Insoluble Sulfur Market Report Scope & Overview:

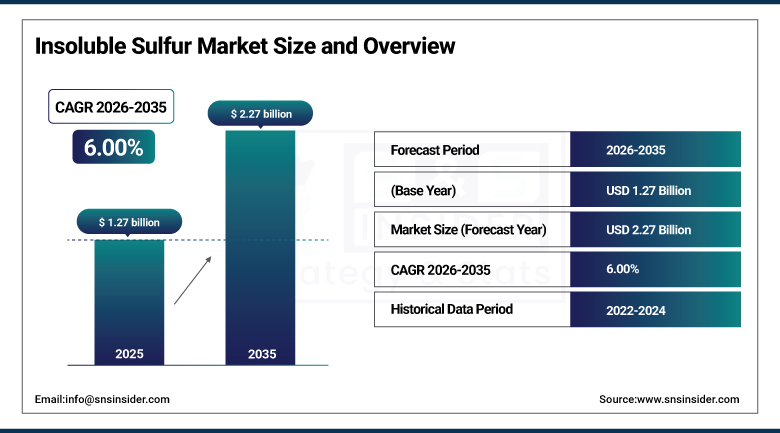

The Insoluble Sulfur Market was valued at USD 1.27 Billion in 2025 and is expected to reach USD 2.27 Billion by 2035, growing at a CAGR of 6.00% from 2026–2035.

The global insoluble sulfur market is growing at a steady and commercially significant pace. Insoluble sulfur (IS) is a polymeric allotrope of sulfur produced by rapid quenching of molten sulfur, used as a rubber vulcanization agent that provides superior bloom resistance, improved adhesion between rubber and steel cord in tire belts, and better processing safety compared to soluble sulfur alternatives. The market is evolving rapidly driven by increasing demand in tire manufacturing and industrial rubber applications, with producers optimising formulations to enhance dispersion, reduce waste, and improve processing efficiency. Demand from replacement tire markets further supports long-term revenue stability.

In 2024, Sennics Co. Ltd., the leading insoluble sulfur producer, announced capacity expansion at its Chinese manufacturing facilities to meet growing demand from the EV tire segment whose high-performance low-rolling-resistance tire formulation requires above-standard insoluble sulfur specification for belt adhesion and durability performance. The expansion reflects the commercial recognition that EV tire’s above-conventional performance demands create above-commodity insoluble sulfur specification whose technical qualification creates commercial differentiation that sustains premium pricing.

Market Size and Forecast:

-

Market Size in 2026E: USD 1.35 Billion

-

Market Size by 2035: USD 2.27 Billion

-

CAGR: 6.00% from 2026 to 2035

-

Fastest Growing Region: Europe (6.5% CAGR)

-

Largest Region: Asia Pacific (42.8%)

To Get more information on Insoluble Sulfur Market - Request Free Sample Report

Insoluble Sulfur Market Trends:

-

Growing electric vehicle production is increasing demand for insoluble sulfur as tire manufacturers require enhanced durability, thermal stability, and steel cord adhesion for EV tires

-

Adoption of high-dispersion grade insoluble sulfur is rising in premium tire manufacturing to improve vulcanization consistency, product quality, and performance

-

Expansion of the global replacement tire market is creating stable and recurring demand for insoluble sulfur across automotive tire production

-

Sustainable sulfur recovery and circular economy initiatives are supporting environmentally responsible insoluble sulfur production using recovered sulfur feedstocks

-

Increasing use of insoluble sulfur in industrial rubber products such as conveyor belts and hoses is expanding demand beyond traditional tire manufacturing applications

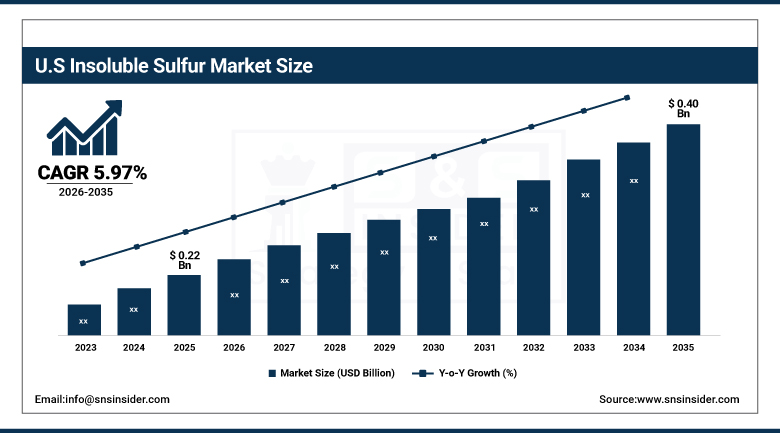

U.S. Insoluble Sulfur Market Outlook:

The U.S. Insoluble Sulfur Market was valued at approximately USD 0.22 Billion in 2025 and is expected to reach approximately USD 0.40 Billion by 2035, growing at a CAGR of approximately 5.97%.

The U.S. is the most commercially significant insoluble sulfur market within North America. Eastman Chemical Company’s Crystex insoluble sulfur brand and imported supply from Asian producers collectively serve the domestic tire manufacturing and industrial rubber markets. The U.S. tire manufacturing sector, encompassing Michelin, Goodyear, Bridgestone, and Cooper Tire’s domestic plants, creates consistent insoluble sulfur procurement whose OEM and replacement tire production volume sustains commercial demand. The growing EV manufacturing sector’s premium tire specification creates above-average per-tonne value commercial procurement that sustains U.S. market growth.

Eastman Chemical Company upgraded its Crystex HD insoluble sulfur production process in 2024 with enhanced oil-extension technology that improves dust suppression and handling safety for tire compound mixing operations, addressing the tire manufacturer’s occupational health and processing efficiency requirements without compromising the high dispersion performance that premium tire formulations require.

Insoluble Sulfur Market Segment Analysis:

-

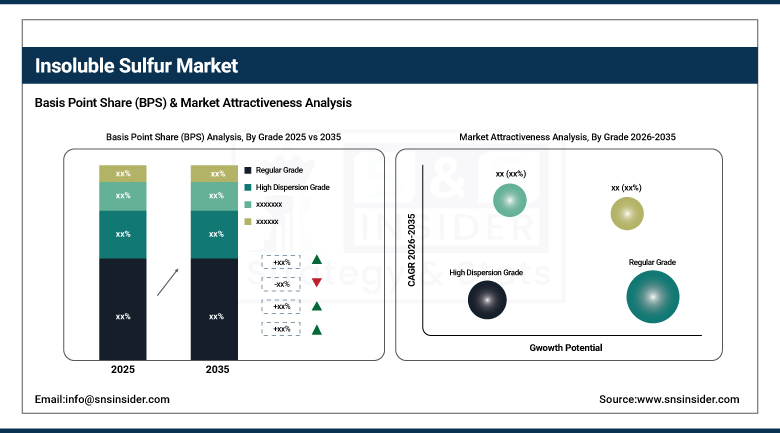

By Grade, the Regular Grade segment dominated the Insoluble Sulfur Market with 50.3% share in 2025, , while the High Dispersion Grade (HD Grade) segment is the fastest growing.

-

By Application, the Tire Manufacturing segment dominated the Insoluble Sulfur Market with approximately 65% share in 2025, while the Industrial Rubber Products segment is the fastest growing.

-

By End Use, the Automotive OEM Tire Manufacturing segment dominated the Insoluble Sulfur Market with approximately 55% share in 2025, while the Replacement Tire Market segment is the fastest growing.

By Grade, regular grade dominates, HD grade grows fastest

Regular grade insoluble sulfur retained the dominant grade position with 50.3% of the insoluble sulfur market in 2025. Regular grade’s commercial primacy reflects its position as the cost-effective standard specification for the majority of commercial tire and industrial rubber formulations whose vulcanisation performance requirements are adequately served by standard dispersion and stability characteristics. Each standard passenger car and commercial vehicle tire that specifies regular grade insoluble sulfur for steel cord belt adhesion creates procurement whose aggregate across the global tire industry’s annual production creates the most commercially significant insoluble sulfur procurement category. The regular grade’s compatibility with standard rubber mixing equipment whose batch mixer and open mill processing does not require the specialised dispersion infrastructure that high-dispersion grades benefit from creates specification accessibility across tire producers without premium processing investment.

High dispersion grade insoluble sulfur is the fastest-growing grade because EV tire’s performance demands and premium passenger tire’s uniformity specification create structured procurement growth that compounds with EV adoption’s extraordinary pace. Each premium tire production run whose specification requires consistent micro-dispersion and above-standard steel cord adhesion creates HD grade procurement whose per-tonne commercial value substantially exceeds regular grade alternatives. EV tire’s above-conventional loading requirements, whose battery weight creates elevated stress on tire belt adhesion, creates structural technical motivation for HD grade specification that sustains the premium tier’s above-market growth rate.

By Application, tire manufacturing dominates, industrial rubber grows fastest

Tire manufacturing retained the dominant application position with approximately 65% of the insoluble sulfur market in 2025. The global tire industry’s annual production exceeding 3 billion tires creates aggregate insoluble sulfur consumption whose scale at even moderate application rates per tyre creates the most commercially significant procurement volume. Each tire’s steel belt cord adhesion requirement, whose insoluble sulfur’s superior bond strength performance creates specification preference over soluble sulfur alternatives in the critical structural component, creates per-tire procurement whose aggregate across billions of annual tires creates commercial scale. The tire industry’s quality and consistency requirements create long-term supply relationships with qualified insoluble sulfur producers whose product performance validation sustains commercial stability.

Industrial rubber products is the fastest-growing application because the global industrial infrastructure’s expansion creates growing demand for high-performance rubber goods whose service life and temperature resistance requirements benefit from insoluble sulfur’s superior vulcanisation characteristics. Mining industry’s conveyor belt demand, oil and gas industry’s hose and seal requirements, and construction’s rubber bearing application collectively create non-tire insoluble sulfur procurement that compounds with industrial development investment. Each industrial rubber product that specifies insoluble sulfur for its enhanced heat resistance and bond strength creates procurement whose quality motivation sustains commercial differentiation from soluble sulfur alternatives.

By End Use, OEM dominates, replacement grows fastest

Automotive OEM tire manufacturing retained the dominant end-use position with approximately 55% of the insoluble sulfur market in 2025. OEM tire production’s specification as original equipment on new vehicles creates quality-sensitive procurement whose per-tyre performance standard sustains premium insoluble sulfur specification. Each new vehicle production programme’s OEM tire qualification creates long-term supply relationships between tire manufacturers and insoluble sulfur producers whose specification stability creates commercial certainty that replacement market’s more variable procurement cannot match equivalently. The global new vehicle production of approximately 90 million vehicles annually creates OEM tire procurement whose scale compounds with vehicle electrification’s above-standard performance specification.

The replacement tire market is the fastest-growing end use because global vehicle parc expansion, increasing annual mileage from economic development, and the growing awareness of tire safety and fuel efficiency creates above-average replacement tire demand whose volume growth is less correlated with economic cycle variation than OEM production. Each vehicle that remains in service beyond its first tire replacement cycle creates second and third replacement procurement that compounds with the global fleet’s growth. The replacement market’s geographic diversification across emerging markets whose vehicle ownership growth creates new replacement demand that sustained OEM market growth cannot replicate equivalently.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

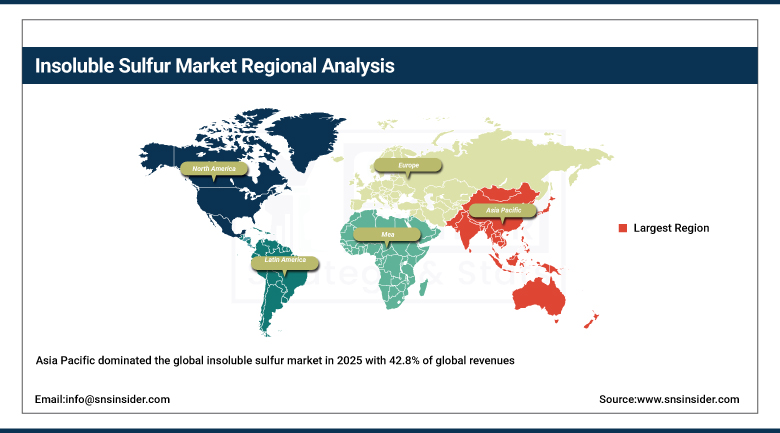

Asia Pacific Insoluble Sulfur Market Insights

Asia Pacific dominated the global insoluble sulfur market in 2025 with 42.8% of global revenues. China accounts for approximately 54.6% of Asia Pacific revenues through Sennics Co.’s market leadership, the world’s largest tire manufacturing concentration, and the extraordinary vehicle production volume creating OEM tire procurement. Asia Pacific’s dominance reflects the concentration of the world’s most commercially active tire manufacturing in China, South Korea, Japan, and India whose combined procurement creates regional commercial scale.

South Korea’s Kumho and Hankook, Japan’s Bridgestone and Yokohama, and India’s rapidly growing tire manufacturing sector create significant secondary markets whose combined procurement sustains Asia Pacific’s dominant regional position.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Insoluble Sulfur Market Insights

Europe is the fastest-growing regional insoluble sulfur market with a CAGR of 6.5%, driven by premium tire demand, EV tire specification advancement, and the automotive industry’s above-average tire performance standard. Germany accounts for approximately 22.3% of European revenues through Continental, Pirelli, and Michelin’s European manufacturing operations, LANXESS’s domestic chemical presence, and the automotive OEM’s premium tire specification.

France, Italy, and Sweden are significant secondary markets where Michelin’s French operations, Pirelli’s Italian manufacturing, and Nokian Tires’ performance specification create consistent premium insoluble sulfur procurement whose above-commodity specification sustains above-average commercial growth.

North America Insoluble Sulfur Market Insights

North America is a commercially significant insoluble sulfur market anchored by Eastman Chemical’s Crystex production, the U.S. tire manufacturing sector’s procurement, and the industrial rubber industry’s demand. The United States accounts for approximately 87.4% of North American revenues through Michelin North America’s South Carolina plant, Goodyear’s domestic manufacturing, and Cooper Tire’s production whose combined OEM and replacement tire procurement sustains consistent demand.

Canada and Mexico contribute approximately 12.6% of North American revenues through the growing automotive manufacturing sector’s tire procurement and the industrial rubber industry’s application demand.

MEA & Latin America Insoluble Sulfur Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its rubber products industry, petrochemical complex’s sulfur supply infrastructure, and the growing automotive sector’s tire procurement. Brazil leads Latin American revenues at approximately 44.2% through its tire manufacturing sector, the automotive industry’s domestic production, and the growing vehicle replacement tire market.

Market Dynamics:

Growth Drivers: Rising global tire production and EV tire premium specification driving above-market demand

Rising global tire production driven by vehicle parc expansion, growing freight transport, and above-average vehicle utilisation is the insoluble sulfur market’s most commercially certain growth driver. The global vehicle fleet’s progressive expansion toward 2 billion vehicles creates proportional tire production demand whose insoluble sulfur component compounds with fleet growth. Electric vehicle adoption’s above-average tire wear rate from battery weight and instant torque creates EV-specific replacement demand that sustains tire volume above conventional ICE vehicle equivalents. Each EV that replaces a conventional vehicle creates a tire procurement that compounds with the EV market’s extraordinary adoption pace.

EV tire’s premium performance specification creates a structurally important insoluble sulfur demand quality shift whose per-tonne commercial value increase from regular to HD grade compounds with EV adoption’s volume growth. Each major tire manufacturer that develops EV-specific premium tire ranges creates HD grade insoluble sulfur specification whose qualification creates long-term supply relationships that sustain above-commodity commercial positioning for technically qualified producers.

Restraints: Sulfur price volatility and competition from alternative vulcanisation systems

Elemental sulfur feedstock price volatility, driven by oil refinery desulfurisation volume and natural gas sweetening activity whose production economics create irregular supply, creates insoluble sulfur production cost uncertainty that limits manufacturer pricing predictability. Each oil price cycle that modifies refinery throughput creates sulfur supply variation whose impact on insoluble sulfur production cost creates commercial uncertainty for budget-sensitive procurement programmes.

Alternative rubber vulcanisation systems using peroxides and metal oxides create competitive pressure in speciality applications whose heat resistance or specific elastomer requirements create alternatives to sulfur-based systems. Each application where non-sulfur vulcanisation achieves superior performance creates market limitation that moderates insoluble sulfur’s addressable application range.

Opportunities: High dispersion grade EV tire specification and emerging market tire industry expansion

HD grade insoluble sulfur specification in the EV tire market represents the most commercially premium growth opportunity whose technical differentiation sustains pricing above commodity regular grade alternatives. Each EV OEM that specifies premium tire performance creates HD grade procurement chain that cascades to tire manufacturer purchasing whose volumes compound with EV production scale-up.

Emerging market tire industry expansion in India, Southeast Asia, and Africa creates first-time insoluble sulfur procurement from new manufacturing facilities whose capacity compounds with domestic vehicle production growth. Each new tire manufacturing plant commissioned in an emerging market creates long-term insoluble sulfur supply relationships whose qualification investment sustains commercial scale.

Recent Developments:

-

2024: Sennics Co. Ltd. announced capacity expansion at its Chinese manufacturing facilities in 2024 to meet growing demand from the EV tire segment whose high-performance low-rolling-resistance formulation requires above-standard HD grade insoluble sulfur specification for belt adhesion and durability.

-

2024: Eastman Chemical Company upgraded its Crystex HD insoluble sulfur production process in 2024 with enhanced oil-extension technology that improves dust suppression and handling safety for tire compound mixing operations without compromising high dispersion performance.

-

2024: LANXESS AG expanded its insoluble sulfur product range in 2024 with new Rhenogran IS-60/20 masterbatch formulations for European premium tire manufacturers, improving processing safety and dispersion consistency in high-speed tire compound mixing lines.

Insoluble Sulfur Market Key Players:

-

Sennics Co., Ltd.

-

Eastman Chemical Company (Crystex)

-

LANXESS AG (Rhenogran)

-

Oriental Carbon & Chemicals Limited (OCCL)

-

Shikoku Chemicals Corporation

-

Henan Kailun Chemical Co., Ltd.

-

Luoyang Sunrise Industrial Co., Ltd.

-

Lions Industries s.r.o.

-

Nynas AB

-

GSPC Distribution Networks Limited

-

Kawaguchi Chemical Industry Co., Ltd.

-

Zhejiang Sunsong Chemical Co., Ltd.

-

Sinochem Hebei Co., Ltd.

-

Enaspol a.s.

-

Grupa Azoty S.A.

-

Evonik Industries AG

-

Thai Rubber & Latex Corporation

-

Jinpang Chemical Group

-

Arkema S.A.

-

China National Chemical Corporation (ChemChina)

Insoluble Sulfur Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.27 Billion |

| Market Size by 2035 | USD 2.27 Billion |

| CAGR | CAGR of 6.00% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Grade (Regular Grade, High Dispersion Grade/HD Grade, High Stability Grade/HS Grade, Others) • by Application (Tire Manufacturing, Industrial Rubber Products, Footwear, Conveyor Belts & Hoses, Others) • by End Use (Automotive OEM Tire Manufacturing, Replacement Tire Market, Industrial & Non-Tire Rubber, Footwear Industry) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Sennics Co., Ltd., Eastman Chemical Company (Crystex), LANXESS AG (Rhenogran), Oriental Carbon & Chemicals Limited (OCCL), Shikoku Chemicals Corporation, Henan Kailun Chemical Co., Ltd., Luoyang Sunrise Industrial Co., Ltd., Lions Industries s.r.o., Nynas AB, GSPC Distribution Networks Limited, Kawaguchi Chemical Industry Co., Ltd., Zhejiang Sunsong Chemical Co., Ltd., Sinochem Hebei Co., Ltd., Enaspol a.s., Grupa Azoty S.A., Evonik Industries AG, Thai Rubber & Latex Corporation, Jinpang Chemical Group, Arkema S.A., China National Chemical Corporation (ChemChina) |

Frequently Asked Questions

The Insoluble Sulfur Market is expected to grow at a CAGR of 6.00% from 2026 to 2035.

The Insoluble Sulfur Market was valued at USD 1.27 Billion in 2025.

Rising global tire production from vehicle parc expansion and replacement tire demand, and increasing specification of HD grade insoluble sulfur in EV and high-performance tire formulations requiring enhanced steel cord adhesion, thermal resistance, and dispersion consistency.

Regular Grade dominated the Insoluble Sulfur Market with 50.3% share in 2025 as confirmed by SNS Insider, while High Dispersion Grade is the fastest growing.

Asia Pacific dominated the Insoluble Sulfur Market in 2025 with 42.8% of global revenues, while Europe is the fastest-growing region with a CAGR of 6.5%.

Get in Touch