Dental Handpiece Market Report Scope & Overview:

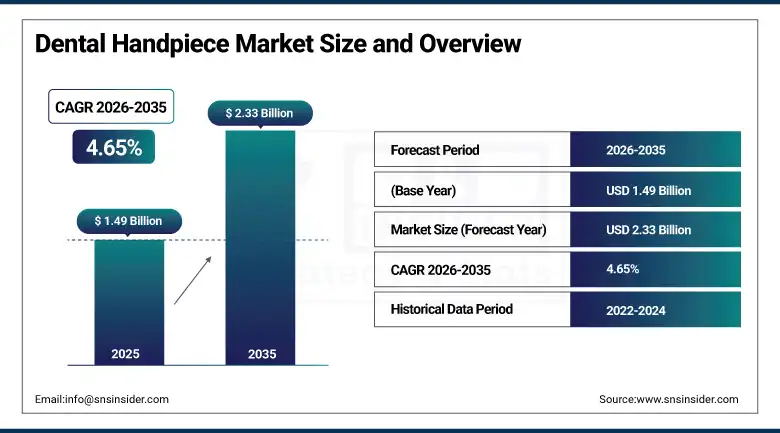

The Dental Handpiece Market was valued at USD 1.49 Billion in 2025 and is expected to reach USD 2.33 Billion by 2035, growing at a CAGR of 4.65% from 2026 to 2035.

The dental handpiece market is super important in dental equipment. These tools are used tons in day-to-day operations by dentists. They help with everything from filling cavities to making crowns, fixing root canals, and even some lab work for false teeth. Handpieces let dentists do a wide variety of tasks better and faster. New tech makes these tools much more precise and easier to use than older models. They also make it simpler to follow hygiene rules between patients. This steady stream of improved features keeps demand high for both new and replacement parts in countries where dental care is common.

On average, a single mid-sized dental clinic performs 3,000–6,000 handpiece-driven procedures annually, spanning cavity preparation, crown cutting, endodontic shaping, periodontal therapy, and oral surgical interventions. High-speed handpieces typically operate at rotational speeds of 200,000–400,000 RPM, while low-speed variants function in the range of 5,000–40,000 RPM, enabling precision across both hard and soft tissue applications.

Market Size and Forecast

-

Market Size in 2026E: USD 1.55 Billion

-

Market Size by 2035: USD 2.33 Billion

-

CAGR: 4.65% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Dental Handpiece Market - Request Free Sample Report

Dental Handpiece Market Trends

-

Rising adoption of electric handpieces is driven by higher torque consistency, precision control, and improved clinical outcomes in restorative and endodontic procedures.

-

Fiber-optic integration is enhancing visibility and accelerating premium handpiece adoption in clinics globally.

-

Strict infection control standards are boosting demand for autoclavable, corrosion-resistant, and sterilization-ready handpiece systems.

-

Expansion of dental tourism and private clinics in Asia-Pacific and Latin America is increasing procurement and replacement demand.

-

Growth of digital dentistry and CAD/CAM integration is creating demand for advanced, procedure-specific handpiece systems

The U.S. Dental Handpiece Market Outlook

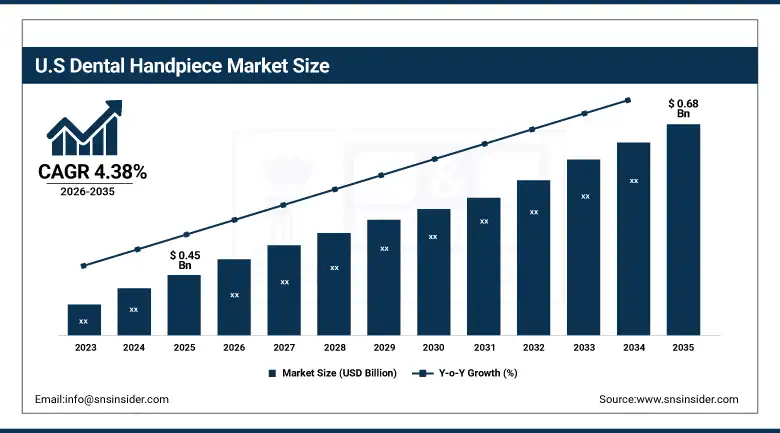

The U.S. Dental Handpiece Market was valued at USD 0.45 Billion in 2025 and is expected to reach USD 0.68 Billion by 2035, growing at a CAGR of 4.38%.

The United States leads the global dental handpiece market, thanks to its advanced dental care system supported by insurance. With more than 200,000 active dentists, it sees lots of procedures in both restorative and cosmetic areas. Dental educators promote new tech, too, which drives the need for updated tools. In the U.S., handpieces get replaced regularly due to regular wear and tear from use and sterilization. This steady replacement pace means demand stays stable and isn't as affected by economic ups and downs. Also, there's a growing trend toward electric handpieces, especially among dental specialists, pushing sales in the high-end sector.

Henry Schein Inc., in its 2025 full-year results, highlighted continued strength in dental equipment and technology sales across North American dental practices, noting that handpiece categories within its equipment distribution portfolio benefited from sustained dental office capital investment activity and professional product upgrade cycles supported by dental continuing education programs and clinical society endorsements.

Dental Handpiece Market Segment Analysis

-

By Product Type, air-driven dental handpieces dominated the market with a 42.13% share in 2025, while hybrid dental handpieces are the fastest growing product type with the highest CAGR of 5.88% from 2026 to 2035.

-

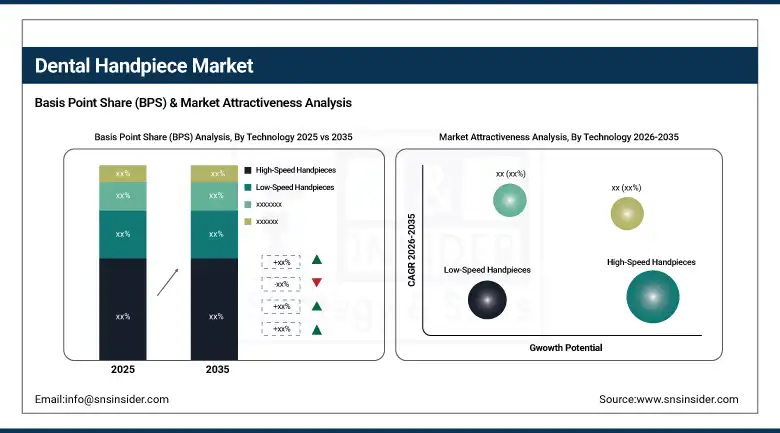

By Technology, high-speed handpieces dominated the market with a 45.12% share in 2025, while fiber-optic handpieces are the fastest growing technology segment with the highest CAGR of 5.58% from 2026 to 2035.

-

By Application, restorative dentistry dominated the market with a 30.15% share in 2025, while orthodontics is the fastest growing application segment with the highest CAGR of 7.77% from 2026 to 2035.

-

By End User, dental clinics dominated the market with a 55.15% share in 2025, while academic & research institutes are the fastest growing end user segment with the highest CAGR of 5.88% from 2026 to 2035.

By Product Type, air-driven dental handpieces dominate the dental handpiece market, while hybrid dental handpieces are the fastest-growing segment.

The air-driven dental handpieces segment dominated the market with the highest revenue share of 42.13% in 2025 owing to their widespread adoption across general dentistry practices, cost-effectiveness relative to electric alternatives, established clinical familiarity among dental professionals globally, and extensive compatibility with existing dental unit infrastructure. Their high operational speeds, lightweight ergonomic profiles, and lower acquisition costs continue to support broad penetration across both high-volume clinical environments and price-sensitive emerging market dental practices.

The hybrid dental handpieces segment is estimated to register the highest CAGR of 5.88% during the forecast period of 2026–2035 owing to rising demand for instruments that combine the lightweight characteristics of air-driven handpieces with the torque consistency and variable speed control advantages of electric systems. Growing clinical interest in procedural precision without full electric system investment requirements, particularly among restorative and endodontic specialists, is accelerating adoption of hybrid platform handpieces across professional dental markets.

By Technology, high-speed handpieces dominate the dental handpiece market, while fiber-optic handpieces are the fastest-growing segment.

The high-speed handpieces segment dominated the market with the largest revenue share of 45.12% in 2025 attributed to their fundamental role in tooth preparation, cavity removal, crown and bridge work, and the broad range of standard restorative and prosthetic procedures that constitute the majority of clinical dental workload across general dentistry and specialty practice environments. Their universal adoption across dental practice categories and established clinical workflows continue to anchor segment dominance across global markets.

The fiber-optic handpieces segment is projected to witness the fastest CAGR of 5.58% during 2026–2035 owing to the significant procedural visibility advantages that integrated illumination systems provide within oral cavities, enabling superior cavity preparation accuracy, improved margin visualization in crown work, and enhanced safety in surgical procedures. Increasing dental professional awareness of fiber-optic handpiece benefits for clinical quality improvement and the declining price premium of fiber-optic-equipped platforms relative to standard alternatives are progressively expanding market penetration.

By Application, restorative dentistry dominates the dental handpiece market, while orthodontics is the fastest-growing segment.

The restorative dentistry segment dominated the dental handpiece market with the highest revenue share of 30.15% in 2025 owing to the consistently high procedural volumes associated with cavity preparation, composite and amalgam restorations, crown and bridge preparations, and dental veneer placements that collectively represent the foundational workload of general dental practice globally. The large and continuously expanding global burden of dental caries and tooth loss drives structurally sustained demand for restorative dental procedures and the handpiece tools through which they are performed.

The orthodontics segment is projected to witness the fastest CAGR of 7.77% during the forecast period of 2026–2035 driven by the global expansion of orthodontic treatment acceptance, rising cosmetic dentistry awareness, growing adoption of clear aligner therapy requiring handpiece-assisted procedures, and expanding orthodontic specialist practice establishment across emerging markets. The increasing integration of digital orthodontic workflows requiring specialized rotary instruments for bracket bonding preparation and aligner attachment procedures is further driving specialty handpiece demand within this application segment.

By End User, dental clinics dominate the dental handpiece market, while academic & research institutes are the fastest-growing segment.

The dental clinics segment dominated the dental handpiece market with the highest revenue share of 55.15% in 2025 owing to the centralized procurement patterns of private and group dental practice environments, the high per-clinic handpiece utilization rates driven by multi-chair configurations, and the consistent replacement cycle demands generated by high-volume clinical environments requiring multiple handpiece sets for concurrent operatory use, sterilization rotation, and specialty procedure requirements. The global expansion of private dental group practices and dental service organization networks continues to consolidate and amplify handpiece procurement volumes within clinical settings.

The academic & research institutes segment is anticipated to record the fastest CAGR of 5.88% throughout the forecast period of 2026–2035 driven by expanding dental school enrolments globally, growing dental research activity requiring specialized handpiece instrumentation, increasing simulation laboratory investments incorporating high-fidelity dental training environments, and the progressive development of dental education infrastructure across emerging economy academic institutions that are establishing or scaling their clinical training programs.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.54% |

|

Europe |

Germany |

31.46% |

|

Asia Pacific |

China |

37.64% |

|

Middle East & Africa |

UAE |

32.45% |

|

Latin America |

Brazil |

44.29% |

North America Dental Handpiece Market Insights

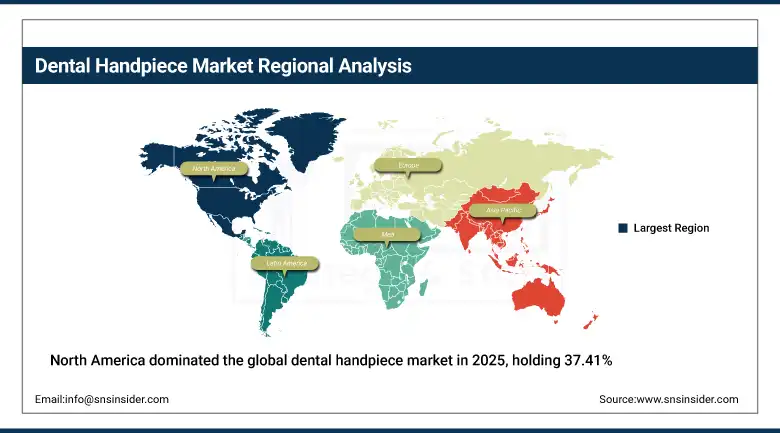

North America dominated the global dental handpiece market in 2025, holding 37.41% of global revenues, with the United States accounting for 80.54% of regional revenue. Market leadership in North America is attributable to the region's comprehensively developed dental healthcare infrastructure, high rates of dental insurance coverage across both employer-sponsored and government-administered programs, an extensively trained and technologically progressive dental professional workforce, and strong institutional support for dental technology adoption through professional society continuing education frameworks.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. dental market, characterized by more than 200,000 active dental practitioners and a structurally high volume of annual dental visits, generates consistent handpiece procurement and replacement activity at a scale unmatched by any other single national market.

Canada provides additional regional demand through its publicly supported dental care framework, which has expanded access to dental services for previously underserved populations, generating incremental procedural volume growth that supports handpiece utilization increases. The Canadian Dental Care Plan, launched in recent years, has accelerated dental service utilization among lower and middle-income households, broadening the patient base served by dental clinics and supporting equipment procurement investments across general and specialty practice categories.

North America remains the most mature dental handpiece market, supported by 200,000+ active dental practitioners in the United States and one of the highest dental visit frequencies globally, exceeding 300+ million dental visits annually. Replacement cycles typically occur every 3–5 years in high-usage clinical environments, sustaining continuous equipment turnover.

Europe Dental Handpiece Market Insights

European dental handpiece market shows a diverse demand with top-notch public systems in Northern Europe and mostly private markets in the South and East. This blend leads to varied buying habits and pricing sensitivities between regions. Germany's market is the biggest in Europe, thanks to a cluster of leading dental makers like W&H Dentalwerk, Bien-Air, and KaVo Dental. It also boasts advanced dental tech and a strong focus on education. Major cities have lots of dental practices too. Post-pandemic, strict infection controls in Western Europe are pushing more frequent handpiece replacements and preference for higher-end products.

Europe's dental industry contributes over EUR 15 billion annually to regional healthcare equipment revenues. Infection control regulations require routine sterilization compliance, driving handpiece replacement cycles approximately every 4–6 years depending on clinical load. Germany, Switzerland, and Austria represent the premium segment, where locally manufactured brands such as KaVo and W&H are widely used in over 60% of high-end clinical setups.

Asia Pacific Dental Handpiece Market Insights

Asia Pacific is the fastest-growing regional dental handpiece market at a CAGR of 5.40% through 2035. China accounts for 37.64% of Asia Pacific revenues as its rapidly expanding middle class and accelerating dental awareness programs are generating procedural volume growth across both public hospital dental departments and the rapidly proliferating private dental clinic sector that is attracting significant domestic and foreign investment in dental service delivery infrastructure. India represents the region's fastest-growing country-level market through the progressive formalization of its dental care delivery ecosystem, growing dental professional workforce, expanding dental school output, and government health scheme integration of dental services across public healthcare networks.

China's dental market has seen significant investment in private dental group expansion, with chains such as China alone has 100,000+ dental clinics and hospital-based dental departments, with rapid expansion of private dental chains such as Arrail Dental across Tier 1 and Tier 2 cities, generating consolidated handpiece procurement volumes that increasingly Favor premium electric and fiber-optic handpiece platforms as clinical quality differentiation becomes a competitive priority among private dental service providers.

MEA & Latin America Dental Handpiece Market Insights

Middle East and Latin America are big deals when it comes to dental handpiece markets. These regions have a ton of growth potential because more folks there are learning about dental care. Also, both areas are boosting their private dental practices and investing in health infrastructures. In the Middle East, the UAE is king, leading with 30.45% of regional revenues. Their top-notch services come from having loads of cash per person, dentists who've been trained abroad, and posh private dental clinics. They even bring in patients from neighbouring countries looking for first-rate care.

As for Latin America, Brazil takes the lead in their dental handpiece market thanks to being the region’s most populated country. It boasts a huge private dental sector and an impressive dental school system that turns out tons of new dentists yearly. On top of that, they excel at getting dental products into the market. Meanwhile, Mexico and Colombia are rapidly becoming major players. With their blossoming dental insurance coverage, growing tourist industries focused on dental work, and bettering private clinic conditions, these countries are really stepping up in the premium dental equipment race.

Latin America's dental market has benefited from Brazil's unique position as one of the world's leading per-capita dental procedure volume markets, with over 300,000 registered dentists serving both public and private sector patients and representing one of the most significant dental handpiece procurement markets in the developing world.

Market Dynamics

Growth Drivers: Rising dental procedure volumes and electric handpiece adoption

Global dental procedure growth drives the dental handpiece market because these tools are crucial for most dental procedures. With the increasing burden of dental caries, periodontal disease, and tooth loss affecting billions worldwide, there's steady demand for dental treatments. This need stays strong despite economic ups and downs. More people now see managing dental diseases as vital for overall health too, not just oral health. So, handpieces remain key in addressing these widespread issues in both rich and developing countries.

Restraints: High acquisition costs and infection control compliance burden

Premium electric and fiber-optic dental handpieces come with higher prices, making it tough for budget-conscious dentists to buy them, especially in developing areas. In these spots, cash for dental tools is tight due to limited revenues and trouble getting equipment financing. On top of that, supplies that get frequent use take priority over big equipment costs. Beyond just the upfront cost, though, there's the overall price of owning a handpiece. Dentists must cover initial purchases, but they also need money for regular upkeep service agreements, turbine part swaps, head cleanups, and fixing pieces for sterilization. All these make the real expense much larger and explain why many hold off on upgrading their gear too often.

Opportunities: Electric handpiece premiumization and emerging market dental infrastructure expansion

The dental handpiece market is at a turning point. While basic air-driven handpiece sales are slowing, there's a growing high-end market for electric, fiber-optic, and hybrid models. These advanced electric types do much better in key dental tasks, giving companies that make them a big edge in profits. As more dentists see how well electric versions work, especially in tricky procedures like endodontics and implants, they're becoming popular even in regular general practices, not just specialty offices. Plus, as these electric devices are made on a larger scale, their prices are dropping too, making them accessible to more dentists.

Recent Developments:

-

2026: KaVo Dental (Envista Holdings) commercially launched its next-generation INTRA LUX electric handpiece platform with advanced torque management electronics and compatibility with digital dental unit integration systems for practice management connectivity.

-

2026: NSK (Nakanishi Inc.) expanded its Ti-Max Z electric handpiece range with enhanced titanium alloy body construction, improved autoclave resistance, and expanded coupling compatibility designed to accelerate electric handpiece adoption across multi-brand dental practice environments in Asia Pacific markets.

-

2025: Dentsply Sirona launched its updated MIDWEST TRADITION Plus air-driven handpiece series incorporating enhanced bearing systems, improved turbine cartridge longevity, and refined ergonomic grip designs targeting high-volume general dentistry procedural environments.

-

2025: W&H Dentalwerk introduced the Synea Fusion electric handpiece line featuring integrated LED illumination, brushless motor technology, and expanded speed range capability designed for comprehensive clinical use across restorative, endodontic, and prosthetic applications.

Dental Handpiece Market Key Players are:

-

Dentsply Sirona

-

Envista Holdings Corporation (KaVo Kerr)

-

Nakanishi Inc. (NSK)

-

W&H Dentalwerk Bürmoos GmbH

-

Bien-Air Dental

-

J. Morita Corporation

-

Brasseler USA

-

Planmeca Oy

-

Straumann Group (Anthogyr handpiece portfolio)

-

MK-dent GmbH

-

Saeshin Precision Co., Ltd.

-

Dentamerica Inc.

-

Henry Schein Inc. (private label handpieces)

-

Sinol Dental

-

Being Foshan Medical Equipment Co., Ltd.

-

FONA Dental (Planmeca Group)

-

TPC Advanced Technology

-

Aseptico Inc.

-

KaVo Dental (Envista brand)

-

Lares Research

Dental Handpiece Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.49 Billion |

| Market Size by 2035 | USD 2.33 Billion |

| CAGR | CAGR of 4.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Air-Driven Dental Handpieces, Electric Dental Handpieces, Hybrid Dental Handpieces, Surgical Handpieces, Laboratory Handpieces) • By Technology (High-Speed Handpieces, Low-Speed Handpieces, Fiber-Optic Handpieces, Non-Fiber Optic Handpieces) • By Application (Restorative Dentistry, Endodontics, Periodontics, Oral Surgery, Prosthodontics, Orthodontics) • By End User (Dental Clinics, Hospitals, Dental Laboratories, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dentsply Sirona, Envista Holdings Corporation (KaVo Kerr), Nakanishi Inc. (NSK), W&H Dentalwerk Bürmoos GmbH, Bien-Air Dental, J. Morita Corporation, Brasseler USA, Planmeca Oy, Straumann Group (Anthogyr handpiece portfolio), MK-dent GmbH, Saeshin Precision Co., Ltd., Dentamerica Inc., Henry Schein Inc. (private label handpieces), Sinol Dental, Being Foshan Medical Equipment Co., Ltd., FONA Dental (Planmeca Group), TPC Advanced Technology, Aseptico Inc., KaVo Dental (Envista brand), Lares Research. |

Frequently Asked Questions

The dental handpiece market is expected to grow at a CAGR of 4.65% from 2026 to 2035.

The dental handpiece market was valued at USD 1.49 Billion in 2025.

Key growth factors include rising global dental procedure volumes, increasing adoption of electric handpieces for higher precision, and expanding dental infrastructure across Asia Pacific, Latin America, and the Middle East.

Hybrid Dental Handpieces is the fastest-growing product type in the dental handpiece market, with a CAGR of 5.88% from 2026 to 2035.

North America dominated the dental handpiece market in 2025, holding 37.41% of global revenues, with the United States accounting for 80.54% of North American revenues.

Get in Touch