Diesel Generator Market Report Scope & Overview:

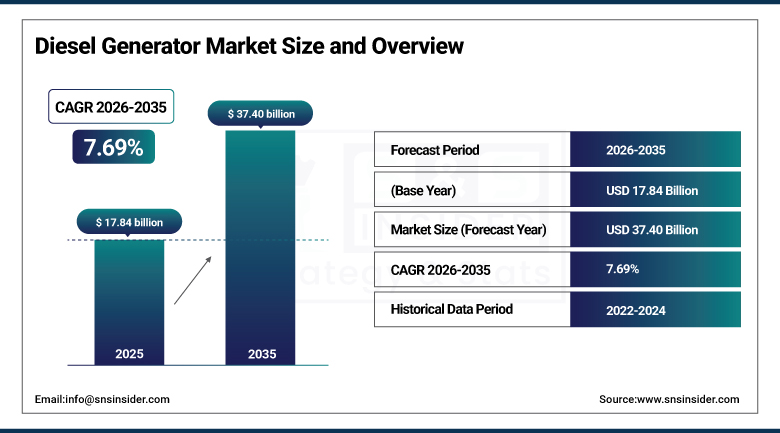

The Diesel Generator Market was valued at USD 17.84 Billion in 2025 and is expected to reach USD 37.40 Billion by 2035, growing at a CAGR of 7.69% from 2026–2035.

The Diesel Generator Market is witnessing positive growth owing to the increasing demand for uninterrupted power generation systems in industries, businesses, and homes. The occurrence of frequent power shortages and poor grid system infrastructure in developing nations are encouraging the installation of diesel generators as alternatives. Industrialization, infrastructural developments, and the growth of data centers are contributing to the demand. Construction activities and development in the oil and gas industry are also supporting market growth. Moreover, the requirement of constant electricity in hospitals, manufacturing plants, and telecommunication infrastructure, coupled with the benefits of low cost and high power generation, is also positively affecting global market growth.

According to the International Energy Agency (IEA), around 675 million people globally still lack access to electricity, highlighting a substantial reliance on alternative and backup power sources such as diesel generators in off-grid and underserved regions. The World Bank and SE4ALL initiative also report that billions of people experience intermittent or unreliable electricity supply, particularly in developing economies, further increasing dependence on backup and standby power systems.

Diesel Generator Market Size and Forecast

-

Market Size in 2026E: USD 19.21 Billion

-

Market Size by 2035: USD 37.40 Billion

-

CAGR: 7.69% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Diesel Generator Market - Request Free Sample Report

Diesel Generator Market Trends

-

Rising demand for reliable backup power solutions across industrial, commercial, and residential sectors is driving the diesel generator market.

-

Growing frequency of power outages and grid instability is boosting market growth.

-

Expansion of construction activities, mining operations, and infrastructure projects is fueling generator deployment.

-

Increasing focus on uninterrupted power supply for critical facilities such as hospitals, data centers, and telecom networks is shaping adoption trends.

-

Advancements in fuel-efficient engines, hybrid generator systems, and low-emission technologies are improving performance and compliance.

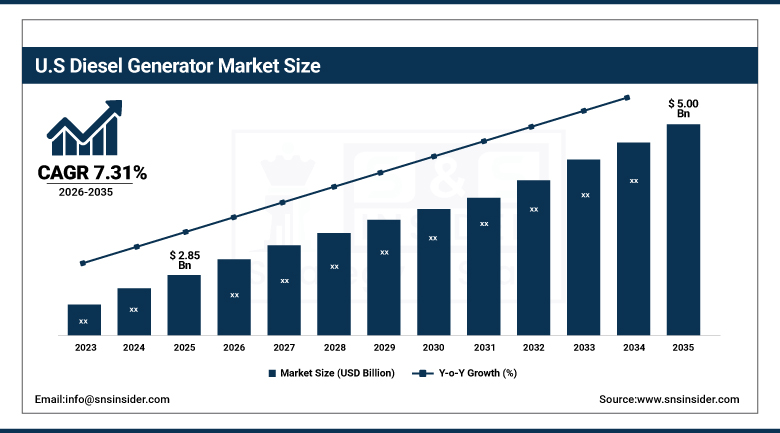

U.S. Diesel Generator Market Outlook

The U.S. Diesel Generator Market was valued at approximately USD 2.85 Billion in 2025 and is expected to reach approximately USD 5.00 Billion by 2033, growing at a CAGR of approximately 7.31%.

The United States diesel generator market benefits from the combination of a large commercial and industrial facility base with established standby generator requirements, the most extensive data centre infrastructure globally whose AI-driven expansion is creating unprecedented large generator procurement, and a healthcare sector whose Joint Commission and NFPA 99 emergency power requirements create mandatory generator installation standards across hospital, ambulatory care, and long-term care facilities.

According to the U.S. Energy Information Administration (EIA), the United States experiences billions of dollars in annual economic losses due to power outages, largely driven by extreme weather events, grid instability, and infrastructure failures, highlighting the critical need for reliable backup power solutions such as diesel generators.

Diesel Generator Market Segment Analysis

-

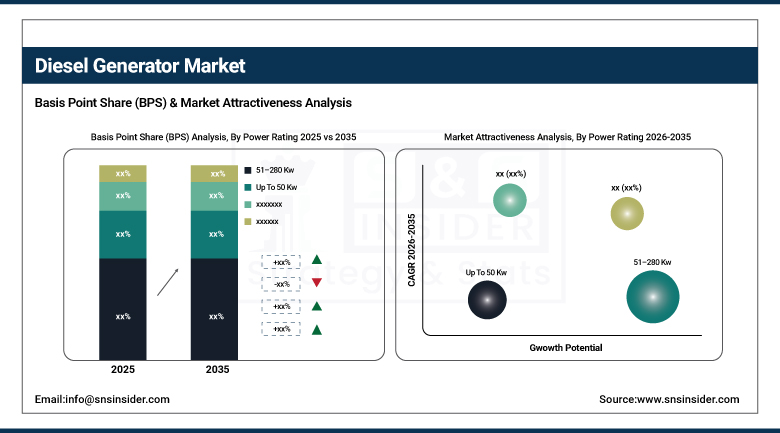

By Power Rating, 51–280 kW segment dominated the market in 2025 with 31.02% share; Up to 50 kW segment is the fastest growing segment with a CAGR of 7.50%.

-

By Design, Stationary segment dominated the market in 2025 with 64.70% share; Portable segment is the fastest growing segment with a CAGR of 6.16%.

-

By Application, Standby Power segment dominated the market in 2025 with 55.64% share; Prime & Continuous Power segment is the fastest growing segment with a CAGR of 7.44%.

-

By End User, Industrial segment dominated the market in 2025 with 51.48% share; Residential segment is the fastest growing segment with a CAGR of 6.66%.

By Power Rating, 51–280 kW segment dominates the market, while up to 50 kW segment is the fastest-growing segment

The 51–280 kW segment dominated the market because of its high suitability for industrial, commercial, and infrastructural applications, where there exists a need for mid-range power generation. This segment is most efficient, performs well, and costs less. Moreover, since it is mostly used in manufacturing plants, data centers, and construction sites, the demand keeps on rising. The growing demand for uninterrupted power supply continues to make it a leader in the global market.

The up to 50 kW segment is the fastest growing due to the increasing popularity of this capacity in both households and small enterprises. Frequent power outages and interruptions together with growing urbanization are contributing factors. Low cost, portability, and installation expenses make it an attractive option for low load needs. Its implementation in various mobile units is boosting demand.

By Design, stationary segment dominates the market, while portable segment is the fastest-growing segment

The stationary segment dominated the market owing to their reliability, high capacity of generating energy, and capability to work continuously. The products in the segment are used extensively in industries, commercial facilities, and other critical infrastructures that need constant availability of power supply. Their durable construction and capacity to handle bulky electrical appliances make them the most favored products among consumers. The growing need for efficient solutions in terms of power backup solutions will ensure dominance of the segment in the market.

The portable segment is the fastest growing owing to rising demand for such equipment in construction sites, outdoor facilities, and emergencies. Their portable nature and fast deployment will make them the perfect choice for providing a temporary power solution in such cases. Growing development in the infrastructural sector and increasing off-the-grid projects are expected to drive the demand for such equipment. Improved technology will provide better performances.

By Application, standby power segment dominates the market, while prime and continuous power segment is the fastest-growing segment.

The standby power segment dominated the market owing to its importance in providing instant support during a power outage. It has widespread use in healthcare institutions, data centers, commercial buildings, and manufacturing industries for ensuring continuous operations. The increasing need for uninterrupted energy supply among various end-user industries has made it even more significant. Reliability, instant start-up capability, and capability to avoid disruptions have resulted in its wide acceptance in the market.

The prime and continuous power segment is the fastest growing due to the escalating requirement for uninterrupted power supplies in off-grid areas. Continuous power systems find great significance in sectors such as mining, construction, oil, and gas. Growth in infrastructure development along with lack of sufficient grid connection has played an important role in stimulating the growth of this market. Enhanced fuel efficiency has also contributed to the rising use of prime power generators.

By End User, industrial segment dominates the market, while residential segment is the fastest-growing segment

The industrial segment dominated the market due to their higher consumption of energy as well as the need for an assured electricity supply in such industries where there is an extensive requirement for electricity usage in manufacturing and processing operations. Backup power supplies are essential in industries that need electricity for running their businesses to ensure a continuous power supply. Growth within industries owing to automation and increased manufacturing units further supports its dominance.

The residential segment is the fastest growing owing to the increasing recognition of the importance of having backup power sources and frequent interruptions of electricity. Adoption and use of generators for lighting, heating, and other essential processes in households are expected to drive demand growth further. Increased disposable incomes along with rapid urbanization and affordability of power backup systems will drive growth. Increasing dependency on electricity for daily household chores will further boost adoption.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Asia Pacific |

China |

38.5% |

|

Europe |

Germany |

28.5% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Diesel Generator Market Insights

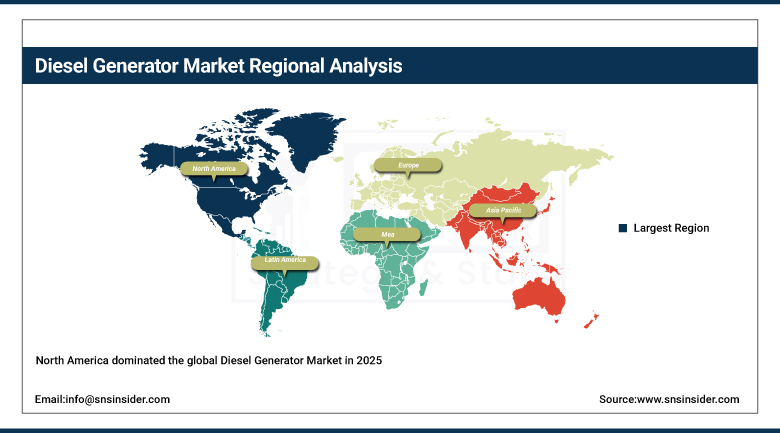

North America dominated the global Diesel Generator Market in 2025, driven by the world's largest data centre infrastructure, extensive industrial facility base, stringent healthcare emergency power regulations, and growing residential standby generator adoption. The United States accounts for approximately 82.5% of North American revenues through its concentrated data centre hyperscale construction, commercial facility emergency power requirements, and the commercial presence of Caterpillar, Cummins, and Kohler whose generator product lines define North American market standards.

The U.S. Department of Energy (DOE) reports that data centers account for approximately 4–5% of total U.S. electricity consumption, reinforcing the importance of uninterrupted power supply systems and robust backup infrastructure to ensure continuous operations. These factors collectively strengthen the demand for diesel generators across commercial, industrial, and digital infrastructure sectors.

Canada contributes supplementary demand through its oil sands extraction, mining, and resource sector industrial generator requirements, and the growing commercial and residential standby generator market driven by its own grid reliability challenges from extreme weather events.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Diesel Generator Market Insights

Asia Pacific is the fastest-growing regional Diesel Generator Market, driven by rapid industrialisation creating new manufacturing and processing facility power requirements, urbanisation expanding commercial and residential electrical demand beyond grid capacity in rapidly growing cities, and infrastructure investment creating construction and public works prime power requirements.

China accounts for approximately 38.5% of Asia Pacific revenues through its enormous industrial base, rapidly growing data centre sector, and the continuing grid reliability challenges in interior provinces whose industrial facilities require backup and prime power capability. India and Southeast Asian markets are growing fastest within the region where grid reliability limitations in industrial corridors and commercial developments create prime power diesel generator demand that approaches in scale the standby power applications that dominate developed market generator demand.

Europe Diesel Generator Market Insights

Europe held a significant share of the global Diesel Generator Market in 2025. Germany, France, the United Kingdom, Norway, and the Netherlands are the leading national markets whose advanced industrial and commercial infrastructure, data centre sector, and healthcare facilities create consistent generator demand.

Germany accounts for approximately 28.5% of European revenues through its large industrial base, growing data centre sector, and the commercial presence of MTU Onsite Energy (Rolls-Royce Power Systems) and other European generator manufacturers. European emissions regulations are progressively restricting diesel generator operation hours in populated areas, creating commercial incentive for hybrid generator adoption and accelerating product transition toward Tier 4 compliant and HVO-compatible engine platforms.

MEA & Latin America Diesel Generator Market Insights

The UAE leads MEA revenues at approximately 38.4% of the regional total through its world-class commercial and data centre infrastructure requiring premium generator backup power, the construction sector's prime power requirements for large-scale development projects, and the oil and gas sector's offshore and remote facility generator demand. Saudi Arabia, Nigeria, and South Africa contribute significant regional demand through their industrial, commercial, and off-grid power applications where grid unreliability creates both prime power and standby generator deployment at above-average density relative to GDP.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large industrial, commercial, and healthcare sectors, the construction industry's prime power requirements, and the residential market's growing standby generator adoption in areas with persistent grid reliability challenges. Mexico contributes significant secondary demand through its large manufacturing sector's generator requirements and commercial facility standby power investment.

Market Dynamics

Growth Drivers: Data centre AI construction and grid unreliability are driving strong diesel generator demand globally.

The diesel generator market's growth is driven by the extraordinary AI infrastructure investment cycle creating the largest hyperscale data centre construction wave in history and the enduring grid reliability gap in developing market industrial zones whose prime power requirements sustain diesel generator procurement independent of standby application growth. The AI computing infrastructure expansion whose USD 350 billion annual data centre capital expenditure includes 15 to 20% backup power infrastructure content creates annual diesel generator procurement at scales that are reshaping the market's demand composition, with individual data centre campus generator procurement events matching the scale of entire national generator markets in smaller economies.

Additionally, data center resilience requirements, as highlighted by Uptime Institute, show that over 99.9% uptime is expected in modern facilities, driving widespread deployment of diesel backup generators to ensure uninterrupted operations during grid failures and power disruptions.

Restraints: Emissions regulations and alternative backup technologies are limiting diesel generator adoption in developed market

Diesel generators' significant NOx, particulate matter, and CO2 emissions create progressive regulatory restriction in North American and European markets whose Tier 4 Final requirements in the United States and equivalent Stage V standards in Europe impose substantial emissions control technology costs on new installations that restrict market access for non-compliant equipment and increase total cost of ownership for compliant alternatives.

California's South Coast Air Quality Management District and similar regulatory bodies in other air quality non-attainment areas impose emergency generator operation hour limits and installation restrictions that constrain the standby power application scope in the most commercially advanced markets. Battery energy storage systems whose rapidly declining cost per kilowatt-hour is making extended runtime capability more accessible at medium-scale standby power requirements creates an alternative backup power technology whose operational silence, zero local emissions, and maintenance simplicity advantages over diesel are progressively expanding the operating contexts where battery storage replaces or reduces diesel generator reliance.

Opportunities: Hybrid diesel-battery systems and emerging infrastructure investments are creating new high-growth commercial opportunities.

Hybrid diesel-battery generator systems whose combination of diesel engine runtime flexibility and battery storage instant response capability creates a power system architecture that achieves 30 to 60% fuel consumption reduction versus diesel-only operation in prime and peak shaving applications represent the most commercially significant product innovation opportunity for diesel generator manufacturers seeking sustainable market positioning in an increasingly decarbonisation-conscious procurement environment.

Each hybrid generator system whose documented fuel efficiency and emissions reduction versus diesel-only equivalents creates verifiable sustainability credentials that corporate procurement sustainability commitments and regulatory fuel use limits recognise creates commercial adoption motivation that sustains generator manufacturer investment in hybrid product line development. Emerging market infrastructure investment whose road, water, healthcare, and telecommunications projects in Africa, South Asia, and Southeast Asia create construction phase prime power requirements for which diesel generators remain the dominant solution creates a market expansion frontier whose commercial scale grows with the infrastructure investment pace.

Recent Developments:

-

2025: Caterpillar launched its XQP1250 Next-Generation Power Module with a Cat C32 ACERT engine meeting EPA Tier 4 Final emissions standards and integrated remote monitoring through Cat Connect, providing data centres and industrial customers with a 1,250 kVA standby solution combining emissions compliance, fuel efficiency improvement, and digital management capability.

-

2024: Cummins launched the QST30G9 generator set platform for data centre applications incorporating advanced load acceptance capability and digital load management integration, enabling faster transient response to sudden large load steps that data centre UPS transfer testing requires without voltage deviation.

-

2024: Kohler Power Systems expanded its industrial and commercial generator product line with new 1,250 kW to 3,000 kW high-capacity platforms targeting data centre, utility, and large industrial applications, extending its generator capacity range to address the above-1 MW segment whose fastest growth is driven by hyperscale data centre backup power requirements.

Diesel Generator Market Key Players

-

Caterpillar Inc.

-

Cummins Inc.

-

Generac Power Systems

-

Kohler Co.

-

Atlas Copco AB

-

HIMOINSA

-

FG Wilson

-

Kirloskar Electric Co. Ltd.

-

Mitsubishi Heavy Industries Ltd.

-

Wärtsilä Corporation / MTU

-

Rolls Royce plc / MTU Onsite Energy

-

Denyo Co., Ltd.

-

Yanmar Co., Ltd.

-

Ashok Leyland Ltd.

-

Briggs & Stratton Corporation

-

American Honda Motor Company, Inc.

-

John Deere & Company

-

Broadcrown Generators Australia (Pty) Ltd.

-

Wuxi Kipor Power Co., Ltd.

-

Mahindra Powerol

Diesel Generator Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.84 Billion |

| Market Size by 2035 | USD 37.40 Billion |

| CAGR | CAGR of 7.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Power Rating (Up To 50 Kw, 51–280 Kw, 281–500 Kw, 501–2,000 Kw, Above 2,000 Kw) • By Design (Stationary, Portable) • By Application (Standby Power, Peak Shaving, Prime & Continuous Power) • By End User (Industrial, Commercial, Residential) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Caterpillar Inc., Cummins Inc., Generac Power Systems, Kohler Co., Atlas Copco AB, HIMOINSA, FG Wilson, Kirloskar Electric Co. Ltd., Mitsubishi Heavy Industries Ltd., Wärtsilä Corporation / MTU, Rolls‑Royce plc / MTU Onsite Energy, Denyo Co., Ltd., Yanmar Co., Ltd., Ashok Leyland Ltd., Briggs & Stratton Corporation, American Honda Motor Company, Inc., John Deere & Company, Broadcrown Generators Australia (Pty) Ltd., Wuxi Kipor Power Co., Ltd., Mahindra Powerol, and Others. |

Frequently Asked Questions

The Diesel Generator Market is expected to grow at a CAGR of 7.69% from 2026 to 2035.

Data center growth, grid unreliability, healthcare mandates, climate-related outages, and industrialization are driving strong diesel generator market expansion globally.

The 51–280 kW segment dominated the Diesel Generator Market with approximately 31.02% share in 2025.

North America dominated the Diesel Generator Market in 2025.

Get in Touch