Direct Write Semiconductor Market Size & Growth:

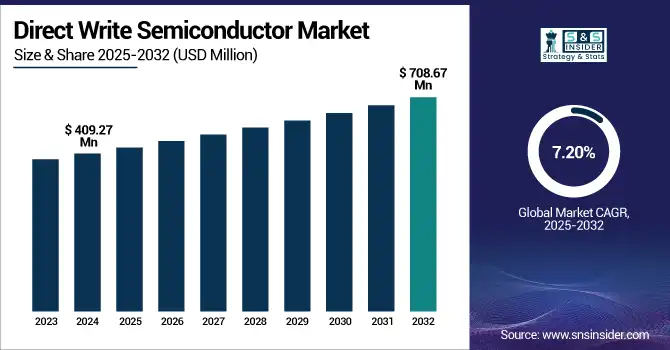

The Direct Write Semiconductor Market Size was valued at USD 409.27 million in 2024 and is expected to reach USD 708.67 million by 2032 and grow at a CAGR of 7.20% over the forecast period 2025-2032. The worldwide market for Direct Write Semiconductor is increasing with the expanding interest for the maskless lithography and high precision semiconductor parts. This technique provides flexible, low-cost prototyping for applications including IC packaging, sensor production and photonic devices. Growing tendency toward electronics and development of miniaturized devices is driving direct write semiconductor market growth globally.

To Get more information on Direct Write Semiconductor Market - Request Free Sample Report

The U.S. Direct Write Semiconductor Market size was USD 105.31 million in 2024 and is expected to reach USD 152.73 million by 2032, growing at a CAGR of 8.85% over the forecast period of 2025–2032.

The U.S. market is growing with the strong technical advancements, significant R&D investments and presence of advanced semiconductor manufacturing facilities. Growing need for miniaturized electronics and rapid prototyping from sectors, including the defense, healthcare, and bearing industries, is supporting the market growth. The market profit is driven by a skilled labour force and active support from government.

Direct Write Semiconductor Market Dynamics

Key Drivers:

-

Rising Adoption of Maskless Lithography for Rapid Prototyping Enhances the Growth of the Market.

Growing trend to maskless lithography process is the major factor to boost up the growth for the Market. This method enables a quicker design iteration, shorter time to production and lower cost in semiconductor manufacturing. Consumer electronics, aerospace, and medical device industries are using this technology from prototype to custom component. As innovation cycles accelerate, the capacity to rapidly iterate without conventional photomasks enhances market acceptance and sustained competitiveness.

Recently, JDI announced the development of eLEAP technology, the world's first OLED technology ready for mass production using maskless lithography.

Restrain:

-

Inconsistent Performance Across Diverse Substrates Limits Widespread Adoption of Direct Write Semiconductor Technology.

One of the major constraints in the Market is the variability in performance when implemented on different substrate materials like glass, metal, and composites. The ink adhesion, resolution, and electrical characteristics of different substrates can be impacted, making it challenging to guarantee consistent quality in applications. This constraint limits the flexibility of the technology and inhibits its uptake in applications demanding high reliability over multiple material types.

Opportunities:

-

Growing Integration of Direct Write Technology in Flexible Electronics Creates Lucrative Opportunities for Market Players.

Growing application of bendable and wearable electronics presents new expansion opportunities for the Market. With this technology, high-definition patterning can be achieved on a wide variety of substrates like polymers and composites necessary for compact and bendable devices. When the demand from consumers for wearable devices like smartwatches, flexible displays, and medical wearables grows, the industry finds ways to solve design complexity, performance, and size needs with direct write options providing plenty of scope for market and innovation development.

Challenges:

-

Material Compatibility and Process Standardization Pose Key Challenges to the Market Growth.

The most significant issue in the Market today continues to be consistent process standardization and compatibility with many materials. And since inks, substrates and thermal properties can vary, so too can the results and quality. These technical challenges, however, add complexity to mass deployment, and restrict the ability of the manufacturers to satisfy stringent performance and reliability requirements particularly in high-end or mission critical semiconductor applications.

Direct Write Semiconductor Market Segment Analysis:

By Process Type

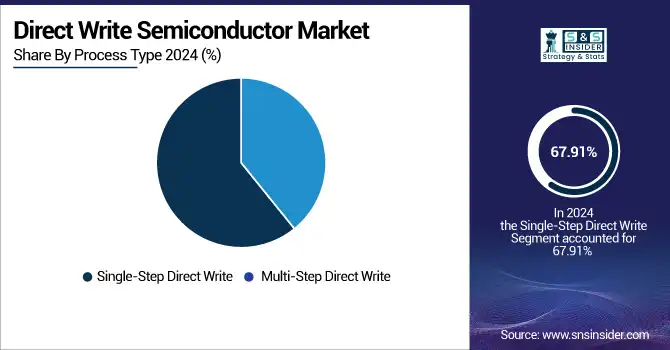

Single-Step Direct Write dominated the Market in 2024, with 67.91% revenue share. Its dominance arises due to optimized processes and minimized production times, ensuring it is the best for low-volume manufacturing as well as rapid prototyping. Optomec has been the company that has pushed this segment forward through developments such as the Aeon 3000 system, which employs femtosecond laser technology for high-resolution patterning.

The Multi-Step Direct Write segment will have the fastest growth rate of 8.31% CAGR from 2025-2032 owing to its capability of high accuracy and flexible manufacturing process of advanced semiconductor products. The method is particularly useful for applications requiring multi-layering and alignment. Direct write semiconductor market companies like Nano Dimension have been instrumental in accelerating this trend with the advancement of multi-material 3D printing that is raising the rate of production of complex electronics.

By Technology

The Electron Beam Direct Write segment dominated the highest direct write semiconductor market share of 48.11% in 2024 due to its accuracy and capacity to write high-resolution patterns in semiconductor production. The technology is highly beneficial for the production of photonic devices and integrated circuits. Raith GmbH, among other companies, has recently introduced new electron beam lithography systems that provide high speed and resolution, and electron beam technology plays a significant role in high-end semiconductor manufacturing. The expansion of this segment is critical to developing next-generation devices.

The Laser-Based Direct Write is expected to register the fastest CAGR of 8.37% during the forecast period 2025 to 2032. Fast, non-penetrating laser-based technologies, such as patterning of flexible electronics and microelectronics, are suitable for fast non-contact patterning. Recent technology development from companies such as Coherent, Inc., who introduced the RISE 3D laser printing system, are expanding the use of laser technology in semiconductor production. This is driving the market, particularly in applications such as consumer electronics and automotive, which depend on high accuracy.

By Application

IC Packaging segment dominated the largest market share of 39.04% in 2024, owing to increasing need for small and high performance chips. Direct write methods are needed, providing mask-less patterning and precision for intricate interconnects. Leading players such as Amkor Technology have scaled up their capabilities in system-in-package (SiP) and 3D packaging to make a dent in increasing outhrow of mobile and automotive electronics. The evolution of this system is indicative of the use of direct write processes in IC packaging and its ability to drive high speed, low cost assembly and miniaturization.

The Photonic Devices segment will witness the fastest CAGR of 8.82% from 2025 to 2032 in the Market. The trend is driven by increasing demand for high-speed data transmission and processing in, for example, AI and data centers. Enter TDK, which has managed to develop a new the world's first "spin photo detector" which incorporates optical, electronic, and magnetic material components to deliver ultrafast response time. These demonstrations illustrate the importance of direct write techniques in the development of photonic devices.

By Material

The Metal Inks segment dominated the Market in 2024 with a revenue share of 45.17% owing to superior electrical conductivity and printability. These inks are essential to the production of fine conductive tracks in semiconductor devices. DuPont for example, has recently gained traction in the printed electronics with a wider range of silver nanoparticle inks for improved performance in flexible circuits and RFID. These developments highlight the role of metal inks in increasing production efficiency and accuracy in direct-write technologies, which makes them unavoidable for high-speed maskless semiconductor fabrication devices.

The Ceramic Inks market will witness the fastest CAGR of 8.13% during the forecast period 2025-2032, owing to high resolutions and long-lastingness in printing for semiconductor and associated sectors. Other companies such as Ferro Corporation, have developed high-definition ceramic inks, to enable direct digital printing technology to improve quality and throughput for semiconductor devices. These developments are in response to the trend in the industry for miniaturization and complex design, and highlight the importance of ceramic inks to the development of direct write semiconductor technologies.

By Substrate

The Silicon segment dominated the maximum revenue share of 36.17% in 2024 in the Market, owing to its central positioning in microelectronics. Silicon continues to be the material of choice for semiconductor components because of its high conductivity and reliability. GlobalFoundries and other companies are still developing silicon-based chip technology, with recent emphasis on increasing production of 5nm nodes. These technologies augment the performance of direct write technologies to enable the need for more energetic, energy-efficient chips in consumer electronics and industrial uses.

The Glass segment will witness the fastest CAGR of 9.12% during 2025-2032 based on its novel combination of flexibility and strength for semiconductor production. Technological innovations from firms such as Corning Incorporated, which launched glass-based substrates for flexible displays, indicate its growing use in high-end electronics. With the rise in demand for high-performance, lightweight devices, glass substrates become a critical enabler of direct-write technology, facilitating next-generation semiconductor devices, particularly in wearable and flexible electronics markets.

Direct Write Semiconductor Market Regional Outlook:

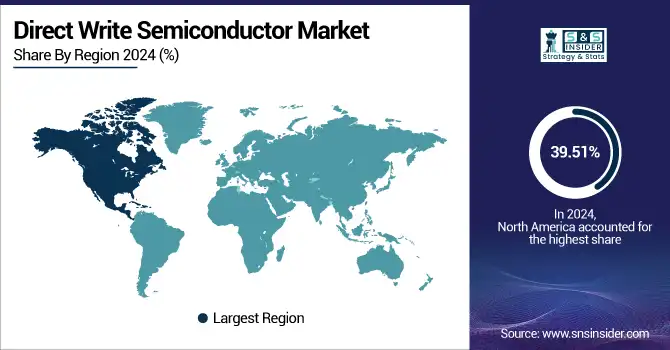

North America dominated the Market in 2024 at a 39.51% revenue share with the support of cutting-edge technological advancements in the U.S. and Canada. The region has been favored with heavy investments in semiconductor R&D, especially from players such as Intel, who have increased next-generation chip-making efforts. The CHIPS Act also strengthens the country's domestic semiconductor manufacturing, advancing direct-write technologies in packaging and component integration, positioning North America as a leader in innovation and boosting capacity in the semiconductor industry.

-

The U.S. dominated the North American Market with its sophisticated semiconductor manufacturing facilities, large R&D investments, and government incentives like the CHIPS Act. Top players such as Intel and TSMC contribute to its leadership position

Asia Pacific is expected to register the fastest CAGR of 8.77% from 2025 to 2032 on account of the rising demand for semiconductor manufacturing in China, Japan, and South Korea. Japan’s continued investment in R&D – such as its recent agreements between Rapidus Corporation and the Japanese government – highlight the technological superiority in the region. This region’s emphasis on the growth of semiconductor manufacturing plants is propelling the penetration of direct-write technologies, which is in turn driving rapid market growth, and, an increase in the production of advanced chips.

-

China is owning the Asia Pacific Market owing to the huge volume of semiconductor production in the country and strong government support for the advanced technology investments. A strong electronics sector has driven demand for direct-write solutions in literally all fields.

The Market in Europe is expanding consistently as the EU Chips Act is passed and investments in advanced manufacturing surface. Companies such as STMicroelectronics and Infineon are leading innovation, as demand increases from the automotive, renewable energy and industrial electronics markets.

-

Germany leads Europe due to the presence of a robust semiconductor industry which includes companies such as Infineon and Bosch and significant investments in automotive tech, R&D, and industrial automation.

The Latin America and Middle East & Africa regions are observing growth in the Direct Write Semiconductor Market at a steady pace, spearheaded by Brazil and the UAE, respectively. Smart city projects and defense spending in the UAE support growth, while Brazil witnesses growth supported by government industrial development schemes in its increasing electronics and automotive industry demand for semiconductors.

Get Customized Report as per Your Business Requirement - Enquiry Now

Direct Write Semiconductor Companies are:

Major Key Players in Direct Write Semiconductor Market are Samsung Electronics, Park Systems, JEOL, TEL, Veeco Instruments, Applied Materials, ASML, Canon, Tokyo Electron, Nikon and others.

Recent Development:

-

January 2025, Samsung will install its first High-NA EUV lithography machine, the ASML EXE:5000, at its Hwaseong campus, positioning it ahead of TSMC in sub-2nm chip production.

-

September 2024, Canon launched the FPA-3030i6 i-line Stepper, a semiconductor lithography system for small wafers. It features a newly developed lens, enhancing transmittance and productivity for efficient semiconductor manufacturing.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 409.27 Million |

| Market Size by 2032 | USD 708.67 Million |

| CAGR | CAGR of 7.20% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Technology (Laser-Based Direct Write, Electron Beam Direct Write, Chemical Direct Write) •By Application (IC Packaging, Photonic Devices, Sensor Fabrication, Display Fabrication) •By Material (Metal Inks, Ceramic Inks, Polymer Inks) •By Substrate (Silicon, Glass, Metal, Composite Materials) •By Process Type (Single-Step Direct Write, Multi-Step Direct Write) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Samsung Electronics, Park Systems, JEOL, TEL, Veeco Instruments, Applied Materials, ASML, Canon, Tokyo Electron, Nikon. |

Frequently Asked Questions

North America dominated the Direct Write Semiconductor Market in 2024.

Single-Step Direct Write segment dominated the Direct Write Semiconductor Market.

The major growth factor of the Direct Write Semiconductor Market is the increasing demand for miniaturized, high-performance electronic components across automotive, aerospace, and consumer electronics sectors.

The Direct Write Semiconductor Market size was USD 409.27 million in 2024 and is expected to reach USD 708.67 million by 2032.

The Direct Write Semiconductor Market is expected to grow at a CAGR of 7.20% from 2025-2032.

Get in Touch