Dolomite Market Report Scope & Overview:

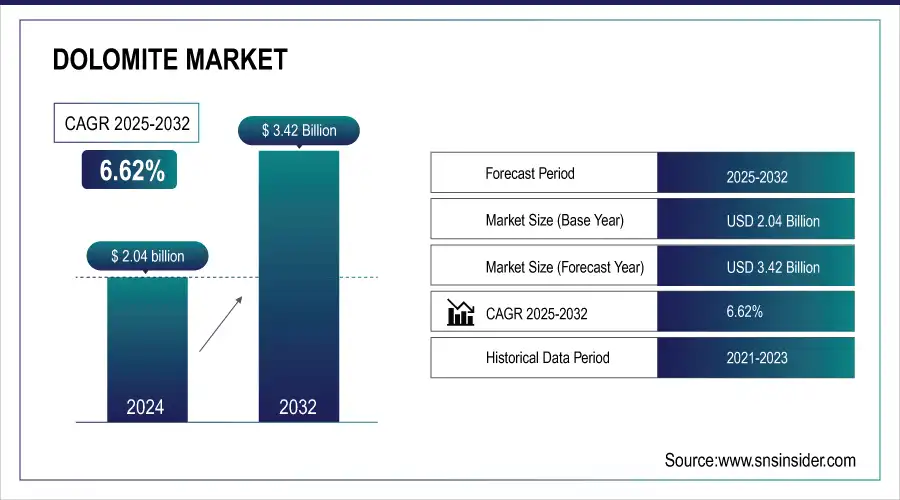

The Dolomite Market Size was valued at USD 2.04 billion in 2025E and is expected to reach USD 3.42 billion by 2033 and grow at a CAGR of 6.62% over the forecast period 2026-2033.

The dolomites market is fast-growing, with a huge number of applications due to growing demands from the construction, agriculture, and steel industries. Dolomites, being one of the most important minerals, consist of calcium magnesium carbonate that has more than one application: dolomites are used as an aggregate in the construction sector, a soil conditioner in agriculture, and a flux in the steel-making process. The development of infrastructure in newly developing economies, primarily Asian-Pacific regions, is regularly upscaling the demand for dolomites. As an example, the improvement in India's infrastructure and housing facilities, proposed by the government, has elevated the direct consumption of dolomites in cement and concrete production. Such rising construction activities are a result of a huge market demand, which will persist strongly in the years to come.

Market Size and Forecast:

-

Dolomite Market Size in 2025E: USD 2.04 Billion

-

Dolomite Market Size by 2033: USD 3.42 Billion

-

CAGR: 6.62% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

Get more information on Dolomite Market - Request Sample Report

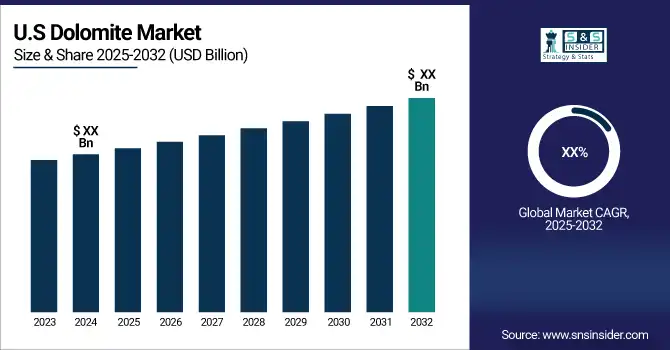

The U.S. Dolomite market size was valued at an estimated USD 0.75 billion in 2025 and is projected to reach USD 1.25 billion by 2033, growing at a CAGR of 5.8% over the forecast period 2026–2033. Market growth is driven by increasing demand for dolomite in construction, glass, ceramics, and steel manufacturing, as well as its growing use as a raw material in agriculture and chemical industries. Rising infrastructure development, urbanization, and industrial production in the U.S. further support market expansion. Additionally, technological advancements in mining and processing, coupled with sustainable practices and strong participation from leading domestic manufacturers, contribute to the steady growth outlook of the U.S. dolomite market during the forecast period.

Key Dolomite Market Trends

-

Increasing demand in the construction industry as a key ingredient in cement, concrete, and building materials.

-

Growing use in steel and iron manufacturing as a fluxing agent to remove impurities.

-

Rising adoption in glass manufacturing to improve clarity and durability.

-

Expansion in chemical and agricultural applications, including fertilizers and pH control agents.

-

Increasing demand in environmental applications such as wastewater treatment and flue gas desulfurization.

-

Growing use in refractories and ceramics for high-temperature stability and thermal resistance.

-

Technological advancements in calcination and grinding processes improving product quality and efficiency.

-

Rising interest in sustainable mining practices and eco-friendly production methods to meet environmental regulations.

Dolomite Market Growth Drivers

-

Increased Demand for Construction Materials Boosting Dolomites Market Growth

The growth of the construction industry is one of the main impelling factors pushing the dolomites market. With a rapid urbanization process prevailing globally, especially in emerging economies, there has been an increased demand for quality building materials. Dolomites are mainly used primarily because of their unique properties across various construction applications, which are significant aggregates for concrete, for soil stabilization, and as constituents in cement production. Dolomites can be used to strengthen construction materials, hence their popularity with builders and contractors. For instance, in India and China, the governments' infrastructure development activity has spurtted massive consumption of dolomite in road and bridge building works. Dolomites also act as an effective substitute for other, more environmentally destructive materials. This trend towards environment-friendliness in the industry adds to the popularity of dolomites as the construction material of choice. This trend encourages dolomite sourcing by construction companies for both performance and regulatory requirements. Larger firms, such as Carmeuse and Lhoist Group, expand their dolomite production to cater to this increasing demand more conclusively enforcing the mineral's role in modern construction practice, thus securing its market growth.

-

Agricultural Applications Driving Increased Utilization of Dolomites

A growing application of dolomites in agricultural uses, especially as soil conditioners and fertilizers fuels the growth of the market. Farmers are slowly realizing that healthy soils are essential for yields of crops and how to farm sustainably. Some much-needed nutrient resources present in dolomites include calcium and magnesium. They neutralize acidic soils and, hence, improve availability of nutrients to the plant. There also seems to be an improvement in agricultural structures, and facultative microbial activity, and its contributions lead to healthier crops. Presently, dolomites are finding their way as a solution to various acidity problems of soil in parts of Southeast Asia and South America. For example, Omya AG produces specific specialized products of dolomite for agricultural purposes, showing the versatility of dolomites. The awareness of organic farming and sustainable agriculture is on the rise, and dolomites are increasingly being used as eco-friendly substitutes for chemical fertilizers. With growing food production requirements worldwide, usage of dolomites in agriculture will rise, thus becoming one of the primary driving forces in the overall dolomites market.

Dolomite Market Restraints

-

Price Volatility of Raw Materials Presents Challenges for Producers

Price volatility in raw materials is an important constraint within the dolomites market. That puts huge pressure on the low cost of producers and, of course, maintains profitability. Operations costs involved with dolomite extraction and processing are high: mining, transportation, and processing. Price fluctuations in such involuntary inputs as energy and labor impact the cost structure for dolomite producers. Higher such raw material prices will result in increased costs for the producers, making them increase their selling price, which in turn reduces competitiveness, particularly with applications in construction and agriculture. Moreover, volatile pricing would create uncertainty in demand as end-users may opt for alternative materials if the pricing of dolomite becomes excessively high. Companies in this market need to address these fluctuations through different hedging strategies: for example, spreading the supplier base, streamlining production processes to minimize possible volatility in input costs, or investing in technologies that minimize the usage of volatile inputs. Without sound risk management, raw material price volatility is always going to be an important challenge for the producers in the Dolomites market.

Dolomite Market Opportunities

-

Innovations in Dolomite-Based Products Offer New Market Opportunities

The ever-increasing innovations in dolomite-based products can be a significant opportunity for growth in the market for dolomites. Further, as specific industries search for specialized solutions for their applications, producers now primarily target the development of high-performance dolomite products that might meet their performance standards. Along with purification, particle size, or other surface modifications for reactivity, dolomites are now more used for their industrial applications. These are some of the examples where advances in processing technologies are being used to generate special dolomites for industries for glass and ceramics. These industries require very pure and consistent quality, and companies like Minerals Technologies Inc are investing in research and development with new products for the various dolomites that would fill a gap in the market according to the needs of specific applications. The trend toward sustainable and eco-friendly materials further accelerates innovation, for which manufacturers are looking to innovate in new applications, thus creating opportunities in dolomites for green building materials and agricultural solutions. Manufacturers will be able to capitalize on emerging opportunities and enhance their competitive positioning in the dolomites market by making product development consistent with market trends and sustainability initiatives.

Dolomite Market Challenge:

-

Environmental Regulations Challenge Dolomites Production Practices

Growing environmental regulations that further limit the ecological footprint of mining activities are becoming significant pressures for the dolomites market. Increasing awareness of sustainable development throughout the world translates into more limiting regulatory policies. Companies in this market would be forced to devise practices that reduce their environmental footprint. Mining activities should conform to different environmental regulations, from the need to carry out an extensive environmental impact assessment to environmentally friendly extraction activities. These requirements may also imply a significant operational cost rise for dolomite producers since the investment will be in technology and procedures that prevent or minimize environmental destruction. The measures of compliance may seriously burden smaller operators and further freeze their chances of fair market competition. Failure to comply with the requirements would lead to severe penalties, legal battles, and reputational damage, giving further complexity to the operational landscape. Thus, companies of Dolomites will have to be proactive about adaptability in their practices and strategies that meet the principle of evolution in regulations while keeping mining sustainable and responsible. Environmentally responsible practices can also lead to opportunities for differentiation since companies position themselves ahead of environmentally conscious markets in the future.

Dolomite Market Segment Analysis

By Product

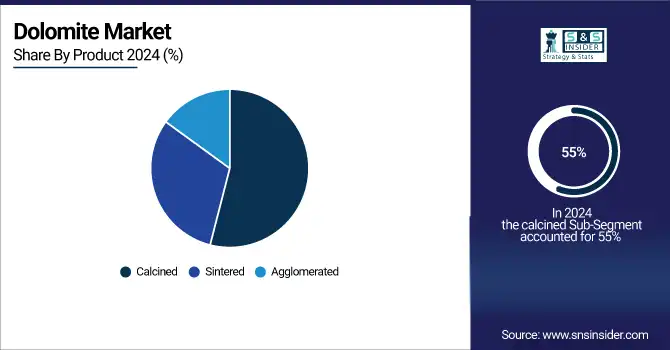

The calcined dolomites segment dominated the dolomites market and accounted for nearly 55% market share in 2025. Calcined dolomites are the outcome of heating raw dolomite to extremely high temperatures and are applied mainly to various applications, which include steel production, glass manufacturing, and refractory. Their high purity level and specific chemical properties make them applicable to varied industrial operations. For instance, the calcined dolomite in steel production serves as a flux that helps eliminate impurities and, hence, improves the quality of the final product. The demand for high-quality aggregates and binders from the construction industry also added a supporting force to the development of the calcined segment. Companies such as Carmeuse Lime & Stone have heavily invested in the production of calcined dolomites to cater to the huge requirements that have been witnessed across these sectors, forming the leading role in the dolomites market.

By End-use

In 2025, iron and steel dominated the dolomites market and accounted for an estimated market share of 40% in the dolomites market. This is because the dolomites play a crucial role in the steel-making process, which acts as a flux eliminating impurities from iron ore thereby further enhancing the quality of the produced product. Demand for Steel Related to Infrastructure Development and High-Speed Urbanization Thus, has been strong enough to underpin this segment. For instance, large steel manufacturers like Tata Steel and ArcelorMittal have scaled up their capacity and have instead centered their production on the dolomites to increase the value of their production operations. In addition, the growth in the automotive and building sectors currently is also an influence, which, in turn, fuels the high steel demand and fuels the market share of the iron and steel segment of the dolomites.

Dolomite Market Regional Analysis

Asia Pacific Dolomite Market Insights

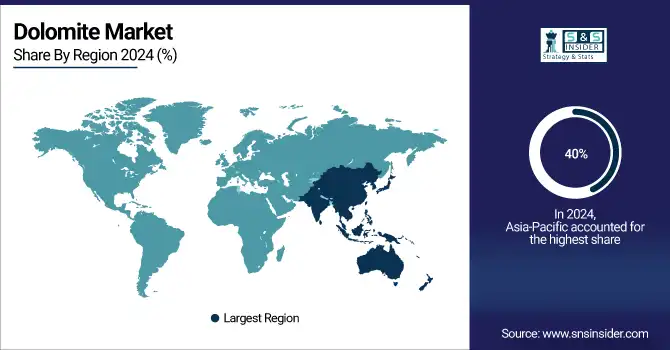

In 2025, the Asia-Pacific region dominated the dolomites market and accounted for a revenue share of about 40%. This is due to the strong construction and industrial sectors of the region, primarily China and India. China is one of the largest cement-producing regions and is also a significant player concerning construction activity, with tremendous demands for dolomites. Dolomites are important for cement production as well as other construction materials. More recently, dolomites have also been accepted in the agricultural field in India as a soil conditioner and fertilizer, thus contributing to this increasing demand for dolomites. Omya and Carmeuse have strengthened their presence in the region with greater production capacity to meet the said demand. Further, the government initiative towards infrastructure improvement and urbanization in developing economies would also continue to drive this consumption of dolomites in the Asia-Pacific region.

Get Customized Report as per your Business Requirement - Request For Customized Report

North America Dolomite Market Insights

However, the North American region emerged as the fastest growing region in the dolomites market, with an estimated CAGR of about 6% in 2025. This is due to an increase in sustainable construction trends and the demand for high-quality building materials in the United States and Canada. This shift in construction material change in North America is gradually and increasingly focusing on green materials, and hence, dolomites are growing in their demand due to properties and minimizing environmental damage. Moreover, the region is vigorously pursuing infrastructure development projects that pertain primarily to renewable energy projects and smart cities, thereby high demand for dolomite in various applications such as construction on roads and water treatment applications. Key players in the region consisting of the U.S. Silica and Graymont, are investing in advanced dolomite production technologies. This is to cater to the growing demand of the market. With increased recognition of the benefits of dolomites, North America is expected to grow lucratively for the next few years.

Europe Dolomite Market Insights

The Europe dolomite market is witnessing steady growth in 2025, driven by increasing demand from the construction, steel, and glass industries. Key markets such as Germany, France, and the U.K. are adopting dolomite in cement, concrete, and refractory applications due to its durability and cost-effectiveness. Environmental regulations promoting sustainable raw materials and eco-friendly manufacturing processes are further supporting market growth.

Latin America (LATAM) Dolomite Market Insights

The Latin America market is expanding steadily in 2025, supported by growth in the construction and agricultural sectors. Brazil, Mexico, and Argentina are key markets where dolomite is increasingly used in cement production, soil amendment, and steel manufacturing. Rising infrastructure investments and urbanization are fueling the adoption of dolomite-based products across the region.

Middle East & Africa (MEA) Dolomite Market Insights

The MEA dolomite market is gaining momentum in 2025, driven by the demand from steel, glass, and chemical industries. Countries such as Saudi Arabia, UAE, and South Africa are investing in dolomite for refractory products, water treatment, and pH control applications. Growth is further supported by expanding industrialization, government initiatives for sustainable raw materials, and increasing import of high-quality dolomite for specialized applications.

Dolomite Market Competitive Landscape

Dolomite (DeFi Platform)

Dolomite is a decentralized finance (DeFi) platform enabling asset lending and trading on blockchain networks.

-

In April 2024, DeFi lending protocols were launched on X Layer, OKX's Ethereum-based Layer 2 network, boosting Dolomite's asset lending functionalities and placing it in the number four lending market within the Arbitrum environment.

-

In February 2024, Dolomite was deployed on the Arbitrum DEX within the Polygon zkEVM ecosystem. Initially, it only accepted transactions denominated in ETH, USDC, WETH, and MATIC, with plans to add more tokens later.

RHI Magnesita

RHI Magnesita is a global leader in refractory products and solutions for the steel and non-ferrous industries.

-

In January 2023, RHI Magnesita acquired an effective majority stake in Jinan New Emei Industries Co. Ltd., expanding its portfolio of steel flow control refractory products and further increasing manufacturing capacity in China and East Asia.

Dolomite Market Key Players

-

Calcinor (calcined dolomite, dolomitic lime)

-

CARMEUSE (calcined dolomite, dolomitic lime)

-

Essel Mining & Industries Limited (EMIL) (dolomite lumps, dolomite powder)

-

Imersys S.A. (natural dolomite, calcined dolomite)

-

JFE Mineral & Alloy Company, Ltd. (dolomite pellets, calcined dolomite)

-

Lhoist (lime, dolomitic limestone)

-

Omya AG (dolomite powder, calcined dolomite)

-

RHI Magnesita (magnesia-dolomite, dolomite refractory)

-

Sibelco (ground dolomite, crushed dolomite)

-

VARDAR DOLOMITE (industrial dolomite, agricultural dolomite)

-

ACG Materials (dolomitic limestone, ground dolomite)

-

Buehler (dolomite granules, calcined dolomite)

-

Graymont (quicklime, dolomitic lime)

-

Huber Engineered Materials (ground dolomite, calcined dolomite)

-

Martin Marietta (dolomitic limestone, crushed dolomite)

-

Minerals Technologies Inc. (precipitated dolomite, dolomite powder)

-

Nordic Mining (natural dolomite, calcined dolomite)

-

Schaefer Kalk (calcined dolomite, dolomitic lime)

-

U.S. Silica (dolomite sand, ground dolomite)

-

W. R. Grace & Co. (dolomitic hydrate, dolomite powder)

-

Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 2.04 billion |

| Market Size by 2033 | USD 3.42 Billion |

| CAGR | CAGR of 6.62 % From 2026 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Calcined Dolomite, Agglomerated Dolomite, and Sintered Dolomite) |

| •By End-Use (Iron & Steel, Construction, Glass & Ceramics, Water Treatment, Agriculture, Others) | |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Calcinor, Carmeuse, Essel Mining & Industries Limited (EMIL), Imersys S.A., JFE Mineral & Alloy Company, Ltd., Lhoist, Omya AG, RHI Magnesita, Sibelco, Vardar Dolomiteand other players |

Frequently Asked Questions

Ans: North America is expected to hold the largest market share in the global Dolomite Market during the forecast period.

Ans: Factors such as rising in the construction sector drives the growth of dolomite market

Ans: The calcined product type segment will grow rapidly in the Dolomite Market from 2026-2033.

Ans: The expected CAGR of the global Dolomite Market during the forecast period is 6.62%.

Ans: The Dolomite Market was valued at USD 2.04 billion in 2025.

Get in Touch