Hydroxyapatite Market Report Scope & Overview:

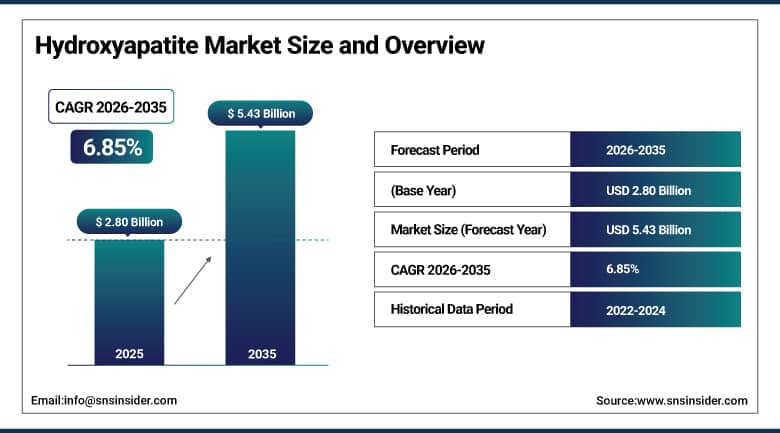

Hydroxyapatite Market was valued at USD 2.80 billion in 2025 and is expected to reach USD 5.43 billion by 2035, growing at a CAGR of 6.85% from 2026-2035.

The Hydroxyapatite Market is driven by the the calcium phosphate mineral whose chemical formula Ca₁₀(PO₄)₆(OH)₂ constitutes approximately 70% of human bone mineral content and is the primary inorganic component of tooth enamel and dentin occupies a unique position in the biomaterials landscape as both the benchmark for bone-compatible material biocompatibility and the standard against which synthetic bone substitutes are evaluated. The material's commercial applications span a range from reconstructive surgery to analytical chemistry: as a bone graft substitute in orthopedic and craniofacial surgery, where its chemical composition promotes osseointegration; as a dental restoration material in coatings, bone grafts, and root canal sealers; as a drug delivery carrier whose mesoporous structure enables controlled release of therapeutic agents; as a chromatography medium whose selective protein-binding characteristics separate biomolecules in pharmaceutical manufacturing; and in a growing range of cosmetic and nutraceutical applications where its biocompatibility and regulatory acceptance sustain consumer product formulation. It reflects the compounding growth of orthopedic and dental procedure volumes driven by aging populations requiring bone reconstruction, joint replacement, and dental implant procedures and the expanding application of nanoscale hydroxyapatite in drug delivery and tissue engineering whose performance advantages over conventional formulations are sustaining R&D investment and commercial adoption.

The American Academy of Orthopedic Surgeons documents that over 4.5 million orthopedic procedures requiring bone graft or synthetic bone substitute material are performed annually in the United States creating the domestic hydroxyapatite demand base whose procedure growth tracks aging population demographics. The dental implant market's compound growth where global dental implant placements exceeded 15 million procedures annually in the most recently documented year creates proportional demand for hydroxyapatite-containing dental bone grafts, implant surface coatings, and periimplant defect repair materials.

Hydroxyapatite Market Size and Forecast

-

Market Size in 2025: USD 2.80 Billion

-

Market Size by 2035: USD 5.43 Billion

-

CAGR: 6.85% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Hydroxyapatite Market - Request Free Sample Report

Hydroxyapatite Market Trends

-

Nano-hydroxyapatite technology advancement where particle size reduction below 100nm creates nanocrystalline hydroxyapatite whose surface area, protein adsorption, and cellular interaction properties improve bone formation outcomes versus micron-scale alternatives is sustaining R&D investment and premium pricing in orthopedic and drug delivery applications.

-

Bioprinting of hydroxyapatite scaffolds where 3D bioprinting of composite hydroxyapatite-polymer scaffolds creates patient-specific bone defect reconstruction geometries that conventional block and granule formats cannot achieve is advancing from research demonstration to clinical application.

-

Ion-substituted hydroxyapatite development where calcium substitution with strontium, magnesium, zinc, or silver ions modifies biological activity, stimulates bone formation, or imparts antimicrobial properties is creating specialty hydroxyapatite formulations whose performance advantages sustain premium positioning.

-

Hydroxyapatite coating of orthopedic implants where plasma-sprayed HA coatings on titanium joint replacement implants accelerate osseointegration and improve long-term fixation is an established application sustaining consistent procurement alongside newer direct-surface treatment alternatives.

-

Drug-loaded hydroxyapatite for localized antibiotic delivery where antibiotic-impregnated hydroxyapatite granules placed in bone defects following infection provide sustained local drug release while simultaneously serving as bone graft material addresses the periprosthetic joint infection management challenge whose clinical burden sustains innovation investment.

-

Hydroxyapatite in oral care consumer products where nano-hydroxyapatite in toothpaste and mouthwash is marketed as an enamel remineralization agent replacing fluoride in consumer preference segments is growing with oral care premiumization trends.

-

Injectable hydroxyapatite formulations where flowable calcium phosphate cement systems enable minimally invasive bone defect augmentation through injection rather than surgical placement are growing with the minimally invasive orthopedic procedure trend.

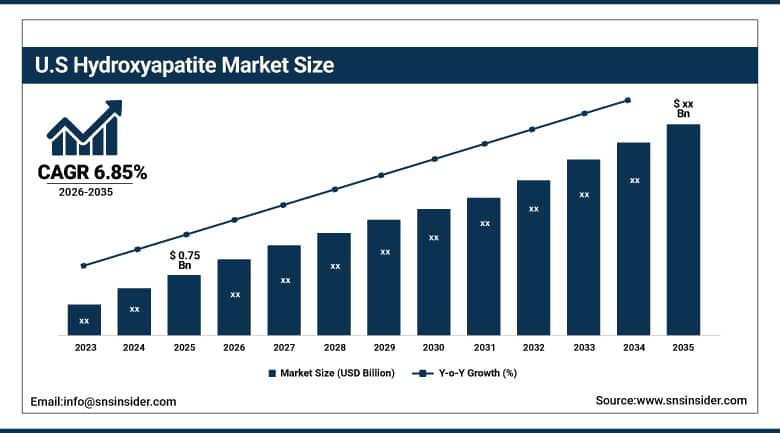

U.S. Hydroxyapatite Market was valued at approximately USD 0.75 billion in 2025 and is expected to grow at a CAGR of 6.85% from 2026-2035.

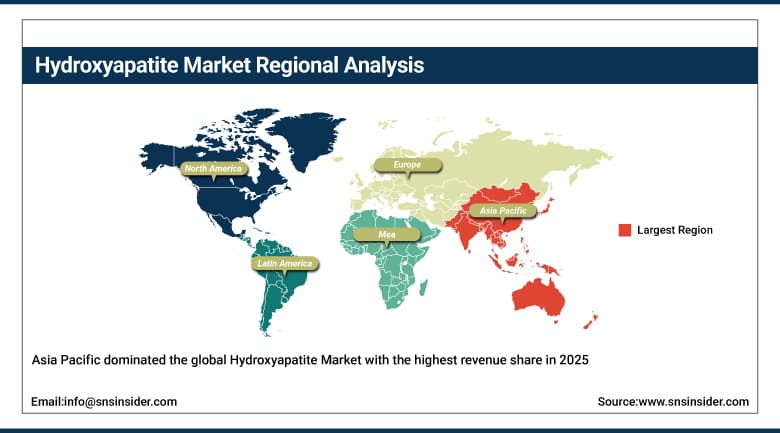

Asia Pacific dominated the global Hydroxyapatite Market with the highest revenue share in 2025, reflecting the region's combination of the largest orthopedic procedure volume where China, India, Japan, and South Korea collectively perform the highest number of bone reconstruction, joint replacement, and spinal fusion procedures annually and the region's established hydroxyapatite production industry whose China-based manufacturers including Nanjing Emperor Nano Materials, Kunshan Chinese Technology, and Shanghai Apptec supply both domestic and international markets. China's rapidly growing orthopedic surgery market where joint replacement procedures are growing at 15-20% annually driven by an aging population and improved healthcare access under the national insurance coverage expansion creates proportional hydroxyapatite demand whose domestic production capabilities serve the majority of consumption without the import dependence that would elevate procurement cost.

The Asia Pacific Orthopedic Association documents that orthopedic procedure volumes across the region are growing at 8-10% annually nearly double the global average driven by aging demographics in Japan and South Korea and rapidly expanding healthcare access in China and India. Evonik Industries' VESTAKEEP dental hydroxyapatite specified in dental implant coatings by Straumann, Dentsply Sirona, and Nobel Biocare demonstrates the international B2B supply chain where European specialty chemical producers supply hydroxyapatite intermediates to global medical device manufacturers for incorporation in premium dental restoration products.

Hydroxyapatite Market Segment Analysis

-

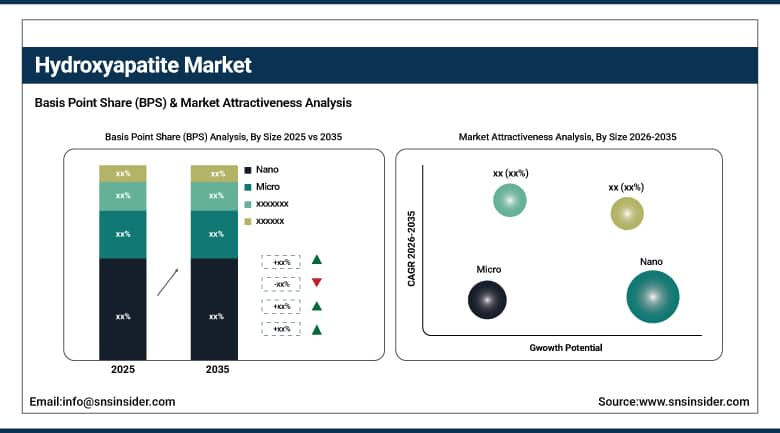

By Size, Nano-sized growing at fastest CAGR; Micro-sized holding significant share in 2025.

-

By Application, Orthopedics & Bone Repair dominated the Hydroxyapatite Market; Drug Delivery growing rapidly.

-

By End Use, Hospitals & Clinics dominated; Research Institutes growing as nano-HA research expands.

By Size: Nano fastest growing, Micro significant

Nano-sized hydroxyapatite is growing at the fastest CAGR, driven by the superior biological performance that nanocrystalline HA demonstrates in bone regeneration applications where particle sizes mimicking the 20-50nm natural bone mineral crystals achieve more complete cellular interaction, protein adsorption, and osteogenic stimulation than micron-scale alternatives and the expanding drug delivery applications where nano-HA's high surface area and porous structure enable higher drug loading and more controlled release profiles. Micro-sized hydroxyapatite maintains significant market share as the established form in traditional orthopedic bone graft granule and block applications where their handling characteristics during surgical implantation, established regulatory approval history, and cost-competitive production sustain specification in the majority of routine bone graft procedures.

By Application: Orthopedics dominant, Drug Delivery growing

Orthopedics and Bone Repair held the dominant application position in the Hydroxyapatite Market in 2025, reflecting both the historical commercial foundation of hydroxyapatite in bone graft substitution where synthetic HA has progressively replaced autologous bone graft in applications whose morbidity of donor site harvesting sustains synthetic alternative adoption and the growing procedure volumes in spinal fusion, cranio-maxillofacial reconstruction, and orthopedic defect repair that aging populations sustain. Dentistry represents a significant and closely related application where hydroxyapatite in dental bone grafts, implant coatings, and periodontal defect repair sustains consistent demand from the global dental implant procedure growth. Drug Delivery is growing at an above-market application CAGR, driven by the expanding pharmaceutical research investment in hydroxyapatite as a controlled-release drug delivery platform for cancer therapeutics, antibiotics, and bone anabolic agents.

Hydroxyapatite Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

52% |

|

North America |

United States |

85% |

|

Europe |

Germany |

28% |

|

Middle East & Africa |

Israel |

38% |

|

Latin America |

Brazil |

52% |

Asia Pacific Hydroxyapatite Market Insights

Asia Pacific dominated the global Hydroxyapatite Market with the highest revenue share in 2025, driven by China's established hydroxyapatite production industry and the region's growing orthopedic and dental procedure volumes. China's domestic hydroxyapatite producers serve both domestic medical device manufacturers and export markets, with Chinese-origin hydroxyapatite powders and granules achieving cost-competitive positioning against Western producers in price-sensitive emerging market applications.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Hydroxyapatite Market Insights

North America holds a significant Hydroxyapatite Market position driven by the United States' sophisticated orthopedic and dental surgery markets, the concentration of leading medical device companies specifying hydroxyapatite materials Zimmer Biomet, DePuy Synthes (J&J), and Stryker in orthopedics; Dentsply Sirona, Straumann, and Nobel Biocare in dental and the active academic and pharmaceutical research programs investing in advanced nano-HA drug delivery systems. The U.S. FDA's established 510(k) and PMA regulatory pathways for hydroxyapatite-containing bone graft substitutes and dental materials sustain commercial product development investment at scale that other regulatory frameworks' longer review timelines discourage.

Europe Hydroxyapatite Market Insights

Europe's Hydroxyapatite Market is driven by the EU's sophisticated medical device market whose CE marking regulatory pathway enables hydroxyapatite bone graft and dental product commercialization and the active biomaterial research ecosystem including Germany's Charité, France's École Polytechnique, and UK's Loughborough University sustaining next-generation hydroxyapatite formulation development. European specialty chemical producers including Evonik Industries and Merck KGaA sustain high-purity hydroxyapatite production for dental and pharmaceutical applications.

MEA and Latin America Hydroxyapatite Market Insights

The Middle East and Africa's Hydroxyapatite Market is growing with expanding healthcare infrastructure where Gulf state hospitals are investing in advanced orthopedic and dental surgery capabilities and the growing awareness of advanced bone graft materials among the region's expanding surgical specialization. Latin America's market concentrates in Brazil's established orthopedic and dental surgery markets whose procedure volumes sustain consistent hydroxyapatite demand from domestic and international material suppliers.

Hydroxyapatite Market Growth Drivers:

- Aging population orthopedic procedure growth and nano-HA drug delivery expansion driving sustained hydroxyapatite market growth globally

The Hydroxyapatite Market's 6.85% CAGR is driven by the structural growth of orthopedic and dental procedure volumes sustained by the global aging population whose musculoskeletal and dental health deterioration creates consistent bone reconstruction and dental implant procedure demand and the expanding application of nano-hydroxyapatite in pharmaceutical drug delivery whose controlled-release performance advantages over conventional polymer carriers create new commercial demand above the established orthopedic and dental segments. The relationship between procedure volume and hydroxyapatite demand is not directly proportional as each procedure's bone graft material consumption grows with the adoption of synthetic graft substitutes over autologous bone harvest creating above-procedure-growth material demand as synthetic substitute penetration increases.

Hydroxyapatite Market Restraints:

- Resorption rate variability and manufacturing scalability creating hydroxyapatite market challenges globally

Hydroxyapatite's biological performance is constrained by its relatively slow resorption rate where pure crystalline HA resorbs over years to decades rather than the months that bone healing completion requires creating a mismatch between scaffold degradation and bone regeneration timelines that limits HA specification in favor of biphasic calcium phosphate formulations whose beta-tricalcium phosphate component provides faster resorption kinetics alongside HA's biocompatibility. Manufacturing scalability of nano-hydroxyapatite at the particle size consistency, purity, and sterility standards required for clinical implantation creates quality control challenges whose resolution adds cost above micron-scale conventional hydroxyapatite production.

Hydroxyapatite Market Opportunities:

- Bioprinted patient-specific scaffolds and nano-HA oral care products creating significant hydroxyapatite market growth opportunities globally

Bioprinted patient-specific hydroxyapatite scaffolds where CT scan data is used to design and 3D-print exact-geometry HA scaffolds matching a patient's craniofacial defect or spinal fusion cage requirement represent the hydroxyapatite market's most technically advanced growth opportunity. Each bioprinted patient-specific scaffold commands premium pricing above standard implant formats reflecting the design, material, and manufacturing complexity of individualized production whose revenue per procedure substantially exceeds standard block or granule graft material pricing. The nano-hydroxyapatite oral care product market where toothpaste, mouthwash, and dental varnish formulations containing nano-HA provide enamel remineralization benefits promoted as fluoride-free alternatives is growing with the consumer wellness trend whose natural product preference sustains premium nano-HA oral care adoption.

Recent Developments:

-

2026: Zimmer Biomet launched its Vivify HA Plus biphasic calcium phosphate granule with 70% hydroxyapatite / 30% beta-tricalcium phosphate composition optimized for maximal osteoconductivity alongside controlled resorption rate achieving CE marking and FDA 510(k) clearance simultaneously reporting 25% improvement in bone volume formation at 6-month histological evaluation versus standard HA granule controls in a 200-patient multicenter clinical study that established Vivify HA Plus as the company's primary synthetic bone graft substitute across spinal fusion and foot/ankle orthopedic surgery indications.

-

2025: Evonik Industries launched its RESOMER HA nanocomposite combining nano-hydroxyapatite with biodegradable PLGA polymer in an injectable flowable cement format enabling minimally invasive bone defect augmentation through percutaneous injection that achieves mechanical support within 15 minutes of injection and complete resorption with bone replacement over 12-18 months, targeting the vertebroplasty and kyphoplasty market whose minimally invasive approach creates patient recovery advantages that open surgical bone grafting cannot provide at equivalent spinal defect repair.

-

2025: GC Corporation (Japan) launched its MI Paste Ultra nano-hydroxyapatite professional dental remineralizing cream incorporating 10% nano-HA particles at 50nm average diameter whose in vitro enamel remineralization efficacy matched sodium fluoride at equivalent application protocols receiving American Dental Association acceptance seal as the first ADA-accepted nano-hydroxyapatite remineralizing agent, enabling dental professional recommendation that sustains premium consumer product adoption above the broader nano-HA oral care market.

Hydroxyapatite Market Key Players

Some of the Hydroxyapatite Market Companies

-

Zimmer Biomet Holdings Inc.

-

DePuy Synthes (Johnson & Johnson)

-

Stryker Corporation

-

Evonik Industries AG

-

Merck KGaA (Sigma-Aldrich)

-

Fluidinova SA

-

Himed LLC

-

GC Corporation

-

Olympus Terumo Biomaterials Corp.

-

Berkeley Advanced Biomaterials Inc.

-

Bio-Rad Laboratories Inc.

-

Calcitec Inc.

-

Nanjing Emperor Nano Materials Co. Ltd.

-

Shanghai Apptec Co. Ltd.

-

Trans-Tissue Technologies LLC

-

OsteoMedical Group SA

-

Genesys Spine (Alphatec)

-

SigmaGraft Biomaterials Inc.

-

Innotere GmbH

-

Xpand Biotechnology BV

Hydroxyapatite Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.80 Billion |

| Market Size by 2035 | USD 5.43 Billion |

| CAGR | CAGR of 6.85% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Size (Nano, Micro, and Macro) • By Application (Orthopedics & Bone Repair, Dentistry, Drug Delivery, Chromatography, and Others) • By End Use (Hospitals & Clinics, Research Institutes, Pharmaceutical & Biotechnology Companies, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cam Bioceramics B.V., SofSera Corporation, Fluidinova, Berkeley Advanced Biomaterials, Taihei Chemical Industrial Co., Ltd., SigmaGraft, Bio-Rad Laboratories, Inc., Merz North America, Inc., Premier Biomaterials, Himed, Nano Interface Technology, Sangi Co., Ltd., Osartis GmbH, Zellwerk GmbH, Himed Japan Co., Ltd., Medtronic, Collagen Matrix, Inc., Kuros Biosciences, BioInteractions Ltd., Xtant Medical |

Frequently Asked Questions

The Hydroxyapatite Market was valued at USD 2.80 billion in 2025.

Asia Pacific dominated with China leading; North America holds a significant position.

Orthopedics & Bone Repair dominated; Drug Delivery is growing rapidly.

Nano-sized hydroxyapatite is growing at the fastest CAGR; Micro-sized holds significant existing share.

The Hydroxyapatite Market is expected to grow at a CAGR of 6.85% from 2026 to 2035.

Get in Touch