Cognitive Media Market Report Scope & Overview:

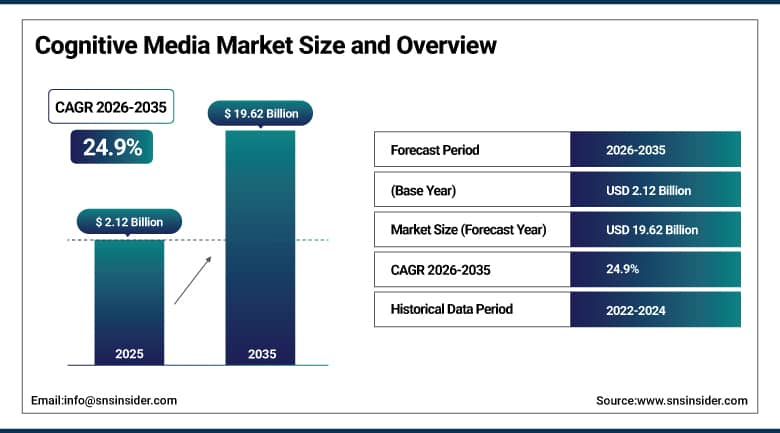

The Cognitive Media Market was valued at USD 2.12 Billion in 2025 and is expected to reach USD 19.62 Billion by 2035, growing at a CAGR of 24.9% from 2026–2035.

The cognitive media is the use of AI technologies such as natural language processing, machine learning and deep learning in the context of content creation, curation and personalization in media. The implementation of these solutions leads to automated content tagging, better content discovery and improved engagement through broadcasting, streaming and digital publishing. With media companies having larger collections of media content and increasing demands for content personalization, cognitive media technologies have progressed from being an experiment to an important part of the infrastructure used by media companies. Media large companies continue leading in the implementation of these technologies because of large technology budgets and existing digital infrastructures, but small and medium-sized media organizations also begin implementing cognitive media technologies in the form of subscription-based services offered by cloud providers.

It was found that AI auto-tagging significantly changes content workflows and increases the efficiency of media companies: auto-tagging helps to reduce manual tagging by 80%, increases the accuracy of metadata by 60%, reduces the cost of related work by 50%, increases the speed of searching content by 70% and allows to triple the number of scalable content.

Market Size and Forecast

-

Market Size in 2026E: USD 2.65 Billion

-

Market Size by 2035: USD 19.62 Billion

-

CAGR: 24.9% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Cognitive Media Market - Request Free Sample Report

Cognitive Media Market Trends

-

Media and broadcasting organizations are increasingly integrating generative AI capabilities directly into content production workflows, extending automation beyond tagging and classification into content creation itself.

-

Demand for multilingual and real-time content processing is expanding as media platforms pursue global audience reach, driving adoption of AI-powered translation, transcription, and localization tools.

-

Recommendation and personalization engines are becoming increasingly sophisticated, incorporating real-time behavioral data to deliver more precisely targeted content and advertising experiences.

-

Regulatory frameworks including the European Union's AI Act and existing data protection legislation are prompting media organizations to invest in AI governance and content compliance infrastructure.

-

Cloud-based, subscription-priced cognitive media platforms are expanding adoption among small and medium-sized media organizations that previously lacked the resources to deploy enterprise-grade AI tools.

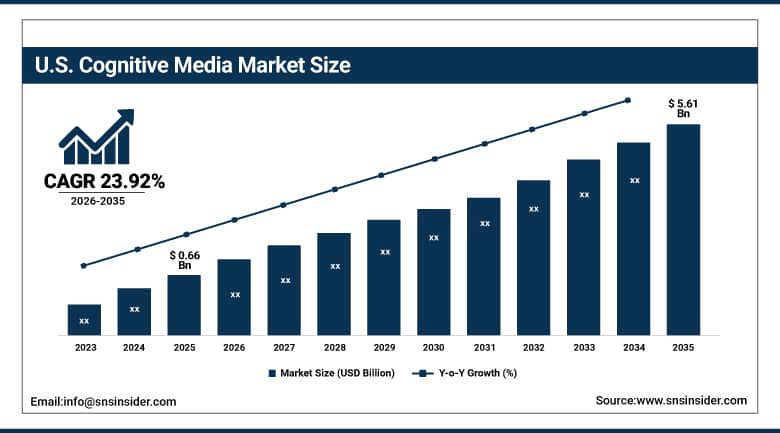

U.S. Cognitive Media Market Outlook

The U.S. Cognitive Media Market was valued at approximately USD 0.66 Billion in 2025 and is expected to reach approximately USD 5.61 Billion by 2035, growing at a CAGR of approximately 23.92%.

The United States holds an important position in the use of cognitive media, driven by enterprise-level interest in AI technologies for media, broadcasting, and over-the-top media platforms. The developed digital infrastructure, presence of technology giants such as IBM, Microsoft, and Google, as well as early investment in research and development of artificial intelligence technologies help to keep the leading position of the country in the cognitive media market. High level of consumption of media content, personalized content platforms, and cloud computing deployment infrastructure contribute to ongoing innovation and demand for these products in the national market.

In May 2024, Adobe and IBM extended the technology partnership by incorporating IBM's watsonx AI and data platform into Adobe Experience Platform for predictive machine learning models and improved content personalization. It exemplifies the increasing tendency towards deep integration of media technologies platforms and AI infrastructure in the industry that allows delivering more precisely targeted content.

Cognitive Media Market Segment Analysis

-

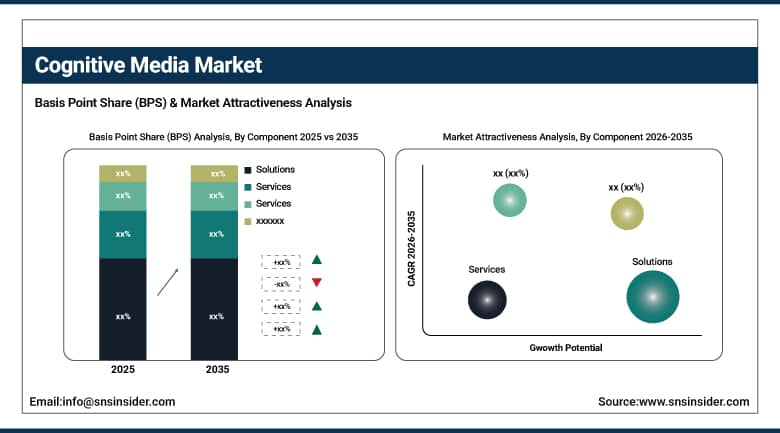

By Component, the Solutions segment dominated the Cognitive Media Market with a 69.48% revenue share in 2025, while the Services segment is the fastest growing with a CAGR of approximately 25.89%.

-

By Organization Size, Large Enterprises dominated the Cognitive Media Market with a 62.70% revenue share in 2025, while SMEs are the fastest growing segment with a CAGR of approximately 25.75%.

-

By Technology, the Machine Learning and Deep Learning segment dominated the Cognitive Media Market with a 35.92% revenue share in 2025, while the Natural Language Processing segment is the fastest growing with a CAGR of approximately 24.40%.

-

By Application, the Content Management segment dominated the Cognitive Media Market with a 34.40% revenue share in 2025, while the Recommendation and Personalization segment is the fastest growing with a CAGR of approximately 24.89%.

By Component, solutions maintain market leadership, services demonstrate the fastest growth

Solutions were responsible for approximately 69.48% of the overall market in 2025, owing to the high demand for artificial intelligence-driven content management solutions, recommendation systems, and analytics dashboarding solutions. Technology leaders like IBM and Microsoft have rolled out end-to-end cognitive media solutions encompassing voice to text solutions, video indexing, and visual recognition capabilities, with IBM Watson Media being a frontrunner when it comes to cognitive video solutions.

Services were anticipated to be the fastest-growing segment during the forecast period, recording a CAGR of about 25.89%, fueled by increasing demand for consulting and integration services for implementing cognitive media solutions. The managed services are in higher demand from smaller and mid-size media organizations, and players like Accenture and Cognizant are extending their service portfolio for cognitive media.

By Organization Size, large enterprises lead adoption, SMEs register the strongest growth

Large enterprises contributed the most market revenue, holding 62.70% of total revenues in 2025 due to the ability of large enterprises to finance the adoption of advanced cognitive media platforms based on AI technology. Large enterprises still make considerable investments in automated content creation, customer analytics, and intelligent advertising. Companies such as Amazon and Google are making progress in adopting cognitive media solutions in their media sectors.

Small and medium enterprises are the fastest-growing segment in terms of organization size and will have the highest CAGR of about 25.75%. The reason for this growth rate is the cost-effectiveness of cloud-based cognitive media solutions for SMEs along with increasing demand for personalized digital content. Some of the SMEs which offer cognitive media tools as a service are Synthesia and Veritone.

By Technology, machine learning and deep learning lead current adoption, NLP shows the fastest growth

Machine learning and deep learning technologies led the market in 2025, accounting for 35.92% of revenue, underpinning critical cognitive media capabilities including predictive analytics, object detection, and automated video editing. Leading technology companies, including NVIDIA and Google, have optimized their machine learning frameworks specifically for media applications, including TensorFlow releases tailored for video analytics.

Natural language processing is projected to register the fastest growth among technology segments, at a CAGR of approximately 24.40%, driven by its central role in automated content creation, sentiment analysis, and multilingual media accessibility. NLP technologies facilitate voice-to-text translation and automated script generation, and companies including OpenAI have introduced advanced NLP models supporting multilingual media content creation, expanding digital storytelling capabilities worldwide.

By Application, content management leads current demand, recommendation and personalization shows the fastest growth

Content management represented the biggest portion of the application segment, accounting for 34.40% of the market's revenue in 2025, due to high demands for intelligent tagging, classification, and archiving of large collections of media. The development of AI-based software, such as Adobe Experience Manager, allows publishing and broadcasting companies to efficiently handle large amounts of content while keeping its discoverability, compliance, and smooth production process.

The recommendation and personalization application segment is forecasted to grow with the highest compound annual growth rate of about 24.89%, driven by the demand for personalized experiences from consumers by media companies. Amazon and Netflix developed AI-based recommendations engines that adapt content based on the preferences of the viewer, while Jivox and Revcontent developed AI-based personalization within digital advertising.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.0% |

|

Europe |

Germany |

24.0% |

|

Asia Pacific |

China |

39.0% |

|

Middle East & Africa |

UAE |

27.0% |

|

Latin America |

Brazil |

36.0% |

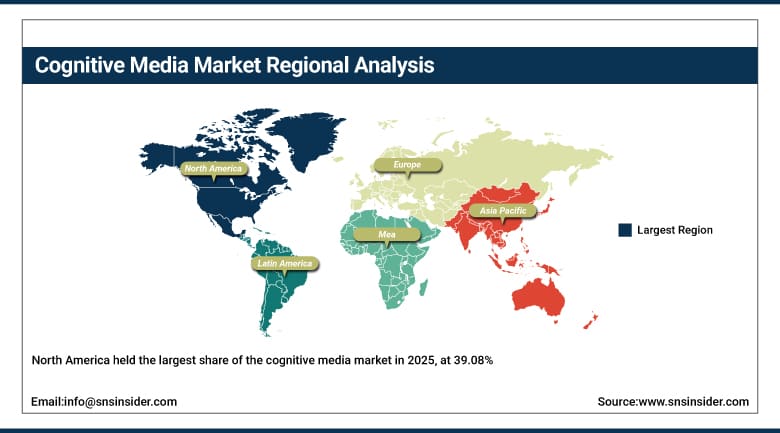

North America Cognitive Media Market Insights

North America held the largest share of the cognitive media market in 2025, at 39.08%, supported by early adoption of machine learning and artificial intelligence technologies, an established digital ecosystem, and a strong concentration of leading global technology companies within the region. Investment in cognitive content generation, broadcasting, and real-time analytics continues to expand across the region's media sector.

The United States leads the North American market, driven by a robust innovation ecosystem, a substantial media and entertainment industry, and the presence of major technology companies including IBM, Google, and Microsoft, all of which continue to lead AI adoption within media production and distribution processes. Canada contributes a smaller but consistent share of regional demand, supported by its own growing media technology sector.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Cognitive Media Market Insights

Asia Pacific is projected to register the fastest regional growth rate, at a CAGR of approximately 26.14% through the forecast period, driven by increasing smartphone penetration, expanding online video consumption, and accelerating investment in cognitive technology across the region. China, Japan, and India are leading adoption of artificial intelligence within entertainment, advertising, and social media applications.

China leads the regional market, supported by its extensive digital user base, government-sponsored artificial intelligence initiatives, and substantial investment by leading technology companies, including Tencent and Alibaba, in cognitive media applications. This combination of scale and sustained technology investment continues to reinforce the region's leading growth trajectory.

Europe Cognitive Media Market Insights

Europe is showing signs of consistent growth in terms of the use of cognitive media due to rising needs for automated content management, language capability, and compliance monitoring requirements. The support from regulations for innovations in AI, along with an increasing concern for responsible digital transformation, keeps fueling the growth of the market in Europe.

The German market stands out in the European market due to its strong industrial capability, investment in innovation of media technology, and efforts towards AI transformation in publishing and broadcasting sectors. This makes Germany one of the leading markets for cognitive media adoption in Europe.

MEA & Latin America Cognitive Media Market Insights

The Middle East and Africa are experiencing steady, encouraging growth in cognitive media adoption, driven primarily by government-initiated digital transformation programs, increasing adoption of artificial intelligence within media production, and the proliferation of local streaming services. These developments continue to reshape content distribution and audience engagement across emerging digital economies within the region.

Latin America is following a similar growth trajectory, supported by expanding digital media consumption and increasing enterprise investment in AI-powered content platforms. While both regions remain smaller markets relative to North America, Europe, and Asia Pacific, sustained investment in digital transformation initiatives is expected to support continued market development throughout the forecast period.

Market Dynamics

Growth Drivers: Increasing AI and machine learning integration enhances automation and personalization

The principal driver of cognitive media market growth is the increasing use of artificial intelligence and machine learning technologies for content automation, recommendation engine enhancement, and user interaction optimization. These technologies enable media providers to deliver more personalized experiences while streamlining content production and distribution workflows. Leading cognitive media companies, including IBM, Google, and Adobe, continue to invest substantially in AI tools designed to optimize media performance and monetization.

These sustained technology partnerships and investments reflect the broader shift toward automated content intelligence and data-driven storytelling across the media industry. As media organizations face increasing pressure to deliver personalized content at scale while managing growing content libraries, continued investment in cognitive media technology is expected to sustain market growth throughout the forecast period.

Restraints: High implementation costs and integration complexity limit broader adoption

A significant constraint on cognitive media market growth is the cost associated with implementing cognitive technologies and the complexity of integrating these systems with existing infrastructure. Small and medium-sized media companies frequently lack the financial and technical resources required to deploy sophisticated cognitive media solutions at scale.

The need for specialized technical expertise to operate and maintain these systems adds further operational burden, particularly for organizations with limited internal IT capacity. These combined factors can result in slower adoption rates and reduced return on investment, particularly within regions characterized by less developed digital infrastructure.

Opportunities: Multilingual and real-time content processing present substantial growth potential

Rising demand for real-time, multilingual content processing capable of reaching diverse global audiences represents a substantial growth opportunity within the cognitive media market. As media content becomes increasingly internationalized, cognitive solutions offering instant language translation, voice recognition, and sentiment analysis are experiencing growing demand across global digital platforms.

Companies including Google and Microsoft have introduced multilingual AI tools specifically designed for media applications, while AI-powered transcription services are gaining broader adoption in live broadcasting and content repurposing. As media organizations continue expanding their reach into international markets, demand for cognitive media solutions capable of supporting multilingual, real-time content processing is expected to sustain growth throughout the forecast period.

Recent Developments:

-

2024: In May 2024, Salesforce launched Einstein Copilot for Marketers and Merchants, enhancing AI-driven personalization and automation by leveraging real-time customer data to streamline content creation and campaign management.

-

2024: In May 2024, Adobe and IBM expanded their technology partnership, integrating IBM's watsonx AI and data platform into Adobe Experience Platform to support predictive machine learning models and enhanced content personalization.

-

2024: In December 2024, Google announced Veo, a generative AI video model capable of producing high-definition 1080p video from text or image inputs, accessible through Google's Vertex AI platform and incorporating digital watermarking through DeepMind's SynthID technology.

Cognitive Media Market Key Players

-

Microsoft Corporation

-

Google LLC

-

Amazon Web Services, Inc.

-

Adobe Inc.

-

IBM Corporation

-

NVIDIA Corporation

-

Salesforce, Inc.

-

Baidu, Inc.

-

Crimson Hexagon (Brandwatch)

-

Veritone, Inc.

-

Accenture plc

-

Cognizant Technology Solutions Corp.

-

OpenAI, Inc.

-

Synthesia Limited

-

Alibaba Group Holding Limited

-

Tencent Holdings Limited

-

Meta Platforms, Inc.

-

SAP SE

-

Oracle Corporation

-

Netflix, Inc.

Cognitive Media Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.12 Billion |

| Market Size by 2035 | USD 19.62 Billion |

| CAGR | CAGR of 24.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solutions, Services), Organization Size (Large Enterprises, SMEs) • by Technology (Deep Learning and Machine Learning, Natural Language Processing) • by Application (Content Management, Network Optimization, Recommendation and Personalization, Customer Retention, Predictive Analysis, Security Management, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Microsoft Corporation, Google LLC, Amazon Web Services, Inc., Adobe Inc, IBM Corporation, NVIDIA Corporation, Salesforce, Inc., Baidu, Inc., Crimson Hexagon (Brandwatch), Veritone, Inc., Accenture plc, Cognizant Technology Solutions Corp., OpenAI, Inc., Synthesia Limited, Alibaba Group Holding Limited, Tencent Holdings Limited, Meta Platforms, Inc., SAP SE, Oracle Corporation, Netflix, Inc. |

Frequently Asked Questions

Solutions dominated with a 69.48% revenue share in 2024, while Services is the fastest growing segment with a CAGR of approximately 25.89%.

North America dominated the Cognitive Media Market in 2025 with a 39.08% market share, while Asia Pacific is the fastest-growing region.

North America dominated the Cognitive Media Market in 2025 with a 39.08% market share, while Asia Pacific is the fastest-growing region.

The Cognitive Media Market was valued at USD 2.12 Billion in 2025.

The Cognitive Media Market is expected to grow at a CAGR of 24.9% from 2026 to 2035.

Increasing integration of artificial intelligence and machine learning technologies for content automation, recommendation engine enhancement, and personalized user experiences across media platforms.

Get in Touch