Immunoprotein Diagnostic Testing Market Report Scope & Overview:

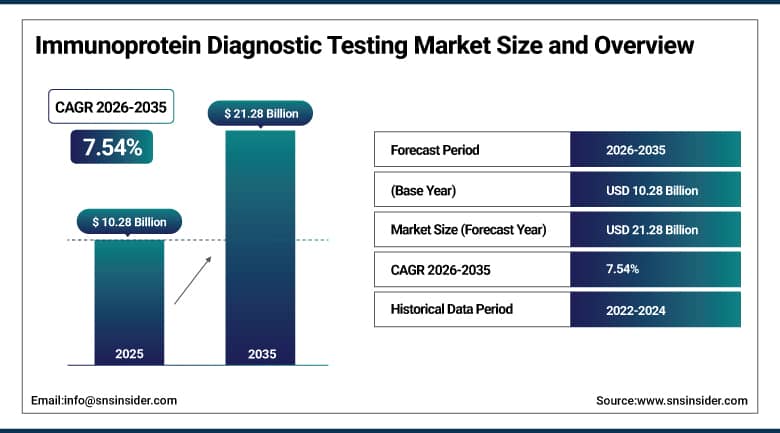

The Immunoprotein Diagnostic Testing Market was valued at USD 10.28 Billion in 2025 and is expected to reach USD 21.28 Billion by 2035, growing at a CAGR of 7.54% from 2026–2035.

The global immunoprotein diagnostic testing market is growing at commercially broad-based pace. Immunoprotein diagnostic testing encompasses the quantitative measurement of specific blood proteins involved in immune system function, acute phase response, and disease pathology including immunoglobulins, C-reactive protein, free light chains, complement proteins, pre-albumin, and haptoglobin. These proteins serve as established clinical biomarkers for immune deficiency, autoimmune disease, and hemolytic conditions whose diagnostic utility creates consistent institutional procurement across hospital, clinical, and research laboratory settings. Market growth is driven by rising incidence of chronic diseases, infectious diseases, and immunological disorders, advancements in immunoassay technology, and increasing demand for point-of-care immunoprotein testing enabling rapid clinical decision-making.

In January 2025, Beckman Coulter launched enhanced immunoprotein panel on the DxI 9000 Access immunoassay analyzer, incorporating high-sensitivity CRP, serum protein electrophoresis, and free light chain measurement in a unified automated workflow for hematology and immunology laboratory testing. The launch reflects the commercial direction of immunoprotein diagnostic testing toward consolidated automated platforms.

Market Size and Forecast:

-

Market Size in 2026E: USD 11.06 Billion

-

Market Size by 2035: USD 21.28 Billion

-

CAGR: 7.54% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Immunoprotein Diagnostic Testing Market - Request Free Sample Report

Immunoprotein Diagnostic Testing Market Trends:

-

High-sensitivity C-reactive protein (hs-CRP) testing adoption is increasing for cardiovascular risk assessment in preventive healthcare programs.

-

Free light chain assays are expanding in multiple myeloma diagnosis and monitoring, supporting precision oncology applications.

-

Point-of-care immunoprotein testing is growing in emergency and ICU settings for rapid infection and inflammation assessment.

-

Multiplex immunoprotein panels are improving efficiency by enabling simultaneous measurement of multiple biomarkers from a single sample.

-

AI-based interpretation platforms are enhancing diagnostic accuracy by integrating immunoprotein results with patient history and clinical data.

U.S. Immunoprotein Diagnostic Testing Market Outlook

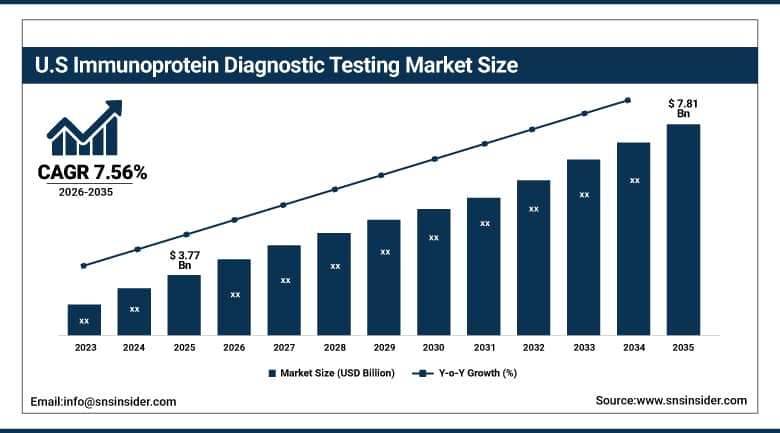

The U.S. Immunoprotein Diagnostic Testing Market was valued at approximately USD 3.77 Billion in 2025 and is expected to reach approximately USD 7.81 Billion by 2035, growing at a CAGR of approximately 7.56%.

The U.S. is the most commercially sophisticated immunoprotein diagnostic testing market within North America’s dominant revenue position. Beckman Coulter, Abbott Diagnostics, Siemens Healthineers, Roche Diagnostics, and Thermo Fisher Scientific’s U.S. operations collectively define the commercial immunoprotein diagnostic landscape. The high incidence of autoimmune diseases, hematological malignancies, and chronic infectious diseases in the U.S. creates above-average immunoprotein testing volume. MYELOMA disease monitoring’s free light chain assay requirement, the acute care sector’s CRP and procalcitonin infection assessment, and the allergy testing infrastructure’s IgE measurement collectively sustain structured commercial immunoprotein procurement across hospital, reference laboratory, and physician office laboratory settings.

In January 2023, Beckman Coulter Diagnostics entered a co-development partnership with MeMed for the MeMed BV test, developed for application on the Access Family of Immunoassay Analyzers to differentiate bacterial from viral infections, enhancing diagnostic efficacy and patient care. The host-response immunoprotein biomarker’s ability to distinguish bacterial from viral infection aetiology creates clinical decision support whose antibiotic stewardship application addresses the commercially urgent infectious disease diagnostic need.

Immunoprotein Diagnostic Testing Market Segmentation Analysis

-

By Type, the immunoglobulin diagnostic tests segment dominated the market with 28.15% share in, while the free light chain diagnostic tests segment is the fastest growing.

-

By Technology, the ELISA segment dominated the market with approximately 42% share in 2025, while the chemiluminescence immunoassay (CLIA) segment is the fastest growing.

-

By Application, the infectious disease testing segment dominated the market with approximately 32% share in 2025, while the oncology testing segment is the fastest growing.

-

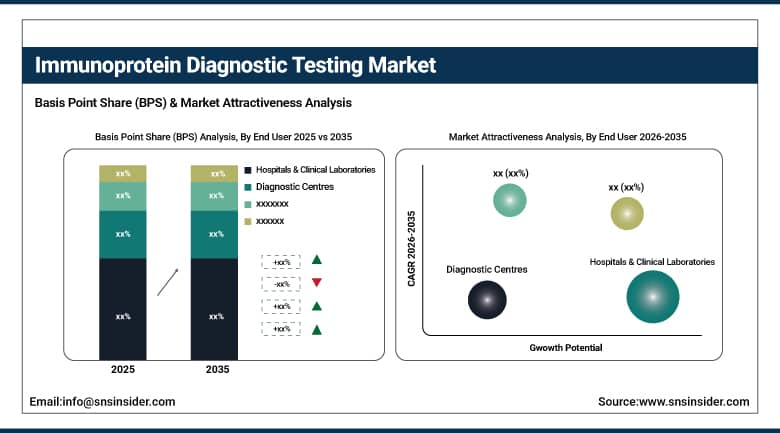

By End User, the hospitals & clinical laboratories segment dominated the market with approximately 52% share in 2025, while the diagnostic centers segment is the fastest growing.

By End User, hospitals dominate, diagnostic centers grow fastest

Hospitals and clinical laboratories retained the dominant end-user position with approximately 52% of the immunoprotein diagnostic testing market in 2025. The hospital laboratory’s comprehensive immunoprotein test menu, high daily test volume from inpatient, emergency, and outpatient services, and the 24/7 availability requirement for critical infectious disease and hematology testing create the most commercially intensive immunoprotein diagnostic procurement environment. Each major hospital laboratory’s comprehensive immunoassay analyzer installation creates multi-analyte immunoprotein procurement relationships whose consumable consumption sustains consistent commercial volume across the analyzer’s operational lifetime.

Diagnostic centers are the fastest-growing end user because outpatient laboratory consolidation into centralized specialist diagnostic networks creates high-throughput immunoprotein testing demand whose volume and efficiency requirements drive premium automated immunoassay system specification. Commercial laboratory operators’ focus on test menu breadth, turnaround time, and per-test cost economics creates above-average investment in high-sensitivity CLIA platforms whose capability creates comprehensive immunoprotein service delivery to physician office and specialist clinic customers.

By Type, immunoglobulin tests dominate, free light chain grows fastest

Immunoglobulin diagnostic tests retained the dominant type position with 28.15% of the immunoprotein diagnostic testing market in 2025. The clinical breadth of immunoglobulin quantification across primary immune deficiency surveillance, chronic infection monitoring, autoimmune disease assessment, and allergy diagnosis creates the diverse and highest-volume single immunoprotein test type. Each patient with a suspected primary immunodeficiency requires IgG, IgA, and IgM quantification whose test volume scales with the growing recognition of primary immunodeficiency as a broader condition category than historically diagnosed.

Free light chain diagnostic tests are the fastest-growing type because multiple myeloma’s progressive treatment landscape is creating above-average kappa and lambda free light chain assay procurement for initial diagnosis, treatment response monitoring, and minimal residual disease assessment. The International Myeloma Working Group’s updated diagnostic criteria incorporating free light chain ratio as a diagnostic criterion creates mandatory test adoption in every hematology center managing myeloma patients.

By Application, infectious disease dominates, oncology grows fastest

Infectious disease testing retained the dominant application position with approximately 32% of the immunoprotein diagnostic testing market in 2025. The clinical breadth of immunoprotein biomarker application in infectious disease management, encompassing C-reactive protein and procalcitonin for infection severity and sepsis risk assessment, IgM quantification for acute infection identification, and immunoglobulin response monitoring for chronic infection management, creates the commercially significant aggregate infectious disease application volume.

Oncology testing is the fastest-growing application because precision oncology’s systematic adoption of protein biomarkers for treatment selection, response monitoring, and residual disease assessment is creating structured hematology and oncology laboratory immunoprotein procurement. Multiple myeloma’s free light chain, serum protein electrophoresis, and immunofixation testing creates the most commercially concentrated oncology immunoprotein procurement category. Solid tumor immunotherapy’s immune status monitoring requirement creates additional oncology application categories whose adoption compounds with immunotherapy’s extraordinary commercial expansion.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Immunoprotein Diagnostic Testing Market Insights

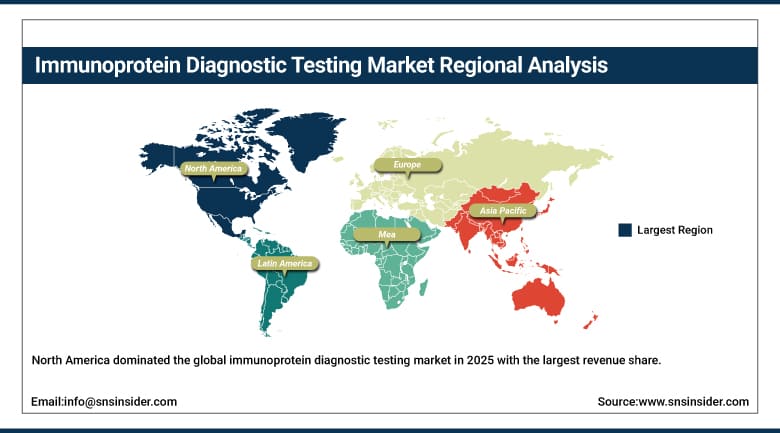

North America dominated the global immunoprotein diagnostic testing market in 2025 with the largest revenue share, driven by high healthcare expenditure, advanced diagnostic infrastructure, and the presence of Beckman Coulter, Abbott, Siemens Healthineers, Roche Diagnostics, and Thermo Fisher Scientific. The United States accounts for approximately 87.4% of North American revenues through its high prevalence of autoimmune disease, hematological malignancy, and chronic infectious disease creating above-average immunoprotein testing volume per capita.

Canada contributes approximately 12.6% of North American revenues through its universal healthcare system’s laboratory testing investment, the growing immunology specialty network’s immunoprotein test adoption, and the cancer center’s hematological malignancy monitoring infrastructure.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Immunoprotein Diagnostic Testing Market Insights

Europe is a technically sophisticated immunoprotein diagnostic testing market where the European Medicines Agency’s regulatory framework, national reimbursement systems’ immunoprotein test coverage, and the pharmaceutical industry’s clinical trial biomarker infrastructure create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced clinical laboratory network, the pharmaceutical industry’s clinical trial immunoprotein biomarker procurement, and Siemens Healthineers’ domestic commercial presence.

The United Kingdom, France, and the Netherlands are significant secondary markets where NHS and equivalent national laboratory service networks create institutional-scale immunoprotein test procurement, and the oncology center’s myeloma monitoring programme creates above-average hematology immunoprotein testing volume.

Asia Pacific Immunoprotein Diagnostic Testing Market Insights

Asia Pacific is the fastest-growing regional immunoprotein diagnostic testing market, driven by expanding healthcare infrastructure in China and India, rising chronic disease and infectious disease burden, growing laboratory automation adoption, and increasing awareness of immunoprotein biomarkers’ clinical utility. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary hospital network expansion, the government’s healthcare infrastructure investment, and the domestic diagnostic manufacturer’s growing immunoassay platform market penetration.

India’s rapidly expanding private laboratory sector, Japan’s advanced clinical chemistry automation, and South Korea’s sophisticated hospital laboratory infrastructure create significant secondary markets whose combined procurement reinforces Asia Pacific’s fastest-growing regional status.

MEA & Latin America Immunoprotein Diagnostic Testing Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital laboratory network, Vision 2030’s healthcare investment programme, and the Ministry of Health’s laboratory standardization that creates structured immunoprotein diagnostic procurement. Brazil leads Latin American revenues at approximately 44.2% through its large hospital laboratory network, the growing private diagnostic sector, and the oncology center’s hematological malignancy monitoring requirements.

UAE’s advanced hospital infrastructure and South Africa’s private laboratory sector create significant MEA secondary markets whose immunoprotein procurement reflects the progressive adoption of advanced immunoassay platforms across both national healthcare systems.

Growth Drivers: Rising chronic disease prevalence and chemiluminescence platform adoption enabling sensitivity and throughput improvements

Rising global prevalence of autoimmune diseases, hematological malignancies, and chronic infectious diseases is the immunoprotein diagnostic testing market’s most commercially certain structural growth driver. The WHO’s estimate that over 80 autoimmune diseases collectively affect 5-8% of the global population creates consistent immunoprotein biomarker testing demand for condition monitoring and treatment response assessment. Multiple myeloma’s growing incidence with aging populations, rheumatoid arthritis’s progressive free light chain monitoring requirement, and the immunodeficiency syndrome’s immunoglobulin supplementation monitoring collectively create test volume that compounds with aging population growth.

Chemiluminescence immunoassay platform adoption’s progressive improvement of immunoprotein test sensitivity, automation compatibility, and turnaround time is simultaneously creating diagnostic capability enhancement whose clinical value sustains platform upgrade investment beyond lifecycle replacement timing.

Restraints: High cost of immunoassay analyser platforms and reimbursement limitations for some immunoprotein tests

Immunoassay analyser platform cost, ranging from USD 50,000-500,000 for high-throughput systems, creates capital procurement barriers for smaller hospitals and diagnostic laboratories whose patient volume does not justify the capital investment in premium immunoprotein testing platforms. Each laboratory whose immunoprotein test volume falls below the economic threshold for dedicated immunoassay system installation creates reference laboratory dependence whose cost and turnaround time characteristics limit comprehensive immunoprotein testing access.

Reimbursement limitations for certain immunoprotein tests in insurance-restricted healthcare systems create procurement barriers in markets where payer coverage determination is the primary driver of test ordering decisions.

Opportunities: Multiplex immunoprotein panel development and POC testing in primary care

Multiplex immunoprotein panel testing enabling simultaneous measurement of multiple immunoproteins from a single patient sample represents the most commercially valuable near-term product development direction. Each multiplex panel that combines immunoglobulin quantification, CRP, free light chain ratio, and complement measurement in a single automated assay creates per-test commercial value substantially exceeding sequential individual test procurement while reducing sample volume and analytical time requirements. Luminex’s and Bio-Plex’s multiplex bead-based immunoassay platforms demonstrate the commercial viability of multiplexed immunoprotein measurement whose clinical utility creates structured laboratory procurement.

Point-of-care immunoprotein testing in primary care and emergency settings represents a growing commercial opportunity whose rapid CRP and procalcitonin result availability at the point of clinical decision-making creates antibiotic stewardship and infection management value that central laboratory alternatives cannot provide at equivalent clinical decision speed.

Recent Developments:

-

2026: bioMérieux expanded VIDAS immunoprotein testing portfolio, improving point-of-care and emergency infection biomarker detection capabilities across global healthcare networks.

-

2026: Thermo Fisher Scientific enhanced Binding Site immunoprotein assays integration, expanding free light chain testing adoption in hematology laboratories worldwide.

-

2025: Abbott expanded high-sensitivity immunoprotein assay menu on ARCHITECT and Alinity platforms, improving cardiovascular and inflammatory disease testing efficiency globally.

Immunoprotein Diagnostic Testing Market key players are:

-

Beckman Coulter Inc. (Danaher)

-

Thermo Fisher Scientific Inc.

-

bioMérieux SA

-

Bio-Rad Laboratories Inc.

-

Qiagen N.V.

-

Ortho Clinical Diagnostics (QuidelOrtho)

-

Sysmex Corporation

-

Luminex Corporation (DiaSorin)

-

QuidelOrtho

-

Instrumentation Laboratory (Werfen)

-

Trinity Biotech plc

-

Randox Laboratories Ltd.

-

Binding Site Group (Thermo Fisher)

-

Sebia SA

-

Helena Laboratories

-

R&D Systems (Bio-Techne)

-

Merck KGaA (MilliporeSigma)

Immunoprotein Diagnostic Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.28 Billion |

| Market Size by 2035 | USD 21.28 Billion |

| CAGR | CAGR of 7.54% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Immunoglobulin Diagnostic Tests, C-Reactive Protein Diagnostic Tests, Free Light Chain Diagnostic Tests, Complement System Protein Tests, Pre-Albumin Tests, Haptoglobin Tests, Others) • By Technology (ELISA, Chemiluminescence Immunoassay/CLIA, Radioimmunoassay/RIA, Immunoturbidity Assay, Immunoprotein Electrophoresis, Others) • By Application (Infectious Disease Testing, Autoimmune Disease Testing, Oncology Testing, Allergy Testing, Endocrine Testing, Cardiovascular Testing, Others) • By End User (Hospitals & Clinical Laboratories, Diagnostic Centres, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Beckman Coulter Inc. (Danaher), Abbott Diagnostics, Siemens Healthineers AG, F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific Inc., bioMérieux SA, Bio-Rad Laboratories Inc., Qiagen N.V., Ortho Clinical Diagnostics (QuidelOrtho), Sysmex Corporation, Luminex Corporation (DiaSorin), QuidelOrtho, Instrumentation Laboratory (Werfen), Trinity Biotech plc, Randox Laboratories Ltd., Binding Site Group (Thermo Fisher), Sebia SA, Helena Laboratories, R&D Systems (Bio-Techne), Merck KGaA (MilliporeSigma) |

Frequently Asked Questions

The market is expected to grow at a CAGR of 7.54% from 2026 to 2035.

The market was valued at USD 10.28 Billion in 2025.

Rising incidence of chronic diseases, autoimmune disorders, and hematological malignancies requiring consistent immunoprotein biomarker monitoring.

Immunoglobulin Diagnostic Tests dominated the market with 28.15% share in 2025.

North America dominated the market in 2025.

Get in Touch