Data Governance Market Report Scope & Overview:

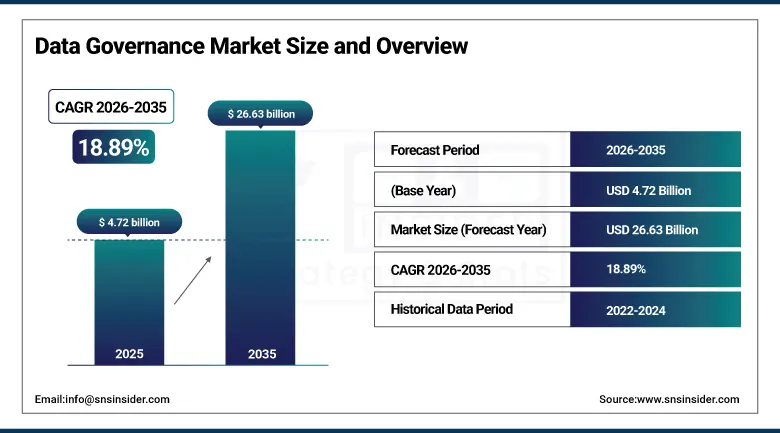

The Data Governance Market was valued at USD 4.72 billion in 2025 and is expected to reach USD 26.63 billion by 2035, growing at a CAGR of 18.89% from 2026–2035.

The global data governance market is experiencing extraordinary and accelerating growth, driven by the convergence of escalating regulatory compliance requirements that mandate formal data management programmes, exploding growth of enterprise data volumes creating existential complexity in state-of-the-art quality literally all aspects of data lineage to deliver a significant return on investment (ROI) including time saving and increased end-user productivity; and high-quality, well governed research being recognised as an essential prerequisite component across virtually all strategic AI and advanced analytics programmes organisations covering every industry need to tackle if are going to meet this strategic imperative. Over the past five years, data governance (policies, processes, standards, metrics and roles for ensuring that enterprise information can be trusted and is accessible to support business needs) has evolved from a discretionary data management best practice into an essential organisational capability: the new global privacy regulatory framework collectively created by GDPR, CCPA, HIPAA and PCI-DSS requires formal governance infrastructure to enable the data transparency, lineage documentation and retention management that they mandate. The early and most committed adopters included financial institutions, healthcare providers, and technology companies that understand data governance is the foundation of regulatory compliance and operational risk management as well as of the trusted data foundations that drive competitive AI and analytics capabilities.

it is simply a reflection of the structured factors that indicate how data governance is shifting from being an optional investment to becoming mandatory organisational infrastructure as AI adoption forces the level of quality assurance for training data to mission-critical minimums, regulatory frameworks crystallise tangible and legally enforceable obligations imposed by those who create or use data (the regulators) on organisations responsible for management, discovery and usage of such assets; and enterprises themselves discover that poor data governance in fact creates tangible operational costs measurable through events such as failure in achieving desired levels of accuracy in analytics, compliance penalties incurred due non/partial-compliance with legislation/regulations or inefficiencies introduced into analytic processes caused by systematic issues within datasets each presenting individual and aggregate ROI-optimising arguments for enterprise-wide expenditure on end-to-end governance programmes over the next five years.

Market Size and Forecast

-

Market Size in 2025: USD 4.720 Billion

-

Market Size by 2035: USD 26.631 Billion

-

CAGR: 18.89% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Data Governance Market - Request Free Sample Report

Data Governance Market Trends

-

Rapid integration of AI and machine learning into data governance platforms enabling automated discovery, classification, quality scoring, metadata management, and lineage tracking.

-

Growing adoption of active metadata management frameworks supporting dynamic, context-aware governance across interconnected enterprise data ecosystems.

-

Accelerating convergence of data governance and data catalog platforms creating unified discover-and-govern experiences for broader enterprise adoption.

-

Rising prominence of governance solutions in cloud-native and multi-cloud environments through native integration with AWS, Azure, and Google Cloud services.

-

Growing importance of data governance in AI development lifecycles supporting data quality validation, bias monitoring, lineage documentation, and consent management.

-

Expansion of domain-driven and federated governance models inspired by data mesh architectures enabling agile, decentralised governance accountability.

-

Rising adoption of data governance solutions in BFSI and healthcare sectors due to increasing regulatory scrutiny on data quality and transparency

U.S. Data Governance Market

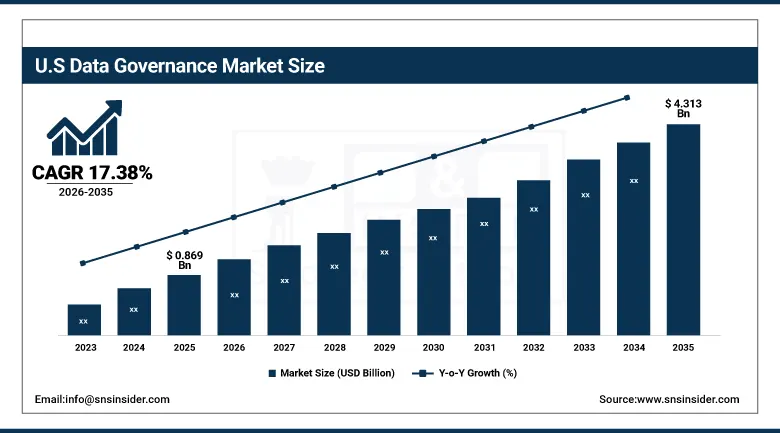

U.S. Data Governance Market was valued at USD 0.869 billion in 2025 and is expected to reach USD 4.313 billion by 2035, registering a CAGR of 17.38% during 2026–2035.

With the most advanced Digital infrastructure, the most severe combination of federal and state Data Privacy regulations including CCPA, HIPPA, and GLBA mandating formal data governance programmes across virtually every major industry segment in North America as well the deepest level of cloud computing and AI uptake driving an increasingly urgent need for comprehensive data governance investment - The United States currently dominates the Global Data Governance Market accounting for most of North America's market share. World-leading data governance platform providers in the U.S. with significant commercial operations and R&D investment-- IBM, Oracle, Informatica, Collibra and Alation -- ensures that the most advanced governance capabilities are commercially available for deployment and aggressively adopted used by the U.S. enterprise market place. In the case of the largest three U.S. enterprise vertical segments — namely, the BFSI sector, with its comprehensive model risk management requirements; healthcare sector, which has required some form of PHI governance in compliance with HIPAA; and the technology industry — these represent mandatory governance investment drivers.

The convergence of CCPA compliance mandating data inventory and subject access request capabilities, HIPAA's protected health information governance obligations, and the Federal Reserve's SR 11-7 model risk management guidance requiring data quality documentation for AI/ML models used in credit decisions is creating a multi-regulatory compliance imperative for U.S. enterprises that makes formal data governance programme investment essentially mandatory rather than optional — transforming the U.S. data governance market from a best-practices advisory category into a compliance .

Data Governance Market Segment Insights

-

Based on Component, Solutions accounted for the largest market share in 2025; Services expected to be the fastest-growing component (CAGR) as implementation complexity drives professional service demand.

-

Based on Deployment, Cloud-Based dominated with the largest and fastest-growing market share in 2025, driven by scalability and cost-effectiveness advantages over on-premises alternatives.

-

Based on Organisation Size, Large Enterprises accounted for the largest market share in 2025; SMEs expected to be the fastest-growing segment (CAGR) as cloud-delivered governance platforms democratise access.

-

Based on Industry Vertical, BFSI dominated with the largest market share in 2025; Healthcare expected to be the fastest-growing vertical (CAGR) driven by digital health data governance requirements.

Data Governance Market Segment Analysis

By Component: Solutions dominate, Services grow fastest

Solutions encompassing data governance platform software including data catalog, data quality, metadata management, master data management, and policy management capabilities retained the dominant component revenue share in 2025, reflecting the platform-centric nature of enterprise data governance programme investment. Leading governance platform vendors including Collibra, Alation, Informatica, IBM, and Microsoft Purview have established comprehensive solution portfolios that address the full governance lifecycle from data discovery and classification through quality monitoring, lineage tracking, and policy enforcement with enterprise platform licensing generating the largest recurring revenue streams in the market.

Services encompassing consulting, implementation, integration, training, and managed governance services are projected to be the fastest-growing component through 2035, due to the complex nature of enterprise data governance programme implementation across heterogeneous data environments that requires high investments in expert professional services. The increasing complexity of multi-cloud data governance, AI governance framework implementation and regulatory compliance programme design creates an ongoing need for a specialised data governance consulting capability that most enterprise data management teams are not equipped to handle themselves.

By Deployment: Cloud dominates and grows fastest

Cloud-based data governance platforms dominated the market in 2025 and are simultaneously projected to grow at the fastest deployment segment CAGR through 2035, driven by the mass migration of enterprise data to cloud platforms that makes cloud-native governance solutions the natural, low-friction implementation choice, combined with cloud governance platforms' advantages of automatic feature updates, elastic scalability, reduced infrastructure management overhead, and seamless integration with cloud data warehouse and analytics services. Leading cloud governance platforms including Alation Cloud Service, Collibra Cloud, and Microsoft Purview are capturing the majority of new enterprise governance deployment decisions as cloud-first data strategy becomes the enterprise IT default.

On-premises deployments for data governance will remain an important option for highly regulated industries faced with stringent regulations and/or companies that have extremely sensitive classified or proprietary data not permitted to run from shared cloud infrastructure. Hybrid deployments leveraging on-premises governance policy management with cloud data asset discovery and quality monitoring is the realistic architecture for large enterprises managing their legacy on-premises data assets workloads while rapidly expanding their cloud data estate sustaining hybrid deployment need throughout the forecast period.

By Organisation Size: Large Enterprises lead, SMEs grow fastest

Large Enterprises accounted for the dominant share of the Data Governance Market in 2025, driven by their extensive data ecosystems, complex regulatory compliance obligations, and increasing investments in enterprise-wide governance frameworks supporting digital transformation, cloud migration, and AI-driven analytics initiatives. Large organisations across BFSI, healthcare, telecom, and manufacturing sectors are prioritising advanced governance capabilities including metadata management, data lineage tracking, policy orchestration, and cross-border compliance management to maintain data integrity, operational transparency, and regulatory readiness across distributed global operations. The scale and complexity of enterprise data environments combined with heightened scrutiny surrounding cybersecurity, privacy, and responsible AI governance continue to strengthen adoption among large enterprises.

SMEs are projected to witness the fastest CAGR through 2035 as cloud-delivered and SaaS-based data governance platforms significantly reduce implementation complexity and upfront infrastructure costs, making enterprise-grade governance capabilities increasingly accessible to smaller organisations. Growing digitalisation among SMEs, rising dependence on cloud-native business applications, and increasing exposure to privacy regulations such as GDPR and emerging AI governance mandates are accelerating demand for scalable and automated governance solutions. Vendors are increasingly offering modular, low-code, and AI-enabled governance platforms tailored for SMEs, enabling smaller businesses to improve data quality, compliance monitoring, and operational decision-making without requiring large in-house data management teams.

By Industry Vertical: BFSI leads, Healthcare grows fastest

BFSI retained the dominant industry vertical position in the Data Governance Market in 2025, driven by financial institutions' regulatory compliance intensity encompassing data governance requirements embedded in Basel III/IV, MiFID II, GDPR financial data provisions, SR 11-7 model risk management, and stress testing regulations combined with the commercial imperative of data-driven financial product personalisation, credit risk modelling, and fraud detection that requires the highest-quality governed data foundations. Banking regulators globally are imposing increasingly specific data governance requirements on financial institutions, with data lineage documentation, data quality measurement, and critical data element management now embedded in regulatory examination processes.

Healthcare is forecasted to be the fastest growing industry vertical until till year 2035 as digital transformation of healthcare delivery creates unprecedented quantities of clones of billions of health data that require additional levels sophisticated and federated governance electronic health records, medical imaging data, genomic datasets from DNA sequencing services, and streams of remote patient monitoring data combined with obligations under HIPAA's protections for sensitive protected health information (PHI), redesigning artificial intelligence/machine learning capabilities FDA guidance in statutory oversight over AI-assisted/AI-driven medical devices related to clinical performance risk defined and regulated by the AI-based analytics platform used during use in care patterns via "digital growth" machine learning bias (ML) capability to decision slide reduction strategies the European Union's promulgation new regulation details under its ambitious European Health Data Space (EHDS) process creating a new comprehensive regulatory governance mandate for healthcare perforating parallel paths globalizing across geospatial perimeters. Clinical decision support, diagnostic imaging AI, and predictive clinical analytics are some of the top use cases driving extremely demanding and urgent in any industry vertical AI-data governance dependencies.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

40% |

|

Europe |

United Kingdom |

31% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

27% |

|

Latin America |

Brazil |

42% |

North America Data Governance Market Insights

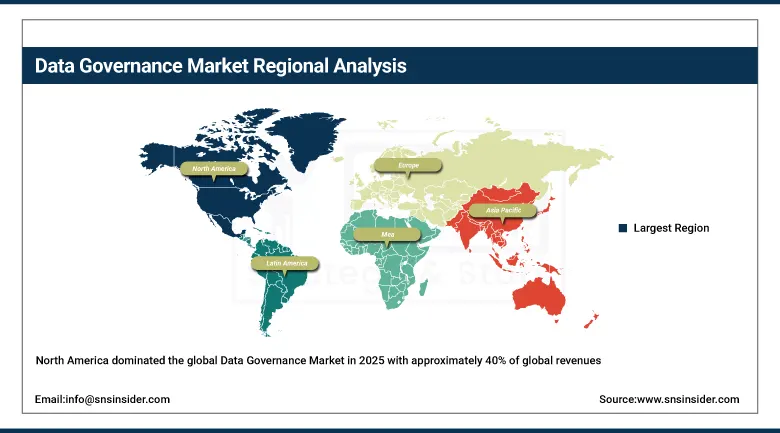

North America dominated the global Data Governance Market in 2025 with approximately 40% of global revenues, followed by United States Even more, the U.S. represents the world's most developed digital economy with its advanced broadband infrastructure and data privacy framework, as well as being home to the global leaders in enterprise cloud products and services and the commercial presence of the leading global providers of data governance platforms. The Federal Data Strategy, data transparency mandates, and corresponding growing number of civilian agencies adopting data governance frameworks are creating a public sector demand dimension to sit alongside the strong enterprise market for data governance frameworks.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Data Governance Market Insights

Asia Pacific is projected to grow at the fastest regional CAGR of 19.93% through 2035, as digital transformation continues rapidly across China, India, Japan and Southeast Asia creating new vast data volumes requiring governance accelerating cloud adoption and enhancing data privacy regulatory frameworks including PIPL in China, the DPDP Act in India, ASEAN Data Governance Framework Guidelines that generate significant compliance-driven investments mandates for governance capabilities. The vast structural demand for scaleable data governance solutions is created by growing IT expenditures and expanded digital economies throughout the region with India's IT sector managing petabytes of enterprise data on behalf of global clients.

Europe Data Governance Market Insights

Europe's data governance market is anchored by the GDPR's comprehensive data management obligations including data inventory requirements, processing purpose limitation, data minimisation, and retention management that collectively mandate formal data governance programme investment across all organisations processing EU resident data. The EU AI Act's tiered data governance requirements for high-risk AI systems, the European Health Data Space regulation, and the Data Governance Act creating frameworks for data intermediary services are collectively advancing Europe's regulatory-driven data governance investment through 2035. Germany, France, the UK, and the Netherlands are the leading European data governance markets.

Middle East & Africa and Latin America Data Governance Market Insights

MEA and Latin America are growing data governance markets, to expand for data governance, supported by rapidly evolving digital transformation, increasingly robust legal privacy regulations, and increasing enterprise awareness of data quality as a competitive differentiator. Again Brazil comes top of the table for Latin American revenues, accounting for approximately 42% of regional share with LGPD compliance obligations forcing spend on governance programmes across Brazilian enterprises. The UAE is the top country in the MEA adoption based on a mix of its existing data protection regulatory frameworks (e.g., ADGM and DIFC), government initiatives to drive Smart Dubai efforts for data governance along with large volumes of regional financial services and technology companies that are establishment enterprise-grade governance capabilities.

Market Growth Drivers:

Regulatory compliance mandates, AI data quality requirements, and cloud data complexity driving governance investment: The main structural growth drivers of the Data Governance Market are three irresistible converging forces that compound upon each other: increasing global regulatory landscape mandating formal data management and transparency programmes (exemplified by GDPR) requiring to build proper governance infrastructure; pressing need for AI adoption mandating highest-quality consistently governed data foundations in order to ensure reliable performance of AI models; and escalating complexity of multi-cloud enterprise data environment driving silos in this distributed global data landscape causing governance gaps which must be addressed all whilst ensuring automated, scalable solutions providing visibility, quality and policy enforcement across these types of architectures.

The BFSI sector's recognition — embedded in regulatory frameworks including SR 11-7 and Basel IV — that AI and ML model governance is inseparable from data governance, requiring auditable data lineage, validated training data quality, and documented data transformation histories for every model used in credit, risk, and compliance decisions, demonstrates how AI regulatory governance is becoming a powerful institutional multiplier of data governance investment, creating mandatory programme expansion from basic data inventory management to comprehensive AI-enabled data governance infrastructure across the market's largest and most compliance-intensive customer vertical through the forecast period.

Market Restraints

Implementation complexity, cultural resistance, and talent shortage limiting governance programme velocity: A major constraint on the Data Governance Market is that enterprise data governance programmes across diverse data environments of legacy on-premises databases, multiple cloud platforms, disparate application systems and unstructured data sources require substantial technology integration investment generating complexity that creates considerable time for implementation. Resistance from data owners to be bound by accountability obligations and resistance from data consumers to have governance constraints placed on their access flexibility introduce change management impediments that often stretch out the programme timelines and impact achievement of governance objectives. If firms are to be able to build and operate a governance programme, the imperative of finding experienced data governance professionals who can combine domain knowledge in data management with regulatory compliance expertise and organisational change management capability is first..

Market Opportunities

AI governance integration, SME cloud governance platforms, and healthcare data space development: With the European Union's upcoming regulation requiring specific data governance around high-risk AI systems (e.g., medical algorithms) and enterprise realization that model governance is integral to effective data governance creation of a new product category for data-governance platform vendors to extend their offerings across AI model lineage monitoring, training-data quality monitoring, bias monitoring/detection/removal capabilities and both cost-effective methodologies developed with Harvard's SHEI for quantifying behavioral risk. Furthermore, the potential available SMEs market segment currently not served by any enterprise-grade governance platform is reaching upwards of 50B CNY (over $8.5 Billion USD) and dedicated fully integrated cloud-delivered platforms leveraging rapid deployment combined with simplified governance solutions designed for organizations having fewer than 20 persons are optimal to address clients whose human resources are limited and do not have a specialized data management team. The EU-led framework establishment for the secondary use of health data is forcing healthcare organisations and data intermediaries to accelerate investment under a policy-driven demand catalyst.

Recent Developments:

-

2025: Collibra launched its next-generation AI-powered data governance platform featuring automated data classification, intelligent data quality scoring, and AI-driven policy recommendation capabilities, reducing the manual governance programme implementation effort by up to 60% for enterprise deployments.

-

2025: IBM expanded its Watson Knowledge Catalog with enhanced AI governance capabilities integrating data lineage, model risk management, and regulatory compliance documentation into a unified governance and AI lifecycle management platform, addressing the growing enterprise requirement for integrated data and AI governance.

-

2024: Alation extended its data intelligence platform with automated data governance workflow capabilities that embed policy enforcement directly into data consumer search and access workflows, making governance participation seamless and non-disruptive for data analysts and data scientists.

-

2025: Microsoft expanded Microsoft Purview's data governance capabilities with enhanced multi-cloud data estate scanning supporting Google BigQuery and Snowflake data assets, enabling enterprises to govern data assets across their entire multi-cloud data estate from a single governance management platform.

-

2024: Informatica launched enhanced CLAIRE AI-powered metadata intelligence capabilities within its Intelligent Data Management Cloud, enabling automatic discovery of sensitive data, AI-driven data quality monitoring, and intelligent data relationship mapping across enterprise data environments at petabyte scale.

Data Governance Market Key Players

-

IBM Corporation

-

Oracle Corporation

-

Informatica Inc.

-

Collibra Inc.

-

Alation Inc.

-

Microsoft Corporation (Purview)

-

SAP SE

-

SAS Institute Inc.

-

Talend (Qlik)

-

Erwin (Quest Software)

-

Data Ladder

-

Ataccama Corporation

-

Profisee Group

-

Precisely (Syncsort)

-

Varonis Systems, Inc.

-

Reltio Inc.

-

Stibo Systems

-

TIBCO Software Inc.

-

MicroStrategy Incorporated

-

Denodo Technologies

Data Governance Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.72 Billion |

| Market Size by 2035 | USD 26.63 Billion |

| CAGR | CAGR of 18.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (Cloud-Based, On-Premises, Hybrid) • By Organisation Size (Large Enterprises, SMEs) • By Industry Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Oracle Corporation, Informatica Inc., Collibra Inc., Alation Inc., Microsoft Corporation (Purview), SAP SE, SAS Institute Inc., Talend (Qlik), Erwin (Quest Software), Data Ladder, Ataccama Corporation, Profisee Group, Precisely (Syncsort), Varonis Systems, Inc., Reltio Inc., Stibo Systems, TIBCO Software Inc., MicroStrategy Incorporated, Denodo Technologies |

Frequently Asked Questions

Ans: North America dominated the Data Governance Market in 2025 with approximately 40% of global revenues, led by the United States — the world's most data-intensive economy with the most comprehensive multi-layer data privacy regulatory framework, the highest enterprise cloud and AI adoption rates, and the world's leading data governance platform providers including IBM, Oracle, Informatica, Collibra, and Alation.

Ans: BFSI dominated the Data Governance Market in 2025, driven by financial institutions' exceptional regulatory compliance intensity encompassing GDPR, PCI-DSS, SR 11-7 model risk management, and Basel regulatory data governance requirements, combined with the commercial imperative of data-driven financial services that requires the highest-quality governed data foundations for credit, risk, and personalisation applications.

Ans: The convergence of expanding global data privacy regulatory compliance mandates requiring formal data management programmes, the AI adoption imperative demanding high-quality governed data foundations for reliable and compliant AI model performance, and the escalating complexity of multi-cloud data environments creating automated governance requirements are the compounding structural growth drivers through 2035.

Ans: The Data Governance Market was valued at USD 4.720 billion in 2025.

Ans: The Data Governance Market is expected to grow at a CAGR of 18.89% from 2026 to 2035.

Get in Touch