Electronic Skin Market Report Scope & Overview:

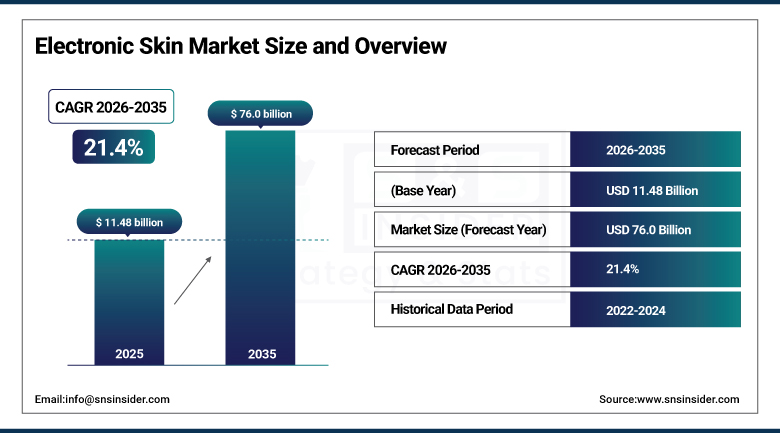

The Electronic Skin Market was valued at USD 11.48 billion in 2025 and is expected to reach USD 76.0 billion by 2035, growing at a CAGR of 21.4% from 2026-2035.

The growth of the electronic skin market is attributed to the increase in the demand for wearable health monitoring devices, developments in flexible electronics and stretchable electronics technology, and increased use in robotics and artificial limbs. The increase in the application of remote patient monitoring, human machine interface technology, and AI-based sensors contributes to the growth of the market.

The U.S. Department of Health and Human Services reported a 15% rise in chronic disease prevalence among adults from 2020 to 2024, directly increasing demand for continuous health monitoring devices. The FDA cleared 30% more wearable medical devices utilizing electronic patches between 2021 and 2024, reflecting accelerating regulatory acceptance of this technology category.

Electronic Skin Market Size and Forecast

-

Market Size in 2025: USD 11.48 Billion

-

Market Size by 2035: USD 76.0 Billion

-

CAGR: 21.4% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Electronic Skin Market - Request Free Sample Report

Electronic Skin Market Trends

-

Ultra-thin nanomesh organic field-effect transistors enabling breathable, long-wear electronic skin that can be worn continuously without the discomfort that earlier rigid-substrate patches caused.

-

Self-powered electronic skin devices harvesting energy from human sweat, body heat, and motion are eliminating battery dependence that previously constrained deployment duration.

-

AI integration in e-skin sensor networks is enabling real-time pattern recognition that identifies clinically significant physiological events from the continuous data streams these devices generate.

-

Integration of electroactive polymers capable of changing shape or size under electrical stimulation is enabling haptic feedback e-skin for robotic prosthetic limbs and teleoperation systems.

-

Cosmetic applications including microcurrent face masks and electronic beauty devices are creating a consumer market for e-skin technology beyond clinical and industrial applications.

-

Advances in biocompatible encapsulation materials are extending the operational lifetime of implantable e-skin devices, making multi-year continuous monitoring applications clinically feasible.

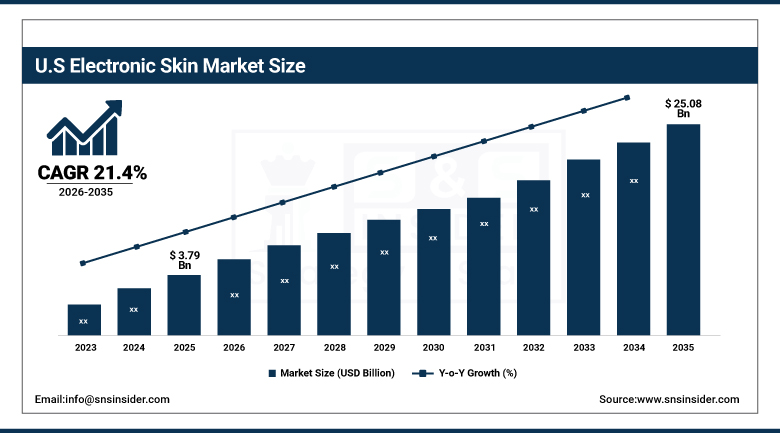

U.S. Electronic Skin Market was valued at USD 3.79 billion in 2025 and is expected to reach USD 25.08 billion by 2035, growing at a CAGR of 21.4% from 2026-2035.

The United States is the leading market for electronic skin, combining the world's most active FDA device clearance ecosystem for wearable electronics with deep NIH and DoD research funding, a sophisticated medical device manufacturing industry, and the highest concentration of healthcare AI companies integrating e-skin sensor data into clinical decision support platforms.

The U.S. Centers for Medicare & Medicaid Services reported a 45% increase in reimbursements for remote patient monitoring services using wearable devices between 2022 and 2024. The U.S. Department of Defense increased funding for electronic patch research by 40% in 2024, focusing on soldier health monitoring and performance enhancement applications.

Electronic Skin Market Segment Analysis

-

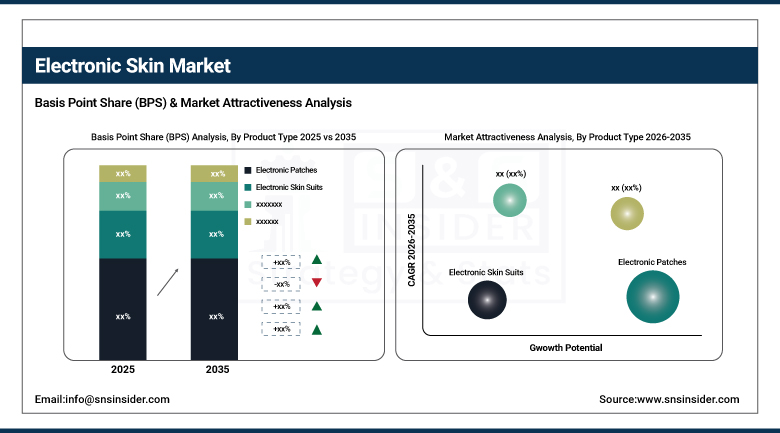

By Product Type, Electronic Patches segment dominated with ~87% share in 2025; Electronic Skin Suits segment growing in robotics and defense applications.

-

By Component, Electroactive Polymers segment dominated with ~30% share in 2025; Organic Field-Effect Transistors (OFETs) fastest growing.

-

By Sensors, Electrophysiological Sensors segment dominated with ~39% share in 2025; Pressure and Temperature Sensors growing fastest.

-

By Application, Health Monitoring segment dominated with ~39% share in 2025; Robotics & Prosthetics segment fastest growing.

By Product Type, Electronic Patches segment dominates the Electronic Skin Market, Electronic Skin Suits growing in specialized applications

The market share of electronic patches was close to 87% in the Electronic Skin Market in 2025. It is due to their versatile and non-invasive nature, which allows the application of such products in an exceptionally wide range of clinical and consumer areas. An electronic patch is an adhesive and conformable array of sensors that can be placed on the skin surface without surgical assistance, enabling users to put it on themselves and take it off independently, allowing for usage outside hospitals. The rise in the number of FDA-approved wearable devices employing electronic patches by 30% from 2021 to 2024 demonstrates the actual development of business, not just science. This is also confirmed by the fact that 75% of physicians believe electronic patch-based systems have higher levels of patient compliance.

Electronic Skin Suits represent the smaller but growing segment targeting robotics, defense, and advanced prosthetics applications where full-body or large-area coverage is required rather than the targeted spot monitoring that patches provide. Full-body e-skin suits for industrial exoskeleton operation, military performance monitoring, and humanoid robot tactile sensing are early-stage but commercially emerging applications.

By Component, Electroactive Polymers segment dominates the Electronic Skin Market, OFETs expected to grow fastest

Electroactive polymers (EAPs) held approximately 30% of component revenue in 2025. EAPs are materials that change shape or size in response to electrical stimulation a property that makes them uniquely suited for creating flexible, responsive electronic skin that can both sense inputs and generate mechanical outputs. Their ability to function across diverse sensing modalities including pressure, strain, temperature, and chemical detection makes them the most versatile single component class in e-skin device architectures. The U.S. Department of Energy reported a 35% increase in research funding for advanced polymer materials in 2024 with substantial allocation to electroactive polymers for flexible electronics, while NIST confirmed 25% improved sensitivity and responsiveness in EAP-based sensors over previous generations.

Organic Field-Effect Transistors (OFETs) are expected to grow fastest among components, driven by their central role in the nanomesh breathable e-skin architectures that are enabling the longest continuous wear durations achieved by any e-skin platform. DGIST's mesh-structured OFET-based electronic skin demonstrated prolonged use without discomfort a breakthrough for applications requiring days or weeks of continuous wear rather than the hours that earlier rigid-substrate devices sustained. As manufacturing processes for nanomesh OFETs scale from laboratory to commercial production, this component category will underpin the next generation of clinical and consumer e-skin products.

By Sensors, Electrophysiological Sensors segment dominates the Electronic Skin Market, Pressure and Temperature Sensors growing fastest

Electrophysiological sensors accounted for the largest sensor segment revenue share of 39% in 2025, reflecting the clinical primacy of electrical signal monitoring ECG, EMG, EEG, and electrodermal activity in the most commercially developed e-skin applications. Monitoring vital signs and neurological activity is where the strongest clinical evidence and FDA clearance pathway history exists, and where the commercial product landscape is most developed. The CDC documented 25% improvement in cardiovascular disorder early detection rates through wearable electrophysiological sensors from 2022 to 2024 a clinical outcome that directly drives healthcare provider adoption.

Pressure and temperature sensors are growing fastest as robotics, prosthetics, and tactile feedback applications scale beyond the research phase into commercial product development. For prosthetic limbs to feel natural to their wearers, they need to transmit pressure sensation information that allows users to modulate grip force and detect surface textures. Temperature sensing adds thermal awareness that biological hands possess but conventional prosthetic hands have historically lacked. As prosthetics manufacturers like Ottobock and Touch Bionics advance toward sensory-feedback-enabled prosthetic hands, pressure and temperature sensor arrays integrated into prosthetic covers represent a near-term commercial opportunity.

By Application, Health Monitoring segment dominates the Electronic Skin Market, Robotics & Prosthetics expected to grow fastest

Health monitoring systems accounted for the largest application share of 39% in 2025. The CDC found that 65% of adults with chronic conditions used wearable health-monitoring devices in 2024, up from 40% in 2022 growth that directly reflects e-skin device adoption expanding beyond early adopters to mainstream chronic disease management. The 45% increase in CMS reimbursements for remote patient monitoring between 2022 and 2024 provides the financial incentive that sustains adoption among healthcare providers who need payment certainty before integrating new monitoring modalities into their clinical workflows. The VA's nationwide e-skin deployment achieving 30% hospital readmission reduction demonstrates the magnitude of clinical impact that sustained systemic adoption can achieve.

Robotics & Prosthetics is growing fastest because it represents the application category where e-skin's unique mechanical conformability and multi-modal sensing capability creates functionality that no alternative technology can replicate. Industrial robots equipped with e-skin tactile sensor arrays can safely collaborate with human workers by detecting inadvertent contact and responding protectively before injury occurs. Surgical robots gain tissue texture feedback that improves surgical precision. Prosthetic limbs with e-skin overlay transmit pressure and temperature sensation to users. Each of these is a commercial application where e-skin provides unique value rather than competing with conventional sensor alternatives on a cost or performance basis.

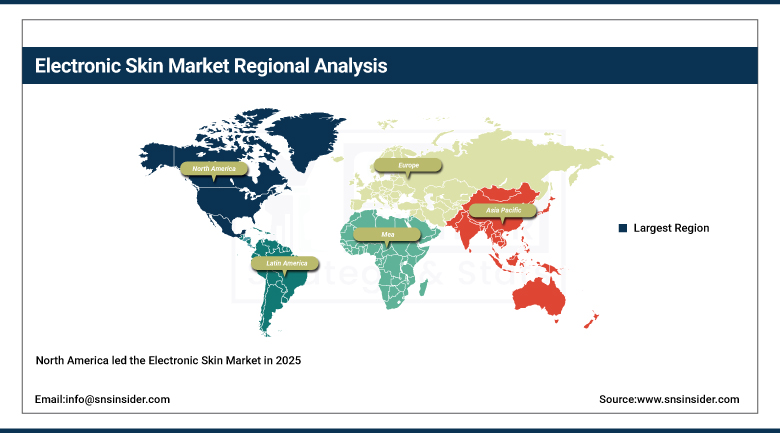

Electronic Skin Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

Israel |

35% |

|

Latin America |

Brazil |

45% |

North America Electronic Skin Market Insights

North America led the Electronic Skin Market in 2025, driven by strong FDA regulatory infrastructure for wearable medical devices, deep NIH and DoD research funding sustaining innovation, and the world's highest concentration of medical device and health technology companies actively commercializing e-skin applications. iRhythm's Zio cardiac patch generating over USD 400 million in annual revenue exemplifies the commercial scale that e-skin health monitoring products are now achieving in the U.S. market. The VA and military healthcare systems represent large institutional buyers that are actively deploying e-skin monitoring at scale and generating the clinical outcome data that drives broader healthcare system adoption. Advanced materials research at MIT, Stanford, and other leading U.S. universities continuously produces the next generation of e-skin performance improvements that commercial companies then translate to products.

The NIH National Institute of Biomedical Imaging and Bioengineering (NIBIB) has identified flexible electronics and e-skin as priority research areas with dedicated funding streams. The FDA's Digital Health Center of Excellence has created dedicated review pathways for AI-enabled wearable medical devices that accelerate e-skin product clearance timelines.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Electronic Skin Market Insights

Asia Pacific is the fastest-growing regional market for electronic skin, driven by strong academic research programs in Japan, South Korea, and China, rapidly growing aging populations creating healthcare monitoring demand, and significant government investment in advanced materials and flexible electronics manufacturing capability. Japan's aging population the oldest in the world by median age creates extraordinary structural demand for continuous health monitoring solutions. South Korean semiconductor and flexible display manufacturing expertise is being applied to e-skin substrate and circuit fabrication. DGIST and Samsung's research collaborations have produced some of the most technically advanced OFET-based e-skin architectures published in the academic literature, with several reaching early commercial development stages.

Japan's Ministry of Health, Labour and Welfare has designated wearable medical monitoring as a priority technology area under the Society 5.0 framework, with government procurement programs supporting clinical evaluation of e-skin monitoring devices at national hospital networks.

Europe Electronic Skin Market Insights

Europe holds an important position in the global Electronic Skin Market, with strength in research institutions, pharmaceutical and medical device manufacturing, and regulatory frameworks for clinical medical devices. The EU Medical Device Regulation (MDR) has raised the evidence bar for electronic skin health monitoring products entering European markets, which has lengthened time-to-market but ultimately strengthens the clinical credibility of approved products. Germany's Fraunhofer institutes, the UK's engineering research councils, and Swiss medtech manufacturing expertise collectively sustain a strong European e-skin innovation and commercialization ecosystem. European cosmetics and personal care companies exploring e-skin for advanced skin treatment applications represent a second commercial demand stream beyond clinical healthcare.

The EU Medical Device Regulation (MDR 2017/745), fully applicable since 2021, requires clinical evidence for electronic skin health monitoring devices at a level significantly exceeding previous directives. EMA's collaborative work with FDA on digital health technology through the International Medical Device Regulators Forum (IMDRF) is harmonizing e-skin device regulatory approaches globally.

Middle East & Africa and Latin America Electronic Skin Market Insights

Both regions are at early stages of electronic skin market development but show growing interest driven by healthcare infrastructure investment and specific application demand. Israel's medical technology sector one of the most active globally relative to its population size has produced several e-skin-adjacent companies addressing wound monitoring and physiological sensing for military applications. Gulf healthcare systems in the UAE and Saudi Arabia are investing in advanced wearable monitoring technologies as part of their digital health transformation programs. Brazil's medical device market and aging population create incremental healthcare monitoring demand, while the country's aerospace and defense sector generates military application interest in e-skin performance monitoring platforms.

Electronic Skin Market Growth Drivers:

-

Rising chronic disease burden and nanotechnology advances driving global adoption of electronic skin health monitoring

The clinical need that e-skin addresses is fundamental and growing. Chronic disease management diabetes, cardiovascular disease, epilepsy, cancer requires monitoring that is continuous, comfortable enough for daily wear, and capable of detecting signals that matter clinically. Conventional vital sign monitoring requires clinic visits; conventional wearables are rigid devices that patients tolerate rather than forget they are wearing. E-skin's ability to deliver clinical-grade sensor capability in a form factor that patients actually wear consistently is the primary value driver. Nanotechnology advances are continuously improving sensitivity, reducing power consumption, and extending wear duration in ways that keep opening new clinical application possibilities. The 15% rise in chronic disease prevalence documented by HHS over just four years demonstrates the scale and pace of the underlying health need that e-skin is positioned to address.

The CDC's National Center for Chronic Disease Prevention estimates that chronic diseases account for 90% of the USD 4.1 trillion in annual U.S. healthcare expenditure. Wearable medical device clinical trials registered with ClinicalTrials.gov increased by over 200% between 2019 and 2024, reflecting accelerating validation activity for continuous monitoring applications including e-skin devices.

Electronic Skin Market Restraints:

-

High fabrication costs and material complexity limiting widespread commercial scaling of electronic skin devices

The materials and manufacturing challenges of electronic skin are genuine and not trivially solved by incremental engineering effort. Graphene one of the most promising substrate materials for high-performance e-skin costs between USD 60,000 and USD 200,000 per ton, a price point that makes commercial-scale e-skin manufacturing economics very different from conventional electronics. The complex fabrication processes required to achieve the flexibility, stretchability, biocompatibility, and sensor accuracy that high-performance e-skin demands involve multiple specialized deposition and patterning steps that cannot easily be simplified into conventional semiconductor manufacturing flows. The result is that e-skin devices with best-in-class performance remain expensive, limiting their practical deployment to high-value clinical applications where device cost is justified by clinical benefit while mass-market consumer applications require cost reductions that materials science has not yet fully delivered.

Electronic Skin Market Opportunities:

-

Telemedicine expansion and continuous health monitoring demand creating transformative commercial opportunities for electronic skin

The telemedicine revolution that the pandemic normalized has created permanent structural demand for clinical-grade monitoring that works outside hospital walls. Patients with chronic conditions who previously required clinic visits for monitoring now have both the expectation and the insurance reimbursement pathway to receive that monitoring through connected wearable devices at home. E-skin's continuous monitoring capabilityproviding the kind of longitudinal physiological data that episodic clinic measurements cannot gives clinicians a richer picture of disease progression and treatment response that demonstrably improves outcomes. The commercial path from current FDA-cleared e-skin patches to the next generation of multi-parameter continuous monitoring platforms is being funded by both venture capital and large medical device company strategic investment. As manufacturing scale reduces unit costs and clinical evidence accumulates, the addressable market expands from high-value chronic disease applications toward the broader preventive health monitoring market.

Recent Developments:

-

2026: iRhythm Technologies launched the Zio AT wireless cardiac patch with expanded AI-powered arrhythmia classification covering 15 clinically significant rhythm abnormalities, receiving FDA 510(k) clearance for remote cardiac monitoring during activities of daily living including showering and exercise that previous patch generations could not sustain.

-

2025: MC10 Inc. received FDA breakthrough device designation for its BioStamp RC electronic skin patch platform for multi-parameter clinical trial monitoring, enabling simultaneous ECG, EMG, accelerometry, and temperature measurement in a single wearable device without the multiple sensors that equivalent clinical monitoring previously required.

Electronic Skin Market Key Players

Some of the Electronic Skin Market Companies

-

MC10 Inc.

-

Xenoma Inc.

-

Xsensio SA

-

Gentag Inc.

-

VivaLnk Inc.

-

Bionics Institute

-

Invacare Corporation

-

Draper Labs

-

Philips Healthcare

-

Toyobo Co., Ltd.

-

3M Company

-

Koninklijke Philips N.V.

-

Tekscan Inc.

-

T+Ink Inc.

-

Infineon Technologies AG

-

Canatu Oy

-

Eleksen Group

-

Empatica Srl

-

iRhythm Technologies, Inc.

-

Dexcom, Inc.

Electronic Skin Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.48 Billion |

| Market Size by 2035 | USD 76.0 Billion |

| CAGR | CAGR of 21.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Electronic Patches, Electronic Skin Suits) • By Component (Electroactive Polymers, Organic Field-Effect Transistors, Others) • By Sensors (Electrophysiological Sensors, Pressure Sensors, Temperature Sensors, Chemical Sensors, Others) • By Application (Health Monitoring, Robotics & Prosthetics, Wound Management, Cosmetics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | MC10 Inc., Xenoma Inc., Xsensio SA, Gentag Inc., VivaLnk Inc., Bionics Institute, Invacare Corporation, Draper Labs, Philips Healthcare, Toyobo Co., Ltd., 3M Company, Koninklijke Philips N.V., Tekscan Inc., T+Ink Inc., Infineon Technologies AG, Canatu Oy, Eleksen Group, Empatica Srl, iRhythm Technologies, Inc., and Dexcom, Inc. |

Frequently Asked Questions

Ans: North America dominated the Electronic Skin Market in 2025.

Ans: The Robotics & Prosthetics segment is expected to register the fastest CAGR through 2035.

Ans: The Electronic Patches segment dominated with approximately 87% share in 2025.

Ans: The Electronic Skin Market was valued at USD 11.48 billion in 2025.

Ans: The Electronic Skin Market is expected to grow at a CAGR of 21.4% from 2026 to 2035.

Get in Touch