Greases Market Report Scope & Overview:

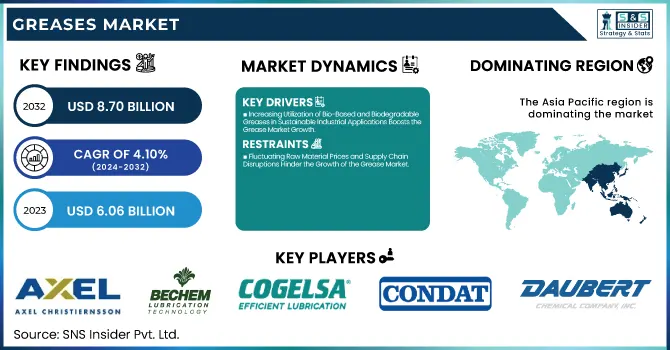

The Greases Market Size was valued at USD 6.06 Billion in 2023 and is expected to reach USD 8.70 Billion by 2032, growing at a CAGR of 4.10% over the forecast period of 2024-2032.

To Get more information on Greases Market - Request Free Sample Report

The Grease Market is undergoing a transformation fueled by evolving raw materials, regulatory shifts, and changing industry needs. Raw Material Analysis delves into the impact of base oils, thickeners, and additives on performance and costs. The balance between OEM vs. Aftermarket Demand shapes supply dynamics, while Grease Consumption per Industry highlights key sectors like automotive, construction, and metal production. Stricter REACH & EPA regulations are driving sustainable formulations, reshaping product innovation. Meanwhile, Investment Trends & Growth Hotspots uncover emerging opportunities across high-demand regions and specialized applications. Our report provides a detailed exploration of these crucial factors, offering a strategic perspective on market trends, challenges, and opportunities shaping the future of the grease industry.

Greases Market Dynamics

Drivers

-

Increasing Utilization of Bio-Based and Biodegradable Greases in Sustainable Industrial Applications Boosts the Grease Market Growth

The shift towards sustainability is significantly impacting the grease market, with increasing adoption of bio-based and biodegradable greases. Regulatory bodies such as the European Chemicals Agency (ECHA) and the United States Environmental Protection Agency (EPA) are enforcing stringent policies that encourage industries to transition away from conventional petroleum-based lubricants. Bio-based greases, derived from renewable sources like vegetable oils and synthetic esters, offer several advantages, including reduced toxicity, lower environmental impact, and enhanced biodegradability. Sectors such as marine, forestry, and food processing are increasingly incorporating these greases to comply with environmental regulations while ensuring equipment efficiency. Moreover, advancements in bio-based formulations have led to improved oxidative stability, water resistance, and temperature tolerance, making them viable alternatives to traditional lubricants. Companies investing in sustainable lubrication solutions benefit from reduced carbon footprints and enhanced compliance with international regulations. As environmental concerns continue to shape industrial practices, the market for bio-based greases is projected to expand, creating new opportunities for manufacturers developing eco-friendly lubrication solutions.

Restraints

-

Fluctuating Raw Material Prices and Supply Chain Disruptions Hinder the Growth of the Grease Market

The grease market is heavily dependent on raw materials such as base oils, thickeners, and performance additives, which are subject to price volatility due to fluctuations in crude oil costs, geopolitical instability, and supply chain disruptions. The rising cost of synthetic and bio-based base oils, along with shortages of essential additives, creates significant challenges for grease manufacturers. Additionally, supply chain inefficiencies, trade restrictions, and environmental regulations further impact production schedules, leading to increased operational costs. The dependency on specific raw material sources makes the market vulnerable to unpredictable price shifts, forcing manufacturers to either absorb costs or pass them onto consumers. This volatility can hinder market growth, particularly for small and mid-sized players who lack the financial flexibility to manage cost fluctuations effectively. Moreover, disruptions in global trade and logistics, such as those experienced during the COVID-19 pandemic, have exposed vulnerabilities in the supply chain, making long-term pricing stability a key challenge for the grease industry.

Opportunities

-

Rising Adoption of High-Performance Lubricants in Wind Energy and Renewable Power Generation Drives the Grease Market Growth

The expansion of the wind energy sector and the increasing focus on renewable power generation present lucrative opportunities for high-performance greases. Wind turbines operate under extreme conditions, including high humidity, variable temperatures, and heavy mechanical loads, requiring durable lubricants to reduce friction and minimize maintenance. Synthetic and specialty greases with superior thermal stability, anti-corrosion properties, and extended service life are gaining prominence in this sector. Additionally, with governments worldwide investing in renewable energy infrastructure and offering incentives for wind farm development, the demand for efficient lubrication solutions is expected to rise. As the renewable energy industry continues to expand, grease manufacturers have a significant opportunity to develop and market specialized lubricants tailored for sustainable energy applications.

Challenge

-

Compatibility Issues Between New Grease Formulations and Existing Machinery Pose a Significant Challenge for the Grease Market

The introduction of advanced grease formulations, including bio-based and synthetic alternatives, often leads to compatibility issues with existing machinery and lubrication systems. Many industrial equipment and automotive components are designed to function with specific lubricant compositions, and switching to new formulations can result in operational inefficiencies, increased friction, or premature wear. Industries are often hesitant to transition to newer greases due to concerns regarding equipment performance, potential breakdowns, and additional maintenance costs. Manufacturers must conduct extensive testing and provide compatibility assurances to encourage wider adoption of next-generation greases. Addressing these compatibility concerns through standardized testing procedures and detailed product specifications is critical for overcoming this challenge.

Greases Market Segmental Analysis

By Thickener Type

Metallic Soap Thickener dominated the greases market in 2023 with a market share of 68.5%, with Lithium-based greases leading within this category, holding an estimated 60% share among metallic soap thickeners. Lithium-based greases are widely preferred due to their excellent water resistance, thermal stability, and compatibility with various industrial and automotive applications. According to the National Lubricating Grease Institute (NLGI), lithium-based greases are the most commonly used worldwide due to their superior performance in high-load and high-temperature conditions. The growing demand for lithium complex greases in electric vehicles, aerospace, and heavy-duty industrial machinery has further solidified their dominance. Additionally, industry reports indicate that lithium-based greases are favored by automotive manufacturers such as Ford and General Motors for use in wheel bearings, chassis components, and engine applications. However, concerns about lithium supply constraints and price volatility have led to research on alternative thickeners, but lithium-based metallic soap greases continue to dominate due to their established market presence and widespread industry preference.

By Base Oil

Mineral Oil-based greases dominated the greases market in 2023, accounting for 65% of the total market share. Despite the growing shift toward synthetic and bio-based greases, mineral oil remains the most widely used base oil due to its cost-effectiveness, easy availability, and satisfactory performance across diverse industrial applications. Organizations such as the Society of Tribologists and Lubrication Engineers (STLE) recognize mineral oil-based greases as the preferred choice for general-purpose lubrication in sectors like automotive, construction, and manufacturing. Major automotive brands, including Toyota and Volkswagen, continue to use mineral oil-based greases for chassis and bearing lubrication due to their proven performance and affordability. Additionally, many industrial applications, such as conveyor belt systems and mechanical bearings, rely on mineral-based greases because of their ability to provide effective lubrication under moderate operating conditions. While synthetic greases offer enhanced longevity and stability, their higher costs and specific application requirements have kept mineral oil-based greases as the dominant choice in the market.

By Application

The automotive industry dominated the greases market in 2023, holding a dominant 42.1% market share. The extensive use of greases in vehicle components, such as wheel bearings, chassis, gears, and electric motor systems, has contributed to this dominance. The International Energy Agency (IEA) has reported a significant increase in vehicle production, particularly in emerging economies, fueling the demand for automotive lubricants, including greases. Additionally, with the rapid expansion of the electric vehicle (EV) sector, major automakers like Tesla, BMW, and Mercedes-Benz are investing in advanced greases with enhanced thermal and electrical insulation properties to improve vehicle performance and longevity. The European Automobile Manufacturers’ Association (ACEA) has also emphasized the importance of high-quality greases in reducing friction and improving fuel efficiency in internal combustion engine (ICE) vehicles. Moreover, the shift toward electric mobility is further driving the adoption of specialized greases for battery components, drivetrains, and high-performance braking systems, reinforcing the automotive sector's leading position in the greases market.

Greases Market Regional Outlook

Asia Pacific dominated the greases market in 2023, accounting for 45.3% of the total market share. The region’s leadership is driven by rapid industrialization, expanding automotive production, and robust manufacturing activities across China, India, and Japan. China, as the world's largest automotive producer, significantly influences the demand for greases, with over 27 million vehicle units manufactured in 2023, according to the China Association of Automobile Manufacturers (CAAM). The country’s extensive construction, mining, and heavy machinery sectors further contribute to the high grease consumption. India, with its fast-growing industrial base, witnessed a 9.5% growth in the manufacturing sector, as per the Ministry of Commerce and Industry, fueling demand for high-performance lubricants. Additionally, Japan, home to automotive giants such as Toyota, Honda, and Nissan, heavily relies on specialized greases for precision engineering and electric vehicle advancements. The rising demand for bio-based and synthetic greases, backed by environmental regulations from agencies like China’s Ministry of Ecology and Environment, further solidifies Asia Pacific's dominance in the global greases market.

On the other hand, North America emerged to be the fastest-growing region in the greases market, projected to expand at a significant CAGR during the forecast period. The growth is primarily driven by the increasing demand for high-performance synthetic greases in the automotive, aerospace, and industrial sectors. The United States, as the largest contributor in the region, has seen a surge in the adoption of premium greases in electric vehicles, with over 1.4 million EVs sold in 2023, as per the U.S. Department of Energy. The Biden administration’s push for sustainable lubricants, along with EPA regulations on environmental safety, is also accelerating the shift toward bio-based greases. Canada, with its expanding oil and gas industry, has a rising demand for specialized greases for drilling equipment and pipelines. Additionally, Mexico, as a leading automotive manufacturing hub, is experiencing increased usage of industrial greases, driven by the presence of global automakers like Ford, Volkswagen, and GM, further fueling the region’s growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Axel Christiernsson (Axel Longlife Grease, Axel Biodegradable Grease, Axel Calcium Sulfonate Grease)

-

BECHEM Lubrication Technology LLC (Berulub FR 43, Berutox VPT 64-2, Berulit GA 250)

-

Battenfeld-Grease & Oil Corporation of New York (Lithoplex MP2, Litholine HD2, Battenplex EP2)

-

Carl Bechem GmbH (Berulub KR EP 2, Beruto njx FH 28 EPK, Berulub FK 164-2)

-

Chemtool Incorporated (Paragon 3000, Omniguard 220, Lubricast 90)

-

COGELSA Efficient Lubrication (Lubgel Complex EP 2, Lubgel LT 1, Lubgel Bioceramic 2)

-

CONDAT Group (Condat Biogrease EP2, Condat Grease TP, Condat Extreme Pressure Grease)

-

Daubert Chemical Company (Tectyl 891D, Tectyl 846, Nox-Rust 5400)

-

D-A Lubricant Company (D-A Reliant, D-A Syn-Xtreme HD2, D-A Lubricast 50)

-

Eastern Oil Company (EOC Moly Grease, EOC Lithium Complex Grease, EOC Synthetic Grease)

-

FUCHS Petrolub SE (Renolit CX-EP 2, Renolit Duraplex EP, Renolit Extreme)

-

Interflon (Interflon Grease MP2, Interflon Grease OG, Interflon Grease LS2)

-

JAX Incorporated (JAX Poly-Guard FG2, JAX Magna-Plate 8, JAX Halo-Guard FG2)

-

Klüber Lubrication (Klüberplex BEM 41-141, Klüberlub BE 41-1501, Klübersynth BHP 72-102)

-

Lubriplate Lubricants Company (Lubriplate 630-2, Lubriplate SFL-1, Lubriplate Low Temp Grease)

-

NYCO (Nyco Grease GN 148, Nyco Grease GN 3058, Nyco Grease GN 25013)

-

Orlen Oil Ltd (Orlen Greasen Complex EP, Orlen Litol 24, Orlen Graphite Grease)

-

Primrose Oil Company, Inc. (Primrose 357 Moly EP, Primrose 405 Amber, Primrose Syn-O-Gel 680)

-

RichardsApex, Inc. (RichardsApex Draw Grease 705, RichardsApex Copper Grease 90, RichardsApex Forge Grease)

-

Royal High-Performance Oil & Greases (Royal Ultra 865 EP, Royal Ultra 8800, Royal Purple Ultra-Performance)

Recent Developments

-

September 2024: Maxol Lubricants launched the Maxol Agri-Max Plus Grease range for agriculture, marine, and forestry applications. The company also introduced sustainable packaging. Key products include Maxol Agri-Max-Plus Calcium Grease and Agri-Max-Plus EFS Grease, catering to the agricultural and food processing sectors. (mobilityplaza.org)

-

March 2024: Shell Indonesia announced its first grease manufacturing plant in Bekasi, integrated with its Marunda Lubricants Oil Blending Plant. The facility will produce 12 kilotonnes of grease annually using advanced technology to meet Indonesia’s growing demand.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 6.06 Billion |

| Market Size by 2032 | USD 8.70 Billion |

| CAGR | CAGR of 4.10% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Thickener Type (Metallic Soap Thickener, Non-soap Thickener [Inorganic, Polyurea, Clay-based]) •By Base Oil (Mineral Oil, Synthetic Oil, Bio-based Oil) •By End-use Industry (Automotive, Construction, Mining, General Manufacturing, Metal Production, Power Generation, Agriculture, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | FUCHS Petrolub SE, Klüber Lubrication, Axel Christiernsson, Carl Bechem GmbH, Chemtool Incorporated, CONDAT Group, NYCO, BECHEM Lubrication Technology LLC, Lubriplate Lubricants Company, COGELSA Efficient Lubrication and other key players |

Frequently Asked Questions

Ans: North America is the fastest-growing region in the Greases Market due to rising demand for eco-friendly products.

Ans: The rising demand for Greases in sustainable nanotechnology applications is expanding the Greases Market.

Ans: The increasing use of Greases in oil spill remediation is boosting the Greases Market.

Ans: The Greases Market is projected to reach USD 8.70 Billion by 2032, growing at a CAGR of 4.10%.

Ans: The Greases Market was valued at USD 6.06 Billion in 2023.

Get in Touch