Commercial Security System Market Report Scope & Overview:

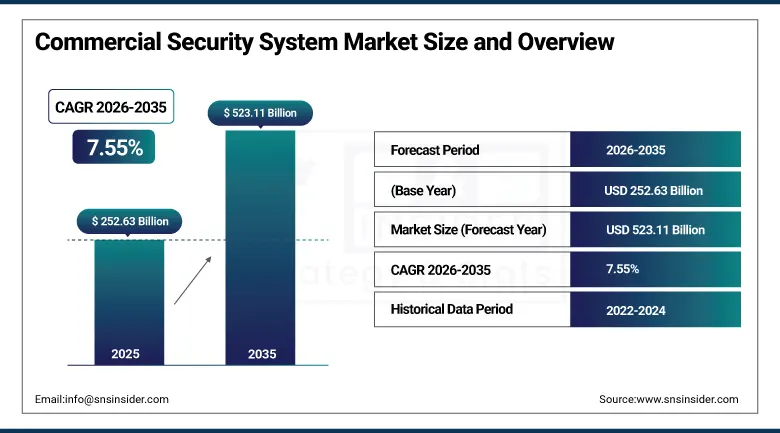

The Commercial Security System Market was valued at USD 252.63 Billion in 2025 and is expected to reach USD 523.11 Billion by 2035, growing at a CAGR of 7.55% from 2026 to 2035.

The global market of commercial security systems is showing strong growth owing to the increasing cases of thefts, security threats, unauthorized access, compliance regulations, and IoT and AI based smart security deployment as well as investments in the protection of critical infrastructure, thereby generating sustainable demand across all commercial segments. The number of installations of commercial security systems is expected to surpass 85 million business premises by 2025. With the help of AI technology, false alarms have decreased by 40%, 60% of new installations in commercial sectors are using cloud-based security systems, and 55% of installations use wireless IoT devices.

By 2025, investments in commercially-focused AI security are expected to increase by more than 18% due to the requirement for real-time data analytics and automatic response capabilities that will turn security from a reactive practice into one where potential threats can be prevented. The rationale behind such investments is that there are benefits to commercially-based AI security systems apart from loss prevention, including analytics related to occupancy rates, operational efficiency, and regulatory compliance.

Commercial Security System Market Size and Forecast

-

Market Size in 2026E: USD 271.70 Billion

-

Market Size by 2035: USD 523.11 Billion

-

CAGR: 7.55% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Commercial Security System Market - Request Free Sample Report

Commercial Security System Market Trends

-

AI-powered security analytics are improving threat detection accuracy, reducing false alarms, and accelerating incident response workflows.

-

Cloud-based security management platforms are gaining adoption through centralized monitoring, remote access, and subscription-based deployment models.

-

Physical security and cybersecurity convergence is driving demand for integrated protection across connected security infrastructure.

-

Mobile credentials and biometric authentication technologies are replacing traditional access systems with more secure identity management.

-

Predictive analytics solutions are enabling proactive risk assessment through behavioral monitoring and data-driven threat forecasting.

The U.S. Commercial Security System Market Outlook

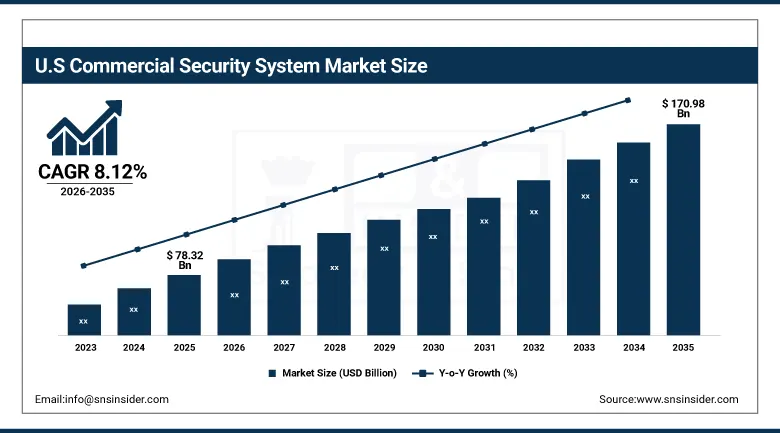

The U.S. Commercial Security System Market was valued at USD 78.32 Billion in 2025 and is expected to reach USD 170.98 Billion by 2035, growing at a CAGR of 8.12%.

In terms of commercial security systems markets, the USA is currently the largest because it faces high incidences of crime within cities, stringent laws on fire and life safety such as NFPA 72 fire alarm systems and UL testing of security hardware, significant insurance rate reductions for property under security, rapid adoption of smart buildings that include the integration of security systems with BMS, HVAC, and access control, and heavy investments in corporate campuses, banks, healthcare centers, retail shops, and infrastructures. Investments in AI-powered security are growing at above-market rates as the 18% investment growth projection for 2025 reflects commercial operator recognition of AI security analytics’ operational value beyond traditional loss prevention.

In 2024, Motorola Solutions acquired Avigilon, extending its AI-powered video analytics and cloud-based security management portfolio to enable enterprise customers to unify access control, video surveillance, and incident management across large multi-site corporate campuses and retail networks within a single integrated security operations platform. The acquisition reflects the commercial strategy of major security platform vendors toward end-to-end integrated security ecosystems that sustain long-term enterprise customer relationships beyond one-time hardware procurement transactions.

Commercial Security System Market Segment Analysis

-

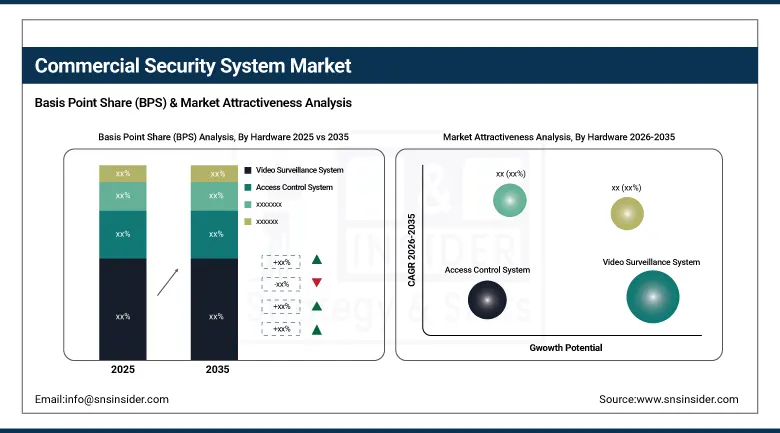

By Hardware, the video surveillance system segment dominated the market with approximately 38.65% share in 2025, while the access control system segment is the fastest growing at approximately 8.95% CAGR.

-

By Software, the video surveillance software segment dominated the market with approximately 41.22% share in 2025, while the access control software segment is the fastest growing at approximately 9.45% CAGR.

-

By Vertical, the commercial corporate & enterprise segment dominated the market with approximately 28.50% share in 2025, while the healthcare segment is the fastest growing at approximately 9.15% CAGR.

By Hardware, video surveillance dominates, access control grows fastest

Video surveillance systems retained the dominant hardware position with approximately 38.65% of the commercial security system market in 2025. IP camera infrastructure's role as the foundational visual security layer across all commercial facility types, whose continuous recording, remote monitoring, and evidence documentation functions create the primary security hardware investment in virtually every commercial security programme, sustains video surveillance's market leadership. AI-analytics-ready IP camera deployment growth, whose edge computing capability enables on-camera object detection, people counting, and behavioral analysis without central server dependency, creates above-commodity camera system specification that sustains above-average revenue per deployed camera relative to legacy analogue systems.

Access control systems are the fastest growing hardware category at approximately 8.95% CAGR because the systematic transition from mechanical lock-and-key credential management to electronic, biometric, and mobile-based access control creates new installation procurement in existing facilities undergoing security upgrade as well as standard specification in new commercial construction. Over 60% of new commercial construction projects integrating electronic access control demonstrates the breadth of access control system adoption motivation beyond voluntary security enhancement toward standard building specification. RFID credential, mobile access using BLE-connected smartphones, and facial recognition terminal deployment collectively create procurement across the full access control product spectrum from reader hardware through controller infrastructure and credential management software.

By Software, video surveillance software dominates, access control software grows fastest

Video surveillance software retained the dominant software position with approximately 41.22% of the commercial security system market in 2025. Video management system software's role as the operational platform for multi-camera security operations whose recording management, real-time monitoring, analytics integration, and incident review functions create essential operational infrastructure for organisations deploying more than a handful of cameras. Each enterprise campus that deploys hundreds to thousands of IP cameras creates VMS software procurement whose license value scales with camera count and analytics feature set. Cloud-based VMS adoption's growth, over 60% of new commercial installations adopting cloud management, creates recurring SaaS revenue streams that sustain above-hardware revenue growth for software vendors whose subscription economics improve upon one-time license sales.

Access control software is the fastest growing category at approximately 9.45% CAGR because cloud-based access control management platforms’ 24% subscription growth in 2025 reflects enterprise demand for centralized user lifecycle management, integration with HR information systems for automatic account provisioning and termination, and remote administration capability that on-premise access control software cannot provide at equivalent operational convenience. Each enterprise whose distributed workforce requires access credential management across multiple geographically dispersed facilities creates cloud access control software procurement whose subscription model creates predictable operating expense aligned with headcount. Lenel OnGuard, Software House C-CURE, and Genea’s cloud access platform demonstrate the commercial breadth of enterprise access control software adoption.

By Vertical, commercial corporate dominates, healthcare grows fastest

Commercial corporate and enterprise retained the dominant vertical position with approximately 28.50% of the commercial security system market in 2025. Corporate campus and office building security investment encompasses video surveillance infrastructure for lobby, parking, and common area monitoring, access control systems for all facility entry points and sensitive zone protection, fire alarm and suppression systems for life safety compliance, and integrated security operations platforms whose complexity creates above-average per-square-meter security investment relative to simpler commercial facility types. Data center security investment within the commercial corporate vertical, whose physical security of server infrastructure creates above-average per-facility security spending driven by both insurance requirements and regulatory standards for data protection, sustains commercial corporate vertical revenue leadership.

Healthcare is the fastest growing vertical at approximately 9.15% CAGR because the combination of HIPAA security rule compliance requirements for physical access control of protected health information areas, rising workplace violence incidents in healthcare settings that are driving enhanced security investment, and the sensitivity of pharmaceutical inventory, medical device storage, and patient data systems creates the most comprehensive security compliance investment motivation of any regulated sector. Healthcare security spending growth exceeded 11% in 2025 as hospital systems implemented integrated access control for medication dispensing areas, AI video analytics for infant protection programmes, and emergency lockdown systems for active threat response capability.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Commercial Security System Market Insights

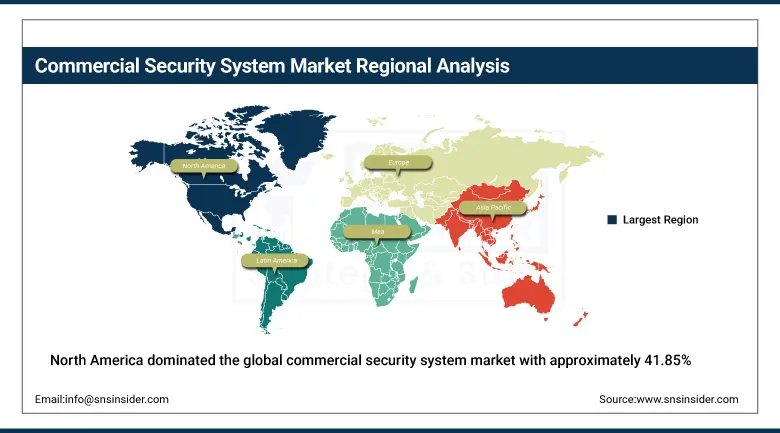

North America dominated the global commercial security system market with approximately 41.85% of revenues in 2025, driven by the large number of Fortune 500 firms, extensive critical infrastructure, strict fire and life safety regulations, and early adoption of AI-powered security technologies. The United States accounts for approximately 87.4% of North American revenues through Honeywell, Johnson Controls, ADT, Motorola Solutions, Bosch Security Systems, and Allegion's commercial operations across enterprise, retail, government, and healthcare verticals.

In terms of physical security investments within the commercial real estate industry, governmental building facilities, and the financial services industry, Canada accounts for about 12.6% of the North American revenues earned through such activities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Commercial Security System Market Insights

Europe is a compliance-driven commercial security market where GDPR's requirements for physical access control of personal data processing systems, EN 50131 alarm system standards, and national fire safety regulations create layered procurement motivation. Germany contributes about 22.3% to European earnings through industrial security investments within their manufacturing industry, adoption of access control on corporate campuses, and comprehensive physical security requirements by the financial industry. Bosch Security Systems and Axis Communications in Sweden keep Europe ahead of commercial security technology trends.

The United Kingdom, France, and the Netherlands constitute important secondary markets that offer steady above-average procurement for security compliance within the financial industry, security investment within NHS healthcare facilities, and loss prevention among retail chains in Europe. The European subsidiaries of Tyco International and Avigilon offer regional market supply within the security segments.

Asia Pacific Commercial Security System Market Insights

Asia Pacific is the fastest growing regional commercial security system market, driven by China's extraordinary commercial construction investment, India's growing corporate sector security awareness, Japan's advanced security technology adoption, South Korea's smart building integration, and Southeast Asia's rapid commercial development. China accounts for approximately 44.8% of Asia Pacific revenues through Hikvision and Dahua Technology's domestic market dominance, the government's social management video surveillance investment, and the extraordinary scale of commercial real estate development creating new facility security system procurement.

India represents the most commercially dynamic emerging market within Asia Pacific where the growing corporate sector's security awareness, the retail sector's loss prevention investment, and the government's smart city initiative creating integrated public-private security infrastructure investment create above-average commercial security system market growth from both compliance-driven and commercially motivated procurement.

MEA & Latin America Commercial Security System Market Insights

The UAE leads MEA revenues at approximately 31.2% through its smart city security infrastructure investment, luxury retail and hospitality sector's premium security adoption, and the financial district's comprehensive physical security compliance. Saudi Arabia's Vision 2030 commercial development and Neom smart city security investment add substantial Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its retail sector's loss prevention investment, corporate campus security compliance, and the financial services sector's physical security procurement. Mexico's commercial retail security and Colombia's corporate sector adoption collectively sustain regional growth through 2035.

Market Dynamics

Growth Drivers: AI-powered security analytics creating operational value beyond loss prevention and rising security threat sophistication driving comprehensive multi-layer system investment

AI-powered commercial security analytics represents the most commercially transformative current market development whose integration of intelligent threat detection, behavioral anomaly identification, and predictive risk modelling creates security system value substantially beyond conventional loss prevention ROI. Each security platform deployment whose AI analytics reduces false alarm burden by 40% while improving true threat detection creates operational efficiency value that sustains premium system specification above conventional video surveillance and access control alternatives. The 18% AI security investment growth projection for 2025 reflects commercial operator recognition that AI security creates operational intelligence assets including occupancy analytics, queue management, and operational compliance documentation that sustain ROI beyond pure security incident prevention.

Rising sophistication of commercial security threats including organized retail crime, corporate espionage, cyberattacks on connected security systems, and terrorism create multi-layer security system investment motivation that individual product category procurement cannot satisfy.

Restraints: High initial installation cost for SMEs and cybersecurity vulnerabilities in connected security systems

High upfront installation costs for comprehensive commercial security solutions involving significant capital expenditure for hardware, software, and integration create adoption barriers for small and medium-sized businesses whose security budget constraints require prioritization among multiple investment alternatives. Each SME whose total security system installation cost ranges from USD 50,000 to over USD 500,000 for comprehensive multi-layer protection creates a capital commitment that requires structured financial justification against insurance premium reduction, theft loss prevention, and regulatory compliance value that modest-scale commercial operators may not fully quantify.

IP cameras, network-connected access control systems, and cloud-connected security management platforms create network-accessible entry points whose exploitation can compromise both physical security system function and the broader enterprise network through the security system's trusted network access.

Opportunities: Smart city integration and AI-powered video analytics for operational intelligence beyond security

Smart city integration creates commercial opportunity for security system vendors whose platform capabilities extend beyond facility security into urban infrastructure management, public safety analytics, and environmental monitoring whose government and municipal procurement creates above-commercial-market revenue opportunities. Each smart city programme that integrates commercial security system infrastructure with city-wide sensor networks, traffic management, and emergency response systems creates procurement relationships whose scope substantially exceeds conventional building security system contracts. Integration with smart city platforms is expected to influence over 35% of new large-scale commercial security projects in 2025, demonstrating the commercial scale of this integration opportunity.

AI-powered video analytics for operational intelligence creates commercial opportunity for security platform vendors to expand the value proposition beyond security into operational performance measurement, customer behavior analytics for retail, occupancy management for corporate real estate, and compliance monitoring for regulated environments. Each commercial security platform that demonstrates measurable operational ROI beyond security incident prevention creates above-commodity system specification motivation that sustains premium product pricing and subscription service adoption.

Recent Developments:

-

2025: AI-powered commercial security investment is projected to grow by over 18% in 2025, driven by demand for real-time analytics and automated incident response, with over 60% of new commercial installations adopting cloud-based security management platforms.

-

2024: Motorola Solutions expanded its AI-powered video analytics and cloud security management capabilities through portfolio integration, enabling enterprise customers to unify access control, video surveillance, and incident management across multi-site corporate facilities within a single integrated security operations platform.

-

2024: Johnson Controls launched its OpenBlue Enterprise Manager platform updates, integrating AI-powered physical security analytics with building management system data to create unified operational intelligence that sustains security investment ROI beyond conventional loss prevention metrics.

Commercial Security System Market key players are:

-

Honeywell International Inc.

-

Johnson Controls International plc

-

Bosch Security Systems GmbH

-

Axis Communications AB (Canon)

-

ADT Inc.

-

Motorola Solutions Inc. (Avigilon)

-

Allegion plc

-

Hanwha Vision Co. Ltd.

-

Dahua Technology Co. Ltd.

-

Hikvision Digital Technology Co. Ltd.

-

Genetec Inc.

-

Milestone Systems A/S (Canon)

-

ASSA ABLOY AB

-

Siemens AG (Siemens Security)

-

LenelS2 (Carrier Global Corporation)

-

Identiv Inc.

-

Napco Security Technologies Inc.

-

Verkada Inc.

-

Brivo Inc.

-

Rhombus Systems

Commercial Security System Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 252.63 Billion |

| Market Size by 2035 | USD 523.11 Billion |

| CAGR | CAGR of 7.55% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Hardware (Fire Protection System, Video Surveillance System, Access Control System, Entrance Control System) • By Software (Fire Analysis, Video Surveillance Software, Access Control Software) • By Vertical (Commercial Corporate & Enterprise, Government, Banking & Finance, Industrial, Energy & Utility, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Honeywell International Inc., Johnson Controls International plc, Bosch Security Systems GmbH, Axis Communications AB (Canon), ADT Inc., Motorola Solutions Inc. (Avigilon), Allegion plc, Hanwha Vision Co. Ltd., Dahua Technology Co. Ltd., Hikvision Digital Technology Co. Ltd., Genetec Inc., Milestone Systems A/S (Canon), ASSA ABLOY AB, Siemens AG (Siemens Security), LenelS2 (Carrier Global Corporation), Identiv Inc., Napco Security Technologies Inc., Verkada Inc., Brivo Inc., Rhombus Systems |

Frequently Asked Questions

The Commercial Security System Market is expected to grow at a CAGR of 7.55% from 2026 to 2035.

The Commercial Security System Market was valued at USD 252.63 Billion in 2025.

AI-powered security analytics creating operational value beyond loss prevention including real-time threat detection, occupancy analytics, and predictive risk management.

Video Surveillance System dominated the Commercial Security System Market with approximately 38.65% share in 2025.

North America dominated the Commercial Security System Market with approximately 41.85% of revenues in 2025.

Get in Touch