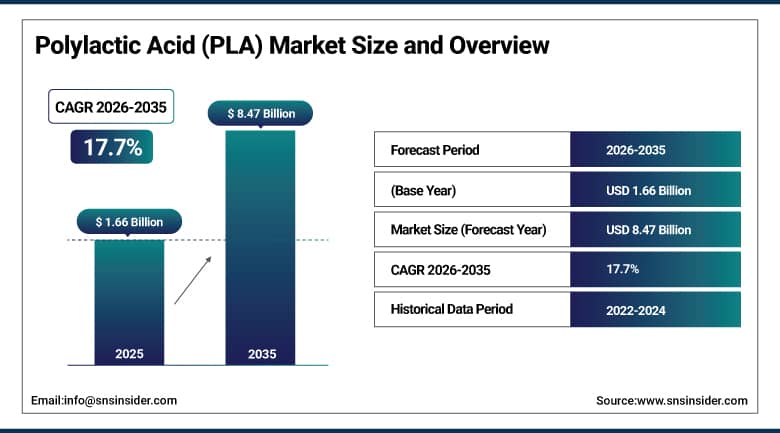

Polylactic Acid (PLA) Market Report Scope & Overview:

The Polylactic Acid (PLA) Market was valued at USD 1.66 Billion in 2025 and is expected to reach USD 8.47 Billion by 2035, growing at a CAGR of 17.7% from 2026 to 2035.

PLA has slowly become one of the success stories when it comes to the wider trend toward materials that do not rely on petroleum for their production, and this development speaks volumes about the degree to which bio-based materials have managed to establish themselves over the past several years. Produced using such renewable resources as cornstarch and sugarcane, PLA has the ability to biodegrade and be composted while not compromising mechanical properties, thus making it a good fit for use in packaging, textiles, agriculture, automotive parts, and electronic housing.

Government policy has done a lot of the heavy lifting here too: regulations promoting biodegradable polymer adoption, particularly across packaging, gained real momentum in 2023, and that regulatory tailwind, combined with steadily improving production economics, has helped PLA move from a niche sustainability play into something closer to a mainstream materials choice for brands trying to cut their plastic footprint.

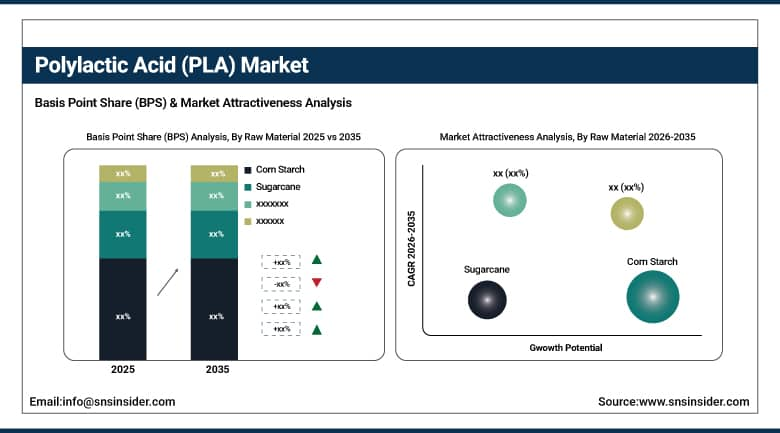

Corn starch accounted for more than 63% of PLA raw material consumption in 2023, reflecting the material's ready abundance and comparatively low-cost relative to alternative renewable feedstocks used in PLA manufacturing.

Market Size and Forecast

- Market Size in 2026E: USD 1.95 Billion

- Market Size by 2035: USD 8.47 Billion

- CAGR: 17.7% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get More Information On Polylactic Acid (PLA) Market - Request Free Sample Report

Polylactic Acid (PLA) Market Trends

- Rising adoption of biodegradable plastics in packaging is cutting environmental pollution and driving demand for sustainable alternatives like PLA across food and consumer goods.

- Increasing use of PLA in 3D printing is supporting lightweight, durable, and customizable manufacturing across a widening range of industries.

- Growth in medical applications, including implants and drug delivery systems, is leaning heavily on PLA's biocompatibility and biodegradability.

- Advancements in polymer blending and compounding are enhancing PLA's thermal stability, mechanical strength, and processability for more demanding applications.

- Government regulations and bans on single-use plastics keep accelerating PLA adoption across both consumer and industrial packaging.

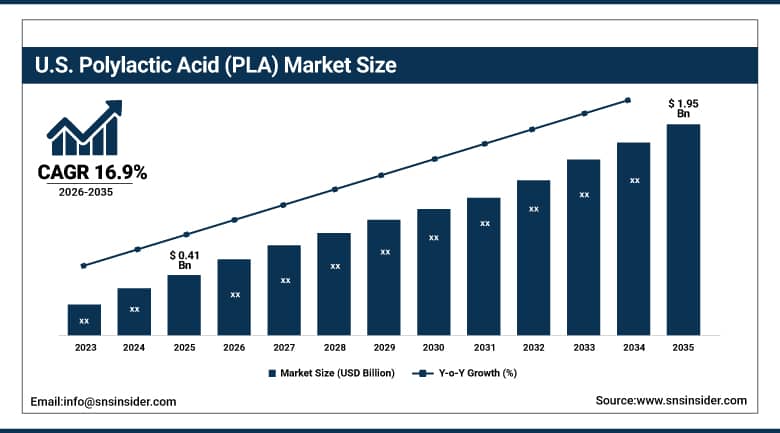

U.S. Polylactic Acid (PLA) Market Outlook

The U.S. Polylactic Acid (PLA) Market was valued at approximately USD 0.41 Billion in 2025 and is expected to reach approximately USD 1.95 Billion by 2035, growing at a CAGR of approximately 16.9%.

The U.S. is currently dominating the PLA market in North America owing to the abundant corn harvest in the region, high-level infrastructure used for the manufacture of bioplastic products, and the presence of favorable government policies such as the Farm Bill and EPA. The investments in the packaging industry and other food industry players that are willing to transition from conventional plastics to bioplastics also continue to support the dominant position of the US in the market, as the consumers’ demand for environmentally friendly PLA grows. These factors make the US the biggest contributor to the PLA market in North America.

The USDA reports that global demand for bioplastics, including PLA, keeps climbing as more countries adopt policy specifically targeting a reduction in single-use plastic waste, reinforcing the U.S. market's role as both a major producer and a major consumer within the global PLA supply chain.

Polylactic Acid (PLA) Market Segment Analysis

- By Raw Material, corn starch dominated the PLA market with more than 63% share in 2025, while Sugarcane is the fastest-growing raw material segment.

- By Application, rigid thermoform led with more than 43% share in 2025, while films & sheets is the fastest-growing application segment.

- By End Use, packaging dominated with more than 36% share in 2025, while textile is the fastest-growing end-use segment.

By Raw Material, corn starch leads, sugarcane grows fastest

Corn starch dominated the raw material segment in 2025, at more than 63% share, largely on the strength of its ready abundance and comparatively low cost as a feedstock for PLA manufacturing. Regions like the U.S. and Brazil have built out substantial corn-starch-to-PLA processing capacity, supported by agricultural subsidies, government policy encouraging resource upgrading, and local economies built around the crop that grows the underlying material. That combination of scale, cost advantage, and established supply chain has kept corn starch firmly ahead of alternative feedstocks.

Sugarcane is emerging as the fastest-growing raw material, as manufacturers look to diversify their feedstock base and tap into regions where sugarcane offers cost and availability advantages that corn doesn't. Growing interest in geographic and agricultural diversification, particularly as manufacturers try to reduce exposure to any single crop's price volatility or supply disruption, is helping sugarcane-based PLA production expand its footprint even as corn starch remains the dominant overall feedstock.

By Application, rigid thermoform leads, films & sheets grow fastest

Rigid thermoform dominated the application segment in 2025, at more than 43% share, driven primarily by growing adoption of biodegradable rigid thermoform packaging within the food packaging sector. Containers, clamshells, and trays made from PLA offer food brands a genuinely compostable alternative to conventional plastic packaging, and that practical substitution, paired with rising consumer and regulatory pressure to cut plastic waste, has kept rigid thermoform the largest single application for PLA globally.

Films & Sheets are set to grow fastest, supported by expanding food and beverage delivery services and the growing use of PLA films in disposable cutlery, cups, and clamshell containers. As food delivery volumes keep climbing globally, the packaging materials supporting that industry are under increasing pressure to be genuinely compostable rather than just recyclable in theory, and PLA films and sheets are proving to be one of the more practical materials able to meet that bar at commercial scale.

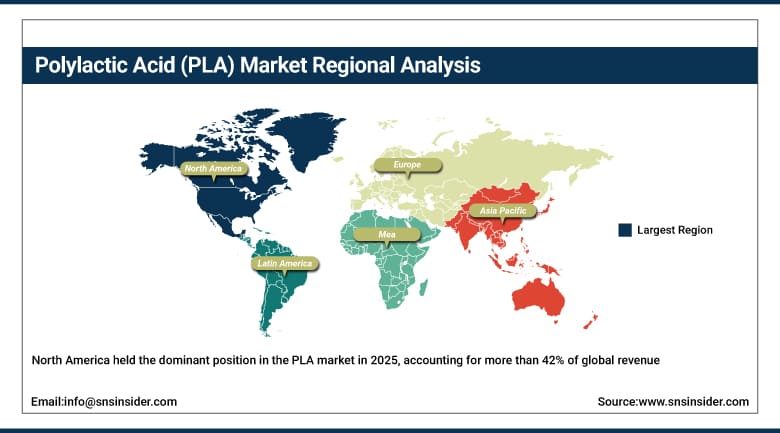

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

76.30% |

|

Europe |

Germany |

23.85% |

|

Asia Pacific |

China |

31.40% |

|

Middle East & Africa |

UAE |

24.90% |

|

Latin America |

Brazil |

38.60% |

North America Polylactic Acid (PLA) Market Insights

North America held the dominant position in the PLA market in 2025, accounting for more than 42% of global revenue, a leadership position driven by progressive environmental policy, federal support for bioplastics, and robust demand from both the packaging and automotive industries. The region's strong demand for sustainable products, combined with a mature bioplastics manufacturing base, has kept North America firmly ahead of every other region in overall market share.

The United States accounts for roughly 76.30% of regional revenue, supported by large-scale corn production, advanced bioplastics manufacturing infrastructure, and government programs including the USDA's initiatives promoting eco-friendly agricultural products. Canada adds further regional demand as its own packaging and consumer goods industries continue shifting toward biodegradable material options, and that combined regional strength should keep North America the largest addressable market for PLA producers through the forecast period.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Polylactic Acid (PLA) Market Insights

Europe represents a genuinely significant market for PLA, underpinned by some of the world's strictest regulation on single-use plastics, including the EU's Single-Use Plastics Directive and Circular Economy Action Plan, both of which have meaningfully accelerated the shift toward biodegradable packaging materials across the bloc. Strong consumer demand for organic and sustainably packaged food products continues reinforcing that regulatory push across the region's major economies.

Germany leads regional demand at roughly 23.85% of European revenue, supported by high economic development and a consumer preference for premium, sustainably packaged food products that's helped drive demand for high-quality biodegradable materials. The UK and France contribute substantial additional demand, and the EU's continued regulatory tightening around single-use plastics should keep European PLA demand climbing steadily through the forecast period.

Asia Pacific Polylactic Acid (PLA) Market Insights

Asia Pacific is the most rapidly growing region in terms of PLA, fueled by extensive manufacturing capacities, government policy favoring the use of biodegradable polymers, and increasing demands from both the packaging and agriculture industry. China and India dominate Asia Pacific in terms of the applications of PLA in packaging and agriculture, aided by low-cost raw materials and growing manufacturing capabilities, alongside initiatives to decrease plastic waste at the national level.

China leads the region, accounting for roughly 31.40% of regional revenue, supported by its large-scale packaging industry and substantial domestic PLA production capacity. India is expected to register a particularly strong growth rate as government initiatives to reduce plastic waste and rising investment in bioplastic manufacturing continue expanding the country's addressable market, and that broadening base of countries investing in domestic PLA capacity is what's keeping Asia Pacific's growth outlook well ahead of every other region tracked in this report.

MEA & Latin America Polylactic Acid (PLA) Market Insights

The Middle East & Africa and Latin America remain earlier in their PLA adoption curve than North America, Europe, or Asia Pacific, but both regions are seeing steady growth as government sustainability initiatives and expanding packaging and consumer goods industries continue building out demand for biodegradable material alternatives.

The UAE leads Middle East & Africa demand of regional revenue, supported by growing government focus on sustainability and expanding investment in packaging infrastructure. Saudi Arabia and South Africa contribute further regional demand through their own sustainability-driven modernization programs. In Latin America, Brazil accounts of regional revenue, with the country's substantial sugarcane feedstock base and growing packaging industry continuing to anchor regional demand for PLA.

Market Dynamics

Growth Drivers: Regulatory pressure and rising demand for sustainable packaging

The growing environmental awareness and rising popularity of authentic eco-friendly materials are the two main factors that will drive the growth of the PLA market. Consumers and companies want sustainable alternatives as a solution to plastic pollution and dependence on fossil fuels. The regulations regarding single-use plastic products that governments of many countries introduce are contributing greatly to the increase in the demand for PLA products since the use of PLA as an environmentally-friendly option becomes inevitable. Such regulatory decisions as the European Union's Single-Use Plastics Directive and Circular Economy Action Plan, along with similar U.S. policies, make such a move necessary rather than voluntary.

As the packaging sector represents one of the biggest sources of plastic pollution, it makes sense that the use of PLA in this industry becomes a key step for any company producing food, beverages, and consumer goods. The compostability and biodegradability of PLA make it a perfect material to produce food containers, wraps, and consumer goods packaging. Sustainability efforts of governments, as well as sustainability coalitions, such as Sustainable Packaging Coalition in the U.S., contribute to the popularity of PLA as a material.

Restraints: Higher raw material and production costs relative to conventional plastics

PLA is still significantly more expensive than the common plastic materials derived from fossil fuels. The cost difference has been one of the key constraints in the wider market penetration of this biodegradable material. The high cost of raw materials due to the complicated manufacturing process that involves fermenting and polymerizing to produce polymer from renewable sources makes PLA more expensive than common plastics such as polyethylene and polypropylene.

The issue is especially acute in emerging markets and low-margin products because customers cannot pay the additional cost associated with sustainability benefits. Unless production capacity and efficiency improve sufficiently to reduce the cost difference, the issue of cost sensitivity will probably continue restraining the widespread market adoption of PLA, especially in price-oriented market segments.

Opportunities: Expanding medical and 3D printing applications

Growth in medical applications, including implants and drug delivery systems, is opening a genuinely significant opportunity for PLA producers looking to move beyond commodity packaging into higher-value, higher-margin product categories. PLA's biocompatibility and biodegradability make it particularly well-suited to medical devices that need to safely dissolve or degrade within the body over time, and that application category carries meaningfully better margins than mass-market packaging typically does.

The growing use of PLA in 3D printing represents a second substantial opportunity, supporting lightweight, durable, and customizable manufacturing across industries ranging from consumer products to industrial prototyping. As additive manufacturing keeps expanding its footprint across both hobbyist and industrial applications, PLA's ease of processing and renewable sourcing makes it one of the more attractive filament materials on the market, and that growing installed base of 3D printing users represents a durable, expanding demand pool well beyond PLA's traditional packaging stronghold.

Recent Developments:

- 2025: Balrampur Chini Mills announced plans to establish India's first large-scale PLA bioplastics facility, operating under the Bioyug brand, expanding domestic PLA production capacity.

- 2023: Sulzer launched its SULAC technology, addressing growing market demand for lactic acid by enabling efficient conversion into lactide, a critical intermediate for producing PLA.

- 2023: Sulzer partnered with Jindan New Biomaterials on a planned annual PLA output of 75,000 tonnes for packaging, molded goods, and fiber applications in China.

Polylactic Acid (PLA) Companies are:

- NatureWorks LLC

- TotalEnergies Corbion PLA S.A.

- BASF SE

- Futerro S.A.

- Toray Industries, Inc.

- Mitsubishi Chemical Corporation

- COFCO Biotechnology (COFCO Biochemical)

- Zhejiang Hisun Biomaterials Co., Ltd.

- Evonik Industries AG

- Unitika Ltd.

- Danimer Scientific

- Jiangxi Keyuan Biopharm Co., Ltd.

- Shanghai Tong-jie-liang Biomaterials Co., Ltd.

- Sulzer Ltd

- Jiangsu Supla Bioplastics Co., Ltd.

- Braskem S.A.

- PTT MCC Biochem Co., Ltd.

- Teijin Limited

- Galactic S.A.

- Corbion N.V.

Polylactic Acid (PLA) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.66 Billion |

| Market Size by 2035 | USD 8.47 Billion |

| CAGR | CAGR of 17.7% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Raw Material (Corn Starch, Sugarcane, Cassava, Sugar Beet, Others) • By Application (Rigid Thermoform, Films & Sheets, Fiber, Others) • By End Use (Packaging, Textile, Agriculture, Automotive & Transport, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NatureWorks LLC, TotalEnergies Corbion PLA S.A., BASF SE, Futerro S.A., Toray Industries, Inc., Mitsubishi Chemical Corporation, COFCO Biotechnology (COFCO Biochemical), Zhejiang Hisun Biomaterials Co., Ltd., Evonik Industries AG, Unitika Ltd., Danimer Scientific, Jiangxi Keyuan Biopharm Co., Ltd., Shanghai Tong-jie-liang Biomaterials Co., Ltd., Sulzer Ltd, Jiangsu Supla Bioplastics Co., Ltd., Braskem S.A., PTT MCC Biochem Co., Ltd., Teijin Limited, Galactic S.A., and Corbion N.V. |

Frequently Asked Questions

The Polylactic Acid (PLA) Market was valued at USD 1.66 Billion in 2025.

The Packaging segment dominated the Polylactic Acid (PLA) Market with more than 36% share by end use in 2025.

The major growth factor is rising demand for eco-friendly, biodegradable materials, supported by government regulations promoting biodegradable polymers, particularly across packaging.

North America dominated the Polylactic Acid (PLA) Market in 2025 with more than 42% of total global market revenue.

Get in Touch