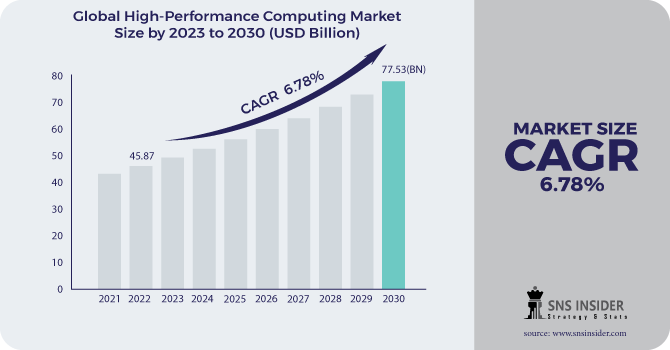

The High-Performance Computing Market size was valued at USD 45.87 Bn in 2022 and is expected to reach USD 77.53 Bn by 2030, and grow at a CAGR of 6.78 % over the forecast period 2023-2030.

High-performance computing is the use of parallel processing to run complex application programs efficiently, consistently, and fast. High-Performance Computing (HPC) is a method of accumulating computing power to offer high-performance capabilities in dealing with a wide range of challenges in research, industry, and engineering. All sorts of servers and micro-servers used for highly computational or data-intensive activities are included in HPC systems. High-performance computing makes use of computers that can accomplish more than a teraflop, or 1012 floating-point operations per second. High-performance computing is sometimes used interchangeably with supercomputing.

Get more information on High-Performance Computing Market - Request Sample Report

Currently, as HPC has become inextricably linked with economic competitiveness and scientific achievements, it is becoming increasingly vital to nations. High-performance computing is delivered via on-premise or cloud solutions. Because computers is high-tech, the cost varies proportionately. High-performance computing (HPC) enables us to analyze data and conduct complicated computations at extremely fast rates. It is made up of and composed of thousands of computing nodes that collaborate to execute one or more tasks. This is known as parallel processing.

High-performance computing is mostly employed in government and defense, as well as healthcare and life sciences, to ensure flawless delivery and faster reaction times when utilizing government programs. HPC systems may assist in meeting a wide range of defense-related needs, such as real-time data collecting and analysis, emergency operations planning, disaster modeling and analysis, simulations, surveillance, and private information encryption/decryption. They are also widely used in media and entertainment, banking, finance, and insurance, education and research, manufacturing, energy, and utilities.

KEY DRIVERS:

There is a growing demand for efficient computation, great scalability, and dependable storage.

Increasing need for high-speed, accurate data processing.

In genomics research, there is an increasing demand for high-performance computing (HPC) devices.

RESTRAINTS:

Concerns about cyber security.

Commercial high-performance computer clusters have substantial deployment costs.

OPPORTUNITY:

The deployment of hybrid high-performance computing (HPC) systems is becoming increasingly important.

Exascale computing is being introduced.

Increased investment in data centers to support HPC capability.

CHALLENGES:

Less technical knowledge in high-performance computing.

SMEs have limited expenditures.

Cooling HPC systems has unique challenges.

Advanced frameworks are required to increase fault tolerance and assure resilience.

The COVID-19 epidemic has had a massive influence on people's lives all around the world. Every firm must fight on two fronts—health and economic—and must weather this period of forced recession. With the global economic crisis costing trillions of dollars, there is widespread concern that the recovery phase may last far into early next year. Because of the present coronavirus scenario, a new work-from-home arrangement was implemented. This method aided the high-performance computing sector in resolving commercial difficulties that required large quantities of mathematical calculation and calculating skills. According to industry analysts, the HPC market will rise significantly through 2019. However, the market is expected to fall significantly in 2020.

MARKET ESTIMATION:

In 2021, the server’s category had the highest revenue share. This is due to an increase in the number of data centers as various mid-size firms and corporations engage in colocation and on-premises infrastructure to serve the rising demand for public cloud services. Furthermore, the industry is distinguished by the presence of major HPC server manufacturers. From 2023 to 2030, the services category is predicted to grow. HPC providers offer a variety of services, including as maintenance, support, and management. Support is very important while establishing and utilizing HPC systems. Maintenance services, on the other hand, include system upgrades and troubleshooting.

In 2021, the on-premise sector had the highest revenue share. This is due to the fact that governments continue to be worried about safeguarding sensitive data linked to national security and individuals' personal data, while businesses are concerned about the safety of their respective organizational data. As a result, on-premise infrastructure continues to outperform cloud-based technology. Over the projected period, the cloud sector is predicted to grow at the fastest CAGR. Because no extra computer resources are required, cloud implementation allows enterprises to reduce their operational expenses. Other advantages, including as increased efficiency and cost-effectiveness, are likely to propel the cloud segment's expansion.

In SMEs, desktop PCs are inefficient in meeting the computational and storage demands of high-end applications. As a result, SMEs are migrating toward solutions that can meet their high-computational needs. Capital, expertise, and scalability are three major problems for SMEs. To address these difficulties, SMEs are turning to cloud-based HPC solutions, which allow them to extend their IT infrastructure as needed. SMEs face tremendous competition from major organizations; as a result, in order to obtain a competitive advantage, they are progressively installing HPC solutions that help in enhancing productivity, and this trend is projected to continue over the projection period.

In 2021, the government and defense had the highest revenue share. This is due to the government and defense organizations rapidly embracing cutting-edge IT technologies to improve computing efficiency. HPC systems are likely to be adopted by government agencies to assist digitalization projects and contribute to economic development. Meanwhile, industrial procedures are often computationally and time-consuming. As a result, incumbents in the manufacturing business frequently use simulation and CAD software, as well as HPC equipment. In the manufacturing business, HPC systems may be employed specifically for computational fluid dynamics, computational structural mechanics, and computational electromagnetics to improve performance, computational speed, and data availability, leading in segment growth throughout the projection period.

On The Basis of Component

Servers

Storage

Networking Devices

Software

Services

Cloud

Others

On The Basis of Deployment

On-premise

Cloud

On The Basis of Organization Size

Small and Medium-Sized Enterprises

Large Enterprises

On The Basis of End-use

BFSI

Gaming

Media & Entertainment

Retail

Transportation

Government & Defense

Education & Research

Manufacturing

Healthcare & Bioscience

Others

.png)

Need any customization research on High-Performance Computing Market - Enquiry Now

Since the year 2022, North America has led the market with the biggest market share. The key elements identified for North America's high growth rate include technical developments as well as establishing supercomputing facilities. Furthermore, the United States is the dominant market, with other nations such as Canada projected to exhibit rapid development in the near future. The Asia Pacific is also one of the most rapidly increasing markets for high-performance computing. The causes driving such a fast-growing industry include the rising use of high-performance computers for weather forecasting and research purposes. During the anticipated period, the remainder of the areas are expected to increase at a stable rate.

REGIONAL COVERAGE:

North America

USA

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

The Netherlands

Rest of Europe

Asia-Pacific

Japan

south Korea

China

India

Australia

Rest of Asia-Pacific

The Middle East & Africa

Israel

UAE

South Africa

Rest of Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin America

The major key players are Advanced Micro Devices Inc., NEC Corporation, Hewlett Packard Enterprise, Sugon Information Industry Co. Ltd, Intel Corporation, International Business Machines Corporation, Microsoft Corporation, Dell EMC (Dell Technologies Inc.), Dassault Systems SE, and Lenovo Group Ltd & Other Players

| Report Attributes | Details |

|---|---|

| Market Size in 2022 | US$ 45.27 Billion |

| Market Size by 2030 | US$ 77.53 Billion |

| CAGR | CAGR of 6.78% From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Servers, Storage, Networking Devices, Software, Services, Cloud, and Others) • by Deployment (On-premise and Cloud) • by Organization Size (Small and Medium-Sized Enterprises and Large Enterprises) • by End-use (BFSI, Gaming, Media & Entertainment, Retail, Transportation, Government & Defense, Education & Research, Manufacturing, Healthcare & Bioscience, and Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Micro Devices Inc., NEC Corporation, Hewlett Packard Enterprise, Sugon Information Industry Co. Ltd, Intel Corporation, International Business Machines Corporation, Microsoft Corporation, Dell EMC (Dell Technologies Inc.), Dassault Systems SE, and Lenovo Group Ltd |

| Key Drivers | •There is a growing demand for efficient computation, great scalability, and dependable storage. •Increasing need for high-speed, accurate data processing. |

| RESTRAINTS | •Concerns about cyber security. •Commercial high-performance computer clusters have substantial deployment costs. |

Ans: - The forecast period of the High-Performance Computing market is 2022-2028.

Ans: - There is a growing demand for efficient computation, great scalability, and dependable storage.

Ans: - 4 segments of the High-Performance Computing Market.

Ans: - The major key players are Advanced Micro Devices Inc., NEC Corporation, Hewlett Packard Enterprise, Sugon Information Industry Co. Ltd, Intel Corporation, International Business Machines Corporation, Microsoft Corporation, Dell EMC (Dell Technologies Inc.), Dassault Systems SE, and Lenovo Group Ltd

Ans: - Manufacturers, Research Institutes, university libraries, suppliers, and distributors of the product.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 COVID-19 Impact Analysis

4.2 Impact of Ukraine- Russia war

4.3 Impact of ongoing Recession

4.3.1 Introduction

4.3.2 Impact on major economies

4.3.2.1 US

4.3.2.2 Canada

4.3.2.3 Germany

4.3.2.4 France

4.3.2.5 United Kingdom

4.3.2.6 China

4.3.2.7 Japan

4.3.2.8 South Korea

4.3.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. High-Performance Computing Market Segmentation, by Component

8.1 Servers

8.2 Storage

8.3 Networking Devices

8.4 Software

8.5 Services

8.6 Cloud

8.7 Others

9. High-Performance Computing Market Segmentation, by Deployment

9.1 On-premise

9.2 Cloud

10. High-Performance Computing Market Segmentation, by Organization Size

10.1 Small and Medium-Sized Enterprises

10.2 Large Enterprises

11. High-Performance Computing Market Segmentation, by End-use

11.1 BFSI

11.2 Gaming

11.3 Media & Entertainment

11.4 Retail

11.5 Transportation

11.6 Government & Defense

11.7 Education & Research

11.8 Manufacturing

11.9 Healthcare & Bioscience

11.10 Others

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 USA

12.2.2 Canada

12.2.3 Mexico

12.3 Europe

12.3.1 Germany

12.3.2 UK

12.3.3 France

12.3.4 Italy

12.3.5 Spain

12.3.6 The Netherlands

12.3.7 Rest of Europe

12.4 Asia-Pacific

12.4.1 Japan

12.4.2 South Korea

12.4.3 China

12.4.4 India

12.4.5 Australia

12.4.6 Rest of Asia-Pacific

12.5 The Middle East & Africa

12.5.1 Israel

12.5.2 UAE

12.5.3 South Africa

12.5.4 Rest

12.6 Latin America

12.6.1 Brazil

12.6.2 Argentina

12.6.3 Rest of Latin America

13. Company Profiles

13.1 Advanced Micro Devices Inc.

13.1.1 Financial

13.1.2 Products/ Services Offered

13.1.3 SWOT Analysis

13.1.4 The SNS view

13.2 NEC Corporation

13.3 Hewlett Packard Enterprise

13.4 Sugon Information Industry Co. Ltd

13.5 Intel Corporation

13.6 International Business Machines Corporation

13.7 Microsoft Corporation

13.8 Dell EMC (Dell Technologies Inc.)

13.9 Dassault Systems SE

13.10 Lenovo Group Ltd

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Connected Mining Market size was valued at 11.9 billion in 2022 and is anticipated to reach USD 28.22 billion in 2030 with a growing CAGR of 11.4% from 2023 to 2030.

The LTE And 5G Broadcast market size was valued at USD 785.3 Million in 2023 and is expected to reach USD 1758.2 Million by 2031 and grow at a CAGR of 10.6% over the forecast period 2024-2031.

The Security Orchestration, Automation, and Response (SOAR) Market size was valued at USD 1.01 Bn in 2022 and is expected to reach USD 2.92 Bn by 2030, and grow at a CAGR of 14.12% over the forecast period 2023-2030.

The Data Center Automation Market size was valued at USD 7.96 billion in 2022 and is expected to grow to USD 21.0 billion by 2030 and grow at a CAGR of 12.9 % over the forecast period of 2023-2030.

Wireless Microphone Market size was valued at USD 1.82 billion in 2022 and is expected to grow to USD 3.76 billion by 2030 and grow at a CAGR of 9.52 % over the forecast period of 2023-2030.

The Digital Farming Market size was valued at USD 22.12 billion in 2022 and is expected to grow to USD 58.72 billion by 2030 and grow at a CAGR of 12.98 % over the forecast period of 2023-2030.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd