Hydrophilic Coating Market Report Scope & Overview:

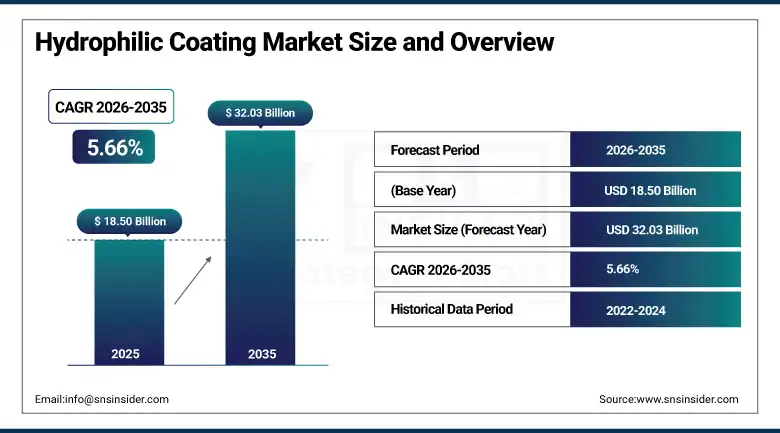

The Hydrophilic Coating Market was valued at USD 18.50 Billion in 2025 and is expected to reach USD 32.03 Billion by 2035, growing at a CAGR of 5.66% from 2026–2035.

The Hydrophilic Coating Market is growing steadily owing to rising needs for minimal invasive procedures and medical devices, including catheters, guidewires, and stents, which have greater requirements for lubricity and biocompatibility. Rise in incidence rates of cardiovascular diseases, urological problems, and neurological disorders is yet another factor behind the growing demand for medical devices with hydrophilic coating. In addition, technological developments in coatings, their usage in aerospace and automobiles industries, and development of healthcare infrastructure will contribute towards market growth.

In 2024, DSM-Firmenich (now Envalior) launched its Hydak next-generation medical device hydrophilic coating with enhanced lubricity, durability, and biocompatibility certification for cardiovascular catheter, guide wire, and endoscopic instrument applications. The product reflects the commercial direction of medical-grade hydrophilic coating development toward application-specific formulations whose clinical performance validation, regulatory dossier support, and biocompatibility testing create differentiated commercial value that commodity hydrophilic coating alternatives cannot match in the FDA-regulated medical device supply chain.

Hydrophilic Coating Market Size and Forecast

-

Market Size in 2026E: USD 19.55 Billion

-

Market Size by 2035: USD 32.03 Billion

-

CAGR: 5.66% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Hydrophilic Coating Market - Request Free Sample Report

Hydrophilic Coating Market Trends

-

Rising demand for minimally invasive medical devices driving adoption of hydrophilic coatings to reduce friction and improve patient comfort during procedures

-

Growing use of hydrophilic coatings in catheters, guidewires, and other interventional devices to enhance maneuverability and procedural efficiency

-

Increasing focus on infection prevention and biocompatibility encouraging the development of advanced coating technologies for medical applications

-

Expanding applications in automotive, optical, and industrial sectors where anti-fogging, lubrication, and surface wettability properties are required

-

Continuous advancements in coating formulations and application techniques improving durability, performance, and long-term adhesion on diverse substrates

U.S. Hydrophilic Coating Market Outlook

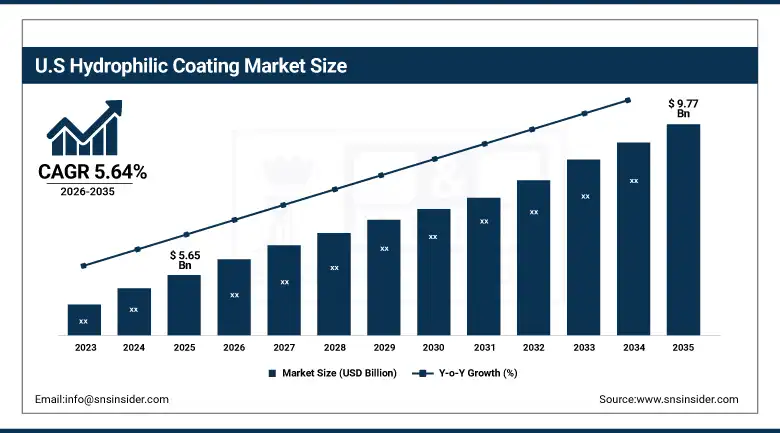

The U.S. Hydrophilic Coating Market was valued at approximately USD 5.65 Billion in 2025 and is expected to reach approximately USD 9.77 Billion by 2035, growing at a CAGR of approximately 5.64%.

The U.S. Hydrophilic Coating Market is driven by rising demand for minimally invasive procedures, increasing prevalence of cardiovascular and urological diseases, and expanding use of advanced medical devices. Strong healthcare infrastructure, technological advancements in coating materials, and growing focus on patient safety and device performance are further supporting market growth.

In 2023, Surmodics received expanded FDA clearance for its SERENE hydrophilic coating system for complex cardiovascular catheter applications, demonstrating durability retention after 120 cm of simulated coronary artery navigation without coating delamination or particle shedding.

Hydrophilic Coating Market Segment Analysis

-

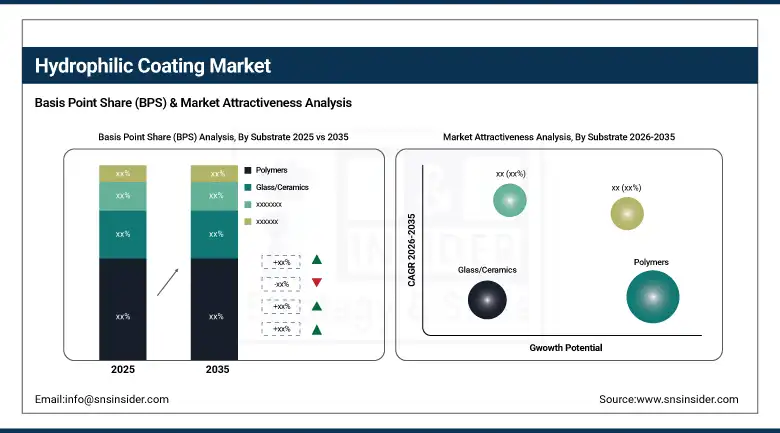

By Substrate, Polymers segment dominated the Hydrophilic Coating Market in 2025 with 48% share; Nanoparticles segment is the fastest growing segment.

-

By Application, Medical devices & equipment segment dominated the market in 2025 with 52% share; Aerospace segment is the fastest growing segment.

By Substrate, polymers segment dominates the hydrophilic coating market, while nanoparticles segment is the fastest-growing segment

The Polymers segment dominated the Hydrophilic Coating Market in 2025 owing to the broad application of polymers in medical devices, industrial equipment, and consumer goods. Polymer substrates have high flexibility, high adhesion strength, and better compatibility with coatings, thereby rendering them highly suitable substrates for creating hydrophilic surfaces. High cost-efficiency and easy mass production make them highly adopted by manufacturers across the world. The rising preference for substrates that can improve surface performance, particularly in medical and diagnostic devices, further propels their dominant market share.

The Nanoparticles segment is the fastest growing on account of increasing demand for advanced coatings with superior performance. Nanoparticle substrates increase surface performance parameters such as wettability and antifouling characteristics; hence, they find a wide range of applications in next-generation products used in medicine and aerospace. Furthermore, increased investment in R&D activities related to nanoparticle-based substrates propels the demand for them. Besides, the requirement for substrates with high precision and longevity drives market growth.

By Application, medical devices & equipment segment dominates the hydrophilic coating market, while aerospace segment is the fastest-growing segment

The Medical devices & equipment segment dominated the Hydrophilic Coating Market in 2025 because of high demand for biocompatible hydrophilic coatings that facilitate efficient device functioning, increase comfort level, and decrease procedure time during minimally invasive surgery. High incidence rates of various chronic conditions and increasing number of surgeries contribute to growth in demand. Stringent regulations in the area of medical devices safety and innovations within the field are other factors that support the segment's leading position in healthcare applications.

The Aerospace segment is the fastest growing as the rising adoption rate of hydrophilic coatings in aircraft parts increases their operational performance, reduces the impact of friction, and provides increased environmental resistance. Rising awareness regarding the importance of fuel economy and weight reduction in aviation promotes demand for surface modifications. The growing production in this area and increasing investments in modernization are additional factors that support the segment's high CAGR. Continuous development in coating technologies is another factor that contributes to rapid adoption.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Hydrophilic Coating Market Insights

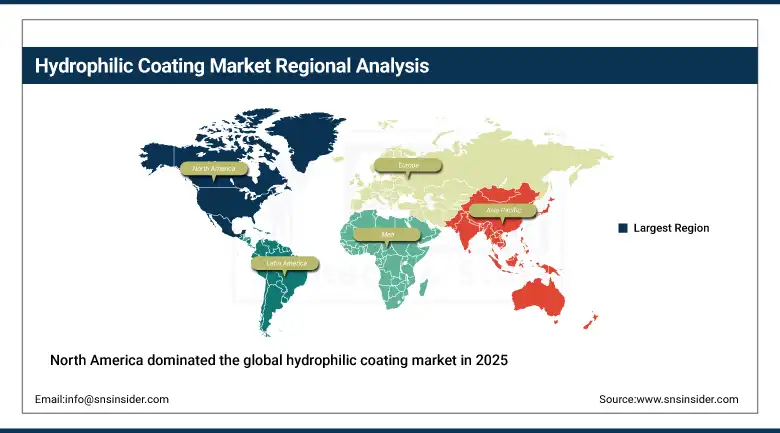

North America dominated the global hydrophilic coating market in 2025 driven by the advanced medical device industry’s coating procurement, the automotive sector’s ADAS sensor coating investment, and the commercial presence of Surmodics, DSM Biomedical (Envalior), Harland Medical Systems, and Biocoat. The United States accounts for approximately 87.4% of North American revenues through its FDA-regulated medical device coating market and the ADAS coating procurement growth.

According to the U.S. Centers for Disease Control and Prevention (CDC), cardiovascular disease causes approximately 695,000 deaths annually in the country, highlighting the scale of treatment needs that rely on interventional procedures.

Additionally, the National Institute of Neurological Disorders and Stroke (NINDS) reports that a stroke occurs roughly every 40 seconds in the United States, reinforcing the high utilization of catheter-based thrombectomy devices, many of which depend on hydrophilic coatings to enhance flexibility, navigation, and patient outcomes during critical neurological interventions.

Canada contributes approximately 12.6% of North American revenues through its automotive manufacturing sector’s hydrophilic surface treatment, the medical device industry’s coating procurement, and the optical industry’s anti-fog application investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Hydrophilic Coating Market Insights

Europe is a technically sophisticated hydrophilic coating market where REACH regulation compliance, the automotive OEM sector’s ADAS and anti-rain glass coating investment, and the medical device industry’s EU MDR-regulated coating procurement create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive sector’s above-average sensor coating investment, BASF and Evonik’s specialty chemical expertise, and the medical device manufacturing sector’s coating material procurement.

According to the European Society of Cardiology (ESC), cardiovascular diseases cause over 1.7 million deaths annually across Europe, accounting for approximately 32% of total deaths, which drives extensive use of interventional cardiology devices. Furthermore, Eurostat reports that EU hospitals perform millions of interventional procedures each year, with percutaneous cardiovascular and endovascular interventions emerging as one of the fastest-growing surgical categories.

Additionally, the European Association of Urology (EAU) notes that urinary tract disorders affect over 50 million Europeans annually, significantly increasing the use of catheters and guidewires where hydrophilic coatings are essential for reducing friction, improving device navigation, and minimizing patient trauma during procedures.

The Netherlands, France, and Switzerland are significant secondary markets where DSM-Firmenich’s (Envalior’s) Dutch operations, the pharmaceutical and medical device industry’s coating material procurement, and the optical industry’s anti-fog lens coating investment create consistent commercial demand.

Asia Pacific Hydrophilic Coating Market Insights

Asia Pacific is the fastest-growing regional hydrophilic coating market, driven by China’s extraordinary electronics and automotive manufacturing scale creating ADAS sensor coating demand, Japan’s precision optical industry’s anti-fog coating procurement, South Korea’s medical device manufacturing, and India’s growing automotive sector.

According to the World Health Organization (WHO), cardiovascular diseases cause over 10 million deaths annually in Asia, while stroke cases in the region account for nearly 60% of global incidence, highlighting the urgent need for advanced interventional and emergency care procedures.

China accounts for approximately 44.8% of Asia Pacific revenues through its automotive and electronics manufacturing scale, the growing medical device export industry’s coating procurement, and the domestic anti-fog glass and optical coating market.

Similarly, the National Health Commission of China states that more than 330 million people in China are affected by cardiovascular diseases, with a rapid expansion of interventional cardiology centers across tier-2 and tier-3 cities, collectively driving strong demand for hydrophilic coatings in medical device applications.

In India, the Ministry of Health and Family Welfare reports that cardiovascular diseases contribute to approximately 28% of total deaths, alongside a rapid increase in catheter-based procedures across tertiary care hospitals.

Japan represents a technically sophisticated secondary market where precision optical lens anti-fog coating, advanced medical device hydrophilic coating, and the automotive electronics sector’s ADAS surface treatment create consistent above-average per-application commercial value.

MEA & Latin America Hydrophilic Coating Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its petrochemical industry’s pipeline coating application, the growing healthcare sector’s medical device procurement, and Vision 2030’s industrial manufacturing investment creating new facilities.

Brazil leads Latin American revenues at approximately 44.2% through its automotive manufacturing sector’s ADAS coating procurement, the growing medical device industry’s catheter coating demand, and the optical sector’s anti-fog application investment. UAE’s solar panel anti-soiling hydrophilic coating adoption and South Africa’s mining equipment coating demand collectively sustain regional market growth through 2035.

Market Dynamics

Growth Drivers: Medical device minimally invasive procedure expansion and ADAS sensor surface coating mandate creating structured procurement

Medical device minimally invasive procedure expansion is the hydrophilic coating market’s most commercially certain structural growth driver. Each new cardiovascular intervention programme, endoscopic procedure category, and minimally invasive surgical approach that adopts lubricious hydrophilic-coated catheter and instrument systems creates commercial coating procurement whose aggregate across global procedural volume growth compounds with the minimally invasive procedure market’s extraordinary expansion. The demonstrated patient benefit of reduced insertion force, diminished tissue trauma, and improved procedural success rates that hydrophilic coated devices create sustains premium coating specification in clinical procurement.

ADAS sensor surface coating requirement is simultaneously creating above-average automotive hydrophilic coating demand as camera, LiDAR, and radar sensor performance reliability in adverse weather conditions creates structured specification investment from automotive OEMs whose NCAP safety rating and regulatory compliance depends on sensor performance consistency in rain, fog, and moisture conditions.

Restraints: High cost of regulatory validation for medical applications and eco-solvent transition investment

Medical-grade hydrophilic coating regulatory validation’s ISO 10993 biocompatibility testing, FDA submission documentation, and clinical performance durability demonstration creates above-commodity development investment whose cost creates barriers for smaller coating suppliers seeking market entry in the premium medical device coating category. Each new coating formulation requiring full biocompatibility assessment creates 12-24 month validation timelines whose cost moderates the pace of medical-grade product portfolio expansion.

Transition from solvent-based to water-based hydrophilic coating formulations creates process engineering investment for industrial coating operations whose equipment modification, process revalidation, and quality system updates create transition cost that moderates the adoption pace of eco-friendly alternatives despite regulatory and sustainability motivation.

Opportunities: Automotive ADAS coating and self-cleaning nanostructured surface development

Automotive ADAS optical surface coating represents the most commercially dynamic near-term growth opportunity whose mandatory ADAS feature adoption across vehicle segments creates coating procurement that compounds with global vehicle production. Each ADAS camera and sensor whose fog-free, rain-free optical performance creates vehicle safety system reliability improvement creates hydrophilic coating procurement whose scale grows with ADAS penetration.

Self-cleaning nanostructured hydrophilic surface coating represents the most commercially premium emerging opportunity whose solar panel efficiency maintenance, building glass self-cleaning, and medical device surface decontamination applications create above-commodity commercial relationships whose functional performance premium sustains above-standard pricing in premium application categories.

Recent Developments:

-

2024: DSM-Firmenich (Envalior) launched its Hydak next-generation medical device hydrophilic coating in 2024 with enhanced lubricity, durability, and biocompatibility certification for cardiovascular catheter, guide wire, and endoscopic instrument applications.

-

2024: Surmodics launched its P1H hydrophilic coating platform in 2024 with enhanced mechanical adhesion for complex catheter shaft geometry, enabling lubricious coating retention on braided and coiled catheter constructions that conventional dip-coating approaches cannot consistently coat.

-

2024: Biocoat expanded its Hydromer-based hydrophilic coating services in 2024 with new PFAS-free lubricious coating formulations for catheter and guide wire medical device manufacturers responding to regulatory pressure on per- and polyfluoroalkyl substance elimination in medical device coatings.

-

2023: Surmodics received expanded FDA clearance in 2023 for its SERENE hydrophilic coating system for complex cardiovascular catheter applications, demonstrating durability retention after 120 cm of simulated coronary artery navigation without coating delamination or particle shedding.

-

2023: Harland Medical Systems launched an enhanced UV-cure hydrophilic coating process line in 2023 for high-volume catheter coating with reduced cure cycle time, improved coating uniformity, and enhanced lubricity consistency compared to thermal cure predecessor coating processes.

Hydrophilic Coating Market Key Players

-

Surmodics, Inc.

-

Biocoat Incorporated

-

Harland Medical Systems, Inc.

-

Hydromer, Inc.

-

Aculon, Inc.

-

AST Products, Inc.

-

DSM Biomedical (dsm-firmenich)

-

Covalon Technologies Ltd.

-

Specialty Coating Systems, Inc. (SCS)

-

Freudenberg Medical, LLC

-

Teleflex Incorporated

-

Medtronic plc

-

Becton, Dickinson and Company (BD)

-

Terumo Corporation

-

Boston Scientific Corporation

-

Cook Medical

-

Integer Holdings Corporation

-

Nordson MEDICAL

-

Mitsubishi Chemical Group Corporation

-

Abbott Laboratories

Hydrophilic Coating Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.50 Billion |

| Market Size by 2035 | USD 32.03 Billion |

| CAGR | CAGR of 5.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Substrate (Polymers, Glass/Ceramics, Metals, Nanoparticles, Others) • By Application (Aerospace, Automotive, Marine, Medical devices & equipment, Optical, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Surmodics, Inc., Biocoat Incorporated, Harland Medical Systems, Inc., Hydromer, Inc., Aculon, Inc., AST Products, Inc., DSM Biomedical (dsm-firmenich), Covalon Technologies Ltd., Specialty Coating Systems, Inc. (SCS), Freudenberg Medical, LLC, Teleflex Incorporated, Medtronic plc, Becton, Dickinson and Company (BD), Terumo Corporation, Boston Scientific Corporation, Cook Medical, Integer Holdings Corporation, Nordson MEDICAL, Mitsubishi Chemical Group Corporation, Abbott Laboratories. |

Frequently Asked Questions

The Hydrophilic Coating Market is expected to grow at a CAGR of 5.66% from 2026 to 2035.

The Hydrophilic Coating Market was valued at USD 18.50 Billion in 2025.

Minimally invasive medical device expansion and automotive ADAS safety systems are driving hydrophilic coating demand growth.

Polymers dominated the Hydrophilic Coating Market with approximately 48% share in 2025, while Nanoparticles is the fastest growing segment.

North America dominated the Hydrophilic Coating Market in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch