Smart Electric Meter Market Report Scope & Overview:

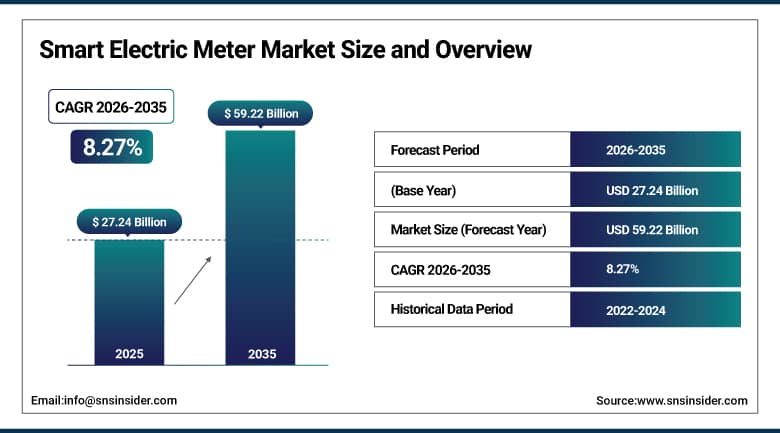

The Smart Electric Meter Market size was valued at USD 27.24 billion in 2025 and is expected to reach USD 59.22 billion by 2035, growing at a CAGR of 8.27% from 2026–2035.

The smart electric meter industry is experiencing notable growth because of higher investments in smart grid upgrades, extensive utility digitization projects, and increased adoption of systems used for real-time monitoring of energy consumption. Various utilities are now adopting advanced metering technologies that will help them ensure accurate billing, cut transmission and distribution losses, and increase grid efficiency. Governments are playing their role too as there are many government programs focused on energy efficiency, reduction of carbon footprints, and the evolution of the electric power infrastructure through digitization. Moreover, the integration of renewable energy systems, distributed generation sources, and pricing strategies is driving up the demand for advanced metering solutions.

In April 2026, leading smart electric meter manufacturers announced expanded collaborations with telecommunications and IoT platform providers to integrate NB-IoT connectivity, predictive grid intelligence tools, and cybersecurity-focused communication architectures into future smart metering deployments, supporting large-scale utility digital transformation initiatives.

Market Size and Forecast

-

Market Size 2026E: USD 28.97 Billion

-

Market Size 2035: USD 59.22 Billion

-

CAGR (2026 - 2035): 8.27%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Smart Electric Meter Market - Request Free Sample Report

Smart Electric Meter Market Trends

-

Rising AMI deployment is improving real-time energy monitoring and utility intelligence.

-

Increasing smart grid modernization is accelerating smart electric meter adoption.

-

Growing AI and cloud-based analytics integration is enhancing grid efficiency.

-

Rising NB-IoT and RF mesh adoption is improving smart meter connectivity.

-

Increasing utility digitization investments are driving global market growth.

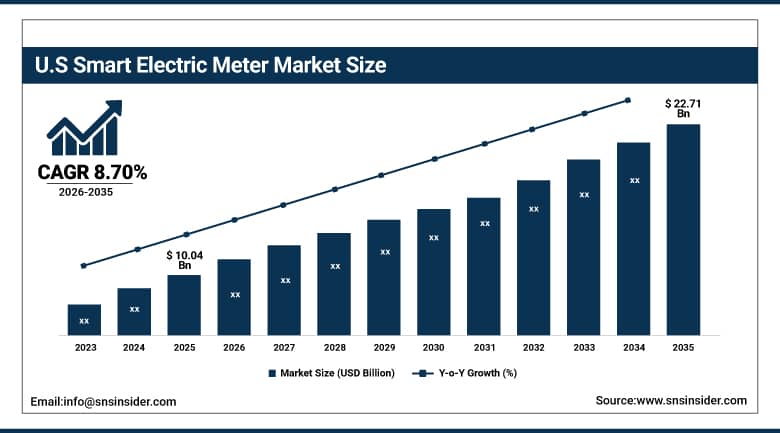

U.S. Smart Electric Meter Market Size Outlook

The U.S. Smart Electric Meter Market was valued at USD 10.04 billion in 2025 and is expected to reach around USD 22.71 billion by 2035, growing at a CAGR of 8.70% from 2026–2035. The United States enjoys a dominant market position in relation to the smart electric meter industry on account of its high number of installations of AMI systems, robust utility digitization policies, and consistent funding for smart grid modernization projects. The US has been able to gain substantial market presence for smart electric meters because of widespread installations driven by utility companies looking to increase their operational efficiency, accurate metering capabilities, ability to deal with power outages, and improved visibility over the grid. Rising demand for solutions such as real-time power consumption monitoring, automated meter reading, and demand side management is expected to drive the market ahead in the coming years.

In January 2026, major U.S. utility operators expanded smart grid modernization initiatives through next-generation AMI deployment programs integrating AI-powered outage detection, predictive analytics, and advanced energy management capabilities to improve utility operational performance and grid reliability.

Smart Electric Meter Market Segment Analysis

-

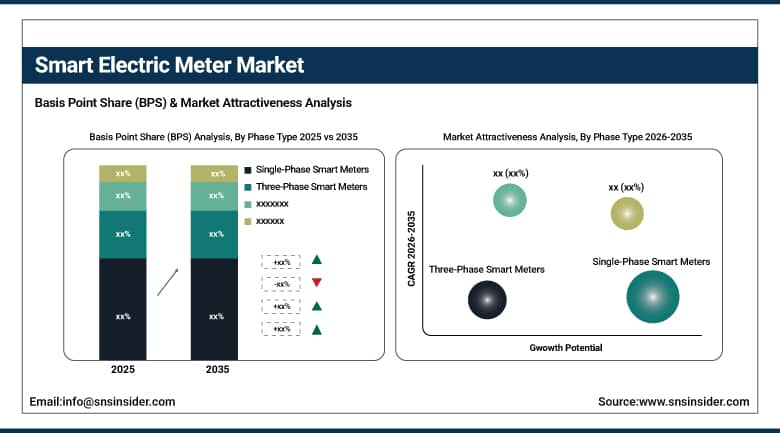

By Phase Type, single-phase smart meters dominated the market with 68.29% share in 2025; three-phase smart meters is the fastest-growing segment with the highest CAGR.

-

By Product Type, smart electricity meters dominated the market with 34.12% share in 2025; prepaid smart meters are the fastest-growing segment with the highest CAGR.

-

By Communication Technology, RF mesh dominated the market with 31.44% share in 2025; NB-IoT / LPWAN is the fastest-growing segment with the highest CAGR.

-

By Application, consumption monitoring dominated the market with 32.11% share in 2025; demand response is the fastest-growing segment with the highest CAGR.

By Phase Type, single-phase smart meters dominate the smart electric meter market, while three-phase smart meters are the fastest-growing segment.

Single-phase smart meters accounted for the highest share of about 68.29% in 2025, largely owing to their extensive usage on residential electricity supply systems around the world. Urbanization efforts, electrification projects, and installations of new smart meters continue to bolster the demand for the product. The residential users form a sizable number of electric supply connections across the globe, thus forming a substantial installed base for single-phase metering systems.

Three-phase smart meters are projected to grow at the fastest CAGR during 2026–2035, backed up by rising demand for electricity among commercial entities, industries, and highly demanding infrastructures. The rise in automation of industries, intelligent factories, commercial infrastructure growth, and power-intensive usage is driving the acceptance rate of smart meters. Such meters ensure advanced metering and better power quality management, which large users require.

By Product Type, smart electricity meters dominate the smart electric meter industry, while prepaid smart meters are the fastest-growing segment.

Smart electricity meters held the largest share of about 34.12% in 2025, owing to their extensive use within utility systems for real-time monitoring of energy usage, automatic meter reading, and efficiency improvement. Such devices constitute the most important elements of current smart grids and have been adopted extensively within homes, businesses, and factories. Utilities have started adopting such technologies in order to enhance billing processes, reduce power loss, increase visibility in grids, and better engage with customers.

Prepaid smart meters are expected to grow at the fastest CAGR during 2026–2035, motivated by the focus on revenue assurance, minimized non-technical losses, and effective payment collection methods. Prepaid metering initiatives are becoming popular among utilities in developing countries as they provide improved cash management and prevent electricity theft.

By Communication Technology, RF mesh dominates the smart electric meter market, while NB-IoT / LPWAN is the fastest-growing segment.

RF mesh accounted for the largest share of about 31.44% in 2025, as a result of its widespread use within advanced metering infrastructure (AMI) installations and in existing utility communications systems. This technology is capable of facilitating secure two-way communications, a self-healing network feature, and secure data transmission over large geographical areas. The choice of RF Mesh technology by utility companies is due to several reasons including scalability and deployment experience.

NB-IoT / LPWAN is expected to grow at the fastest CAGR during 2026–2035, as a result of growing adoption of IoT-based utility ecosystems and advanced communication technologies. Utilities have been increasingly favoring low-power communication technologies owing to their high coverage, energy efficiency, and lesser need for infrastructure investment. Rising adoption of connected utility infrastructure, remote monitoring technology, and cloud-based smart grid applications would help drive demand for NB-IoT and LPWAN communication technologies in future smart metering devices.

By Application, consumption monitoring dominates the smart electric meter market, while demand response is the fastest-growing segment.

Consumption monitoring held the highest share of 32.11% in 2025. This is because it serves as the basic function in most of the installations of smart electric meters around the world. Energy efficiency, which involves monitoring electricity usage, analyzing it, and even efficient billing mechanisms, is something that both power companies and consumers look at as a means of optimizing energy consumption. With the help of monitoring electricity patterns, power companies are able to minimize their losses, forecast demand effectively, and manage the energy consumption of consumers efficiently.

Demand response is projected to grow at the fastest CAGR during 2026–2035, driven by increasing deployment of smart grid infrastructure and intelligent energy management systems. Utility providers are increasingly leveraging demand response programs to optimize electricity load balancing, reduce peak power consumption, and improve grid efficiency.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

81.54% |

|

Europe |

Germany |

27.29% |

|

Asia Pacific |

China |

49.35% |

|

Middle East & Africa |

UAE |

27.96% |

|

Latin America |

Brazil |

35.71% |

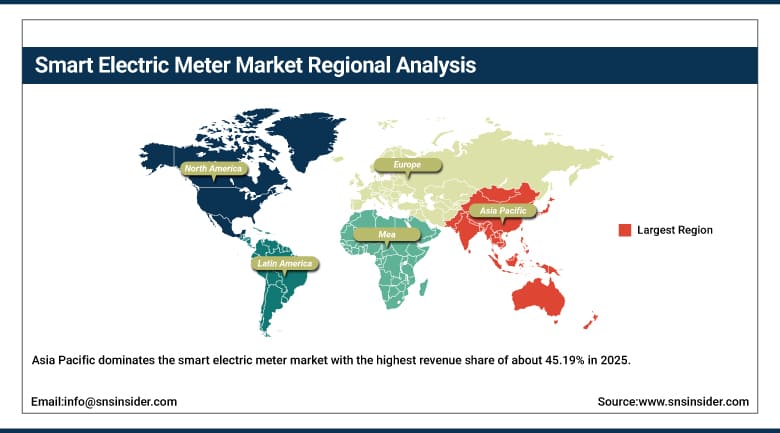

Asia Pacific Smart Electric Meter Market Insights

Asia Pacific dominates the smart electric meter industry with the highest revenue share of about 45.19% in 2025 and it is also expected to grow at the fastest CAGR of about 8.82% from 2026–2035 in the smart electric meter market, due to factors like fast-paced urbanization, rising electricity demand, and the implementation of massive smart grid projects. The countries include China, India, Japan, South Korea, and countries from Southeast Asia. They have seen huge installation of smart metering technology due to the improvement of the aging electrical system infrastructure. As well as improved electricity distribution efficiency. Due to increased growth in the industry sector, smart cities development initiatives, and government-sponsored electrification projects. Continued investments from utilities in smart grid-based AI and digital energy are driving market expansion.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Smart Electric Meter Market Insights

The North American region, owing to high levels of Advanced Metering Infrastructure (AMI) adoption, development of well-established utility eco-systems, and consistent investment in smart grid modernization projects. This is attributable to highly successful utility digitization efforts in both the U.S. and Canada, where increasing amounts of capital is being invested by power companies into sophisticated metering technologies to enhance visibility into their grids, manage outages, and operate more efficiently. Efforts towards integrating renewable energy sources, promoting energy efficiency, and upgrading utility infrastructure are helping further boost growth within this segment. Underlying this leadership position in the market are utility firms in the U.S., which are continually launching smart grid modernization initiatives on a significant scale through AMI replacement and upgrade projects. North America has achieved 72% smart meter penetration in the U.S. with over 119 million AMI meters installed, driven by large-scale utility modernization and grid automation programs.

Europe Smart Electric Meter Market Insights

The European market is regarded as the most evolved one in terms of the use of smart electric meters, mainly because of the country's ambitious agenda for carbon reduction, energy efficiency regulations, and increasing programs for the development of the smart grid. Some of the countries that have undertaken various initiatives in terms of smart metering include Germany, the UK, France, Italy, and the Nordic countries. The government support for the adoption of new energy transition policies and upgrade of old systems will continue to foster the demand in the market.

Middle East & Africa (MEA) and Latin America Smart Electric Meter Market Insights

MEA and Latin America have seen consistent growth in the smart electric meter market owing to investments being made in electricity infrastructures, urbanization projects, and utility network modernization efforts. In the case of MEA, countries like Saudi Arabia, UAE, and South Africa are involved in smart cities projects and digital utilities transformations. For Latin America, Brazil and Mexico are the major markets for which there is an investment in electrification and utility network modernization. In addition to this, smart infrastructure developments and digitization in Saudi Arabia have been making progress towards accelerating smart utilities adoption activities.

Market Dynamics:

Growth Drivers: Rising investments in smart grid modernization and utility digital transformation initiatives are accelerating deployment of smart electric metering systems

The governments and utility companies across the world have been showing an increasing interest in grid modernization projects that seek to increase the efficiency of power transmission, minimize energy loss, and provide more reliable service delivery. Smart electricity meters are gaining relevance as vital elements in the development of smart utility systems thanks to their capability of enabling real-time monitoring and metering, automatic billing, and outage detection among others. In addition, the rising demand for electricity, increasing penetration of renewable energy sources, and the need to manage energy use on the demand side are driving their adoption.

Restraints: High deployment costs and infrastructure integration complexity are limiting large-scale smart electric meter implementation across developing markets

Although there is high demand in the smart electric meter market, the implementation of smart electric meter technology may require huge capital investment linked to communication systems, software systems, power grid enhancements, and other necessary infrastructure. The upgrading of existing metering systems for small- and medium-sized energy companies could be a challenge because of limited financial resources and time to implement the changes. Moreover, the incorporation of smart meters into the existing power grid system could be difficult due to existing technological barriers. Technical difficulties, cybersecurity, and regulatory limitations in some emerging economies may limit widespread deployment.

Opportunities: Increasing integration of AI-enabled analytics and next-generation communication technologies is creating new opportunities for intelligent utility ecosystems

Fast-paced development in technologies such as artificial intelligence, IoT connectivity, cloud technologies, and predictive analytics presents many opportunities in the field of smart electric meters. Modern companies are looking for systems that will be able to provide them with real-time insights into their electricity usage, predictive maintenance abilities, and grid optimization capabilities. Deployment of new technologies like NB-IoT, LPWAN, and edge computing is also contributing to improved connectivity and scalability of the smart electric meter infrastructure. Lastly, increased spending on distributed energy sources, renewable energy, and smart city projects is driving the need for sophisticated energy management systems.

Recent Developments

-

2026: Itron Inc. expanded its smart electric meter portfolio with next-generation AMI solutions integrating AI-powered grid analytics, edge computing capabilities, and real-time outage detection systems, enabling utilities to improve demand forecasting, reduce energy losses, and enhance operational efficiency across large-scale distribution networks.

-

2026: Landis+Gyr advanced its global smart metering offerings by launching upgraded cellular and RF mesh-enabled smart electric meters with enhanced interoperability and cloud-based energy data platforms, supporting utilities in achieving faster deployment of fully digitalized metering infrastructure.

-

2025: Siemens AG introduced advanced smart electric metering solutions integrated with digital grid platforms and cybersecurity-enhanced communication systems, focusing on improving grid automation, real-time energy monitoring, and secure data transmission across smart utility networks.

-

2025: Schneider Electric expanded its EcoStruxure-enabled smart metering ecosystem by integrating AI-driven energy management tools and IoT-based monitoring capabilities, allowing utilities and industrial users to optimize electricity consumption and support decarbonization goals.

Smart Electric Meter Companies are:

-

Itron Inc.

-

Sensus (Xylem)

-

Siemens AG

-

Schneider Electric SE

-

Honeywell International Inc.

-

Aclara Technologies LLC

-

Wasion Holdings Limited

-

Holley Technology Ltd.

-

Jiangsu Linyang Energy Co., Ltd.

-

EDMI Limited

-

Iskraemeco d.d.

-

Genus Power Infrastructures Ltd.

-

CyanConnode Holdings plc

-

Zenner International GmbH & Co. KG

-

Elster Group GmbH

-

Mitsubishi Electric Corporation

-

Osaki Electric Co., Ltd.

-

Huawei Technologies Co., Ltd.

Smart Electric Meter Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 27.24 Billion |

| Market Size by 2035 | USD 59.22 Billion |

| CAGR | CAGR of 8.27% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Smart Electricity Meters, Advanced Metering Infrastructure (AMI) Meters, Automated Meter Reading (AMR) Meters, Prepaid Smart Meters, Others) • By Phase Type (Single-Phase Smart Meters, Three-Phase Smart Meters, Others) • By Communication Technology (RF Mesh, Power Line Communication (PLC), Cellular, NB-IoT / LPWAN, Others) • By Application (Consumption Monitoring, Dynamic Pricing, Grid Management, Outage Detection, Demand Response, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Landis+Gyr, Itron Inc., Sensus (Xylem), Siemens AG, Schneider Electric SE, Honeywell International Inc., Kamstrup A/S, Aclara Technologies LLC, Wasion Holdings Limited, Holley Technology Ltd., Jiangsu Linyang Energy Co., Ltd., EDMI Limited, Iskraemeco d.d., Genus Power Infrastructures Ltd., CyanConnode Holdings plc, Zenner International GmbH & Co. KG, Elster Group GmbH, Mitsubishi Electric Corporation, Osaki Electric Co., Ltd., Huawei Technologies Co., Ltd. |

Frequently Asked Questions

The smart electric meter market is expected to grow at a CAGR of 8.27% from 2026 to 2035.

The smart electric meter market was valued at USD 27.24 billion in 2025.

Rising demand from power grid modernization, smart city development, renewable energy integration, and large-scale utility digitalization projects is driving adoption of smart electric meters globally.

The smart electricity meters segment dominated the smart electric meter market in 2025.

Asia Pacific dominated the smart electric meter market in 2025.

Get in Touch