Herbicide Safeners Market Report Scope & Overview:

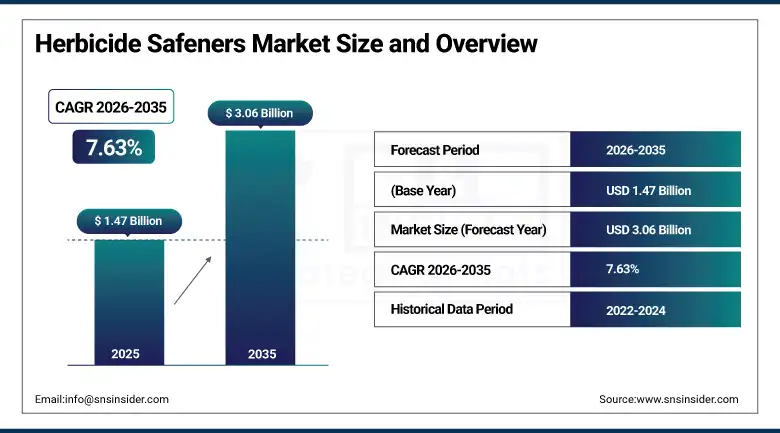

The Herbicide Safeners Market was valued at USD 1.47 Billion in 2025 and is expected to reach USD 3.06 Billion by 2035, growing at a CAGR of 7.63% from 2026–2035.

Herbicide safeners are specialty agrochemical compounds applied to seeds or in herbicide formulations to enhance the tolerance of crop plants to herbicide treatments without reducing weed control efficacy, enabling farmers to apply broad-spectrum and highly effective herbicides at commercially optimal rates without incurring the phytotoxicity damage to crop plants that unsafened application would cause. The commercial imperative for herbicide safeners rests on the fundamental agronomic tension between herbicide efficacy and crop safety. Where the most potent and cost-effective weed control chemistries in cereal, corn, and sorghum production systems create metabolic stress responses in crop plants at commercially justified application rates that safener co-formulation or seed treatment prevents by selectively accelerating the crop plant's herbicide detoxification enzymatic activity while leaving weed control unaffected.

In May 2023, Syngenta and FMC Corporation entered a collaborative agreement to expand their herbicide safener research programmes, focusing on developing novel safener compounds for next-generation herbicide formulations targeting grass weed resistance management in corn and sorghum production systems. The collaboration reflected both companies' recognition that the growing prevalence of herbicide-resistant weed populations is creating commercial urgency for new herbicide-safener combinations, whose performance against resistant weed biotypes requires novel active ingredient chemistry whose crop safety can only be achieved through purpose-designed safener co-formulation rather than broad-spectrum safener application.

Market Size and Forecast

-

Market Size in 2026E: USD 1.58 Billion

-

Market Size by 2035: USD 3.06 Billion

-

CAGR: 7.63% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Herbicide Safeners Market - Request Free Sample Report

Herbicide Safeners Market Trends

-

Advanced safener molecules are gaining adoption due to improved crop tolerance and compatibility with modern herbicide chemistries.

-

Seed treatment-based safener formulations are growing in popularity by providing targeted and consistent crop protection during early growth stages.

-

Integration of herbicide safeners with herbicide-resistant crop technologies is enhancing weed management effectiveness and crop safety.

-

Precision agriculture technologies are enabling optimized safener application based on field-specific crop and soil conditions.

-

Expanding regulatory approvals and increasing adoption of modern weed management practices in Asia Pacific are supporting market growth.

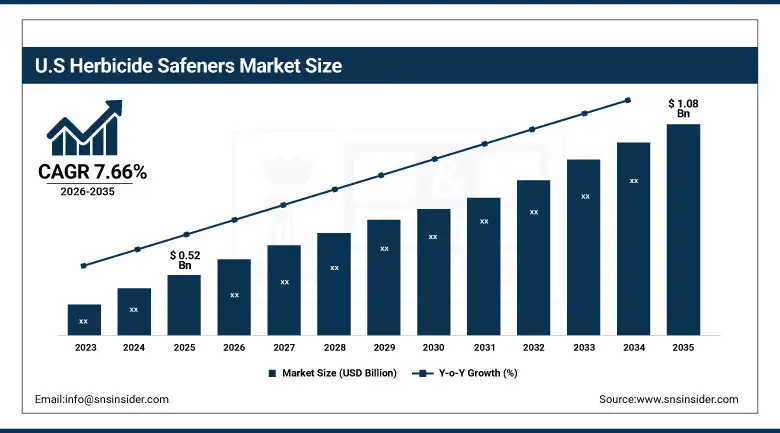

The U.S. Herbicide Safeners Market Outlook

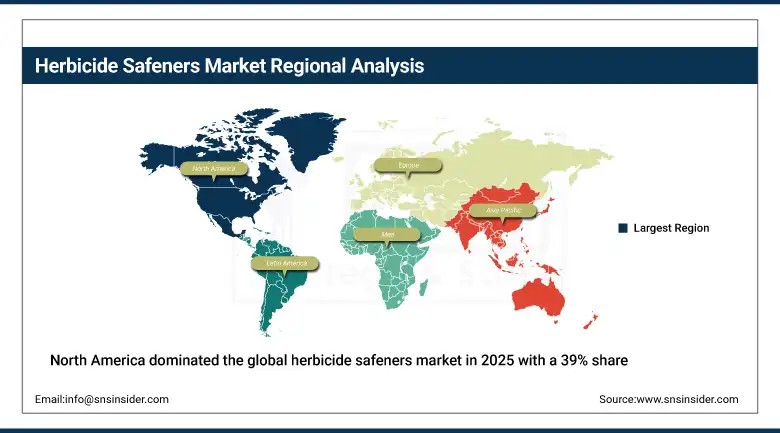

The U.S. Herbicide Safeners Market was valued at approximately USD 0.52 Billion in 2025 and is expected to reach approximately USD 1.08 Billion by 2035, growing at a CAGR of approximately 7.66%. North America led the herbicide safeners market with a share of 39% in 2025, owing to the large-scale adoption of advanced agricultural practices, high herbicide usage, and growing demand for high-yield crops.

The United States herbicide safeners market is anchored by the large-scale commercial corn and sorghum production systems in the Corn Belt whose acetochlor, alachlor, and EPTC herbicide weed management programmes have historically required safener co-formulation to achieve adequate crop tolerance. The progressive adoption of thiencarbazone-methyl, foramsulfuron, and mesosulfuron methyl herbicide mixtures for grass weed management in corn, combined with the growing deployment of new herbicide mode-of-action compounds for resistance management in corn and soybean production, is creating demand for safener compounds compatible with the newer herbicide chemistry whose crop selectivity profile requires dedicated safener support. The USDA's agricultural competitiveness programmes and land grant university crop protection research sustain applied research into herbicide safener performance.

In April 2023, Syngenta introduced its Recognition herbicide for turf management, incorporating its proprietary safener metcamifen that enables broadcast applications on sensitive turfgrass varieties where conventional herbicide application would cause significant foliar injury. The product demonstrated the commercial expansion of herbicide safener technology beyond the traditional row crop domain into specialty horticulture and turf management applications whose crop value and quality sensitivity create strong commercial motivation for safener-enabled herbicide selectivity that protects fine turfgrass cultivars while delivering effective weed control.

Herbicide Safeners Market Segment Analysis

-

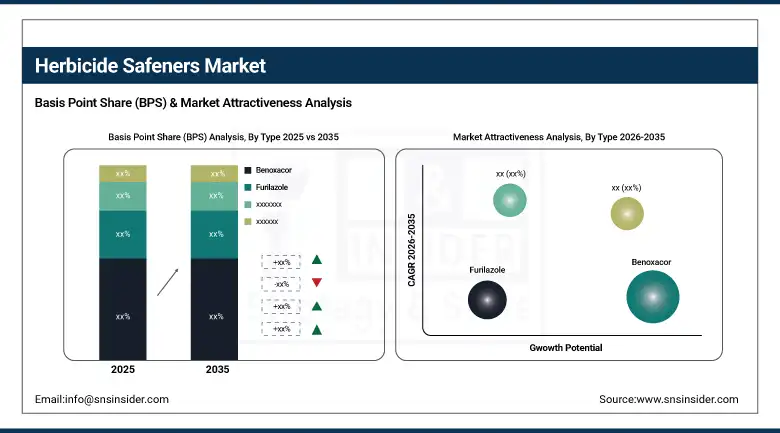

By Type, Benoxacor segment dominated the herbicide safeners market in 2025, while the isoxadifen segment is the fastest growing type.

-

By Crop Type, corn segment dominated the herbicide safeners market with the largest share in 2025, while the wheat segment is growing rapidly as new herbicide-safener combinations for grass weed resistance management in cereal production expand safener use beyond corn's traditional dominance.

-

By Application, pre-emergence segment dominated the herbicide safeners market with approximately 64% share in 2025, while the post-emergence segment is growing as in-season herbicide applications in sensitive hybrid varieties create additional safener requirements throughout the crop growth period.

-

By Formulation, liquid segment dominated the herbicide safeners market in 2025, while granular formulations are growing as seed treatment and soil-incorporated herbicide application methods whose granular format provides consistent safener delivery to the root zone during critical early crop establishment.

By Type, benoxacor dominates, isoxadifen grows fastest

Benoxacor retained the dominant type position in 2025, reflecting its commercial entrenchment as the established safener for acetochlor and alachlor chloroacetamide herbicide pre-emergence applications in corn whose decades of farmer familiarity, established distribution infrastructure, and documented crop safety performance create a durable commercial foundation. Benoxacor's efficacy in protecting corn plants from chloroacetamide herbicide injury through induction of glutathione-S-transferase enzyme activity has been validated across a broad range of corn hybrid varieties and growing conditions that establish grower confidence in the safener's crop protection reliability at commercial application rates. The global acetochlor market's sustained commercial scale in corn pre-emergence weed management sustains benoxacor procurement as the established co-formulated safener whose continued relevance reflects the foundational status of chloroacetamide herbicides in corn weed management programmes globally.

Isoxadifen is growing fastest as its effective crop tolerance enhancement across a broader herbicide chemistry spectrum than traditional safeners enables, including compatibility with ALS inhibitor herbicides used in cereal grass weed management programmes where crop safety is particularly critical due to the narrow selectivity margin of the herbicide at recommended application rates in sensitive cereal cultivars. Isoxadifen's performance in protecting wheat, barley, and corn from ALS inhibitor-induced crop stress is creating commercial adoption in European and North American cereal production systems whose integrated weed management programmes increasingly require ALS inhibitor inclusion for resistance management purposes.

By Application, pre-emergence dominates, post-emergence grows

Pre-emergence applications retained the dominant position with approximately 64% of the herbicide safeners market in 2025, reflecting the foundational commercial role of pre-emergence herbicide weed management in corn, sorghum, and cereal production systems whose residual soil herbicide applications at or immediately before crop emergence represent the highest-volume herbicide safener consumption event in the annual crop production calendar. Pre-emergence herbicide timing's crop sensitivity coincidence with the most vulnerable stage of seedling root development creates the most commercially critical crop protection requirement that herbicide safeners address, where the combination of high soil herbicide concentration, active root growth, and undeveloped crop tolerance enzymatic capacity creates peak phytotoxicity risk whose safener management determines early-season crop establishment quality.

The post-emergence application segment is the fastest-growing segment in the herbicide safeners market, driven by increasing adoption of precision weed management strategies and the growing challenge of herbicide-resistant weed populations. Farmers are increasingly relying on post-emergence herbicides to target weeds after crop establishment, improving application flexibility and weed control effectiveness. Herbicide safeners play a critical role in protecting crops from phytotoxic effects while allowing the use of more potent herbicide formulations. The expansion of high-value crops, rising demand for improved crop yields, and growing adoption of advanced agricultural practices are further supporting segment growth. In addition, precision agriculture technologies, variable-rate spraying systems, and integrated weed management programs are accelerating the use of post-emergence herbicide-safener combinations across major agricultural markets worldwide.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

Egypt |

22.8% |

|

Latin America |

Brazil |

44.2% |

North America Herbicide Safeners Market Insights

North America dominated the global herbicide safeners market in 2025 with a 39% share. The United States accounts for approximately 82.5% of North American revenues through its extensive corn belt production system's large-scale acetochlor and alachlor herbicide programme whose benoxacor and dichlormid safener requirements create the world's largest single national safener demand base. The commercial scale of U.S. corn production at approximately 90 million acres annually, combined with high herbicide application rates per acre that ensure consistent weed pressure management, creates sustained safener procurement volumes that dominate global market demand. Canada contributes supplementary demand through its corn production in Ontario and Quebec and the growing wheat and canola herbicide programmes whose safener requirements are progressively expanding.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Herbicide Safeners Market Insights

Europe held a significant share of the global herbicide safeners market in 2025. Germany, France, the United Kingdom, Spain, and Poland are the leading national markets whose intensive cereal and corn production creates herbicide safener demand from the ALS inhibitor and chloroacetamide herbicide programmes used in grass weed management. Germany accounts for approximately 28.5% of European revenues through its large cereal production area, the commercial presence of BASF and Bayer whose safener-containing herbicide portfolios define European market standards, and the progressive adoption of new safener-herbicide combinations for blackgrass and ryegrass management in wheat. The EU's pesticide regulation framework, whose active ingredient re-evaluation processes are progressively restricting certain herbicide actives, is simultaneously creating demand for new herbicide-safener combination products whose novel chemistry addresses resistant weed populations.

France and the United Kingdom contribute significant secondary market demand through their large wheat and barley acreage, the commercial importance of blackgrass management in European cereal production whose ALS inhibitor herbicide programmes require safener co-formulation, and the progressive adoption of isoxadifen-containing products for enhanced crop tolerance in sensitive cereal varieties.

Asia Pacific Herbicide Safeners Market Insights

Asia Pacific is the fastest-growing regional herbicide safeners market, driven by the expanding adoption of modern herbicide weed management in hybrid rice, corn, and wheat production systems across China, India, and Southeast Asia, the growing commercialisation of safener-containing products by domestic agrochemical companies whose product registration programmes are progressively building the safener formulation portfolio available in Asian markets. China accounts for approximately 38.5% of Asia Pacific revenues through its large hybrid rice and corn production area, the growing domestic herbicide safener manufacturing industry, and the progressive adoption of precision agricultural practices that create demand for high-performance crop protection products including safener-enabled herbicide formulations whose crop safety performance justifies the premium pricing relative to unsafened alternatives.

MEA & Latin America Herbicide Safeners Market Insights

MEA growth is driven through its corn and rice production areas whose herbicide weed management programmes increasingly incorporate safener-containing formulations as awareness of safener crop protection benefits grows among commercial growers and agricultural extension services. South Africa and Kenya contribute growing regional demand through their commercial corn and cereal production sectors.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its extensive corn production whose herbicide weed management requires safener co-formulation for effective pre-emergence and early post-emergence crop protection, and the soybean and sugarcane sectors whose herbicide programmes are progressively incorporating safener technology as new crop-safe herbicide formulations enter the Brazilian registration process. Argentina and Mexico contribute growing secondary market demand through their corn and cereal herbicide programmes.

Market Dynamics

Growth Drivers: Rising herbicide resistance necessitating new herbicide-safener combinations and expanding adoption of precision weed control in high-value crop systems driving market growth

The herbicide safeners market's growth is driven by the convergence of herbicide resistance management requirements and precision agricultural intensity that each create commercial demand for safener products above baseline pre-emergence programme demand. The documented expansion of herbicide-resistant weed populations across major agricultural regions is creating commercial urgency for new herbicide mode-of-action deployment in weed management programmes, and many of the most effective resistance management herbicide actives require safener co-formulation to achieve adequate crop tolerance in sensitive cereal, corn, and sorghum varieties. Each new herbicide active ingredient whose precision selectivity requires safener support to achieve commercial crop safety creates a new long-term safener demand category whose commercial lifetime spans the active's registration period and generates consistent annual procurement across the crop acreage where the herbicide is recommended.

Restraints: Herbicide safener incompatibility with certain herbicide-crop combinations and regulatory approval timelines for new safener actives constraining product portfolio development

Not all herbicide safeners are compatible with all herbicide formulations and crop varieties, creating selectivity gaps in herbicide weed management programmes where effective weed control options lack crop-safe application pathways that available safener products can provide. The incompatibility between specific safener compounds and certain herbicide modes of action limits the versatility of individual safener actives and creates product development requirements for each new herbicide-crop combination whose safety documentation requires dedicated field trial programmes. Regulatory approval timelines for new safener active ingredients, which require ecotoxicological assessment, residue studies, and efficacy documentation comparable to full herbicide registration, create development investment and timeline constraints that limit the pace at which new safener products enter markets requiring them for novel herbicide combination adoption.

Opportunities: Next-generation safener molecule development for grass weed resistance management and emerging market herbicide adoption expansion representing significant commercial growth frontiers

Next-generation herbicide safener molecule development whose performance characteristics address the crop tolerance requirements of new herbicide mode-of-action compounds being developed for grass weed resistance management represents the most commercially compelling innovation opportunity in the safener market. Each novel herbicide active ingredient entering commercial development for resistance management purposes that requires dedicated safener support creates a development partnership opportunity whose commercial value spans the herbicide's commercial lifetime across all markets where it achieves registration. Emerging market agricultural modernization, where smallholder and commercial farmers across Asia, Africa, and Latin America are progressively adopting chemical weed management to improve crop yield and reduce hand-weeding labour cost, creates expanding safener demand.

Recent Developments:

-

2023: Syngenta introduced Recognition herbicide for turf management incorporating its proprietary safener metcamifen, enabling broadcast applications on sensitive turfgrass varieties and demonstrating the commercial expansion of herbicide safener technology into specialty turf management applications beyond traditional row crop markets.

-

2023: Syngenta and FMC Corporation entered a collaborative herbicide safener research agreement focusing on novel safener compounds for next-generation herbicide formulations targeting grass weed resistance management in corn and sorghum production systems.

-

2022: BASF expanded its safener-containing herbicide portfolio with the commercial launch of new cereal herbicide formulations incorporating isoxadifen safener for enhanced crop tolerance in sensitive wheat and barley varieties experiencing stress from residual herbicide activity in intensively managed production systems.

Herbicide Safeners Market Key Players are:

-

Bayer AG

-

BASF SE

-

Syngenta AG

-

Corteva Agriscience

-

Nufarm Limited

-

ADAMA Ltd.

-

UPL Limited

-

FMC Corporation

-

Sumitomo Chemical Co., Ltd.

-

Nissan Chemical Corporation

-

AMVAC Chemical Corporation

-

Albaugh, LLC

-

Sipcam Oxon S.p.A.

-

Gowan Company, LLC

-

Arysta LifeScience Corporation

-

Rallis India Limited

-

PI Industries Ltd.

-

Sharda Cropchem Limited

-

Jiangsu Yangnong Chemical Group Co., Ltd.

-

Zhejiang Zhongshan Chemical Industry Group Co., Ltd.

Herbicide Safeners Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.47 Billion |

| Market Size by 2035 | USD 3.06 Billion |

| CAGR | CAGR of 7.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Benoxacor, Furilazole, Dichlormid, Isoxadifen, Fluxofenim, Others) • By Crop Type (Corn, Sorghum, Wheat, Soybean, Rice, Barley, Others) • By Application (Pre-Emergence, Post-Emergence) • By Formulation (Liquid, Granular, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Bayer AG, BASF SE, Syngenta AG, Corteva Agriscience, Nufarm Limited, ADAMA Ltd., UPL Limited, FMC Corporation, Sumitomo Chemical Co., Ltd., Nissan Chemical Corporation, AMVAC Chemical Corporation, Albaugh, LLC, Sipcam Oxon S.p.A., Gowan Company, LLC, Arysta LifeScience Corporation, Rallis India Limited, PI Industries Ltd., Sharda Cropchem Limited, Jiangsu Yangnong Chemical Group Co., Ltd., and Zhejiang Zhongshan Chemical Industry Group Co., Ltd. |

Frequently Asked Questions

The Herbicide Safeners Market is expected to grow at a CAGR of 7.63% from 2026 to 2035.

The Herbicide Safeners Market was valued at USD 1.47 Billion in 2025.

Rising herbicide resistance, increasing adoption of precision agriculture, expanding corn and cereal cultivation, development of advanced safener-compatible herbicide formulations, and ongoing agricultural modernization in emerging markets are driving the herbicide safeners market.

The Pre-Emergence segment dominated the Herbicide Safeners Market with approximately 64% share in 2023 through its role in the foundational pre-emergence herbicide weed management programme of corn, sorghum, and cereal production systems.

North America dominated the herbicide safeners market in 2023 with a 39% share, with the United States accounting for approximately 82.5% of North American revenues through its extensive corn belt production system's large-scale herbicide safener demand.

Get in Touch