1,3 Propanediol Market Report Scope & Overview:

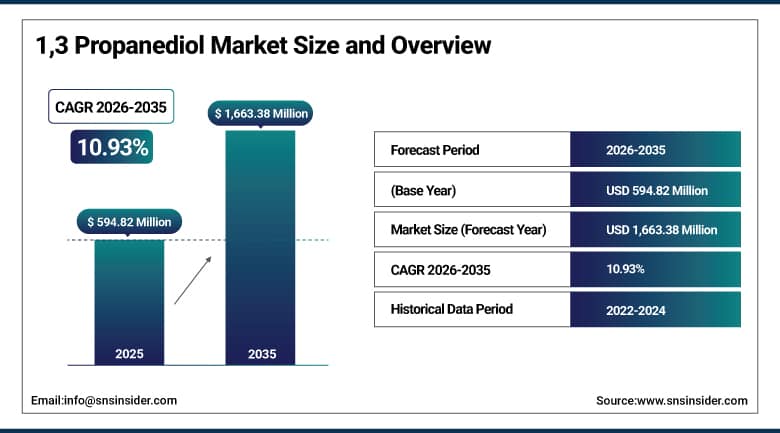

The 1,3 Propanediol Market was valued at USD 594.82 Million in 2025 and is expected to reach USD 1,663.38 Million by 2035, growing at a CAGR of 10.93% from 2026–2035.

The global 1,3 propanediol market is growing at a sustained and commercially significant pace. 1,3 Propanediol (1,3-PDO) is a colorless, viscous organic diol characterized by two hydroxyl groups on a three-carbon backbone, fully miscible with water and versatile across industrial applications. Primarily employed as a monomer in polytrimethylene terephthalate (PTT) production for high-performance textile fibers and carpets, it also functions as a solvent, humectant, antifreeze component, and personal care ingredient. The market is driven by growing demand for bio-based chemicals which drives market growth as the primary catalyst, increasing sustainability requirements across consumer and industrial procurement, and the progressive expansion of PTT applications in textiles, carpets, and technical fibers whose performance advantages create specification preference over conventional polyester alternatives.

In 2023, DuPont Tate & Lyle Bio Products launched Purabloc 2000, a high-purity, renewable bio-PDO grade specifically tailored for stringent cosmetic and personal care specifications, signaling heightened focus on specialty segments that command premium margins. The product’s 99%+ purity from corn-based fermentation, combined with its 100% bio-based credential, creates premium procurement motivation in personal care formulations whose sustainability and safety specifications create above-commodity pricing that sustains DuPont Tate & Lyle’s market leadership in high-value bio-PDO applications.

Market Size and Forecast:

-

Market Size in 2026E: USD 660.08 Million

-

Market Size by 2035: USD 1,663.38 Million

-

CAGR: 10.93% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On 1,3 Propanediol Market - Request Free Sample Report

1,3 Propanediol Market Trends:

-

Growing production of bio-based 1,3-PDO from renewable feedstocks is supporting sustainable manufacturing initiatives and increasing demand for environmentally friendly chemical ingredients

-

Rising adoption of PTT fibers is driving 1,3-PDO consumption due to their superior elasticity, stain resistance, durability, and comfort in textile and carpet applications

-

Increasing use of bio-based 1,3-PDO in personal care products is supporting demand as manufacturers seek natural-origin humectants and sustainable formulation ingredients

-

Expanding adoption of 1,3-PDO in antifreeze and deicing applications is creating opportunities as industries seek safer and more biodegradable alternatives to conventional glycols

-

Strengthening partnerships across agricultural and bio-based supply chains are enhancing the sustainability profile of 1,3-PDO production and supporting circular economy initiatives

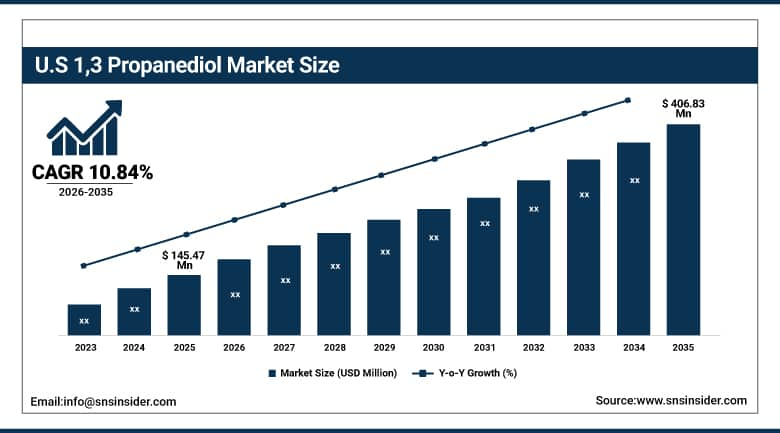

U.S. 1,3 Propanediol Market Outlook:

The U.S. 1,3 Propanediol Market was valued at approximately USD 145.47 Million in 2025 and is expected to reach approximately USD 406.83 Million by 2035, growing at a CAGR of approximately 10.84%.

The U.S. is the most commercially significant 1,3-PDO market within the fastest-growing North American region. DuPont Tate & Lyle Bio Products’ Loudon, Tennessee facility is the world’s largest bio-based 1,3-PDO production site whose corn fermentation creates cost-competitive supply for domestic textile, personal care, and industrial markets. The U.S.’s domestic PTT fiber production, the personal care industry’s bio-based ingredient adoption, and the industrial solvent market’s green chemistry transition create diverse application channels that sustain domestic 1,3-PDO demand growth.

DuPont unveiled plans to increase its bio-PDO production capacity by 50% at its Loudon, Tennessee facility, targeting growing North American demand in PTT textile, personal care, and industrial applications. The expansion confirms DuPont Tate & Lyle Bio Products’ commercial conviction in bio-based 1,3-PDO’s long-term demand growth whose sustainability differentiation creates specification preference that conventional petro-chemical alternatives cannot match in procurement contexts where bio-based credentials create regulatory or consumer-facing value.

1,3 Propanediol Market Segment Analysis:

-

By Type, the Bio-Based 1,3-PDO segment dominated the 1,3 Propanediol Market with approximately 56% share in 2025, while the Conventional/Petrochemical segment is the fastest growing.

-

By Application, the Polytrimethylene Terephthalate (PTT) segment dominated the 1,3 Propanediol Market with approximately 55% share in 2025, while the Cosmetics & Personal Care segment is the fastest growing.

-

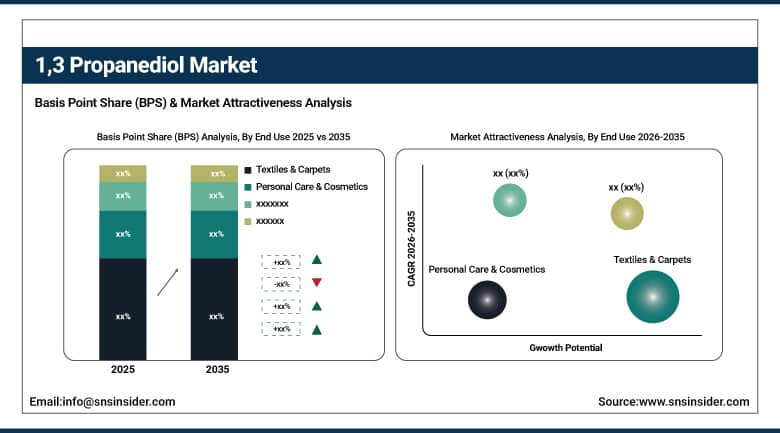

By End Use, the Textiles & Carpets segment dominated the 1,3 Propanediol Market with approximately 48% share in 2025, while the Personal Care & Cosmetics segment is the fastest growing.

By End Use, textiles dominate, personal care grows fastest

Textiles and carpets retained the dominant end-use position with approximately 48% of the 1,3 propanediol market in 2025. The PTT fiber’s progressive adoption across carpet, BCF staple fiber, and technical textile applications creates commercial scale whose aggregate across the global textile sector’s production creates consistent demand. The carpet industry’s specification of PTT for its superior stain resistance relative to nylon creates institutional procurement whose commercial scale sustains textiles’ dominant end-use position. Each new PTT carpet specification sustains 1,3-PDO procurement whose per-ton consumption reflects the carpet’s PTT content.

Personal care and cosmetics are the fastest-growing end use because the extraordinary commercial momentum of the natural and sustainable beauty market is creating above-average specification migration toward bio-based ingredients whose consumer communication value creates premium product positioning. Each personal care formulation that adopts Zemea bio-PDO as its sustainable humectant creates procurement whose per-unit commercial value compound with the premium beauty market’s growth.

By Type, bio-based dominates, conventional grows fastest by volume

Bio-based 1,3-PDO retained the dominant type position with approximately 56% of the 1,3 propanediol market in 2025. Bio-based’s commercial primacy reflects DuPont Tate & Lyle Bio Products’ market leadership whose corn-fermentation process creates a bio-based supply chain whose commercial scale and cost efficiency sustain market dominance. The Susterra and Zemea branded bio-PDO products’ 100% renewable carbon certification creates commercial differentiation whose sustainability credential sustains specification preference in textile, personal care, and industrial markets where bio-based procurement creates regulatory compliance, consumer communication, or corporate sustainability programme value. Each personal care brand that specifies bio-based 1,3-PDO for its humectant creates commercial relationships whose premium pricing sustains DuPont Tate & Lyle’s above-commodity margin.

Conventional petrochemical 1,3-PDO is the fastest growing by volume because cost-sensitive industrial applications including antifreeze, industrial solvent, and coating applications create price-driven procurement whose competitive economics favor conventional synthesis routes at commodity applications where bio-based certification creates no incremental commercial value. Each industrial application whose procurement decision is cost-driven creates conventional 1,3-PDO demand whose volume compounds with industrial market growth in Asia Pacific where petrochemical production economics create cost-competitive conventional supply.

By Application, PTT dominates and grows rapidly

Polytrimethylene terephthalate (PTT) retained the dominant application position with approximately 55% of the 1,3 propanediol market in 2025. PTT’s commercial primacy reflects its role as the primary large-volume 1,3-PDO consuming application whose polymer chain’s unique crystal structure creates textile performance properties that PET and nylon alternatives cannot match equivalently. PTT fiber’s inherent stretch recovery without mechanical treatment, its soil release stain resistance, and its comfortable soft hand feels collectively create specification advantages in carpet, activewear, and workwear whose growing adoption creates above-average 1,3-PDO demand growth. As SNS Insider confirms, PTT will grow rapidly in the 1,3-PDO market from 2024-2032, reflecting the progressive textile sector’s adoption of PTT’s performance benefits.

Personal care and cosmetics are growing rapidly alongside PTT because bio-based 1,3-PDO’s designation as a 100% bio-derived ingredient whose COSMOS and ECOCERT certification creates premium formulation value in natural and organic beauty products whose market growth creates structured above-average demand. Each premium skincare brand that specifies bio-PDO as its humectant and skin-feel modifier creates procurement relationships whose per-kg commercial value substantially exceeds commodity industrial applications.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

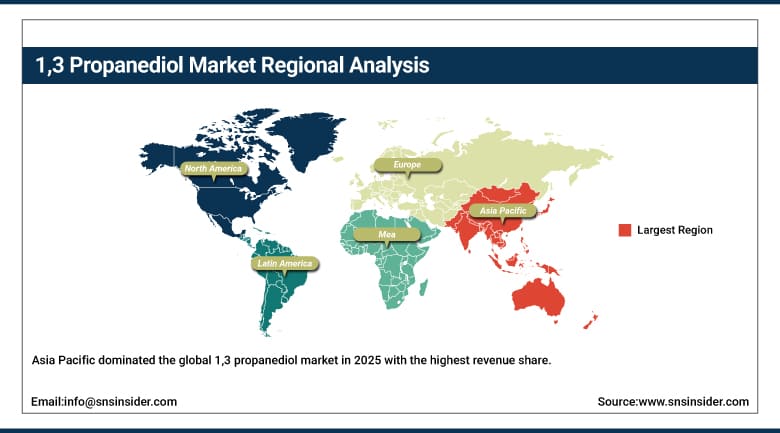

Asia Pacific 1,3 Propanediol Market Insights

Asia Pacific dominated the global 1,3 propanediol market in 2025 with the highest revenue share. China accounts for approximately 54.6% of Asia Pacific revenues through its extraordinary textile manufacturing scale, the domestic chemical industry’s conventional 1,3-PDO production capacity, and the growing personal care sector’s ingredient procurement. The region’s commercial leadership reflects the concentration of PTT fiber and carpet production in Asia Pacific’s textile manufacturing complex.

South Korea’s and Japan’s advanced textile and personal care sectors create significant secondary markets whose premium specification creates above-average per-ton 1,3-PDO commercial value.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America 1,3 Propanediol Market Insights

North America is the fastest-growing regional 1,3 propanediol market, driven by DuPont Tate & Lyle Bio Products’ capacity expansion, the personal care industry’s bio-based ingredient adoption, and growing PTT fiber specification in the carpet and activewear markets. The United States accounts for approximately 87.4% of North American revenues through the Loudon, Tennessee bio-PDO production facility’s domestic supply and the premium personal care market’s bio-based ingredient specification.

Canada contributes approximately 12.6% of North American revenues through its textile and personal care industries’ 1,3-PDO procurement and the industrial solvent market’s green chemistry adoption.

Europe 1,3 Propanediol Market Insights

Europe is a technically sophisticated 1,3-PDO market where REACH regulation, the European Green Deal’s bio-based chemical preference, and the personal care industry’s natural ingredient specification create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced chemical industry, the textile sector’s PTT adoption, and the personal care market’s premium bio-based ingredient procurement.

France, the United Kingdom, and Italy are significant secondary markets where the cosmetics industry’s bio-based ingredient adoption, the carpet sector’s PTT specification, and the pharmaceutical industry’s pharmaceutical-grade excipient procurement create consistent demand.

MEA & Latin America 1,3 Propanediol Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its petrochemical industry’s chemical manufacturing and the growing personal care market’s ingredient procurement. Brazil leads Latin American revenues at approximately 44.2% through its textile industry’s fiber procurement, the personal care market’s bio-based ingredient adoption, and the agricultural sector’s bio-based chemical production infrastructure.

Market Dynamics:

Growth Drivers: Growing demand for bio-based chemicals and PTT textile performance driving sustainable polymer adoption

Growing demand for bio-based chemicals is SNS Insider’s confirmed primary growth driver for the 1,3-PDO market. The progressive globalization of corporate sustainability commitments creates structured procurement migration from petrochemical to bio-based chemical alternatives whose renewable carbon footprint creates regulatory compliance, ESG reporting, and consumer communication value. Each brand that commits to bio-based ingredient sourcing creates 1,3-PDO demand whose commercial scale compounds with sustainability commitment adoption across consumer goods categories.

PTT’s performance advantages in carpet and textile applications create intrinsic adoption motivation beyond sustainability positioning. The carpet industry’s specification shift from nylon to PTT for superior stain resistance, the activewear market’s PTT adoption for stretch recovery without mechanical treatment, and the workwear sector’s PTT specification for durability collectively create structured demand growth that compounds with each new PTT performance validation.

Restraints: Bio-PDO production cost premium and limited feedstock diversification

Bio-based 1,3-PDO’s production cost premium over petrochemical conventional alternatives creates adoption barriers in cost-sensitive industrial applications where sustainability certification creates no incremental commercial value. Each cost-sensitive application whose procurement decision is purely economic creates conventional 1,3-PDO preference that moderates bio-based market penetration below the addressable sustainability-committed market.

DuPont Tate & Lyle Bio Products’ corn-glucose fermentation feedstock concentration in the U.S. Corn Belt creates geographic supply chain concentration risk whose commodity corn price volatility creates bio-PDO production cost uncertainty that moderates pricing predictability for long-term supply agreements.

Opportunities: Pharmaceutical-grade bio-PDO and bio-based PTT circular economy positioning

Pharmaceutical-grade 1,3-PDO as an excipient solvent, humectant, and API carrier creates a premium application whose regulatory quality requirements and supply security motivation sustain above-commodity pricing and long-term commercial relationships. Each new drug formulation that specifies 1,3-PDO creates procurement whose pharmaceutical-grade specification creates commercial differentiation from industrial-grade alternatives.

PTT’s recyclability advantage over nylon carpet, combined with the textile circular economy’s growing regulatory mandate, creates sustainable textile positioning whose end-of-life recyclability creates commercial differentiation that sustains PTT specification in sustainability-committed procurement programmes.

Recent Developments:

-

2023: DuPont Tate & Lyle Bio Products launched Purabloc 2000 high-purity renewable bio-PDO in 2023, specifically tailored for stringent cosmetic and personal care specifications, enabling premium personal care formulations with 100% bio-based humectant and solvent functionality.

-

2022: DuPont unveiled plans to increase its bio-PDO production capacity by 50% at its Loudon, Tennessee facility, targeting growing North American demand in PTT textile, personal care, and industrial applications to sustain its global market leadership position.

-

2022: Covation Biomaterials partnered with Primient in September 2022 for sustainable agriculture programme integration, enabling corn farmers in the American Midwest to implement regenerative farming practices for the bio-PDO corn-glucose feedstock supply chain.

1,3 Propanediol Market Key Players:

-

DuPont Tate & Lyle Bio Products (Susterra/Zemea)

-

Metabolic Explorer S.A. (METabolic EXplorer)

-

Shell Chemicals LP

-

Haier Group Corporation

-

PTT Global Chemical Public Company

-

Degussa AG (Evonik Industries)

-

Archer Daniels Midland Company

-

Cargill Incorporated

-

BASF SE

-

Dow Inc.

-

Primient (formerly Tate & Lyle Americas)

-

Covation Biomaterials LLC

-

Genomatica Inc.

-

LCY Chemical Corp.

-

Qingyun Weiye Chemical

-

Zhangjiagang Glory Chemical Industry

-

Glory BioChem

-

Shandong Shida Shenghua

-

Hunan Rivers Bioengineering Co., Ltd.

-

Zhangjiagang Dawei Fine Chemical

1,3 Propanediol Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 594.82 Million |

| Market Size by 2035 | USD 1,663.38 Million |

| CAGR | CAGR of 10.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Bio-Based 1,3-PDO, Conventional/Petrochemical 1,3-PDO) • by Application (Polytrimethylene Terephthalate/PTT, Solvents, Cosmetics & Personal Care, Adhesives & Coatings, Antifreeze & Deicing, Pharmaceutical Excipients, Others) • by End Use (Textiles & Carpets, Personal Care & Cosmetics, Paints & Coatings, Adhesives, Pharmaceutical & Healthcare, Food & Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | DuPont Tate & Lyle Bio Products, Metabolic Explorer S.A., Shell Chemicals LP, Haier Group Corporation, PTT Global Chemical Public Company, Degussa AG, Archer Daniels Midland Company, Cargill Incorporated, BASF SE, Dow Inc., Primient, Covation Biomaterials LLC, Genomatica Inc., LCY Chemical Corp., Qingyun Weiye Chemical, Zhangjiagang Glory Chemical Industry, Glory BioChem, Shandong Shida Shenghua, Hunan Rivers Bioengineering Co., Ltd., Zhangjiagang Dawei Fine Chemical |

Frequently Asked Questions

The 1,3 Propanediol Market is expected to grow at a CAGR of 10.93% from 2026 to 2035.

The 1,3 Propanediol Market was valued at USD 594.82 Million in 2025.

Growing demand for bio-based chemicals which drives market growth as the primary catalyst, and PTT’s superior performance properties in textile, carpet, and activewear creating structured specification adoption that compounds with the sustainable polymer market’s extraordinary growth momentum.

Polytrimethylene Terephthalate (PTT) will grow rapidly in the 1,3 Propanediol Market from 2024-2032 as confirmed by SNS Insider, reflecting PTT fiber’s progressive adoption across textiles, carpets, and technical applications.

Asia Pacific dominated the 1,3 Propanediol Market in 2025 with the highest revenue share, while North America is the fastest-growing region.

Get in Touch