Defense Electronics Market Report Scope & Overview:

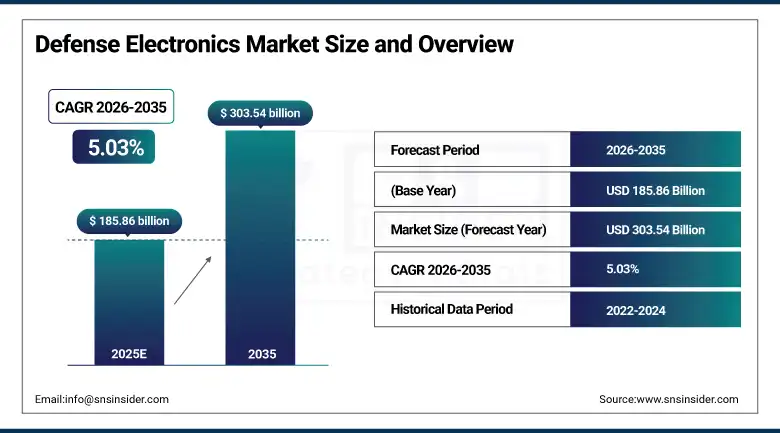

Defense Electronics Market was valued at USD 185.86 billion in 2025 and is expected to reach USD 303.54 billion by 2035, growing at a CAGR of 5.03% from 2026 to 2035.

Defense electronics sits at the intersection of every major trend reshaping modern military power. From the command-and-control networks that enable joint operations across air, land, sea, and space domains, to the electronic warfare systems that contest the electromagnetic spectrum on which all modern forces depend, to the sensors and processors that turn raw battlefield data into actionable intelligence within seconds, defense electronics is the nervous system through which contemporary military capability is expressed and applied. The decade between 2025 and 2035 is expected to be one of the most consequential periods in defense electronics history, as the simultaneous maturation of artificial intelligence, autonomous systems, advanced radar technology, and next-generation communication networks converges with a global security environment demanding faster, more precise, and more connected military operations than any previous era.

The electronics industry for defense applications is undergoing a fundamental restructuring with the overlap of commercial firms that specialize in artificial intelligence, cloud computing, chip design, and autonomy with traditional defense primes. The result has been an acceleration of innovation cycles, software-based systems that can be reprogrammed without physical replacement, and features which the conventional defense procurement system could never have matched in a competitive environment. Countries that have the domestic industry capability to capitalize on this trend will enjoy a permanent advantage in information war in the decade ahead.

Defense Electronics Market Size and Forecast

-

Market Size in 2025: USD 185.86 Billion

-

Market Size by 2035: USD 303.54 Billion

-

CAGR: 5.03% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026 to 2035

-

Historical Data: 2022 to 2024

To Get more information On Defense Electronics Market - Request Free Sample Report

Defense Electronics Market Trends

-

Accelerating integration of artificial intelligence and machine learning into radar signal processing, electronic warfare systems, and intelligence surveillance reconnaissance platforms, enabling real-time pattern recognition, threat classification, and autonomous response recommendation that reduces human cognitive load in high-tempo operational environments.

-

Growing procurement of software-defined radio and open-architecture communication systems aligned with Modular Open Systems Approach standards, enabling multi-vendor competition for software updates and reducing lifecycle costs compared to proprietary closed-architecture predecessors.

-

Expanding investment in electronic warfare capability across all major military powers, driven by the recognition that electromagnetic spectrum dominance is a prerequisite for conventional military success in any peer or near-peer conflict scenario rather than a specialized capability reserved for niche missions.

-

Rising demand for space-based defense electronics following demonstrated counter-satellite capabilities by China and Russia, accelerating procurement of protected satellite communications, space surveillance, and orbital awareness systems that underpin global military command and control architectures.

-

Increasing emphasis on cybersecurity hardening across all defense electronics systems as the attack surface expands with greater connectivity, with military procurement authorities imposing stringent cybersecurity compliance requirements that are reshaping supplier qualification processes industry-wide.

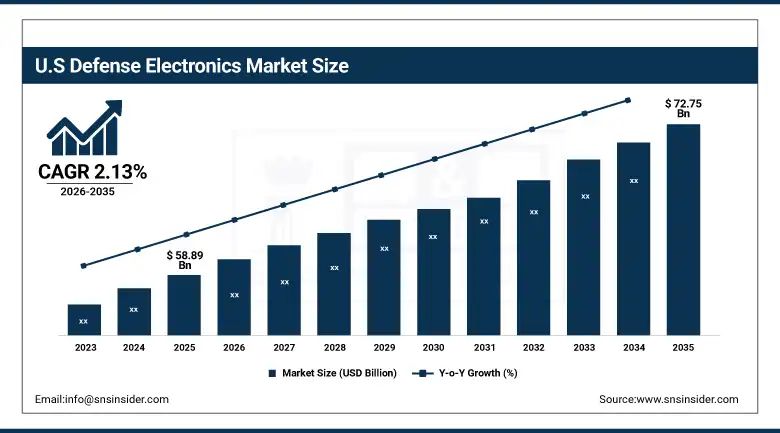

U.S. Defense Electronics Market was valued at USD 58.89 billion in 2025 and is expected to reach USD 72.75 billion by 2035, registering a CAGR of 2.13% during 2026 to 2035.

The United States maintains its commanding position as the world's largest defense electronics market, anchored by a defense procurement budget that has consistently exceeded that of the next several nations combined and a defense industrial base of unparalleled technological depth and manufacturing capacity. American defense electronics leadership spans every major capability domain, from Northrop Grumman's B-21 Raider avionics and mission systems to Raytheon's AESA radar arrays, from L3Harris's electronic warfare systems to General Dynamics' C4ISR integration programs. The U.S. Department of Defense's deliberate push toward open architecture systems through initiatives like the Joint All-Domain Command and Control program is reshaping procurement approaches in ways that open competition to a broader range of suppliers while simultaneously raising the bar for interoperability and cybersecurity compliance.

The passage of the National Defense Industrial Strategy and sustained congressional support for next-generation defense electronics programs reflects a bipartisan recognition that maintaining electronics superiority over near-peer adversaries requires not just procurement spending but systemic investment in the domestic semiconductor manufacturing base, the electronic warfare research pipeline, and the defense contractor workforce development programs that produce the specialized engineers and program managers on whom the entire enterprise depends.

Defense Electronics Market Segment Insights

-

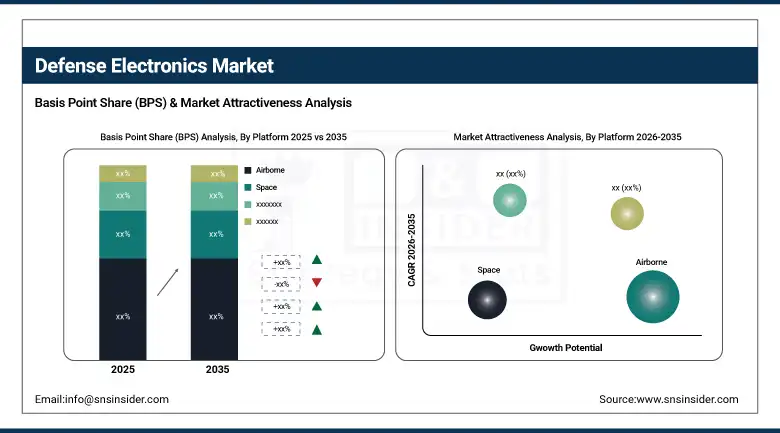

Based on Platform, Airborne platform accounted for the largest market share of 44% in 2025; Space platforms are expected to be the fastest growing segment during the forecast period.

-

Based on Vertical, Navigation, Communication and Display accounted for the largest market share of 47% in 2025; C4ISR is expected to record the fastest growth through the forecast period.

-

Based on Component, Hardware accounted for the largest market share of 65% in 2025; Software is expected to be the fastest growing component segment through 2035.

Defense Electronics Market Segment Analysis

By Platform, Airborne dominates, Space expected to grow fastest

Airborne platforms held 44% of the platform segment in 2025, a position reflecting decades of investment in sophisticated avionics, radar, and mission systems across combat aircraft, surveillance aircraft, transport aviation, and rotary wing fleets that collectively represent the largest repository of deployed defense electronics systems globally. The continuous cycle of avionics modernization, radar upgrade programs, and electronic warfare suite enhancement across aging but structurally sound airframes ensures sustained demand from the retrofit segment alongside procurement of new-production aircraft in all major air force inventories.

Space platforms are expected to register the highest compound annual growth rate through 2035, propelled by the convergence of military recognition that space is now a contested warfighting domain, the commercial satellite revolution reducing launch costs and enabling proliferated low-earth orbit architectures, and the demonstrated vulnerability of conventional high-value geostationary satellites to adversary anti-satellite capabilities. The U.S. Space Force procurement pipeline, combined with parallel investments in allied nations including the United Kingdom, France, Japan, and Australia, is generating sustained demand for space-qualified electronics across communications, navigation, surveillance, and early-warning satellite programs.

By Vertical, Navigation, Communication and Display dominates, C4ISR expected to grow fastest

Navigation, communication, and display systems accounted for approximately 47% of the vertical segment in 2025, a position underpinned by the universal deployment of these capabilities across every military platform and force element globally. Every aircraft, naval vessel, ground vehicle, and soldier system depends on precision navigation for positioning and targeting, secure communication for command and coordination, and intuitive display systems for situational awareness. The sophistication and value of these systems has grown continuously as GPS anti-jamming capability, software-defined radio flexibility, and high-resolution multi-function display technology have become standard requirements rather than premium options in military procurement.

The C4ISR segment is projected to achieve the strongest compound annual growth rate between 2026 and 2035, driven by the all-consuming strategic priority placed on network-centric warfare capability by every major military power. Command, control, communications, computers, intelligence, surveillance, and reconnaissance systems are the connective tissue of modern multi-domain operations, enabling the information advantage that translates sensor data into kill chain closure faster than any adversary can respond. The U.S. Army Project Convergence and Joint All-Domain Command and Control programs, alongside comparable European and Indo-Pacific initiatives, represent the largest C4ISR procurement opportunities in a generation.

By Component, Hardware dominates, Software expected to grow fastest

Hardware components commanded 65% of the defense electronics market by component in 2025, reflecting the foundational reality that defense electronics ultimately requires physical systems, whether radar arrays, communication terminals, electronic warfare transmitters, or sensor processing units, that must be physically manufactured, integrated, tested, and maintained across the defense equipment lifecycle. The defense electronics hardware market benefits from stable retrofit demand as in-service platforms receive capability upgrades, as well as new-production procurement for next-generation platforms across all service branches.

Software is expected to be the fastest growing category of components up until 2035 due to the increasing trend towards software-defined architecture in the defense electronics industry. The capability of updating radar waveforms, electronic warfare response, and communication protocols through software rather than through hardware replacement significantly lowers lifecycle costs while also enabling faster reactions to new threats in months rather than years or decades needed by traditional acquisitions process. This trend is transforming the dynamics of competition in the defense electronics industry.

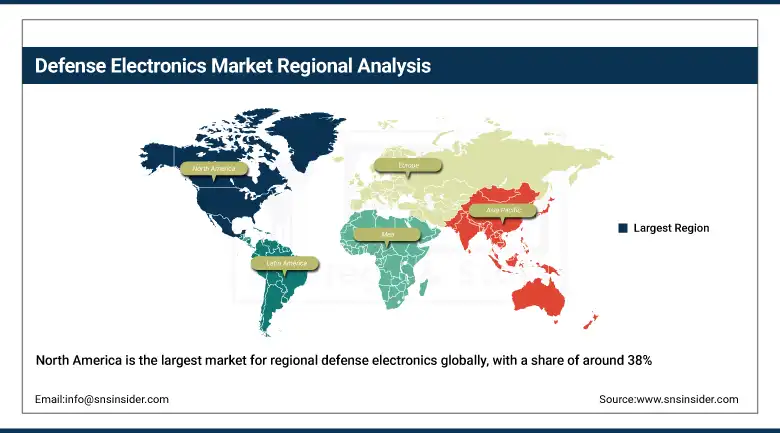

Defense Electronics Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|

North America |

United States |

38% |

|

Europe |

United Kingdom |

22% |

|

Asia Pacific |

China |

31% |

|

Middle East & Africa |

Saudi Arabia |

27% |

|

Latin America |

Brazil |

41% |

North America Defense Electronics Market Insights

North America is the largest market for regional defense electronics globally, with a share of around 38% of the total market revenue in 2025, wherein the United States makes up the lion's share through the procurement process in all military services and all electronics verticals. The extent of the defense electronics industrial base in the U.S., which includes prime contractors, subsystem specialists, semiconductor companies, and software providers, forms an innovation ecosystem that sustains its technological supremacy despite the heavy investments being made by China to close the capability gap. Canada plays a role in the market through procurement for interoperability purposes within the NATO and its own national defense priorities, such as the fighter replacement program of the Royal Canadian Air Force, which involves significant avionics and mission systems value.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Defense Electronics Market Insights

In 2025, the Asia Pacific region is expected to lead the way among other regions in the Defense Electronics Market because of various reasons such as China's unprecedented defense modernization efforts, India's plans to build an indigenous defense industry, South Korea's unmatched prowess in defense technology exports, and increased demand for defense electronics in countries like Japan, Australia, and some Southeast Asian countries due to deteriorating regional security situation. China's spending on defense electronics such as radars, electronic warfare, and C4ISR systems through its military-civil fusion efforts has been of such magnitude that China stands out as the second highest defense electronics spender in the world, while India's Defense Acquisition Procedure is promoting indigenous procurements in its market.

Europe Defense Electronics Market Insights

Europe maintained a significant position in the global Defense Electronics Market in 2025, with the United Kingdom, France, Germany, Italy, and Sweden driving the majority of regional procurement activity as NATO members accelerate defense spending in response to the changed European security environment following sustained conflict in Ukraine. The NATO commitment to member nations spending at minimum 2% of GDP on defense, with many major members now targeting higher levels, is generating a procurement expansion of historic proportions across radar modernization, electronic warfare, communication systems, and space-based defense electronics programs. European defense consolidation and joint procurement initiatives are creating larger addressable market opportunities for regional champions like Thales, BAE Systems, Leonardo, Rheinmetall, and Saab.

Middle East & Africa and Latin America Defense Electronics Market Insights

The Middle East and Africa region is one of the fastest growing regions in terms of defense electronics procurement due to the considerable amount of defense spending by the Gulf Cooperation Council member countries aimed at technology advancement in their military systems as part of efforts to counter the threat posed by ballistic missiles and drones amidst the instability in the region. The Middle East defense procurement budget is one of the largest in the world, with electronics components that range from radar, communications, electronic warfare, and C4ISR being major constituents of the total defense expenditure. Israel continues to be among the top countries producing and exporting defense electronics technologies of high caliber. This includes indigenous technologies produced by companies such as Elbit Systems, Rafael, and IAI. Brazil leads the Latin America market due to its relatively large defense budget and military modernization programs.

Defense Electronics Market Growth Drivers:

-

Escalating geopolitical tensions and rising global defense budgets creating structural demand for advanced electronics across all military platform categories

The international security environment that characterized the decade of 2025 to 2035 is fundamentally more contested and uncertain than the relatively stable post-Cold War period that preceded it. Russia's sustained aggression in Europe, China's military modernization and increasingly assertive regional posture, North Korea's ballistic missile development, and the proliferation of advanced military technology to non-state actors and smaller regional powers have collectively created a demand for defense electronics investment that transcends political cycles and budget pressures. NATO's expansion and the commitment of member states to meaningfully higher defense spending, combined with the independent procurement acceleration of Indo-Pacific nations, is generating a demand wave for radar, communication, electronic warfare, and C4ISR systems that the defense electronics industry is working hard to satisfy.

The single most powerful driver of defense electronics demand growth through 2035 is not any specific technology or threat category, but rather the broad recognition among governments worldwide that information superiority is the decisive competitive advantage in modern warfare, and that achieving and maintaining information superiority requires sustained investment in the electronic systems that sense, process, communicate, and act upon battlefield information faster and more reliably than any adversary. This recognition has elevated defense electronics from a supporting technology category to a primary strategic investment priority in defense planning documents from Washington to Tokyo, from London to Canberra.

Defense Electronics Market Restraints

-

Supply chain vulnerabilities, semiconductor sourcing dependencies, and export control complexities limiting production scalability

The defense electronics industry confronts supply chain challenges of structural significance that cannot be resolved through procurement decisions alone. The concentration of advanced semiconductor manufacturing capacity in Taiwan and South Korea creates a geopolitical risk exposure that defense planners and procurement officials acknowledge but cannot fully mitigate within the timeframes required by urgent capability demands. Export control regimes governing the transfer of advanced electronics technology create friction in the allied nation procurement relationships that the defense industry depends on for scale, while the specialized engineering workforce shortage in areas like RF systems design, electronic warfare algorithm development, and space-qualified electronics integration constrains the industry's capacity to execute on the growing procurement pipeline.

Defense Electronics Market Opportunities

-

Artificial intelligence integration, domestic semiconductor manufacturing investment, and space-based defense electronics expansion

The accelerating integration of artificial intelligence into defense electronics systems represents the most transformative opportunity in the market's near-term development, enabling capability improvements in radar target discrimination, electronic warfare adaptive response, and autonomous system decision-making that fundamentally change what defense electronics systems can achieve in contested environments. Government investment in domestic semiconductor manufacturing through programs like the U.S. CHIPS Act and comparable European and Asian initiatives is simultaneously addressing the supply chain vulnerability concern and creating opportunities for defense-grade semiconductor suppliers to expand capacity. The burgeoning space-based defense electronics market, driven by proliferated satellite architecture investment and the military's growing dependence on space-based capabilities across navigation, communication, intelligence, and early warning domains, represents a multi-billion-dollar growth opportunity over the forecast period.

Recent Developments:

-

2026: L3Harris Technologies announced the successful qualification of a next-generation software-defined radio system meeting the U.S. military's updated waveform and cybersecurity requirements, enabling simultaneous operation across multiple frequency bands and communication protocols on a single hardware platform that replaces multiple legacy radio systems currently deployed across ground force units.

-

2025 (September): Raytheon Technologies completed the acquisition of a specialized cybersecurity firm focused on defense electronics systems protection, integrating its advanced threat detection and response capabilities into Raytheon's radar and electronic warfare product lines to meet increasingly stringent cybersecurity procurement requirements from the U.S. Department of Defense.

-

2025 (August): Northrop Grumman unveiled its new generation of electronic warfare systems that are capable of tackling the latest threats presented by multi-spectral and cognitive radars due to the use of machine learning technologies for spectral analysis, which allows the system to implement adaptive jamming responses quicker than any legacy manual programming.

-

2024 (November): Thales Group signed a huge contract with a leading NATO European ally state to provide the next-generation ground-based radar systems for air surveillance purposes as part of the country's fast-tracked air defense enhancement process with much shorter deadlines compared to historical precedents due to the critical nature of the threat landscape.

-

2024 (July): BAE Systems concluded its successful program of installing active electronically scanned array radar systems into a major allied air force fleet in lieu of the mechanically scanned array counterparts, resulting in marked improvements in terms of multiple target tracking, electronic protection, and low-observable aircraft detection distance capabilities.

Defense Electronics Market Key Players

-

Raytheon Technologies (RTX Corporation)

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

BAE Systems plc

-

Thales Group

-

L3Harris Technologies Inc.

-

General Dynamics Corporation

-

Leonardo S.p.A.

-

Elbit Systems Ltd.

-

Rheinmetall AG

-

Saab AB

-

Israel Aerospace Industries

-

Curtiss-Wright Corporation

-

Cobham Limited

-

Aselsan A.S.

-

Teledyne Defense Electronics

-

Honeywell International Inc.

-

Mercury Systems Inc.

-

Data Patterns (India) Ltd.

-

Singapore Technologies Engineering Ltd.

Defense Electronics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 185.86 Billion |

| Market Size by 2035 | USD 303.54 Billion |

| CAGR | CAGR of 5.03% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Airborne, Space, Land, Marine) • By Vertical (Navigation, Communication and Display, C4ISR, Electronic Warfare, Radar, Optronics) • By Component (Hardware, Software, Services) • By Fit (Line-Fit, Retrofit) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Raytheon Technologies (RTX Corporation), Lockheed Martin Corporation, Northrop Grumman Corporation, BAE Systems plc, Thales Group, L3Harris Technologies Inc., General Dynamics Corporation, Leonardo S.p.A., Elbit Systems Ltd., Rheinmetall AG, Saab AB, Israel Aerospace Industries, Curtiss-Wright Corporation, Cobham Limited, Aselsan A.S., Teledyne Defense Electronics, Honeywell International Inc., Mercury Systems Inc., Data Patterns (India) Ltd., Singapore Technologies Engineering Ltd. |

Frequently Asked Questions

Asia Pacific dominated the Defense Electronics Market in 2025 with the largest regional share, driven by China's massive defense electronics modernization program, India's accelerating indigenous defense industrialization, and the broad procurement expansion of Indo-Pacific nations responding to regional security challenges.

The Airborne segment dominated the Defense Electronics Market in 2025 with approximately 44% of global platform revenue, driven by the dense deployment of avionics, radar, mission systems, and electronic warfare capabilities across combat aircraft, surveillance platforms, and rotary wing fleets worldwide.

Escalating global geopolitical tensions and the universal military priority placed on information superiority through advanced radar, communication, C4ISR, and electronic warfare systems is the primary structural driver, reinforced by rising NATO and Indo-Pacific defense budgets, accelerating artificial intelligence integration into military electronics platforms, and the growing strategic importance of space-based defense electronics capabilities.

The Defense Electronics Market was valued at USD 185.86 billion in 2025.

The Defense Electronics Market is expected to grow at a CAGR of 5.03% from 2026 to 2035.

Get in Touch