies are accelerating innovation and global adoption.

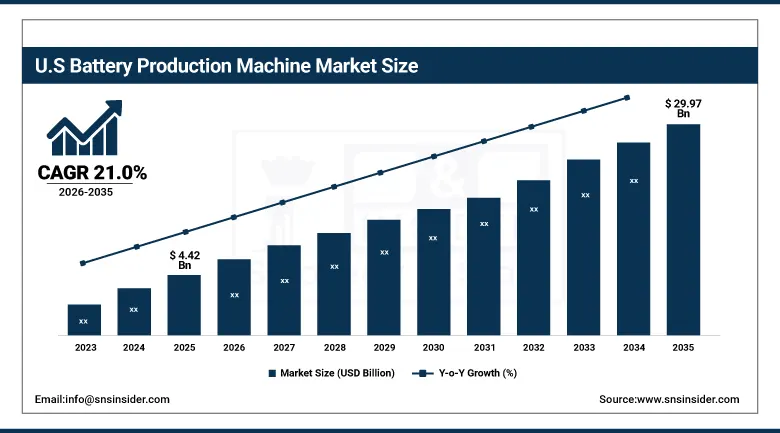

U.S. Battery Production Machine Market Size Outlook:

The U.S. Battery Production Machine Market was valued at approximately USD 4.42 billion in 2025 and is expected to reach around USD 29.97 billion by 2035, growing at a CAGR of about 21.0% from 2026–2035. U.S. Battery Production Machine Market is experiencing growth owing to increased adoption of electric vehicles, significant investments in battery gigafactories, and rising need for renewable energy storage systems. Growth in the market is also fueled by government incentives, advancements in lithium-ion batteries, and automation in production processes.

Battery Production Machine Market Segment Highlights

-

By Machine, Slitting Machines segment dominated the Battery Production Machine Market in 2025 with 31% share; Stackers segment fastest growing (CAGR).

-

By Battery, Lithium-ion Batteries segment dominated the Battery Production Machine Market in 2025 with 68% share; Flow Batteries segment fastest growing (CAGR).

-

By Application, Automotive Industry segment dominated the Battery Production Machine Market in 2025 with 52% share; Energy Storage segment fastest growing (CAGR).

By Machine, Slitting Machines segment dominates the Battery Production Machine Market, Stackers segment expected to grow fastest

The Slitting Machines segment held the largest share of the Battery Production Machine Market in 2025 owing to their importance in electrode production through accurate cutting of battery materials. Slitting machines play an important role in lithium-ion battery assembly line operations where there is need to maintain uniformity in quality and minimize waste. With the fast-paced growth in electric vehicle manufacturing, increased demand for high-performing batteries, and automation in battery production processes, slitting machines dominate the market.

The Stackers segment is the fastest-growing segment in the market owing to increased demand for automated cell stacking in advanced battery manufacturing plants. Stackers help increase the speed of production by layering electrodes and separators automatically while minimizing human error. Increased investments in gigafactories, automation in battery production processes, and demand for increased production capacity for electric vehicles and energy storage systems are contributing factors behind the fast-paced growth in the stackers segment.

By Battery, Lithium-ion Batteries segment dominates the Battery Production Machine Market, Flow Batteries segment expected to grow fastest

Lithium-ion Batteries had the leading market share in the Battery Production Machine Market in 2025. This segment is popular because of its application in electric vehicles, consumer electronic devices, and energy storage systems for renewable energy sources. The lithium-ion batteries possess benefits such as high energy density, extended lifecycle, and fast charging, which makes them the most preferred batteries in all industrial sectors. There is an increased demand for EV manufacturers, and the lithium-ion batteries' cells' chemical structure continues to evolve through research.

The Flow Batteries market is experiencing a fast-paced growth rate due to the increasing demand for high-capacity and long-duration energy storage systems. This type of battery has several advantages such as scalability, long life cycle, and enhanced safety; therefore, it can be used for renewable energy storage purposes. The increasing installation of solar/wind plants and the rising focus on eco-friendly energy storage systems have contributed to the growth of this market.

By Application, Automotive Industry segment dominates the Battery Production Machine Market, Energy Storage segment expected to grow fastest

In 2025, the Automotive Industry segment was dominant in the Battery Production Machine Market, driven by the swift growth of the electric vehicle industry and high demand for premium batteries. The automobile industry is currently making substantial investments in state-of-the-art battery manufacturing equipment to increase performance, range, and charging rates. Policies for the use of EVs, reducing carbon emissions, and increasing public awareness of the benefits of electric cars have further consolidated the position of this market segment.

The Energy Storage segment represents the highest growth rate, attributed to the growing installation of renewable energy sources and the need for large energy storage facilities. Battery storage units aid in maintaining equilibrium between energy supply and demand and facilitate efficient grid management. Growing installations of solar and wind energy and investments in green energy infrastructure are creating high demand for sophisticated battery production machinery in the segment worldwide

Battery Production Machine Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

86.9% |

|

Europe |

United Kingdom |

19.6% |

|

Asia Pacific |

Australia |

5.8% |

|

Middle East & Africa |

UAE |

12.7% |

|

Latin America |

Brazil |

44.9% |

North America Battery Production Machine Market Insights

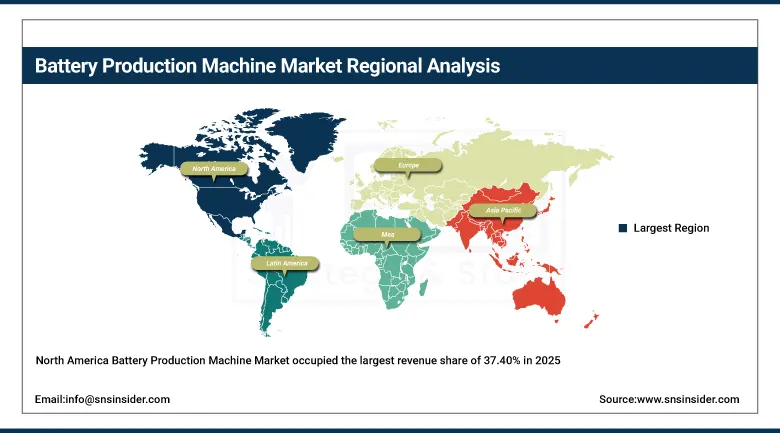

The North America Battery Production Machine Market occupied the largest revenue share of 37.40% in 2025 owing to the fast growth in electric vehicle manufacturing and substantial investment in battery gigafactories. The region is advantaged by sophisticated industrial automation processes, robust presence of key battery and automotive manufacturers, and favorable government initiatives that support the transition towards green energy. Increasing usage of lithium-ion batteries in electric vehicles and energy storage systems also boosts market growth. Besides, constant technological advancement and widespread use of automated machines contribute to regional dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Battery Production Machine Market Insights

Asia Pacific region is anticipated to have the highest CAGR of 22.67% during the forecasted period in the Battery Production Machine market owing to rapid developments in EV manufacturing coupled with rapid emergence of battery gigafactories in nations like China, Japan, South Korea, and India. Growing government initiatives towards clean energy transition and local manufacturing of batteries have led to increased investment in the market. High demand for lithium-ion batteries for consumer electronics, EVs, and energy storage systems coupled with low costs and efficient supply chain networks has accelerated market growth in the region.

Europe Battery Production Machine Market Insights

The Europe Battery Production Machine Market is showing steady growth owing to the significant emphasis laid on the adoption of electric vehicles and renewable energy sources. The increasing number of investment in the development of battery gigafactories in Germany, France, and the United Kingdom has contributed significantly to the demand for manufacturing machines. The stringent environmental norms along with the aim of reducing carbon emissions is adding fuel to the demand for battery production. The increasing use of lithium-ion batteries is positively influencing the growth of the market.

Middle East & Africa and Latin America Battery Production Machine Market Insights

In Middle East and Africa and Latin America Battery Production Machine Market, there has been steady growth because of increased investment in renewable energy and electric vehicle programs. Increased usage of energy storage systems and industrial developments are some reasons why the demand for battery production machines is growing. There is also government encouragement towards energy transformation as well as local manufacturing of batteries. However, technological limitations and high investments are restricting the market's rapid growth.

Growth Drivers: Rapid expansion of electric vehicle manufacturing and global shift toward clean mobility accelerating demand for advanced battery production machinery worldwide

The fast-growing EV industry plays an important role in the increased demand for machinery used for producing batteries. The rising popularity of EVs, coupled with government initiatives aimed at decreasing emissions, encourages large-scale lithium-ion batteries' manufacturing. Automakers are currently building gigafactories that would require equipment capable of processing lithium-ion batteries quickly and with high accuracy. In addition to that, the growing trend towards environmentally-friendly transport and progress in technologies used for making batteries also contribute to the development of production capacity. Moreover, growing competition within the EV manufacturing market contributes to the rising need for efficient manufacturing equipment.

Restraints: High capital investment and complex manufacturing processes limiting entry of small players into advanced battery production equipment market

The need for high investment to establish advanced battery production facilities acts as a restriction on the market growth prospects. The machines used in battery production, including laminating, stacking, and automated machines, require considerable investments, thus making it hard for small and medium scale companies to join the market. In addition, battery production requires sophisticated processes that call for costly engineering, clean room requirements, and a well-skilled labor force. Also, the high costs associated with maintenance and continuous technological upgrades pose a significant challenge to the manufacturer. Dependency on supply chains for advanced component parts contributes to increased costs.

Opportunities: Technological advancements in solid-state batteries and next-generation energy storage systems creating new growth opportunities for advanced production machinery

The rapid advancements being made in solid-state batteries and other future energy storage solutions are generating immense prospects for manufacturers of battery making machines. The manufacturing of such cutting-edge batteries needs sophisticated manufacturing techniques, including accurate coating, stacking, and assembling processes. Growing investments being made in R&D activities are leading to a higher demand for flexible and customizable manufacturing systems. Manufacturing of batteries using automation and AI-based systems is now gaining importance due to changing design demands. Commercialization of these future energy storage solutions in the automotive industry and other industrial applications is boosting the demand.

Recent Developments:

-

2026: Tesla is expected to further enhance AI-based computer vision systems in Full Self-Driving (FSD), improving real-time object detection, neural network perception, and autonomy scaling across fleets. The company continues refining vision-only autonomous architecture for future mobility systems.

-

2025: Siemens expanded collaboration with NVIDIA to accelerate AI-powered industrial computer vision, enabling immersive digital twin environments and smarter manufacturing automation across production ecosystems.

-

2024: Panasonic developed advanced AI vision technology to improve industrial inspection and image recognition efficiency, optimizing deployment of computer vision systems in manufacturing environments and smart factories.

Battery Production Machine Companies are:

-

Tesla

-

Panasonic

-

Samsung SDI

-

CATL (Contemporary Amperex Technology Co. Limited)

-

BYD Company Ltd.

-

Manz AG

-

Wuxi Lead Intelligent Equipment Co., Ltd.

-

Shenzhen Yinghe Technology Co., Ltd.

-

KUKA AG

-

ABB Ltd.

-

Siemens AG

-

Dürr Group

-

Schuler Group

-

Targray Technology International

-

Hymson Laser Technology Group

-

CKD Corporation

-

Toray Industries

-

3M Company

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.20 Billion |

| Market Size by 2035 | USD 119.87 Billion |

| CAGR | CAGR of 20.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Machine(Slitting machines, Laminators, Stackers, Dryers, Formers) •By Battery(Lithium-ion batteries, Lead-acid batteries, Nickel-cadmium batteries, Nickel-metal hydride batteries, Flow batteries) •By Application (Automotive industry, Consumer electronics, Energy storage, Marine applications, Medical devices) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tesla, Panasonic, LG Energy Solution, Samsung SDI, CATL (Contemporary Amperex Technology Co. Limited), BYD Company Ltd., Hitachi High-Tech Corporation, Manz AG, Wuxi Lead Intelligent Equipment Co., Ltd., Shenzhen Yinghe Technology Co., Ltd., KUKA AG, ABB Ltd., Siemens AG, Dürr Group, Schuler Group, Targray Technology International, Hymson Laser Technology Group, CKD Corporation, Toray Industries, 3M Company. |

Frequently Asked Questions

Ans: North America dominated the The Battery Production Machine Market in 2025.

Ans: The Slitting Machines segment dominated the Battery Production Machine Market in 2025.

Ans: The major growth factor of the The Battery Production Machine Market is increasing global demand for electric vehicles, driving investments in advanced battery manufacturing technologies and automation.

Ans: The Battery Production Machine Market was valued at USD 19.20 billion in 2025.

Ans: The Battery Production Machine Market is expected to grow at a CAGR of 20.10% from 2026 to 2035.

Get in Touch