Digital Respiratory Devices Market Size & Trends:

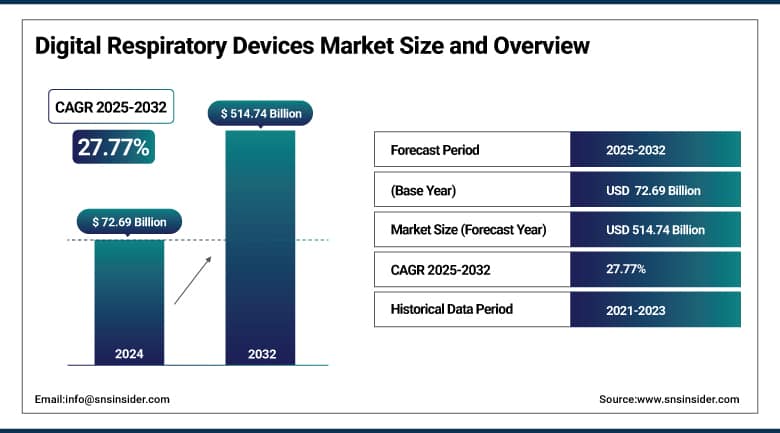

The Digital Respiratory Devices Market size was valued at USD 72.69 billion in 2024 and is expected to reach USD 514.74 billion by 2032, growing at a CAGR of 27.77% over the forecast period of 2025-2032.

The global digital respiratory devices market is driven by the increasing incidence of chronic respiratory diseases like asthma and COPD, coupled with high demand for remote patient monitoring. Smart inhalers, sensors, and mobile health apps are being integrated to improve compliance and provide effective personalized care. Better real-time data collection and patient engagement with the help of the latest technological advancements, such as artificial intelligence and Bluetooth-enabled tracking devices. Supportive reimbursement policies and digitization in the healthcare sector further enhance the growth of this market in developed as well as developing countries.

To Get More Information On Digital Respiratory Devices Market - Request Free Sample Report

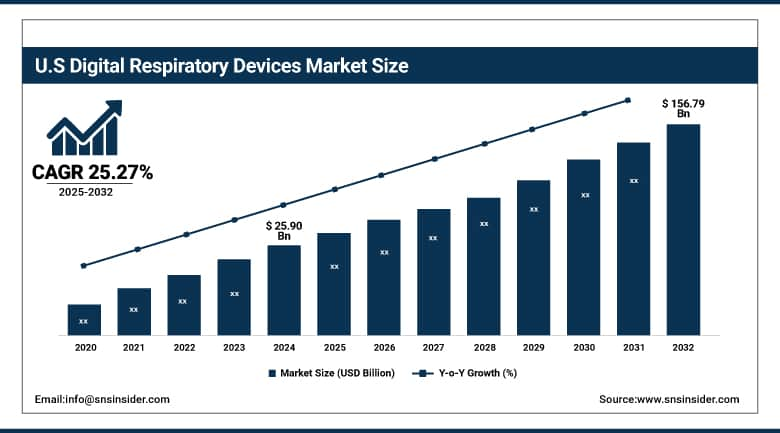

The U.S. Digital Respiratory Devices Market size was valued at USD 25.90 billion in 2024 and is expected to reach USD 156.79 billion by 2032, growing at a CAGR of 25.27% over the forecast period of 2025-2032.

The U.S. accounts for the largest percentage share of the North American digital respiratory devices market and closely followed by Canada and Mexico. The major share of the U.S. digital respiratory devices market is due to the presence of strong advanced health care infrastructure and higher prevalence of respiratory diseases such as asthma and COPD, along with the presence of key industry players in the region, including Philips, ResMed, and Cohero Health. Supportive elements, such as broader reimbursement for remote monitoring (e.g., CMS changes) and high adoption of smart inhalers and nebulizers, also reinforce U.S. regional leadership.

Digital Respiratory Devices Market Dynamics:

Drivers

-

Market Growth is Foreseen to Accelerate due to Increasing Uptake of Remote Patient Monitoring.

The growing use of digital respiratory devices is owing to the transition from hospital-based care to home-based care and telemedicine. For chronic respiratory disease patients like COPD or Asthma, connected inhalers, nebulizers, and wearable sensors provide continuous monitoring with all the data pinged to healthcare providers in real-time. That not only increases adherence to medication regimens but also gives clinicians a chance to intervene earlier, preventing emergency visits and hospitalizations. Remote monitoring is particularly beneficial for elderly patients or those residing in remote locations, further increasing global market reach.

In the U.S., use of remote patient monitoring (RPM), which encompasses both device use and its inherent data collection, is now fully reimbursable under Medicare with monthly limits. Medicaid and most major private insurers, including Cigna, Humana, and UnitedHealth, provide equivalent coverage for RPM services.

-

Technological Advancements in Digital Health Are Propelling the Market to Grow

Digital respiratory care has been transformed through innovations in IoT (Internet of Things), artificial intelligence (AI), and mobile health apps. Advancements in smart devices now mean that inhalers can record use, identify improper techniques, and communicate this data to a cloud platform available to physicians. These algorithms can identify trends and predict exacerbations, allowing for proactive care. The merger with mobile applications gives customized feedback, recommendations, and utilization information to boost self-control of the disease. These developments also allowed for better user experience, improved diagnostic accuracy, and patient outcomes that led to the wide adoption of digital respiratory technologies.

Recently, accurate respiratory monitoring beyond the walls of the clinic, including a handheld PBM Hale asthma detector developed in the UK, and artificial intelligence (AI)-enhanced tools for pediatric auscultation or lung sound analysis.

Restraint

-

The High Price of Devices and Limited Reimbursement in Emerging Markets Are Impeding the Market Growth.

The high price of smart inhalers, connected nebulizers, and integrated sensor systems is one of the main procedural constraints on the digital respiratory devices market growth. Wireless technologies, mobile apps, real-time data, and AI-driven analytics are used to create near-delivery devices that are more expensive to produce and sell.

Access is also severely restricted by either no reimbursement or non-existent reimbursement frameworks in emerging markets. In developed countries, the cost is either covered by health insurance or government schemes, but the same does not hold for developing countries, where most of the health care is out of pocket. This leads to most of the cost coming out of patients’ pockets, which, in turn, inhibits the adoption of these innovative devices. The lack of affordability of these devices, along with the absence of proper policies that support the need for OADs, presents a significant barrier for market penetration in the regions where the burden of chronic respiratory diseases, such as COPD and asthma, is increasing at a fast pace.

Digital Respiratory Devices Market Segmentation Analysis:

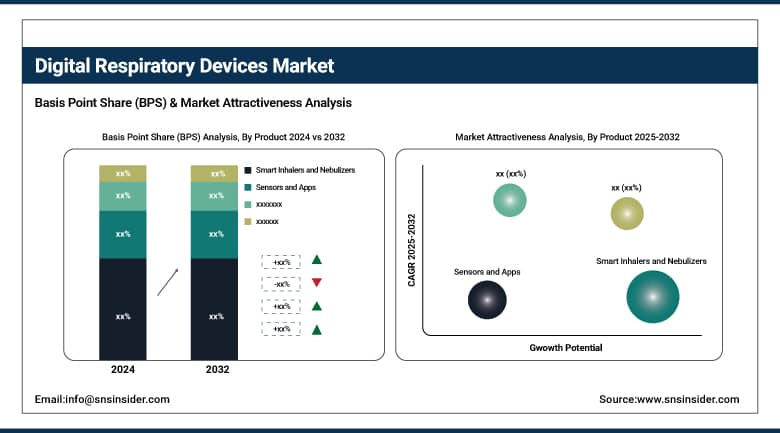

By Product

In 2024, the smart inhalers and nebulizers segment accounted for the largest market share in the digital respiratory device market, with 68.25% market share, owing to continuous application to manage chronic respiratory conditions such as asthma and COPD. Offering such things as real-time medication tracking, dosage reminders, and a link to mobile health platforms, this class of devices can lead to better medication adherence and improved patient outcomes. They were preferred as they became quickly integrated into existing treatment plans by physicians, wider used by the healthcare system to remotely monitor patients. Their use has also been propelled by regulatory approvals and increasing reimbursement in developed and emerging markets.

Owing to increasing digitalization of healthcare and growing demand for consumer desire for self-monitoring tools, the Sensors and Apps segment is expected to grow fastest throughout the forecast years. By continuously monitoring metrics such as peak flow, oxygen saturation, and breathing patterns, these technologies enable early intervention and can make treatment more personalized. Increasing use of mobile phones, an increase in telehealth services, and the development of AI-based health analysis platforms are also expected to fuel the growth of this segment. Additionally, their lower cost and scalability compared to traditional devices make them well-suited for respiratory health at the population level.

By Disease Indication

Due to the high global burden of COPD and the increasing geriatric population, the COPD segment held the largest share of the digital respiratory devices market in 2024, with a 54.2% market share. Chronic obstructive pulmonary disease (COPD) is a slowly worsening disease that needs to be monitored and managed on an ongoing basis and is thus a good candidate for digital therapies, including smart inhalers and nebulizers that are connected to the internet. Chronic obstructive pulmonary disease (COPD) is a chronic disease that affects millions of people globally, and owing to the increasing prevalence of the disease, with more hospital stays and longer treatments, healthcare providers across the globe are looking for digital respiratory solutions to lower costs and improve adherence.

The asthma segment is expected to be the fastest-growing segment during the forecasting years due to its increasing prevalence around the globe, especially among children and young adults. Digital inhalers and smartphone apps that monitor triggers, medication usage, and lung function are increasingly popular due to demand for personalized, technology-aided asthma management solutions. In addition, the increased emphasis on preventive care and rapid growth of digital health infrastructure, particularly in developing markets, is further boosting adoption. Growth of this jet is also fueled by innovations with respect to paediatric asthma care and school-based projects for respiratory health.

By Distribution Channel

The hospital pharmacies segment accounted for the largest share of the digital respiratory devices market in 2024, with 70.2% market share, owing to the critical role of hospital pharmacies in the management of acute and chronic respiratory conditions in clinical settings. These centers are the main point of delivery for complex respiratory therapies, especially in patients with severe COPD or asthma who require monitored therapy. Widespread availability of trained professionals, availability of a broad selection of medical-grade devices, and integration with hospital-based electronic health records (EHRs) for enhanced control and compliance monitoring enable superior treatment outcomes and further bolster hospital pharmacies' leadership in this segment.

The fastest growth rate is expected from the retail pharmacy segment as end-use suppliers prefer retail pharmacies due to the convenience factor provided here and growing consumer preferences for innovative accessibility solutions. Patients are infiltrating local pharmacies for smart inhalers, connected nebulizers, and app-based solutions as self-managed care lessens the need for clinical interactions and as fundamental awareness towards digital respiratory tools broadens. With increasing digital health offerings from retail chains and pharmacist-led support, users are being nudged to adhere to treatments better. High OTC availability of respiratory aids and increasing penetration in semi-urban and rural regions further substantiate the rapid growth of this distribution channel.

By End Use

The hospitals segment held the largest share of the digital respiratory devices market in the end-user segment in 2024, with a 46.12% market share, as a large number of patients are admitted to hospitals for the treatment of moderate to severe respiratory diseases, such as COPD and asthma. Hospitals are commonly the first site of care for diagnosis, initiation of emergency treatment, and monitoring ongoing treatment with connected respiratory technologies. Such facilities should have sufficient infrastructure and a trained workforce to use and analyse data from smart inhalers, nebulizers, and monitoring systems to facilitate clinical white space availability and accurate clinical decisions for optimal outcomes for patients receiving critical care.

Homecare settings are expected to show the fastest growth in the digital respiratory devices market throughout the forecast period, owing to high adoption of remote monitoring and patient-centric care. Aging Population, increasing prevalence of Chronic respiratory diseases, comfort preferences, and cost-effectiveness are pushing the patients towards home care management of this disease. The homecare segment is witnessing growth at the fastest rate due to increased portability of digital respiratory devices along with their user-friendly and cost-effective mechanism, such as Bluetooth-enabled inhalers and app-integrated nebulizers, allowing the patients to monitor their condition independently using their mobile phone.

Digital Respiratory Devices Market Regional Insights:

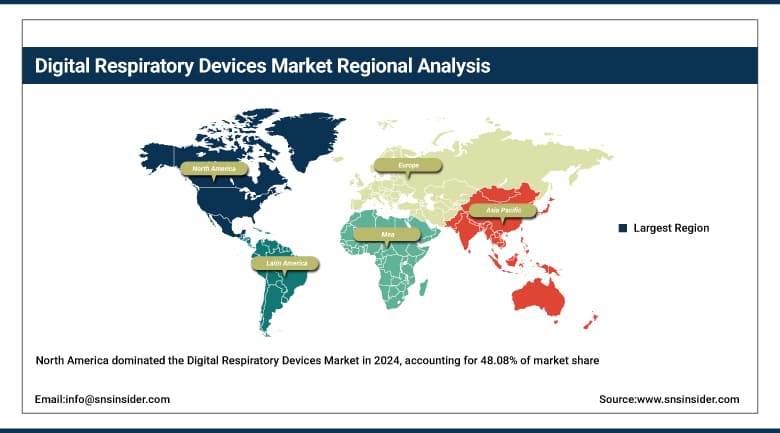

The highest share of North America in the global digital respiratory devices market is attributed to high healthcare infrastructure, awareness about digital health technologies, and a high volume of chronic respiratory conditions, including asthma and chronic obstructive pulmonary disease (COPD). North America contributed to the 48.08% market share in 2024. Furthermore, the early demand for smart inhalers, nebulizers, and remote monitoring devices is due to the high product penetration of market leaders such as ResMed, Philips, and Propeller Health. In addition, the supportive reimbursement frameworks and regulatory approvals of digital therapeutics and connected devices from the U.S. FDA enable market growth. All these factors together make North America the strongest segment in the market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Due to rising healthcare spending, increasing patient awareness, and a rapidly growing geriatric population, Asia Pacific is the fastest-growing region of the digital respiratory devices market with a 28.74% CAGR. In the globe where countries such as China, India, and Japan are experiencing a surge in respiratory diseases caused by air pollution, this is a greater need for real-time monitoring and digital intervention. Furthermore, factors such as growing internet penetration, use of telehealth platforms, and government initiatives promoting digital health solutions are also driving the demand. The region is also witnessing exponential growth spurred in part by local manufacturing capabilities and strategic partnerships with global firms bringing devices to market in the region.

The digital respiratory devices market in Europe is anticipated to witness considerable growth owing to the rising prevalence of respiratory diseases as well as the growing adoption of smart inhaler technologies in the region. Furthermore, the region enjoys the value derived from robust regulatory frameworks, environmental health policies, and public health systems that have put a systematic long-term approach for integrating digital health tools in chronic disease management, such as asthma and COPD.

The digital respiratory devices market in Latin America is exhibiting steady growth owing to the increasing healthcare infrastructure and rising prevalence of chronic diseases during the forecast period. Investment in Connected Respiratory Solutions. In particular, governments and private sectors are investing in the development of connected respiratory solutions for asthma and COPD care. Localized digital health initiatives, such as the AI-enabled inhalers and remote monitoring platforms that are proliferating through strategic partnerships, support wider adoption.

The growth in the Middle East & Africa (MEA) region is moderate, due to increasing investment in healthcare infrastructure and demand for home-based respiratory monitoring. Digital inhalers, pulse oximeters, and telehealth solutions are witnessing high penetration due to the rising incidence of respiratory diseases such as asthma and COPD. Some of the key countries driving initiatives to prevent infection and incorporate digital respiratory technologies into care pathways include the UAE, Saudi Arabia, and South Africa.

Digital Respiratory Devices Market Key Players:

Philips Respironics, ResMed Inc., Fisher & Paykel Healthcare, Medtronic plc, Drägerwerk AG & Co. KGaA, 3M Health Care, AptarGroup Inc., Cohero Health (Amiko Digital Health), Propeller Health, Sensirion AG, and other players.

Recent Developments in the Digital Respiratory Devices Market:

-

In April 2024, Medtronic launched its Touch Surgery Live Stream platform, an innovative solution that allows for the real-time streaming of laparoscopic and robotic-assisted surgical procedures. Now available in more than 20 countries, the platform aims to transform surgical education by optimizing remote training opportunities for medical professionals globally.

-

In September 2024, ResMed, the world leader in sleep, respiratory care, and home healthcare technology, announced the release of new patient-focused innovations designed to enhance the therapy experience for people with sleep apnea. The new solutions feature digital wearable integration and generative AI to provide a more personalized and powerful sleep health experience, enabling better long-term outcomes.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 72.69 Billion |

| Market Size by 2032 | USD 514.74 Billion |

| CAGR | CAGR of 27.77% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Smart Inhalers and Nebulizers, Sensors and Apps) • By Disease Indication (Asthma, COPD, Other Diseases) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) • By End Use (Hospitals, Homecare Settings, Other Settings) Diagnostic Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Philips Respironics, ResMed Inc., Fisher & Paykel Healthcare, Medtronic plc, Drägerwerk AG & Co. KGaA, 3M Health Care, AptarGroup Inc., Cohero Health (Amiko Digital Health), Propeller Health, Sensirion AG, and other players. |

Frequently Asked Questions

Ans: North America dominated the Digital Respiratory Devices Market in 2024.

Ans: The “Smart Inhalers and Nebulizers” segment dominated the Digital Respiratory Devices Market.

Ans: Technological advancements in digital health are propelling the market to grow.

Ans: The Digital Respiratory Devices Market was USD 72.69 billion in 2024 and is expected to reach USD 514.74 billion by 2032.

Ans: The Digital Respiratory Devices Market is expected to grow at a CAGR of 27.77% from 2025 to 2032.

Get in Touch