Automotive Adhesives Market Report Scope & Overview:

The Automotive Adhesives Market Size was valued at USD 6.7 Billion in 2023. It is expected to grow to USD 11.3 Billion by 2032 and grow at a CAGR of 6.04% over the forecast period of 2024-2032.

The growing use of multi-material bonding in today's vehicles is indicative of the trend within the automotive sector toward stronger, lighter, and more efficient designs. In their quest for greater fuel efficiency and reduced emissions, automakers increasingly look to a combination of steel, aluminum, and composites. For instance, in the case of glass-to-metal joints, adhesives offer a flexible, durable, and reliable method for bonding these dissimilar materials with different thermal expansion behavior and mechanical properties to enable successful integration. Adhesives facilitate the bonding of multipurpose materials that help maintain structural stability in vehicles while also having potential implications for crash safety, vehicle weight reduction, and overall performance. This trend is key to satisfying changing regulations and consumer expectations for more environmentally friendly vehicles.

Automotive Adhesives Market Size and Forecast

-

Market Size in 2023: USD 6.7 Billion

-

Market Size by 2032: USD 11.3 Billion

-

CAGR: 6.04% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

Get more information on Automotive Adhesives Market - Request Sample Report

Automotive Adhesives Market Trends

-

Rising vehicle lightweighting initiatives are increasing demand for structural adhesives, with adhesive bonding helping reduce vehicle weight by up to 15%, improving fuel efficiency and EV range.

-

Rapid growth of electric vehicles (EVs) is driving adhesive consumption in battery assembly, with global EV sales rising at over 25% annually, boosting demand for thermal and structural bonding solutions.

-

Increasing adoption of advanced materials such as aluminum and composites is accelerating adhesive usage, as over 40% of new vehicle platforms incorporate lightweight materials requiring specialized bonding.

-

Stringent emission and safety regulations are encouraging OEMs to replace mechanical fasteners with high-performance adhesives, improving crash performance by 20–30% in structural applications.

-

Expansion of automated manufacturing and robotic dispensing systems is enhancing precision bonding, with more than 60% of automotive assembly lines integrating automated adhesive application technologies.

According to the U.S. Department of Energy, the use of lightweight materials such as aluminum and composites in vehicles can reduce vehicle weight by 10-50%, improving fuel efficiency by 6-8% for every 10% reduction in weight. This directly supports the shift towards multi-material bonding in the automotive industry.

The use of adhesives in the automated manufacturing process is changing how vehicles are built, especially in high-volume automotive assembly plants. Vehicle designs are becoming increasingly complex, and new technological advancements are enabling the use of more advanced materials that demand precision production. One of the key technologies in this transformation is adhesive dispensing robots and automated systems. Using exact precision these systems apply the adhesives that optimize the inter-bonding processes for each steel, aluminum, and composites. This can not only increase accuracy in material usage but can also eliminate wastage and lessen the time taken for production, allowing manufacturers to ramp up operations seamlessly.

According to the U.S. Bureau of Labor Statistics (BLS), the use of robots in manufacturing industries, including automotive, increased significantly. By 2021, nearly 30% of U.S. manufacturers used robots in their production processes, with the automotive industry leading this trend. Automation technologies, such as adhesive dispensing systems, are integral to improving precision and efficiency in vehicle production.

Automotive Adhesives Market Dynamics

Drivers

-

Increases in the demand for APAC in the Automotive Adhesive market

-

Rise in the Eco-Friendly and Lightweight Vehicles in Automotive Adhesives market.

The Automotive adhesives market is driven by the growth of eco-friendly and lightweight vehicles. Nowadays, the government has taken stringent rules regarding the environmental concern for the global footprint and provides various advantages tax benefits to the companies. So, car companies have no choice but to aim lower than ever when it comes to carbon footprints. This has caused a transition between regular heavy materials such as steel, and aluminum composites to lighter and high-strength plastic. Adhesives enable this transformation, providing the means to bond these lightweight materials that cannot be joined effectively using standard mechanical fasteners such as bolts or welds. Moreover, they also work to reduce weight by removing the requirement for heavy joining hardware. With the increasing popularity of electric vehicles (EVs), automakers are now more than ever, forced to build lighter and more energy-efficient vehicles that make the most out of EV batteries. Eco-friendly adhesives further support the industry's sustainability objectives due to their low or zero volatile organic compound (VOC) nature and the absence of harmful chemicals. This new wave of increasing demand for sustainable lightweight vehicle production is further escalating the demand for advanced automotive adhesives.

The European Union's Green Deal targets a 55% reduction in CO2 emissions from cars by 2030, compared to 2021 levels. This legislation is propelling the automotive industry toward eco-friendly and lightweight vehicles, and adhesives play a key role in ensuring these vehicles meet the required emissions targets by reducing overall vehicle weight.

Restraint

-

Challenges for manufacturers in the automotive adhesives market.

-

High-Performance Adhesives and Cost Considerations in the Adhesive Industry.

The high prices of raw materials greatly influence the cost price of automotive adhesives and have become a main challenge faced by manufacturing entities. Changes in prices of key raw materials like petrochemicals, resins, or polymers affect the production costs of adhesives. From there, manufacturers must decide if they can absorb those extra costs without squeezing their margins too tightly or hand that cost increase to carmakers. This, in turn, could raise vehicle production costs and ultimate prices to consumers. Additionally, it has proven to be a recipe for sometimes scarceness of adhesive vital parts because of the unrestrained raw material industry. These shortages can halt production schedules, slowing down the supply chain and leading to delayed deliveries of adhesives to automotive manufacturers. This presents additional complications because carmakers need to have a steady supply of adhesives to keep their production on track, which in turn impacts automotive production as a whole.

Opportunity

-

Customization Fuels the Automotive Adhesives Market.

-

Growing electric vehicle (EV) market in the adhesives industry.

-

enhanced strength and heat resistance can open doors for new applications.

As the demand for vehicles that can be modified to different needs and desires continues to rise, automotive adhesives market figures also witness significant transformations in the global automotive market. With consumers increasingly looking for customized features and designs, the automakers are opting for a multitude of materials to satisfy these demands. Traditional joining technologies such as welding have limitations due to the incompatibility of materials combined with the need for rigid joints. On the other hand, adhesives provide much more versatility to flawlessly bond a variety of modern body materials, including high-strength steel regular decay metals composites adjuncts and plastics. This flexibility enables a range of innovative, customized vehicle designs with consistent structural integrity and crash safety performance. Beyond weight reduction and fuel efficiency, they provide additional solutions for the ongoing transition to personalized lightweight vehicles. While automakers look for new vehicle customization possibilities, adhesives are also playing a larger role in achieving functional and aesthetic goals.

Automotive Adhesives Market Segmentation Overview

By Resin Type

The Polyurethane segment held the largest market share around 31% in 2023. polyurethanes are the go-to choice for structural bonding of various automotive components. From body panels and glass installation to interior assembly, PUs offers exceptional adhesive strength, flexibility to accommodate movement, and impressive resistance to both impact and temperature fluctuations. This versatility makes them a popular choice for a wide range of automotive applications. In the automotive industry, polyurethane adhesives are commonly used in structural bonding, windshield installation, and interior assembly, where strong yet flexible bonding is crucial for both safety and performance. Additionally, polyurethane adhesives contribute to vehicle weight reduction, which is a key factor in improving fuel efficiency and meeting stringent emissions regulations. As automakers continue to prioritize lightweight materials and durable bonding solutions, the demand for polyurethane adhesives remains high, solidifying their dominance in the market.

By Technology

Water-based adhesives held the largest market share around 34% in 2023. Water based adhesives are formulated using water as a solvent, therefore they have much lower volatile organic compounds (VOCs) than the solvent-based types. This fits with the trend in the sector towards sustainability and increasingly strict environmental regulations. Water-based adhesives also have great adhesion capabilities on a range of substrates including metals, plastics, and composites, which is key in modern automotive manufacturing. These components are easy to apply and clean, with a fast-drying time that supports production efficiency on an assembly line. In addition to this, the growing awareness among consumers and the increasing regulatory pressure over environmental impacts is likely to drive further demand for water-based adhesives which will continue to dominate automotive adhesives technology.

By Application

Body-in-White (BIW) segment held the largest market share in the automotive adhesives market around 40% in 2023. It is because of its importance on vehicle structure and safety. The term used in automotive nomenclature is the build stage between the frame and body shell of the vehicle, before painting and component installation; hence the acronym BIW. The adhesives used in this stage are critical for joining different substrates like high-strength steel, aluminum, and composites that are increasingly being used to increase vehicle strength and reduce weight. Adhesives are used additionally as they allow the incorporation of these materials into BIW applications which also improves overall vehicle rigidity and crash performance. Also, a rise in the interest toward lightweight planning of vehicles for gathering fuel effectiveness and discharge standards is additionally driving interest for pitches in BIW fragments.

Automotive Adhesives Market Regional Analysis

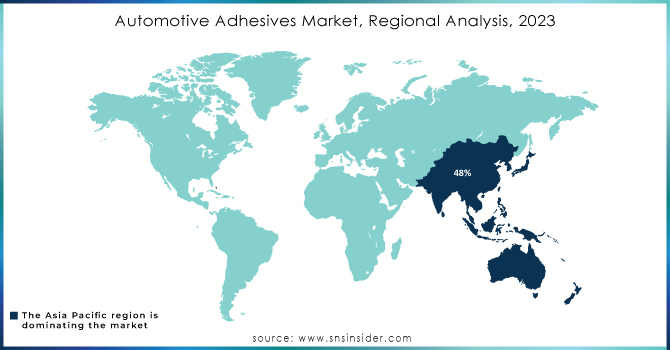

The Asia Pacific region held the largest market share around 48% in 2023. Factors such as robust growth in automotive and general industries are contributing towards the higher market share of the Asia-Pacific region in the automotive adhesives market. It includes top automotive manufacturing countries such as China, Japan, South Korea, and India which are characterized by the provisions of high automotive vehicle production. The automotive industry is one of the major consumers of adhesives, large domestic and foreign brands are continuously increasing production to meet consumer demand in China as it has already become the world's largest automotive market. Moreover, the rise in electric vehicles (EV) and weight reduction materials in this area has created a demand for advanced adhesives capable of bonding various substrates like aluminum & composites. In addition, government initiatives for environmental sustainability along with stringent emission regulations are compelling the manufacturers to utilize innovative bonding solutions which in turn propel the global industrial adhesives market growth. Asia Pacific region possesses a lot of development potential, With the increasing wealth across these countries, more and more people will have cars, thus propelling greater demand for automotive adhesives as well.

Get Customized Report as per your Business Requirement - Request For Customized Report

Key Players in Automotive Adhesives Market

-

Henkel & Co. KGaA (Loctite 498)

-

Akzo Nobel N.V. (Dinitrol)

-

BASF SE (BASF SikaBond)

-

Illinois Tool Works Inc. (ITW Plexus)

-

DowDuPont (Betamate)

-

Bostik (Bostik 646)

-

H.B. Fuller Company (Titebond III)

-

Sika AG (SikaForce)

-

PPG Industries (Pitt-Tech)

-

Solvay S.A (Avery Dennison Adhesives)

-

Jowat AG (Jowat-Toptherm 851.20)

-

3M Company (3M Scotch-Weld)

-

Momentive Performance Materials Inc. (Silicone Adhesive)

-

Lord Corporation (Lord 754)

-

MasterBond Inc. (EP21LV)

-

Permabond LLC (Permabond 105)

-

Gorilla Glue Company (Gorilla Super Glue)

-

Tremco Incorporated (Tremco TREMCO Sealants)

-

Weicon GmbH & Co. KG (Weicon Easy-Mix)

-

Soudal Group (Soudal Automotive Adhesive)

Key Users in End -Use Industry

-

Toyota Motor Corporation

-

Ford Motor Company

-

General Motors (GM)

-

Volkswagen AG

-

Honda Motor Co., Ltd.

-

Delphi Technologies

-

Valeo S.A.

-

Magna International Inc.

-

Bosch Automotive

-

Denso Corporation

Recent Development:

- In May 2023: Henkel Adhesive Technologies, a frontrunner in automotive adhesives, unveiled the Loctite TLB 9300 APSi. This innovative adhesive boasts dual functionality, offering both thermal conductivity and structural bonding, specifically designed for electric vehicle (EV) battery systems.

- In December 2022: Dow introduced the SILASTIC™ SA 994X Liquid Silicone Rubber (LSR) series, a sustainable solution for the transportation industry. This versatile rubber finds application in various automotive components, including connector seals, radiator gasket seals, and battery vent gasket seals for hybrid and electric vehicles (HEVs/EVs).

- In April 2022: 3M joined forces with Innovative Automation Inc. to deliver an automated adhesive solution for industrial manufacturers. The RoboTape System simplifies 3M tape application within assembly processes. This system aims to reduce or eliminate the need for manual labor, ultimately maximizing production efficiency.

- In February 2022: Arkema bolstered its adhesive solutions portfolio by finalizing the acquisition of Ashland's Performance Adhesives business. This acquisition grants Arkema access to a wider range of pressure-sensitive adhesives, particularly those used in protective and signage films for both buildings and automotive applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 6.7 Billion |

| Market Size by 2032 | US$ 11.3 Billion |

| CAGR | CAGR of 6.04% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Resin Type (Polyurethane, Epoxy, Acrylics, Siliconek, SMP, MMA, Others (polysulfide, rubber, polyamide, and others)) • By Application (Body in white, Paint Shop, Assembly, Power Train ) • By Vehicle Type (Passenger cars, LCVs, Trucks, Buses, Aftermarket) • By Technology (Hot melt, Solvent Based, Water based, Pressure Sensitive, Others (Reactive and Thermosetting)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Henkel & Co. KGaA, Akzo Nobel N.V., BASF SE, Illinois Tool Works Inc., DowDuPont, Bostik, H.B. Fuller Company, Sika AG, PPG Industries, Solvay S.A, Jowat AG |

| DRIVERS | • Increases in the demand of APAC in Automotive Adhesive market • Rise in the Eco-Friendly and Lightweight Vehicles in Automotive Adhesives market. |

| Restraints | • Challenges for manufacturers in the automotive adhesives market. • High-Performance Adhesives and Cost Considerations in adhesive industry |

Frequently Asked Questions

Ans. Because they are exceptionally durable even under harsh environmental conditions, allowing them to withstand challenges that other adhesives cannot.

Ans. Automotive adhesives are lighter weight than welding materials and can improve a car's body stiffness, leading to better handling.

Ans. The passage mentions manufacturers are strategically increasing production capacity to meet the rising demand for automotive adhesives. This allows them to expand their reach and become more prominent players in the region.

Ans. The projected market size for the Automotive Adhesive Market is USD 11.3 Billion by 2032.

Ans. The Compound Annual Growth rate for the Automotive Adhesive Market over the forecast period is 6.04%.

Get in Touch