Flow Cytometry Market Report Scope & Overview:

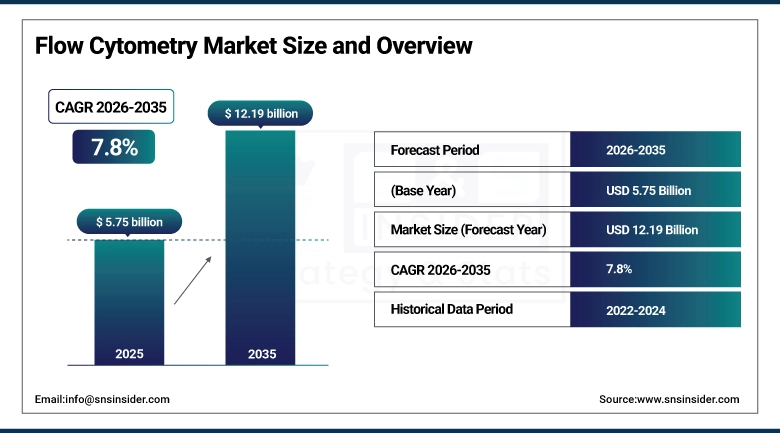

The Flow Cytometry Market was valued at USD 5.75 billion in 2025 and is expected to reach USD 12.19 billion by 2035, growing at a CAGR of 7.8% over the forecast period of 2026–2035.

The global flow cytometry market is poised to witness steady growth on account of growing utilization of flow cytometers in clinical diagnostics, drug development and biomedical research. Increasing prevalence of chronic conditions such as cancer and immunological disorders has also resulted in increased use of flow cytometers for accurately detecting, quantifying, and monitoring these diseases. The expansion of the market is further driven by continuous innovations in the area of flow cytometry that includes multi-parameter analysis, high throughput, and integration into data analysis software. The increasing research and supportive funding from the governmental as well as private sector in new genomics, proteomics, and personalized medicine is one of the underlying factors for regular demand across the market.

Flow Cytometry Market Size and Forecast:

-

Market Size in 2025: USD 5.75 billion

-

Market Size by 2035: USD 12.19 billion

-

CAGR: 7.8% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Flow Cytometry Market - Request Free Sample Report

Flow Cytometry Market Trends

-

Growth of multiparameter flow cytometry systems for more detailed characterization of cells in complex biological samples.

-

More extensive use of technical tools for example, artificial intelligence and software programs to automatically process the gathered materials.

-

Rising application of flow cytometry in immuno-oncology studies, particularly for tumor microenvironment and biomarker discovery for targeted cancer therapy.

-

Abstract Use of flow cytometry for stem cell biology has been skyrocketing over past few decades to design newer therapeutic modalities under the banner of regenerative medicine.

-

Miniature flow cytometry development aids point-of-care diagnostics to meet patient care demands across the continuum of healthcare delivery.

-

Increased focus on innovations in flow cytometry reagents and consumables, i.e. fluorescent dyes and antibodies for cell analysis

-

Increasing movement for regualted and standardized process to validate flow cytometry based test results.

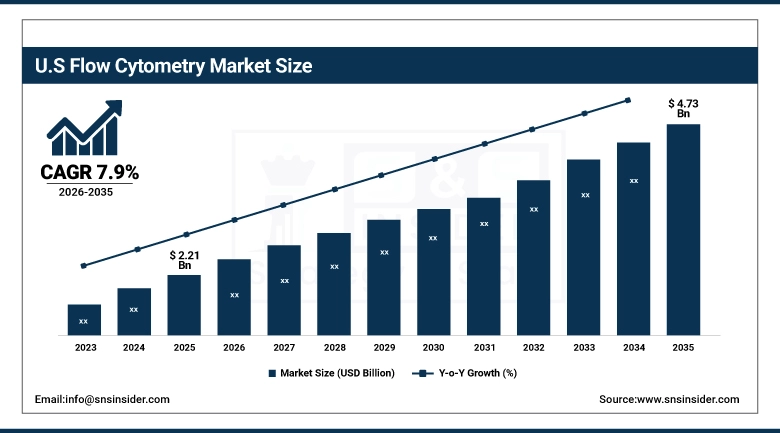

The U.S. Flow Cytometry Market was valued at USD 2.21 Billion in 2025 and is expected to reach USD 4.73 billion by 2035, with a 7.9% CAGR from 2026 to 2035. The global flow cytometry market will hold a significant share in U.S. due to the matured health system, high amount of funding by government and non-governmental organizations in research, and a developed technological approach in laboratories. Local presence of a few large biotechnology companies and major academic research centers helps expedite development and implementation of flow cytometry for basic research, clinical diagnostics, and cytotherapy applications. In addition, the growing interest in immunological studies as well as precision medicine & disease detection increases the demand for high-end cytometry instruments.

Flow Cytometry Market Growth Drivers:

-

Rising Demand for Advanced Cell Analysis and Precision Diagnostics is Driving the Flow Cytometry Market Growth

Growing use of flow cytometry technoogies for diagnostics and research in response to increased emphasis on early diagnosis of disease, immunophenotyping and precision medicine. Regulatory authorities as well as healthcare bodies are routinely promoting the use of novel diagnostic marking devices to improve the precision and efficacy of the processes related to the disease detection and monitoring. As such, flow cytometry devices will contribute to rapid analysis of cells which in turn makes them crucial for oncology, immunology, and hematology application. Growing requirement for sophisticated diagnostic instruments is boosting the demand for flow cytometry products, which is helping to provide continual growth to the global market during the forecast period.

For instance, in July 2024, the National Institutes of Health expanded funding support for advanced cellular analysis technologies, encouraging broader deployment of flow cytometry platforms in translational research and clinical diagnostics.

Flow Cytometry Market Restraints:

-

High Instrument Costs and Operational Complexity are Hampering the Flow Cytometry Market Growth

The large amounts of money involved in purchasing high-end flow cytometry equipment, besides its maintenance and calibration costs, form a considerable challenge for small-scale labs and research institutions. Instrument management, interpreting results, and employing specialists with necessary qualifications also complicate wide application. Moreover, adapting the device to current information systems, as well as other difficulties arising during installation, may also contribute to low efficiency. All these circumstances make for slow adoption, especially in poor countries or healthcare facilities and limit the market’s growth during the forecast period of 2026-2035.

Flow Cytometry Market Opportunities:

-

Integration of AI-Driven Analytics and Expanding Applications in Personalized Medicine Unlock Significant Growth Opportunities for the Flow Cytometry Market

Flow cytometry systems powered by AI and sophisticated data analytics provide only a glimpse into the future and to the potential for better data analysis and clinical decision-making in the future. Automatic gating, pattern recognition, and other features have also become smarter with the assistance of AI. Furthermore, flow cytometry is gaining importance clinically for personalized medicine applications via biomarker discovery and through the development of new targeted therapies. These developments are expected to result in enhanced demand for flow cytometry systems in pharmaceutical research and clinical trials, thereby creating new potential revenue streams.

For instance, in May 2024, Becton Dickinson announced advancements in AI-enabled flow cytometry software, demonstrating measurable improvements in data analysis speed and consistency across complex clinical datasets.

Flow Cytometry Market Segment Analysis

-

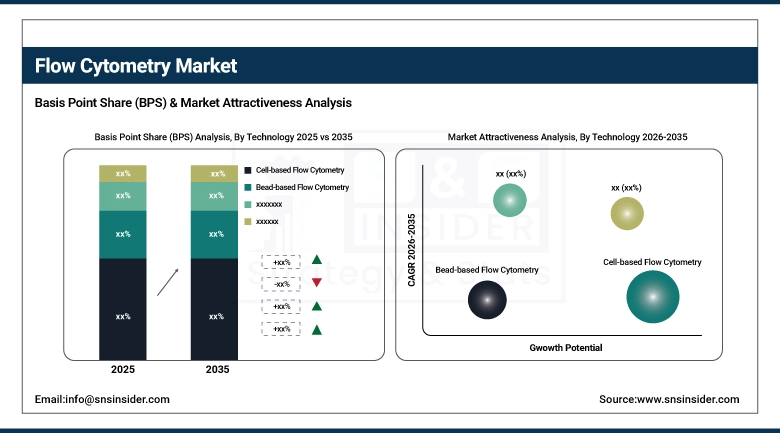

By technology, cell-based flow cytometry dominated the flow cytometry market with a share of around 61.42% in 2025, and the bead-based flow cytometry segment is expected to grow at the highest CAGR of 8.36%.

-

By product and service, reagents and consumables dominated the market in 2025, accounting for around 54.27% share, while the instruments segment is anticipated to expand at the highest CAGR of 8.11%.

-

By end user, academic and research institutes held the largest share of close to 46.83% in 2025, while pharmaceutical and biotechnology companies will register the highest growth with a CAGR of 8.54%.

By Technology, Cell-Based Flow Cytometry Leads the Market, While Bead-Based Flow Cytometry Registers Fastest Growth

In terms of revenues, the cell-based flow cytometry held the largest share of roughly 61.42% in 2025. This is due to wide-scale usage of the system in multiparametric cell analysis, immunophenotyping, and functional assays within research and clinical labs. Flow cytometers find wide application owing to its capability to provide analyses based on the physical and chemical properties of cells in real-time mode and are highly efficient in providing high-throughput data within complex biological studies. On the other hand, the bead-based flow cytometry held the second spot in 2025 in terms of share, however, this segment will record the highest CAGR of around 8.36% between 2026 and 2035. This will be fueled by an increased usage in multiplexing assays and protein quantification.

By Product and Service, Reagents and Consumables Dominate, While Instruments Segment Shows Rapid Growth

The reagents and consumables segment accounted for the maximum market share of 54.27% in 2025 due to the regular requirement for antibodies, assay kits, and other essential consumables that are needed to perform the procedure of flow cytometry. Regular consumption of the product in research applications and clinical settings, along with the need for premium quality reagents to generate accurate results, plays an important role in the dominance of the segment. The instrument segment is expected to be the fastest-growing segment with a CAGR of around 8.11% during the forecast period owing to technological innovation in cell analyzers and cell sorters.

By End-User, Academic and Research Institutes Lead, and Pharmaceutical and Biotechnology Companies Register Fastest Growth

The academic and research institutes dominated the largest market share of about 46.83% in 2025 due to favorable funding in life sciences research, increasing emphasis on immunology and cell biology research, and wide adoption of flow cytometry techniques in scientific research. Flow cytometry techniques are extensively used by these institutes for analyzing cells and discovering new knowledge. On the other hand, pharmaceutical & biotechnology organizations will hold the highest growth rate of 8.54% from 2026 to 2035 due to increasing R&D activities, increased emphasis on personalized medicine, and rising adoption of flow cytometry techniques in clinical trials and biomarker verification.

Flow Cytometry Market Regional Highlights:

North America Flow Cytometry Market Insights:

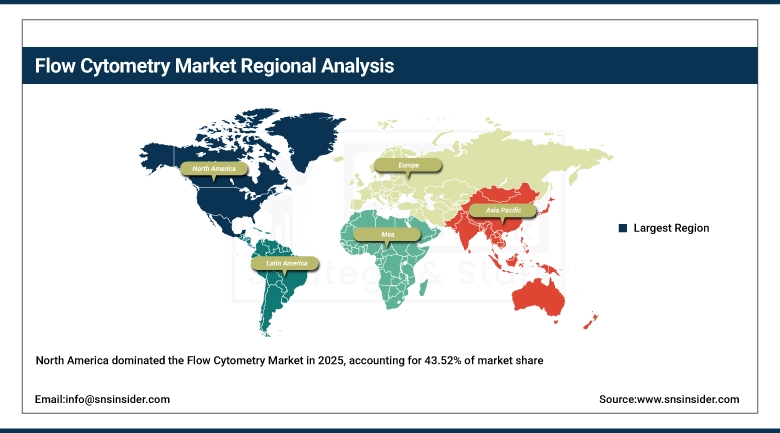

The North American region has been estimated to have the largest revenue share of more than 43.52% in 2025 of the global flow cytometry market on account of the presence of an efficient healthcare system, stringent clinical test procedures, and robust financial support for advanced diagnostic techniques. The US is considered to be the key driver of the flow cytometry market in the North American region, owing to the high adoption rate of flow cytometry instruments by research centers, clinical laboratories, and biotech organizations to improve the efficiency and accuracy of their diagnostics.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Flow Cytometry Market Insights:

Asia Pacific emerges as the most rapidly expanding geographical segment in the flow cytometry market, exhibiting a CAGR of 7.8% through continuous development of healthcare facilities, enhanced research expenditure, and government support within China, India, Japan, and South Korea. Prevalence of diseases, high awareness about early diagnosis, and increased availability of laboratory facilities are propelling the market within the region. Governmental healthcare schemes, advancements in biotech and clinical research are driving growth in adoption. Growth prospects of the region lie in its significant number of patients as well as the demand for personalized medicine therapies.

Europe Flow Cytometry Market Insights:

Europe holds the second position among all regions with respect to the flow cytometry market, driven by the presence of advanced healthcare facilities, effective regulations, and significant financial support in biomedical research in Germany, the UK, France, and the Netherlands. The increasing application of flow cytometry in the areas of diagnosis, drug discovery, and academic research is helping in sustaining market growth. Moreover, the rising importance being placed on research programs in partnership with other institutions, funding from public health agencies, and personalized treatment methods are adding impetus to the adoption of flow cytometry solutions in Europe.

Latin America (LATAM) and Middle East & Africa (MEA) Flow Cytometry Market Insights:

In LATAM and MEA, improvements in accessibility to healthcare, increased use of diagnostics, and investment in laboratories are slowly leading to the acceptance of flow cytometry systems in these countries. Brazil, Mexico, the UAE, and Saudi Arabia can be counted among the key drivers within their regional markets due to increasing research and enhanced diagnostics facilities. Availability of affordable devices, greater knowledge about diagnostics tools, and favorable healthcare policies will help increase market penetration. These will further enable steady growth for the market's revenue in the coming years till 2035.

Flow Cytometry Market Competitive Landscape:

Becton, Dickinson and Company (est. 1897) is a global leader in flow cytometry and life sciences instrumentation, offering a comprehensive portfolio of cell analyzers, sorters, reagents, and software platforms. The company leverages its BD FACSLyric and BD FACSymphony systems to deliver high-precision cell analysis across clinical diagnostics, research laboratories, and biopharmaceutical applications worldwide.

-

In February 2025, Becton, Dickinson and Company launched an advanced high-parameter flow cytometry platform with enhanced spectral analysis capabilities, enabling deeper immune profiling and improved research outcomes for academic and clinical institutions across North America and Europe.

Danaher Corporation (est. 1969) is a diversified global life sciences and diagnostics company with a dedicated flow cytometry portfolio through its Beckman Coulter Life Sciences division, providing cell analysis instruments, reagents, and data analysis software. Danaher integrates its cytometry solutions with digital workflow platforms to deliver scalable and efficient cell characterization for research and clinical laboratories globally.

-

In August 2024, Danaher Corporation introduced an upgraded CytoFLEX platform featuring improved sensitivity and automated data acquisition, strengthening its presence in academic research and clinical diagnostics markets worldwide.

Bio-Rad Laboratories (est. 1952) is a global provider of life science research and clinical diagnostics products, specializing in flow cytometry systems, reagents, and quality control solutions. The company’s ZE5 Cell Analyzer and S3e Cell Sorter serve laboratories across North America, Europe, and Asia Pacific, combining high-throughput capabilities with precise cell sorting and analysis workflows.

-

In October 2024, Bio-Rad Laboratories expanded its ZE5 Cell Analyzer adoption across emerging markets in Asia Pacific, collaborating with regional research institutes to strengthen advanced flow cytometry capabilities and laboratory efficiency.

Flow Cytometry Market Key Players:

-

Becton, Dickinson and Company (BD)

-

Danaher Corporation

-

Bio-Rad Laboratories, Inc.

-

Thermo Fisher Scientific Inc.

-

Agilent Technologies, Inc.

-

Miltenyi Biotec

-

Sony Biotechnology Inc.

-

Luminex Corporation

-

Cytek Biosciences

-

Stratedigm, Inc.

-

Apogee Flow Systems Ltd.

-

Partec GmbH (Sysmex)

-

ACEA Biosciences, Inc.

-

Union Biometrica, Inc.

-

Enzo Biochem, Inc.

-

NovoCyte (Agilent Technologies)

-

iCyt Mission Technology

-

On-Chip Biotechnologies Co., Ltd.

-

CytoBuoy BV

-

De Novo Software

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.75 Billion |

| Market Size by 2035 | USD 12.19 Billion |

| CAGR | CAGR of 7.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology [Cell-based Flow Cytometry, Bead-based Flow Cytometry] • By Product and Service [Reagents and Consumables (Antibodies, Assays & Kits, Other Reagents & Consumables), Instruments (Cell Analyzers {High-range, Mid-range, Low-range}, Cell Sorters {High-range, Mid-range, Low-range}), Services, Software, Accessories] • By Application [Research Applications (Pharmaceuticals and Biotechnology {Drug Discovery, Stem Cell Research, In Vitro Toxicity Testing}, Immunology, Cell Sorting, Apoptosis, Cell Cycle Analysis, Cell Viability, Cell Counting, Other Research Applications), Clinical Applications {Cancer Diagnostics, Hematology, Autoimmune Diseases, Organ Transplantation, Other Clinical Applications}), Industrial Applications] • By End User [Academic & Research Institutes, Hospitals & Clinical Testing Laboratories, Pharmaceutical & Biotechnology Companies] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Becton, Dickinson and Company (BD), Danaher Corporation, Bio-Rad Laboratories, Inc., Thermo Fisher Scientific Inc., Agilent Technologies, Inc., Miltenyi Biotec, Sony Biotechnology Inc., Luminex Corporation, Cytek Biosciences, Stratedigm, Inc., Apogee Flow Systems Ltd., Partec GmbH (Sysmex), ACEA Biosciences, Inc., Union Biometrica, Inc., Enzo Biochem, Inc., NovoCyte (Agilent Technologies), iCyt Mission Technology, On-Chip Biotechnologies Co., Ltd., CytoBuoy BV, De Novo Software |

Frequently Asked Questions

The Flow Cytometry Market is projected to grow from USD 5.75 billion in 2025 to USD 12.19 billion by 2035, registering a CAGR of 7.8% during the forecast period of 2026–2035, driven by increasing adoption in clinical diagnostics and biomedical research.

The Flow Cytometry Market growth is primarily driven by rising demand for advanced cell analysis, increasing prevalence of chronic diseases such as cancer, expanding applications in drug discovery, and continuous technological advancements in multi-parameter analysis systems.

Cell-based flow cytometry dominates the Flow Cytometry Market with a share of approximately 61.42% in 2025, supported by its extensive use in immunophenotyping, cell sorting, and real-time cellular analysis across research and clinical applications.

North America leads the Flow Cytometry Market with over 43.52% share in 2025, driven by strong healthcare infrastructure, high research funding, and widespread adoption of advanced diagnostic technologies.

Key trends in the Flow Cytometry Market include integration of artificial intelligence in data analysis, increasing use in immuno-oncology and personalized medicine, growing demand for portable cytometry devices, and advancements in reagents and consumables.

Get in Touch