Dental 3D Printing Market Report Scope & Overview:

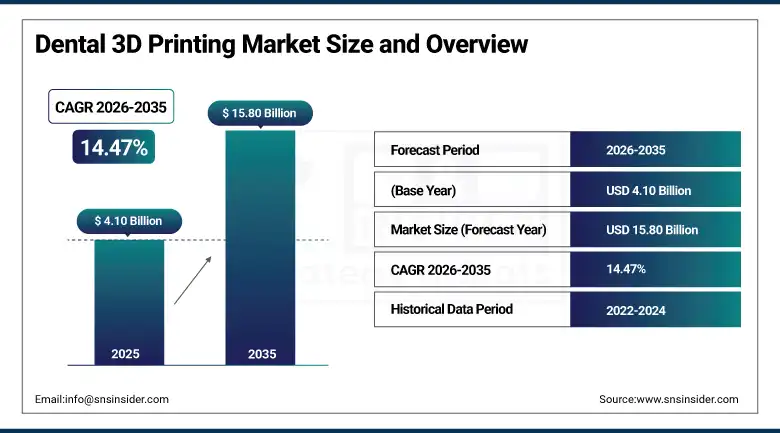

The Dental 3D Printing Market was valued at USD 4.10 Billion in 2025 and is expected to reach USD 15.80 Billion by 2035, growing at a CAGR of 14.47% from 2026 to 2035.

The advent of dental 3D printing technology is changing the economic dynamics of dental product manufacturing with the ability to manufacture patient-specific prosthetic devices, orthodontic appliances, surgical guides, and implant parts using the precision, speed, and cost-efficiency advantages of additive manufacturing in contrast to traditional subtractive manufacturing techniques and dental laboratory procedures. The integration of intraoral digital scanners, cloud-based CAD software, and highly accurate 3D printers in chairside and dental laboratory digital workflows has reduced the manufacturing lead time of customized dental restoration and surgical planning models to just a few minutes compared to several weeks previously. This process improvement has direct economic relevance in terms of improving patient flow and chair time utilization in the dental practice and laboratory turnaround times in dental laboratories. The clear aligners sector, primarily consisting of Align Technology's Invisalign product range alongside many emerging brands of clear aligner products, is currently the largest contributor to the adoption and utilization of dental 3D printing systems, accounting for millions of dental aligner model prints being manufactured every year through dental 3D printers.

Align Technology reported that its Invisalign clear aligner system generated over 15 million cumulative treated patients globally as of early 2025, with annual case volume growth driven by expanded international distribution, growing adult orthodontic treatment adoption.

Market Size and Forecast

-

Market Size in 2026E: USD 4.73 Billion

-

Market Size by 2035: USD 15.80 Billion

-

CAGR: 14.47% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Dental 3D Printing Market - Request Free Sample Report

Dental 3D Printing Market Trends

-

Growing adoption of in-house dental labs and chairside 3D printing is reducing dependence on external dental laboratories and improving workflow efficiency.

-

Advancements in biocompatible ceramic and zirconia materials are expanding 3D printing applications for permanent dental restorations.

-

AI-powered dental design software is automating crown design, implant planning, and aligner staging, improving productivity and accuracy.

-

Multi-material 3D printing is enabling simultaneous production of hard and soft dental components, simplifying denture manufacturing processes.

-

Dental 3D printing service bureaus are helping small clinics access digital manufacturing without investing in in-house printing infrastructure.

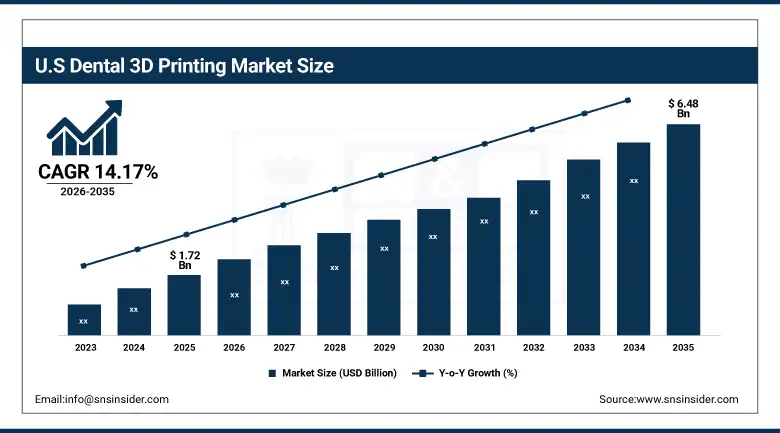

The U.S. Dental 3D Printing Market Outlook

The U.S. Dental 3D Printing Market was valued at approximately USD 1.72 Billion in 2025 and is expected to reach approximately USD 6.48 Billion by 2035, growing at a CAGR of approximately 14.17%.

The United States is the world's most commercially mature dental 3D printing market, driven by a combination of the world's most digitally advanced dental practice and laboratory ecosystem, exceptionally high consumer awareness of and demand for aesthetic orthodontic treatments, a mature clear aligner commercial market whose product manufacturing is fundamentally dependent on high-volume 3D printing, and a favourable FDA 510(k) clearance pathway that has enabled a growing number of 3D printable dental materials and device categories to achieve market authorization efficiently. The American Dental Association's support for digital dentistry technology adoption and the increasing integration of 3D printing modules into U.S. dental school curricula are building the trained practitioner base and professional cultural acceptance that sustains long-term market demand. Private equity consolidation of dental service organizations has accelerated in-house digital technology adoption across large corporate dental group practices whose economies of scale justify investment in comprehensive chairside digital workflow infrastructure including 3D printing.

Stratasys launched its J5 DentaJet multi-material dental 3D printer in expanded commercial availability across North American markets in 2025, enabling dental laboratories to simultaneously print rigid denture base materials.

Dental 3D Printing Market Segment Analysis

-

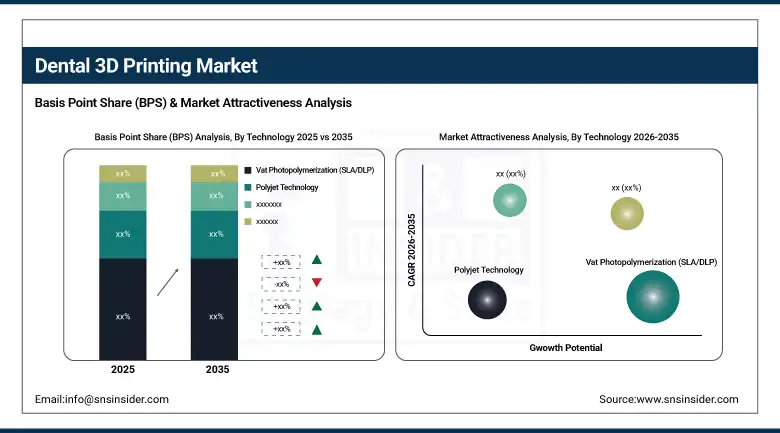

By Technology, the vat photopolymerization segment dominated the dental 3d printing market with 62.47% share in 2025, while the polyjet technology segment is the fastest growing technology during 2026 to 2035.

-

By Material, the photopolymer resins segment dominated the dental 3d printing market with 48.36% share in 2025, while the ceramics segment is the fastest growing material during 2026 to 2035.

-

By Application, the orthodontics & clear aligners segment dominated the dental 3d printing market with 42.84% share in 2025, while the dental implants segment is the fastest growing application during 2026 to 2035.

-

By End User, the dental laboratories segment dominated the dental 3d printing market with 56.73% share in 2025, while the dental clinics & practices segment is the fastest growing end user during 2026 to 2035.

By Technology, vat photopolymerization dominates, polyjet technology grows fastest

Vat photopolymerization technology, encompassing both stereolithography and digital light processing systems, generated 62.47% of dental 3D printing market revenue in 2025. Its commercial dominance reflects the technology's combination of high print resolution capable of producing the fine anatomical detail that dental prosthetics require, broad material compatibility with the photopolymer resin chemistry that constitutes the majority of clinical dental 3D printing material volume, fast print speeds relative to powder-based alternatives, and competitive system pricing that has reached accessible levels for both large laboratories and individual dental practice investment.

Polyjet technology is growing fastest, driven by its unique multi-material simultaneous printing capability that enables the single-step production of complex composite dental structures combining multiple material properties, a capability that is enabling new product categories including full-arch dentures, color-graduated crowns, and anatomically realistic diagnostic models that single-material technologies cannot efficiently produce.

By Application, orthodontics & clear aligners dominate, dental implants grow fastest

Orthodontics and clear aligner applications retained the dominant position with 42.84% of dental 3D printing revenue in 2025, reflecting the category-defining commercial success of the clear aligner treatment model whose digital manufacturing workflow is inseparable from dental 3D printing volume at industrial scale. Every clear aligner treatment case requires the production of multiple precisely printed dental models from which thermoplastic aligner sheets are thermoformed, making aligner production the highest-volume application of dental 3D printing globally.

Dental implants are growing fastest as digital implantology workflows that integrate CBCT imaging, implant planning software, and 3D-printed surgical guides progressively replace manual implant placement techniques with guided protocols that improve placement accuracy, reduce surgical complications, and enable immediate loading protocols whose clinical success rates have improved the commercial viability of comprehensive implant treatment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.62% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.73% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.47% |

North America Dental 3D Printing Market Insights

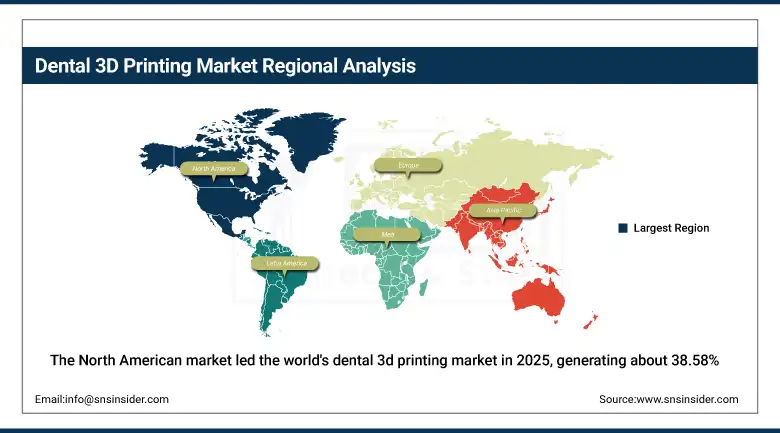

The North American market led the world's dental 3d printing market in 2025, generating about 38.58% of global revenues and the US contributing an additional 84.62% to regional revenues. North America's leading position in the market is a result of its unique confluence of a high willingness-to-pay on the part of consumers for cosmetic dental procedures, being home to the world's best developed commercial market for clear aligners, and adoption of digital workflow by its dental technology sector at rates higher than any other region in the world. Align Technology, 3Shape, Dentsply Sirona, and Envista Holdings are just some of the companies with headquarters or strong commercial operations within the region who led in R&D investments and clinical partnerships driving innovation in the field of digital dentistry.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Dental 3D Printing Market Insights

In 2025, Europe accounted for around 26.84% of total revenues in terms of Dental 3D printing in the world. The top five countries in Europe are Germany, France, the UK, Italy, and Switzerland. Each of them is home to major dental laboratories, special manufacturers in dental technologies, and quality dental schools that offer advanced training in digital technology as part of their clinical education courses. European dental laboratories boast some of the highest rates of using digital workflows worldwide. This is partly due to competition amongst their larger counterparts in adjacent countries and the profitability of using digital technology amidst a highly competitive industry. Around 28.47% of the revenue comes from Germany due to its number of dental technology manufacturers such as Dentsply Sirona and Ivoclar and its complex network of dental laboratories.

Asia Pacific Dental 3D Printing Market Insights

Asia Pacific is the region showing the highest growth rate in terms of the dental 3d printing market, set to grow at a CAGR of approximately 17.84% through to 2035. The Chinese market makes up approximately 38.73% of revenues in Asia Pacific, based on a thriving domestic dental device manufacturing industry, rapid growth in the domestic clear aligner market in line with growing dental aesthetics consciousness driven by increasing urban middle-class consumers, and strong domestic medical device manufacturing support from government policy, such as under the Made in China 2025 healthcare innovation initiative. Regional demand is significant in India, South Korea, Japan, and Australia, with the latter benefiting from a high level of sophistication in aesthetic dentistry in South Korea, and the former with its developing dental tourism industry.

MEA & Latin America Dental 3D Printing Market Insights

The Middle East and Latin America are developing regions for the dental 3d printing market due to increased investments in private dental practice, heightened consumer awareness of aesthetic dentistry, and growth in the distribution networks for clear aligner treatment, which are contributing towards larger addressable markets for digital dental manufacturing solutions. In terms of revenues, the UAE holds the largest share in the MEA region, generating around 22.84% of total revenue for the region by virtue of its premium private dental practices catering to the affluent expatriate population who desire aesthetic dental procedures with world-class quality. Brazil generates around 43.47% of total revenues in the Latin American market owing to its large population of dentists, second only to the US, and rising disposable incomes among consumers spending on aesthetic and reconstructive dental procedures.

Market Dynamics

Growth Drivers: Rising adoption of digital dentistry workflows and increasing demand for aesthetic orthodontic and restorative treatments are driving dental 3d printing market growth.

The expansion of the dental 3D printing industry is supported by the fact that the entire dental manufacturing process is irrevocably transforming into one driven by digital solutions, the economics of which work to scale favorably, while its benefits from a clinical standpoint, in comparison to traditional methods, make the decision to adopt a no-brainer. With the combination of intraoral scanning devices, dental CAD software, and 3D printers becoming a cohesive process, the economic argument becomes self-evident for any clinic or laboratory considering this technology.

High equipment costs and shortage of skilled professionals in digital dental technologies are restraining dental 3d printing market growth.

Access to the field of dental 3D printing is associated with financial investments, both in terms of purchasing printers, but also scanning hardware, dental design software licenses, post-processing equipment including UV curing systems and washing stations, as well as the training of an operational team skilled with regard to the necessary digital expertise. The total system cost involved in setting up a professional dental laboratory for 3D printing can be as high as between USD 50,000 and USD 300,000 depending on the technology and specifications involved, representing a relatively substantial financial investment which will require an adequate output of dental procedures in order to have an acceptable payback period. The speed with which dental educational institutions produce graduates capable of effectively utilizing digital technologies for dentistry has not matched the speed of demand from the private sector, posing labor force availability limitations to technology adoption.

Growth in biocompatible ceramic restorations and chairside same-day dentistry workflows is creating major opportunities in the dental 3d printing market beyond temporary dental applications.

The creation of clinically validated, regulated 3D printable ceramics that are strong enough, have adequate optical qualities, and are biocompatible for making permanent dental crowns, bridges, and veneers is one of the most important material science challenges in the field of dental 3D printing. The ability of ceramic 3D printing to provide results that are fit for a clinical environment and that meet the required standards already exists, and several companies including SprintRay, Stratasys, and Vita Zahnfabrik are working towards developing new ceramic printing materials and printers that can provide clinically cleared outputs. Once the process of ceramic 3D printing becomes regulated, it will allow the development of workflows that allow permanent crowns and bridges to be printed on the day of appointment.

Recent Developments:

-

2025: Stratasys launched commercial availability of its J5 DentaJet multi-material dental 3D printer across North American markets, enabling dental laboratories to produce composite denture structures combining multiple material properties in single print jobs and addressing a critical workflow efficiency gap in full-arch prosthetic manufacturing.

-

2025: SprintRay introduced its Pro 95 S dental 3D printer with integrated AI-guided print optimization and automated material management, reducing operator intervention in the dental 3D printing workflow and enabling continuous overnight automated production that improves laboratory throughput without additional staffing requirements.

Dental 3D Printing Market Key Players are:

-

Align Technology Inc.

-

Stratasys Ltd.

-

3D Systems Corporation

-

Dentsply Sirona Inc.

-

Envista Holdings Corporation (Ormco)

-

SprintRay Inc.

-

Formlabs Inc.

-

Carbon Inc.

-

Ivoclar AG

-

Roland DGA Corporation

-

Asiga Pty Ltd.

-

Prodways Group

-

HeyGears Ltd.

-

Planmeca Oy

-

3Shape A/S

-

Voco GmbH

-

NextDent BV (3D Systems)

-

Rapid Shape GmbH

-

Vita Zahnfabrik H. Rauter GmbH & Co. KG

-

Structo Pte Ltd.

Dental 3D Printing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.10 Billion |

| Market Size by 2035 | USD 15.80 Billion |

| CAGR | CAGR of of 14.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Vat Photopolymerization (SLA/DLP), Polyjet Technology, Fused Deposition Modelling, Selective Laser Sintering, Others) • By Material (Photopolymer Resins, Metals & Alloys, Ceramics, Dental Composites, Others) • By Application (Orthodontics & Clear Aligners, Prosthodontics & Crowns & Bridges, Dental Implants, Surgical Guides & Models, Others) • By End User (Dental Laboratories, Dental Clinics & Practices, Hospitals & Academic Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Align Technology Inc., Stratasys Ltd., 3D Systems Corporation, Dentsply Sirona Inc., Envista Holdings Corporation (Ormco), SprintRay Inc., Formlabs Inc., Carbon Inc., Ivoclar AG, Roland DGA Corporation, Asiga Pty Ltd., Prodways Group, HeyGears Ltd., Planmeca Oy, 3Shape A/S, Voco GmbH, NextDent BV (3D Systems), Rapid Shape GmbH, Vita Zahnfabrik H. Rauter GmbH & Co. KG, Structo Pte Ltd. |

Frequently Asked Questions

North America dominated the Dental 3D Printing Market in 2025, holding approximately 38.58% of global revenues.

The orthodontics & clear aligners segment dominated the Dental 3D Printing Market with 42.84% share in 2025.

The primary growth factors are the accelerating global adoption of integrated digital dentistry workflows, surging consumer demand for clear aligner orthodontic treatments that are fundamentally dependent on dental 3D printing manufacturing.

The Dental 3D Printing Market was valued at USD 4.10 Billion in 2025.

The Dental 3D Printing Market is expected to grow at a CAGR of 14.47% from 2026 to 2035.

Get in Touch