Cloud Workflow Market Report Scope & Overview:

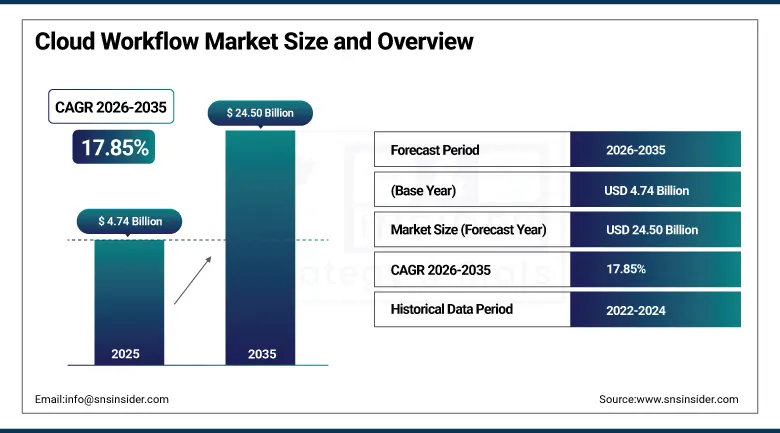

The Cloud Workflow Market size was USD 4.74 Billion in 2025 and is expected to reach USD 24.50 Billion by 2035, growing at a CAGR of 17.85% from 2026–2035.

Cloud Workflow Market is expanding at a rapid pace because of digitization, automation, and increased focus on cloud transformation. Cloud Workflow solution is increasingly being adopted by businesses to cater to their requirements of higher efficiency, enhanced collaboration, and reduced cost of operations. Increasing demands for AI-based automation and integration with enterprise software continue to fuel the growth of the market. Real-time data processing, compliance, and remote employee management are some of the five key growth drivers.

Companies ranging from small businesses to large enterprises are using cloud workflows to streamline their operations. The emergence of low-code and no-code platforms for automation of workflows is further helping ease down the adoption process.

ServiceNow introduced AI-powered workflow automation tools to enhance business process efficiencies in 2025, while Microsoft extended its Power Automate platform with intelligent automation capabilities. IBM released Cloud Pak for Business Automation to make banking workflows more efficient.

Market Size and Forecast

-

Market Size in 2026E: USD 5.58 Billion

-

Market Size by 2035: USD 24.50 Billion

-

CAGR: 17.85% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Cloud Workflow Market - Request Free Sample Report

Cloud Workflow Market Trends

-

AI-powered workflow automation keeps advancing across HR, finance, customer service, and supply chain functions.

-

Low-code and no-code workflow platforms are broadening adoption beyond traditional IT-led deployments.

-

Hyper automation combining RPA, AI, and cloud workflow is reshaping enterprise process automation strategies.

-

Integration with ERP and CRM systems keeps deepening as cloud workflow becomes core enterprise infrastructure.

-

SME adoption is accelerating as workflow-as-a-service models make enterprise automation accessible at lower cost.

-

Vertical-specific cloud workflow solutions for healthcare, BFSI, and retail are gaining traction over generic platforms.

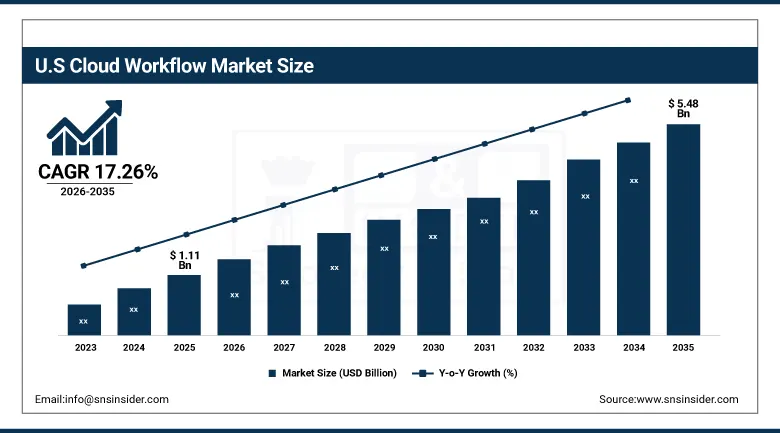

The U.S. Cloud Workflow Market Outlook

The U.S. Cloud Workflow Market was valued at approximately USD 1.11 Billion in 2025. It is expected to reach approximately USD 5.48 Billion by 2035, growing at a CAGR of approximately 17.26%.

Cloud workflow management solutions have been embraced by companies in an effort to increase efficiency, promote collaboration, and guarantee adherence to regulation. The USA is marked by strong IT infrastructures, a high degree of adoption of cloud-based technologies, and investments in AI-driven automation. The BFSI, healthcare, retail, and IT sectors are among the largest users of these solutions that allow optimizing processes. Leading technologies such as Microsoft Power Automate, ServiceNow, and Salesforce have their headquarters in the USA, thus confirming its position as the place of cloud workflow innovations. Increasing popularity of remote work continues boosting demand.

In February 2024, MPEX Solutions released an upgraded HR Management Suite with real-time workflow automation and cloud-based payroll integration. This upgrade reflects growing enterprise expectations for cloud workflow platforms to combine process automation with core HR functions.

Cloud Workflow Market Segment Analysis

This section examines performance across each major segmentation dimension covered in this report.

-

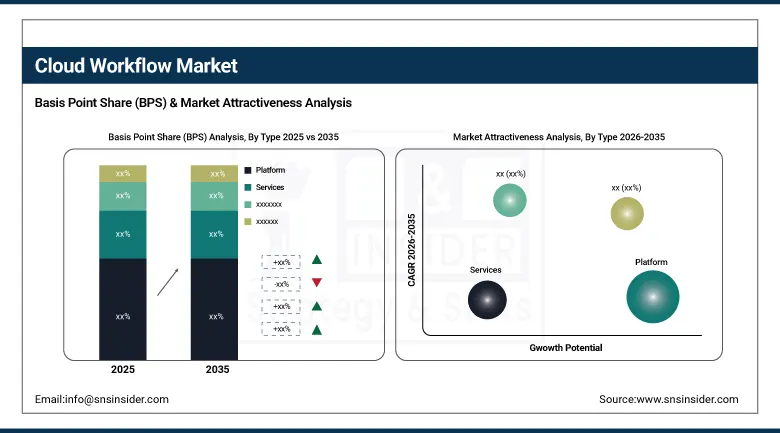

By Type, the Platform segment dominated the cloud workflow market with approximately 61.57% share in 2025. The Services segment is growing fastest, at a CAGR of 18.42%.

-

By Enterprise Size, the Large Enterprises segment dominated the cloud workflow market with approximately 57.42% share in 2025. The SMEs segment is growing fastest, at a CAGR of 19.93%.

-

By Applications, the Sales and Marketing segment dominated the cloud workflow market with approximately 19.81% share in 2025. The Customer Support segment is growing fastest, at a CAGR of 18.98%.

-

By Vertical, the BFSI segment dominated the cloud workflow market with approximately 25.80% share in 2025. The Healthcare segment is growing fastest, at a CAGR of 20.19%.

By Type, platforms dominate, services grow fastest

The revenue contribution from the Platform segment stood at around 61.57% in 2025, fueled by increasing demand for no-code or low-code platforms and workflow automation. Companies such as Microsoft (Power Automate), ServiceNow, and IBM Cloud Pak for Business Automation have taken leadership positions in the platform innovation space with features like artificial intelligence for workflows. Companies looking to enhance their agility and efficiency are opting for platforms-based cloud workflow solutions for enterprise automation. With the help of platform-based cloud solutions, businesses need not rely on custom development and can deploy applications quickly. With continued innovations in AI-enabled platforms, this segment will remain dominant.

With an anticipated highest CAGR of 18.42%, the Services segment is predicted to dominate the global cloud workflow market during the forecast period. Increasing traction for cloud consulting services, implementation, and managed services fuel this fast growth. Service providers of cloud workflow services, which include companies such as AWS, Oracle, and IBM, have upgraded their cloud workflow service offerings to make automation integration easy.

By Enterprise Size, large enterprises dominate, SMEs grow fastest

Large enterprises account for the highest market share of about 57.42% in 2025. Physical business process automation remains key for large enterprises to automate their work processes and ensure optimal efficiency. ServiceNow keeps on releasing new AI-based tools for workflow automation, and Microsoft is continually improving its Power Automate tool for large enterprises. As more large enterprises switch to cloud-based workflows to transform digitally, this category still earns high revenues.

The segment of SMEs records the highest CAGR of 19.93% due to the growing use of inexpensive cloud workflow software. Small and medium enterprises are adopting the cloud-based workflow automation to help automate processes and reduce operational costs. Providers such as Zoho, Monday.com, and Asana cater to this category with intuitive workflow automation tools that are enabled with AI functionalities. The addition of automation capability in Google Workspace by Google has helped SMEs adopt automation tools.

By Applications, sales and marketing dominate, customer support grows fastest

The Sales & Marketing application segment accounted for the largest revenue share of about 19.81% in 2025. The growing adoption of cloud-based automation software for lead management, customer engagement, and campaigns drives this trend. Salesforce and HubSpot have been implementing AI-enabled workflow software solutions in order to enhance their marketing automation and sales pipeline applications. Adobe included advanced AI-enabled analytics features to its Adobe Experience Cloud in order to enhance workflow effectiveness. Cloud-based workflow systems enable organizations to speed up sales work process, enhance productivity, and marketing strategy based on data.

The Customer Support application category will be witnessing the fastest CAGR of 18.98% during the forecast period. The growing requirement for AI-powered chatbots, automated ticketing solutions, and cloud help desk drives this fast-growing category. Zendesk and Freshdesk integrated their cloud workflow platform with AI automation in order to speed up the reaction time and customer interaction. AI-enabled case resolutions in Microsoft's Dynamics 365 Customer Service solution allows significantly streamlining support workflows. With the continuously increasing investments in customer experience, this application category will keep growing fast.

By Vertical, BFSI dominates, healthcare grows fastest

The BFSI vertical has accounted for approximately 25.80% of cloud workflow market share in 2025. The increasing usage of cloud-based automation to enhance operational efficiency, manage risks, and comply with regulations fuels the market share of this vertical. The financial institutions use workflow automation to improve the process of customer onboarding, identify frauds, and digitize banking processes. IBM’s Cloud Pak for Business Automation increases efficiency of the banking processes, whereas Salesforce Financial Services Cloud upgrades enable customer interactions.

The Healthcare vertical is estimated to witness the highest CAGR of 20.19% during the forecast period. The increasing adoption of the automated workflows in patient management, telemedicine, and regulatory compliance boosts the market growth of this vertical. The cloud workflow solution will facilitate the integration of electronic health records and cut down administrative expenses within the healthcare system. Microsoft has introduced AI-based workflow automation in its Cloud for Healthcare, and Oracle has launched advanced EHR analytics based on the cloud.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

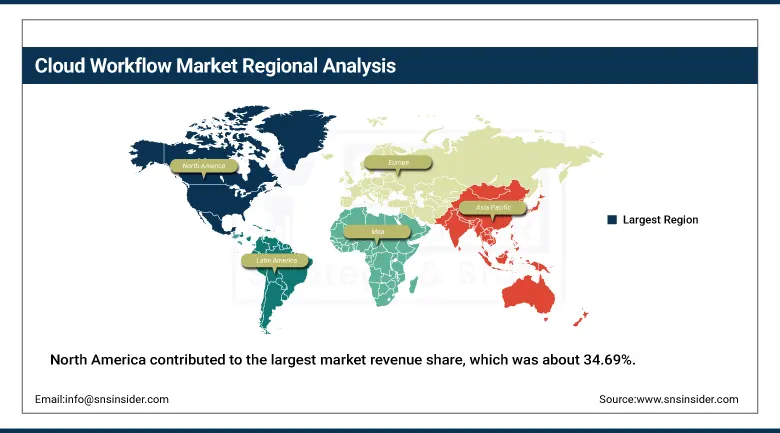

North America Cloud Workflow Market Insights

North America contributed to the largest market revenue share, which was about 34.69%. All of these are attributed to high adoption of cloud services, strong IT infrastructure, and increasing digital transformation. Enterprise behemoths such as Microsoft, IBM, and ServiceNow are still making heavy investments in cloud workflow solutions. ServiceNow developed its AI-enabled cloud workflow solutions and Microsoft launched Power Automate, an intelligent automation feature in its Power Automate service.

The U.S. generates around 82.5% of the revenue in North America. The presence of vendors of cloud workflow platforms in the region is contributing immensely towards its leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cloud Workflow Market Insights

Europe is a significant player in cloud workflow as it offers digitization and high compliance levels. Germany is the leader in the region due to its strong investments in industrial and financial digitization. France and UK offer good demand in cloud workflow due to the growth in enterprise and IT services.

Germany takes 24.6% share of the revenue in Europe. The compliance standards of GDPR continue to drive companies towards adopting cloud-based workflow management.

Asia Pacific Cloud Workflow Market Insights

The Asia Pacific region is witnessing the highest growth rate among all regions in the world, with an estimated CAGR of about 21.80%. The factors responsible for this high growth rate include increasing adoption of clouds, digital transformation plans by governments, and thriving IT industry. The countries that will contribute to high demand in the cloud workflow market are China, India, and Japan. These countries are contributing to the growth in the e-commerce, BFSI, and manufacturing industry.

China represents around 40.6% share of the regional market revenue. All these industries are utilizing cloud workflow solutions for increasing their operational flexibility and reducing costs. As digital transformation continues in this region, it is expected that such growth pattern would sustain in future.

MEA & Latin America Cloud Workflow Market Insights

The UAE ranks first among MEA revenues accounting for roughly 22.8%. Increasing enterprise digitization along with increasing use of cloud computing to automate businesses explains such leadership. Saudi Arabia also increases its infrastructure of digital economy through digital transformations under Vision 2030.

Brazil ranks first in Latin American revenues accounting for 43.8%. Expansion of digital banks, digital commerce, and enterprise IT usage all explain such demand for cloud workflows. Mexico and Argentina provide secondary demand through their enterprise IT markets expansion.

Market Dynamics

Growth Drivers: Increasing adoption of cloud-based automation enhancing business efficiency

Adoption of cloud-based workflow solution is becoming more common due to the rise in demand for automation and digital transformation among the different industry sectors. Automation using cloud computing technology is becoming popular as it helps to increase efficiency in processes while reducing the need for human intervention. Factors such as real-time processing of data, enterprise application integration, and management of remote workers have been responsible for increasing deployment. The cloud workflow market is expected to keep growing as businesses adopt AI-driven automation and intelligent workflow technologies, especially in the IT, BFSI, healthcare, and retail sectors.

Remote working has transformed the needs of enterprises when it comes to workflow processes and the deployment of cloud solutions is expected to continue growing. Companies adopting cloud workflow solutions will be better placed to adapt to changes in market needs. The adoption of digital transformation continues to grow worldwide and hence the driver is expected to maintain its strength during the forecast period.

Restraints: Data security and privacy concerns limiting adoption in regulated industries

The problem of data security and privacy continues to act as an essential constraint in the expansion of cloud workflow management. Some of the industries that require strict compliance with regulations include BFSI and healthcare. Such organizations tend to be cautious about moving their confidential information to the cloud due to potential threats like cyber-attacks and unapproved accesses.

The issue of fear of third-party accesses and breaches leads to slower adaptation by a number of firms when implementing cloud workflow systems. Lack of data governance policies and frameworks continues to act as one of the major reasons why such implementations are difficult.

Opportunities: AI and machine learning integration creating new growth prospects

The use of AI and machine learning in workflow systems is a massive growth opportunity. The AI workflow system is characterized by predictive analytics, intelligent decision-making, and optimization of processes. The insights from AI allow companies to become more efficient and reduce errors while accomplishing tasks quickly.

For industry leaders to retain their competitive edge, it is important for them to invest in AI-based cloud workflow systems that will allow for intelligent automation based on customers. With continuous advancement in AI and ML technology, innovation in cloud workflow automation will only continue to grow.

Recent Developments:

-

2024: MPEX Solutions released an upgraded HR Management Suite in February 2024, featuring real-time workflow automation and cloud-based payroll integration.

-

2024: TALOS introduced an AI-driven workforce scheduling system in January 2024, designed to optimize labor management and reduce compliance risks.

-

2025: ServiceNow introduced AI-powered workflow automation tools to enhance business process efficiencies, including new machine learning features for predictive task routing and intelligent case resolution.

Cloud Workflow Market Key Players are:

These vendors span enterprise automation platform leaders, HR workflow specialists, and cloud service integration providers.

-

TALOS Workforce Solutions

-

Verint Systems Inc.

-

MPEX Solutions

-

Ascentis Corporation

-

Synel

-

SAP SE

-

WorkForce Software, LLC

-

The Hackett Group, Inc.

-

IBM Corporation

-

Workday, Inc.

-

Amdocs

-

Ericsson

-

Huawei Technologies

-

Microsoft Corporation

-

ServiceNow, Inc.

-

Salesforce, Inc.

-

Amazon Web Services (AWS)

-

Google LLC

-

Oracle Corporation

-

Zoho Corporation

Cloud Workflow Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.74 Billion |

| Market Size by 2035 | USD 24.50 Billion |

| CAGR | CAGR of 17.85% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Platform, Services) • By Applications (Human Resource, Sales and Marketing, Accounting and Finance, Customer Support, Procurement and Supply Chain, Operations, Others) • By Enterprise Size (SMEs, Large Enterprises) • By Vertical (BFSI, IT & Telecom, Retail and E-commerce, Healthcare, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | TALOS Workforce Solutions, Verint Systems Inc., MPEX Solutions, Ascentis Corporation, Synel, SAP SE, WorkForce Software, LLC, The Hackett Group, Inc., IBM Corporation, Workday, Inc., Amdocs, Ericsson, Huawei Technologies, Microsoft Corporation, ServiceNow, Inc., Salesforce, Inc., Amazon Web Services (AWS), Google LLC, Oracle Corporation, and Zoho Corporation. |

Frequently Asked Questions

The Platform segment dominated with approximately 61.57% share in 2025. The Services segment is growing fastest at a CAGR of 18.42%.

The Cloud Workflow Market is expected to grow at a CAGR of 17.85% from 2026 to 2035.

North America dominated the Cloud Workflow Market with approximately 34.69% revenue share in 2025. Asia Pacific is the fastest-growing region at a CAGR of approximately 21.80%.

Rising adoption of AI-powered workflow automation, cloud digitalization, and enterprise demand for operational efficiency are the primary growth factors.

The Cloud Workflow Market was valued at USD 4.74 Billion in 2025.

Get in Touch