Education Technology Market Report Scope & Overview:

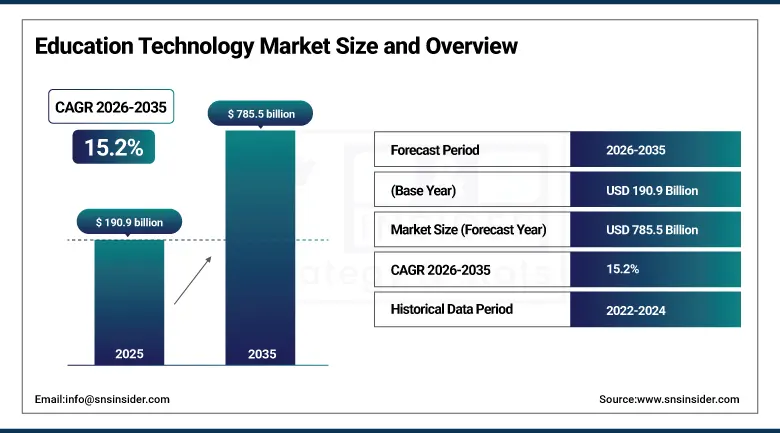

The Education Technology Market was valued at USD 190.9 Billion in 2025 and is expected to reach USD 785.5 Billion by 2035, growing at a CAGR of 15.2% from 2026–2035.

The global education technology (EdTech) market is transforming learning delivery across institutional, corporate, and individual contexts through digital platforms that integrate intelligent tutoring, adaptive content, virtual classrooms, learning management systems, and immersive simulation into flexible, personalised, and measurably more effective learning experiences than traditional classroom instruction can efficiently provide at scale. Artificial intelligence integration is fundamentally upgrading EdTech’s commercial value proposition by enabling real-time learner performance assessment, adaptive content sequencing, automated essay grading, and predictive at-risk student identification whose combined capability creates demonstrably superior learning outcomes that sustain growing institutional procurement. Rising smartphone penetration enabling mobile-first learning in emerging markets, government-mandated digital education infrastructure investment following the COVID-19 pandemic’s demonstration of remote learning feasibility, and corporate workforce reskilling urgency driven by technological job displacement collectively sustain the market’s exceptional growth trajectory.

In February 2024, Google for Education introduced AI-driven features to Google Classroom, including automated assignment creation, intelligent plagiarism detection, and personalised student progress monitoring dashboards that enable teachers to identify struggling students earlier and differentiate instruction more effectively across large classroom populations. The enhancement demonstrated Google’s strategy of embedding generative AI capability directly within its widely deployed education platform infrastructure, progressively elevating Google Workspace for Education’s competitive differentiation versus Microsoft 365 Education and specialist LMS providers in institutional procurement decisions.

Market Size and Forecast

-

Market Size in 2026E: USD 219.9 Billion

-

Market Size by 2035: USD 785.5 Billion

-

CAGR: 15.2% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

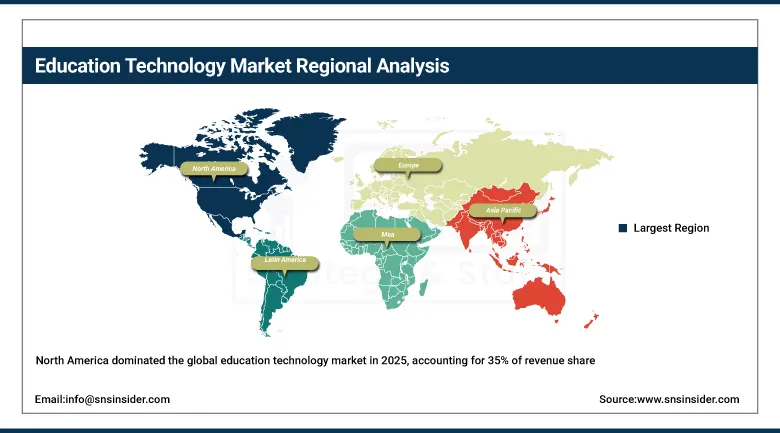

Largest Region: North America

To Get more information on Education Technology Market - Request Free Sample Report

Education Technology Market Trends

-

Generative AI integration in learning platforms is enabling automated content creation, personalised tutoring, and real-time formative assessment at classroom scale.

-

Immersive learning through AR and VR is expanding from healthcare and engineering simulation into mainstream K-12 science, history, and STEM educational applications.

-

Micro-credentialing and digital badging platforms are replacing traditional degree pathways for workforce reskilling as employer hiring criteria increasingly prioritise demonstrated skills.

-

Learning analytics dashboards are enabling institutions to identify at-risk students earlier and measure instructional intervention effectiveness with data-driven precision.

-

Mobile-first EdTech platforms are extending quality digital education access to learners in Sub-Saharan Africa, Southeast Asia, and South Asia without fixed broadband infrastructure.

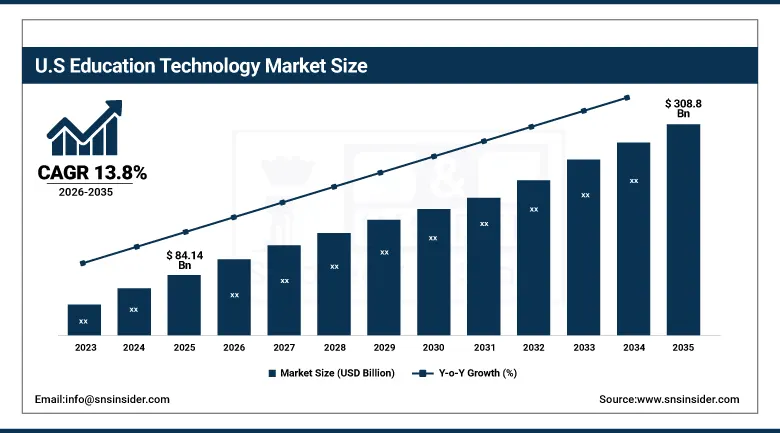

The U.S. Education Technology Market Outlook

The U.S. Education Technology Market was valued at approximately USD 84.14 Billion in 2025 and is expected to reach approximately USD 308.8 Billion by 2035, growing at a CAGR of approximately 13.8%.

The United States leads global EdTech revenues through the world’s most commercially developed digital learning ecosystem, the highest enterprise corporate training investment per employee, and sustained federal and state government digital education infrastructure funding. Coursera, Pearson, McGraw-Hill, Instructure Canvas, and Anthology Blackboard sustain platform leadership across higher education and K-12 markets. Title I and E-Rate government funding programmes create structurally large public school digital learning procurement above commercial market dynamics, reinforcing domestic EdTech market scale through non-discretionary institutional investment.

In January 2024, Coursera expanded its AI-powered learning tools, enhancing personalised course recommendations for its 148 million registered learners worldwide through large language model-driven adaptive learning path generation that sequences content based on individual learner proficiency assessment, career goal alignment, and prior learning history. The enhancement demonstrated Coursera’s strategy of deploying generative AI as a retention and completion rate improvement tool whose commercial impact on subscription revenue depends on its ability to demonstrate measurably better learner outcomes versus undifferentiated catalogue access.

Education Technology Market Segment Analysis

-

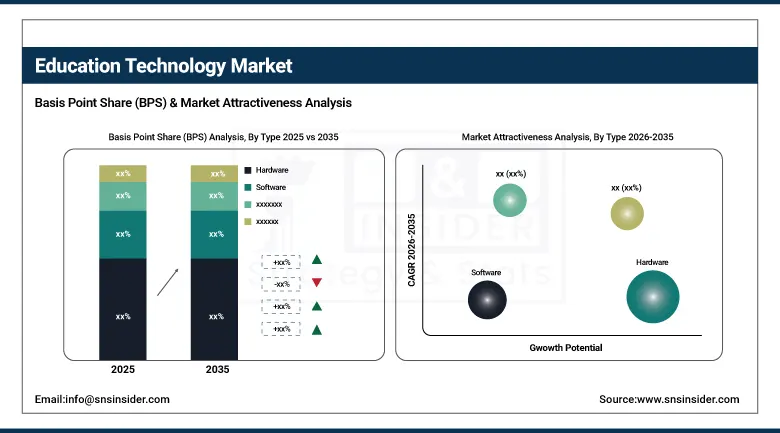

By Type, hardware segment dominated the education technology market with approximately 44.0% share in 2025, while the content segment is the fastest growing type with a CAGR of approximately 16.5% driven by personalised, interactive, and AI-driven learning material demand.

-

By Sector, the K-12 segment dominated the education technology market with the largest share in 2025, while the preschool segment is the fastest growing driven by early childhood digital learning adoption.

-

By Deployment, cloud-based segment dominated the education technology market with the largest share in 2025 and is also the fastest growing, driven by subscription economics, remote accessibility, and continuous platform update advantages.

By Type, hardware dominates, content grows fastest

Hardware retained the dominant type position with approximately 44.0% of the education technology market in 2025. Its commercial primacy reflects the foundational role of physical learning devices whose procurement represents the largest single-category capital expenditure in institutional EdTech investment. Interactive flat panel displays replacing whiteboards, Chromebook and tablet deployments for 1:1 student device programmes, smart projectors, and AR/VR headset rollouts for immersive learning collectively create hardware procurement budgets whose per-institution scale substantially exceeds software licence and content subscription equivalents. Government-funded K-12 device programmes, whose COVID-19 pandemic response created unprecedented device procurement through E-Rate and emergency connectivity fund disbursement, established a hardware installed base requiring refresh cycles that sustain above-baseline hardware demand across the planning horizons of institutional technology administrators.

Content is the fastest-growing type at approximately 16.5% CAGR because the generative AI revolution is creating an entirely new commercial category of AI-generated adaptive content whose personalisation, interactivity, and real-time assessment integration capabilities far exceed what human-authored static digital content libraries provide. Each educational publisher, platform operator, and independent content creator that deploys generative AI for content production, interactive exercise generation, and adaptive assessment item creation multiplies content output velocity while expanding the personalisation dimension of digital learning materials from one-size-fits-all curricula toward individually responsive instructional pathways.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

United Kingdom |

24.8% |

|

Asia Pacific |

China |

42.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Education Technology Market Insights

North America dominated the global education technology market in 2025, accounting for 35% of revenue share through its mature EdTech ecosystem, world-leading university system’s digital learning adoption, and the largest enterprise corporate training investment base globally. The United States accounts for approximately 82.5% of North American revenues through its concentration of EdTech platform leaders including Coursera, Chegg, Instructure Canvas, Anthology, and Pearson whose U.S. headquarters and primary customer relationships sustain domestic market leadership.

Canada contributes supplementary North American revenues through its well-funded public university sector’s LMS and digital learning tool procurement, the growing corporate training market’s D2L Brightspace and other Canadian-headquartered EdTech platform adoption, and the provincial government’s digital education initiative investment across K-12 systems whose classroom technology upgrade programmes create consistent hardware and software procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Education Technology Market Insights

Europe is a commercially significant EdTech market where strong public university systems, active corporate training cultures, and progressive government digital education strategy investment create diverse and growing demand. The United Kingdom accounts for approximately 24.8% of European revenues through its world-leading university sector’s online learning adoption, the Ufi VocTech Trust’s vocational EdTech investment, and the concentration of global EdTech companies’ European headquarters in London and Dublin whose commercial activities serve the continent’s institutional and corporate markets.

Germany’s dual vocational education system’s digital transformation investment, France’s Mon Compte Formation individual training account creating consumer EdTech demand, and the Netherlands’ advanced corporate learning culture collectively sustain European EdTech market development. The European Commission’s Digital Education Action Plan 2021–2027 whose member state implementation creates structured government funding for digital learning infrastructure sustains institutional procurement above purely commercial demand drivers.

Asia Pacific Education Technology Market Insights

Asia Pacific is the fastest-growing regional Education Technology Market with a CAGR of approximately 16.5%, driven by the world’s largest student population, rising smartphone and internet penetration enabling mobile-first learning, and government-led digital education initiatives across China, India, South Korea, and Japan. China accounts for approximately 42.8% of Asia Pacific revenues through its enormous K-12 and higher education technology market, the progressive regulatory environment for private EdTech following sector restructuring, and government digital campus investment across the national university system.

India represents the most commercially dynamic emerging EdTech market within Asia Pacific, where the National Education Policy’s digital learning emphasis, rapidly growing middle class’s investment in children’s education, and the world’s largest English-language online learner population create EdTech demand that PhysicsWallah, Unacademy, and international platforms compete to serve. South Korea and Japan contribute premium regional demand through their advanced educational technology cultures and substantial enterprise corporate training markets.

MEA & Latin America Education Technology Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its world-class digital education infrastructure investment, the Knowledge and Human Development Authority’s smart learning initiative, and the Mohammed Bin Rashid Smart Learning Programme’s nationwide K-12 EdTech deployment. Saudi Arabia’s Vision 2030 education digitisation and the large student population across Gulf Cooperation Council member states create consistent institutional EdTech procurement.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its large higher education and corporate training markets, the government’s national digital education platform investment, and the growing consumer EdTech adoption among Brazil’s large middle class whose investment in professional development and English language learning creates sustained platform subscription demand. Mexico and Colombia are growing secondary markets whose expanding university systems and corporate training sectors create above-regional-average EdTech adoption momentum.

Market Dynamics

Growth Drivers: Generative AI integration transforming personalised learning delivery and government digital education mandates creating structured institutional EdTech procurement

The education technology market’s exceptional growth rate is driven by the generative AI revolution’s transformation of what digital education platforms can deliver, where the combination of adaptive content personalisation, real-time learning analytics, and conversational AI tutoring creates a learning experience whose effectiveness advantage over traditional instruction is increasingly measurable and demonstrable to institutional procurement decision-makers. Each educational institution that documents improved student outcomes from AI-powered EdTech deployment creates a reference case that accelerates peer institution procurement decision timelines, creating a self-reinforcing adoption cycle. Government digital education mandates adopted in response to the COVID-19 pandemic’s demonstration of remote learning feasibility, particularly across Asia, Latin America, and Africa where significant new digital education infrastructure investment was committed, create structured institutional procurement above purely commercial demand.

Restraints: Digital equity gaps limiting EdTech access in low-connectivity communities and educator technology adoption barriers constraining effective implementation

EdTech’s commercial potential is constrained by the persistent digital equity divide between well-resourced institutions whose technology infrastructure enables platform deployment and under-resourced schools in low-income communities and developing countries whose bandwidth limitations, device shortages, and teacher technology capability gaps prevent effective digital learning implementation. Each student in a low-connectivity classroom who cannot access cloud-based adaptive learning platforms due to bandwidth constraints represents a market penetration limitation whose resolution requires infrastructure investment that EdTech commercial revenue cannot fund independently. Teacher technology adoption barriers, where pedagogical discomfort with digital tools, platform training time constraints within already demanding teaching schedules, and resistance to algorithmic student assessment create implementation gaps between platform procurement and classroom deployment, represent a structural EdTech market development constraint.

Opportunities: AI-powered tutoring as a teacher supplement and corporate workforce reskilling investment creating the largest near-term EdTech market expansion categories

AI-powered tutoring systems whose conversational interface, adaptive assessment, and personalised explanation capability provides learners with one-to-one tutoring equivalents at the marginal cost of compute rather than human tutor hourly rates represent the most commercially transformative EdTech capability whose accessibility at smartphone scale creates a global addressable market spanning every student population regardless of institutional resource level. Governments, NGOs, and commercial EdTech platforms whose AI tutoring deployment can demonstrably narrow achievement gaps and improve standardised test outcomes create procurement and investment motivation whose commercial scale could exceed the entire current EdTech market within the decade.

Recent Developments:

-

2024: Google for Education introduced AI-driven features to Google Classroom including automated assignment creation, intelligent plagiarism detection, and personalised student progress monitoring dashboards, embedding generative AI capability within its widely deployed education platform for institutional K-12 and higher education markets.

-

2024: Coursera expanded its AI-powered learning tools for its 148 million registered learners, deploying LLM-driven adaptive learning path generation that sequences content based on individual proficiency assessment, career goal alignment, and prior learning history to improve completion rates and learning outcomes.

-

2024: Microsoft introduced Copilot for Education within Microsoft 365 Education, providing AI-assisted lesson planning, differentiated instruction material generation, and student writing support tools that integrate with Teams for Education and OneNote deployed across millions of students and educators globally.

Education Technology Market Key Players are:

-

Apple Inc.

-

Microsoft Corporation

-

Google LLC (Google for Education)

-

Pearson PLC

-

McGraw-Hill Education

-

Coursera Inc.

-

Duolingo Inc.

-

Chegg Inc.

-

Instructure Inc. (Canvas LMS)

-

Anthology Inc. (Blackboard)

-

D2L Corporation (Brightspace)

-

Cengage Group

-

Turnitin LLC

-

Kahoot! ASA

-

Articulate Global Inc.

-

Adobe Inc. (Adobe Education Exchange)

-

Docebo Inc.

-

Skillsoft Corporation

-

Think & Learn Pvt. Ltd. (BYJU’S)

-

PhysicsWallah Pvt. Ltd.

Education Technology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 190.9 Billion |

| Market Size by 2035 | USD 785.5 Billion |

| CAGR | CAGR of 15.2% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sector (Preschool, K-12, Higher Education, Others) • By Type (Hardware, Software, Content) • By Deployment (Cloud-Based, On-Premises) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Apple Inc., Microsoft Corporation, Google LLC (Google for Education), Pearson PLC, McGraw-Hill Education, Coursera Inc., Duolingo Inc., Chegg Inc., Instructure Inc. (Canvas LMS), Anthology Inc. (Blackboard), D2L Corporation (Brightspace), Cengage Group, Turnitin LLC, Kahoot! ASA, Articulate Global Inc., Adobe Inc. (Adobe Education Exchange), Docebo Inc., Skillsoft Corporation, Think & Learn Pvt. Ltd. (BYJU’S), and PhysicsWallah Pvt. Ltd. |

Frequently Asked Questions

The Education Technology Market is expected to grow at a CAGR of 15.2% from 2026 to 2035.

The Education Technology Market was valued at USD 190.9 Billion in 2025.

Generative AI integration transforming personalised learning delivery, government digital education mandate investment, corporate workforce reskilling urgency, and mobile-first EdTech access expansion in emerging markets are the primary growth factors.

The Hardware segment dominated the Education Technology Market with approximately 44.0% share in 2025.

North America dominated the Education Technology Market in 2025 with 35% revenue share.

Get in Touch