High End Lighting Market Report Scope & Overview

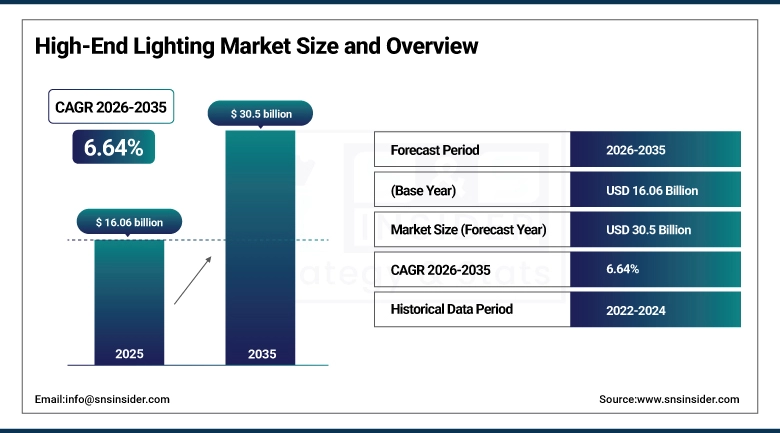

The High End Lighting Market size was valued at USD 16.06 billion in 2025 and is expected to reach USD 30.5 billion by 2035, growing at a CAGR of 6.64% from 2026–2035.

High-end lighting means high-quality lighting solutions that provide high lighting performance and are also designed to look attractive, crafted, and technologically advanced. High-end lighting caters to discriminating consumers and commercial professionals looking for lighting systems that not only fulfill their basic requirements but are also beautiful in appearance. The market for high-end lighting is getting shaped due to a combination of technologies such as LEDs, IoT, and innovative designs of lighting systems used for interiors and exteriors. The increase in construction projects in the luxury housing and commercial industries, development of smart cities, and awareness among consumers about the health impacts of lighting are driving the market.

The most significant technological trend in high-end lighting is the adoption of LEDs in these systems. The adoption of LED high-end lighting was witnessed a rise of 18% between 2021 and 2023. In addition, smart high-end lighting accounted for almost 25% of the entire market. There are many advantages of LEDs that make them suitable for high-end lighting systems including accurate color rendering, linear dimming, long life span, and suitability for wireless technology-based systems.

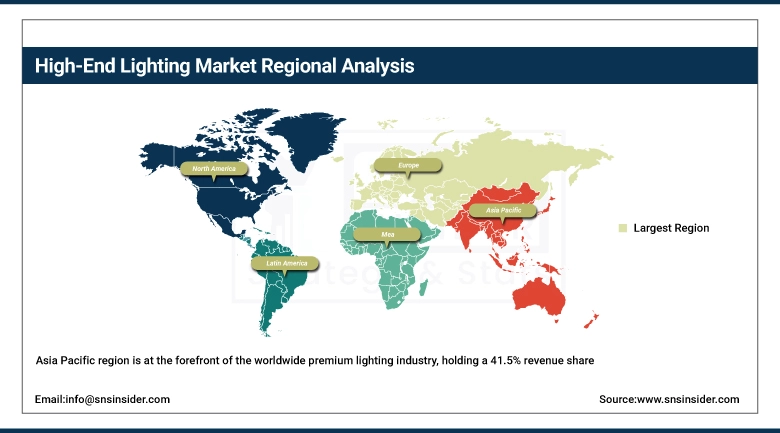

Asia Pacific holds the largest share of the global luxury lighting market with a 41.5% share in 2023, owing to the emergence of luxury real estate in major cities such as Shanghai and Shenzhen in China, increasing luxury hotels in India, and Japanese culture's emphasis on stylish interiors. In addition, Asia Pacific is anticipated to grow at the highest CAGR until 2035.

Market Size and Forecast

-

Market Size in 2025: USD 16.06 Billion

-

Market Size by 2035: USD 30.5 Billion

-

CAGR: 6.64% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on High-End Lighting Market - Request Free Sample Report

High End Lighting Market Trends Highlights:

-

LED technology dominance driving energy-efficient, long-life premium lighting with precise color control and smart integration capabilities.

-

IoT-enabled lighting systems with voice control (Alexa, Google), app-based scene setting, and circadian rhythm programming becoming standard in premium installations.

-

Human-centric lighting (HCL) that adjusts color temperature throughout the day to support occupant health, alertness, and sleep quality.

-

Integration of lights with structural features such as ceiling, wall, and furniture to create an invisible light design.

-

The adoption of smart city outdoor lighting solutions in the Asia Pacific and Middle Eastern regions to enhance the demand for premium and connected streetlights.

-

High-quality and recyclable materials that can be used in the manufacture of premium lights, including recycled metal and Forest Stewardship Council (FSC)-certified wood.

-

Customization and personalization services for architects and designers to request tailor-made finish types, sizes, and color temperatures.

U.S. High-End Lighting Market Size Outlook:

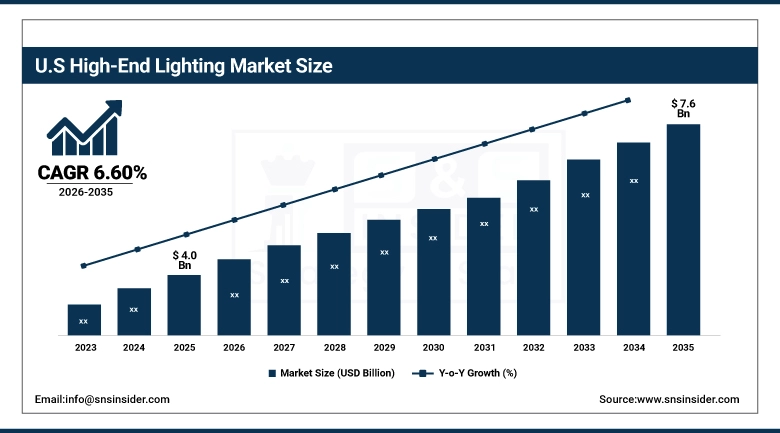

The U.S. High-End Lighting Market was valued at USD 4.0 billion in 2025 and is expected to reach USD 7.6 billion by 2035, at a CAGR of 6.60% from 2026 to 2035. The market for high-end lighting fixtures in the United States is fueled by premium residential construction, commercial building renovation, luxury hospitality projects, and the widespread uptake of smart home systems. The American consumer's preference for premium lighting fixtures is evident from their willingness to spend money on high-end lighting, especially for residential projects and kitchen and bathroom renovations where lighting fixtures play an essential role in creating the right design. Lighting is increasingly becoming a key consideration in the commercial real estate industry because companies recognize its influence on worker productivity, customer satisfaction, and brand recognition.

The U.S. Department of Energy's lighting energy efficiency program, which includes the phasing out of inefficient lighting sources, is facilitating the transition to LED-based lighting fixtures. Premium LED lighting manufacturers stand to benefit from such initiatives since they make it possible to promote high-end lighting fixtures as cost-effective alternatives to traditional lighting systems.

Market Segment Analysis

-

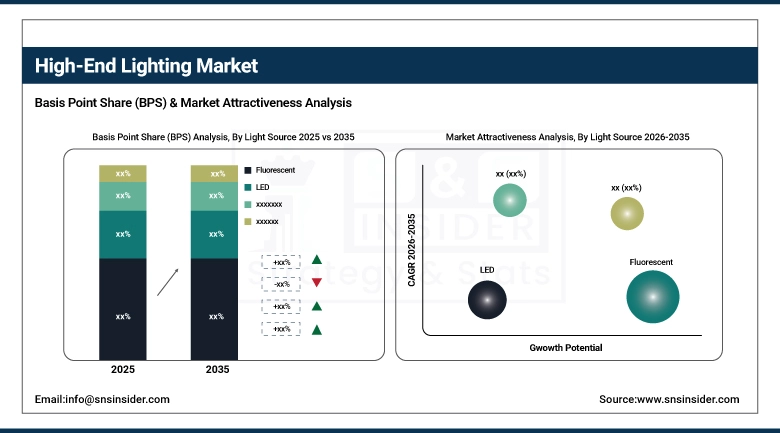

Based on Light Source, Fluorescent held 40.5% share in 2025 as the legacy dominant technology; LED is growing at the fastest CAGR as it displaces all other sources.

-

Based on Connectivity, Wired systems held 63.6% share in 2025 for reliability and infrastructure integration; Wireless is growing fastest driven by smart home adoption.

-

Based on Design, Modern styling led with 46.3% share in 2025 and is also growing at the highest CAGR, driven by demand for minimalist, IoT-compatible designs.

-

Based on End-Use, Commercial led with 41.4% share; Residential is growing at the fastest CAGR due to smart home and luxury home improvement spending.

By Light Source: Fluorescent dominant (40.5% share), LED fastest CAGR

Fluorescent light sources retain the largest market share in the high-end lighting market primarily because of their extensive installation base in commercial settings accumulated over decades. T5 and T8 fluorescent tubes have long been the workhorses of office, retail, and institutional lighting, valued for their energy efficiency relative to incandescent technology and their long service life. In the high-end segment, specialty fluorescent lamps with very high color rendering indices (CRI > 90) are used in art galleries, jewelry stores, and medical examination areas where accurate color representation is critical.

LED-based lighting is experiencing exponential growth in popularity and is quickly capturing market share for all applications under the premium lighting category. The standard for premium LED lighting has improved substantially, achieving CRI ratings over 95, R9 ratings of over 50 for good red reproduction, and accurate color temperature selection in increments of warm white at 2700K to cool daylight at 6500K. Human centric LED solutions that change in color temperature and output according to the time of day are becoming possible.

By Connectivity: Wired Connectivity (63.6% share) dominant, Wireless Connectivity fastest CAGR

Connectivity through wired lighting control systems is the most widely adopted approach among high-end lighting solutions due to their robustness, effectiveness, and maintenance requirements. Light dimming and other controls using protocols such as DALI, DMX512, KNX, and proprietary controls such as Lutron GRAFIK Eye have been instrumental in providing accurate control without signal interference in individual luminaries or zones. The availability of products in the wired lighting control systems and skilled personnel ensure that this category maintains its market leadership.

The fastest-growing connectivity solution in the high-end lighting market is wireless lighting control systems. This is attributed to the rapid proliferation of smart home ecosystems, the convenience of installing wireless systems in retrofit buildings, and the increasing preference for apps and voice commands in controlling lights in homes. The high-end lighting market for wireless control has adopted wireless technologies such as Zigbee, Z-Wave, Bluetooth Mesh, Wi-Fi, and Matter protocols.

By Design: Modern dominant and fastest growing CAGR

Modern design is the leading and fastest-growing design category among luxury lighting designs. It refers to minimalist, geometric, and architectural lighting that features clean lines, hidden light sources, and brushed metal finishes, black matte finishes, and clear acrylic materials. High-end luxury lighting in the modern design category is compatible with modern architecture, being the most suitable choice for high-end luxury houses and offices. The fact that modern design is ideally suited for the application in conjunction with smart homes because of its ability to blend into the decor while still offering precise light control is one of its major drivers.

By End-Use: Commercial (41.4% share) dominant, Residential fastest growing CAGR

Commercial applications represent the largest end-use segment, encompassing office buildings, retail stores, art galleries, museums, healthcare facilities, and educational institutions. Commercial buyers specify high-end lighting for both functional performance and the brand or design experience they create. Luxury retailers including high fashion and jewellery brands treat their lighting as a primary marketing tool, using very high CRI LED downlights and track systems to make merchandise look its absolute best.

The residential sector is witnessing the highest growth rate for the forecast period, propelled by the increase in the construction of luxurious houses, the kitchen and bathroom remodeling segment, and the swift incorporation of smart homes by wealthy individuals. Media channels such as Pinterest and Instagram have also increased consumer awareness regarding luxury lights as essential elements in interior designing.

High End Lighting Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

71% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

China |

52% |

|

Middle East & Africa |

UAE |

42% |

|

Latin America |

Brazil |

48% |

Asia Pacific High End Lighting Market Insights

The Asia Pacific region is at the forefront of the worldwide premium lighting industry, holding a 41.5% revenue share in 2023 and projected to continue at the same pace with the highest CAGR until 2035. The development of luxury property projects in major cities, smart city infrastructure projects, and rapid growth of the luxury hospitality industry are driving factors for demand. The quick rise in the number of high-net-worth individuals in the country along with the development of premium commercial properties in major cities such as Mumbai, Bangalore, and Hyderabad presents huge growth potential.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America High End Lighting Market Insights

North America is the second-largest region for high-end lighting, with the United States being the dominant market. Strong luxury residential construction, premium commercial real estate development, and sophisticated consumer awareness of smart lighting create consistent demand. American-based companies including Lutron Electronics, Cree Lighting, and Acuity Brands are important participants in the commercial specification market. The U.S. market is also a leading adopter of human-centric lighting in commercial office applications, where corporations invest in wellness-supportive lighting environments.

Europe High End Lighting Market Insights

Europe is home to many of the world's most prestigious high-end lighting manufacturers and designers, particularly in Italy (Artemide, Flos), Germany (Erco, Bega), France (DCW Editions), and Scandinavia (Louis Poulsen). European consumers and commercial specifiers are among the most sophisticated in the world regarding lighting design and quality. Strong sustainability requirements in the EU are accelerating the transition to energy-efficient LED solutions. The region's rich architectural heritage creates consistent demand for restoration and retrofit lighting in historic buildings.

Middle East & Africa and Latin America High End Lighting Market Insights

One region which is increasingly becoming relevant for luxury lighting is the Middle East, due to the huge numbers of luxury constructions taking place in the region. The grand hotels being built, ultra-luxury residences, palaces undergoing renovation and large-scale public realm constructions in Saudi Arabia, UAE, and Qatar are all using the best international lighting brands in their projects. Some of the most important demand drivers in the region include the legacy infrastructure created during the Dubai EXPO and the new NEOM and Red Sea project in Saudi Arabia. The weather in the Middle East is suitable for indoor living and thus a very large amount of luxury interior lighting projects exist.

The other important emerging region is Latin America, with Brazil, Mexico, and Chile emerging as key markets due to increased consumption levels in the rich population in these countries, as well as increased development of luxury hotels. Brazilian luxury residential architecture has been known to be keen on incorporating distinctive lighting fixtures into buildings for many years and thus creates continuous demand for the luxury lighting brands.

Market Dynamics:

Market Growth Drivers: Smart home adoption and luxury construction activity are the core demand drivers

The global luxury residential construction boom and the rapid mainstream adoption of smart home technology are the two most important growth drivers for the high-end lighting market. The integration of voice control, app-based scene setting, and circadian rhythm programming into premium lighting systems creates a compelling value proposition that justifies the price premium over conventional lighting. Human-centric lighting is emerging as a significant commercial driver as research confirms that lighting quality materially affects cognitive performance, mood, and circadian health. Large employers including technology companies and financial institutions are investing in high-quality, tunable-white lighting systems to create more productive and wellness-supportive workplaces. This application is still early-stage but growing rapidly, representing a meaningful incremental demand driver within the commercial end-use segment.

Market Restraints: High purchase cost and complex installation requirements limit adoption in budget-sensitive segments

The higher cost of premium lighting makes this solution inaccessible to medium market home consumers and small commercial firms, who would profit from its features but cannot afford such an investment. The complicated nature of the installation of wired smart lighting technology is another factor that makes such products harder to adopt. In addition, rapid technological advancements make consumers reluctant to use particular protocols in their smart lighting due to the risk of becoming obsolete quickly.

Market Opportunities: Human-centric lighting and the premium retrofit market offer high-growth opportunities

The growing body of research linking lighting quality to human health, productivity, and wellbeing is creating a premium market for scientifically designed human-centric lighting systems. Corporate wellness programs, healthcare facility design standards, and educational institution upgrades are all potential growth channels for premium tunable-white lighting. The enormous installed base of commercial buildings with outdated fluorescent or early-generation LED lighting also represents a large retrofit opportunity, where modern high-performance LED systems with smart controls can be positioned as both energy-saving and productivity-enhancing investments.

Recent Developments

-

2026: Signify advanced its connected lighting ecosystem with AI-enabled smart building solutions showcased at Light + Building 2026. The company expanded its Interact platform integration for commercial and outdoor applications, strengthening its leadership in IoT-based architectural lighting systems.

-

2026: Acuity Brands focused on expanding intelligent lighting and building management systems across commercial infrastructure projects. The company enhanced its sensor-based and software-driven lighting controls, supporting energy-efficient smart building adoption across North American construction and retrofit markets.

-

2026: OSRAM developed its portfolio with respect to its smart lighting and semiconductors optics technology products. OSRAM was committed towards developing innovations in automotive and architectural lighting products based on adaptive LED and energy-efficient lighting controls.

High-End Lighting Companies are:

-

Signify N.V.

-

Acuity Brands Inc.

-

Eaton Corporation

-

Artemide S.p.A.

-

Flos S.p.A.

-

Bega GmbH

-

Louis Poulsen A/S

-

Zumtobel Group AG

-

WAC Lighting

-

Zumtobel Lighting GmbH

-

Delta Light NV

-

Iguzzini Illuminazione S.p.A.

-

Targetti Sankey S.p.A.

-

Kreon N.V.

-

Osram GmbH

-

Cree Lighting

-

Legrand S.A.

-

Havells India Ltd.

High-End Lighting Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.06 Billion |

| Market Size by 2035 | USD 30.5 Billion |

| CAGR | CAGR of 6.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Light Source (Fluorescent, LED, Halogen, Others) • By Connectivity (Wired, Wireless) • By Design (Modern, Traditional, Classic) • By End-Use (Commercial, Residential, Industrial, Hospitality) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Signify N.V., Lutron Electronics Co. Inc., Acuity Brands Inc., Eaton Corporation, Artemide S.p.A., Flos S.p.A., Erco GmbH, Bega GmbH, Louis Poulsen A/S, Zumtobel Group AG, WAC Lighting, Zumtobel Lighting GmbH, Delta Light NV, Iguzzini Illuminazione S.p.A., Targetti Sankey S.p.A., Kreon N.V., Osram GmbH, Cree Lighting, Legrand S.A., Havells India Ltd. |

Frequently Asked Questions

Asia Pacific leads with 41.5% revenue share, driven by China's luxury construction boom and the region's smart city programs.

Residential is growing at the fastest CAGR, driven by luxury home construction, smart home adoption, and premium renovation spending.

Modern design leads with 46.3% market share and is also growing at the fastest CAGR, reflecting the demand for minimalist, smart-integrated fixtures.

The market was valued at USD 16.06 billion in 2025.

The High-End Lighting Market is expected to grow at a CAGR of 6.64% from 2026 to 2035.

Get in Touch