Intravenous Iron Drugs Market Report Scope & Overview:

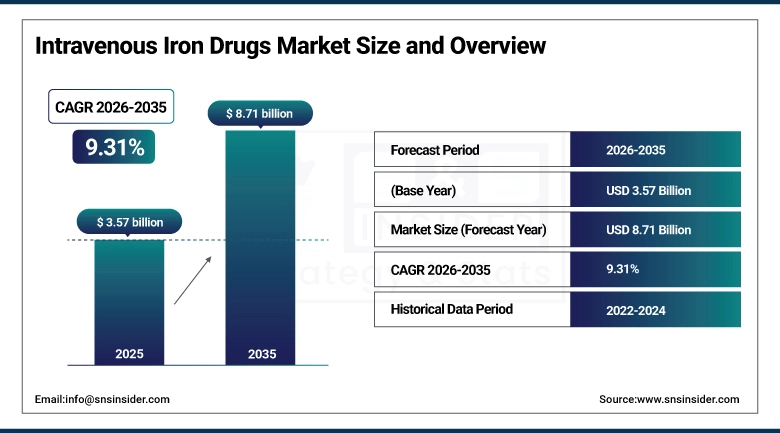

The Intravenous Iron Drugs Market size was valued at USD 3.57 billion in 2025 and is expected to reach USD 8.71 billion by 2035, at a CAGR of 9.31% during the forecast period 2026–2035.

The global intravenous iron drugs market is witnessing robust growth, with the clinical bias for parenteral iron therapy increasingly replacing oral iron supplementation in iron deficiency anemia (IDA) complicated by intolerance, malabsorption, or underlying chronic inflammatory states. The rising global incidence of chronic kidney disease (CKD), inflammatory bowel disease (IBD), and cancer-associated anemia are key drivers in the IV iron formulations market, which include iron sucrose, ferric carboxymaltose, ferric derisomaltose, and iron dextran, among others. According to the World Health Organization (WHO) facts sheet, approximately 1.62 billion people worldwide are affected by anemia, with IDA responsible for almost 50% of the global anemia burden, which directly translates into the expanding market for intravenous iron drugs manufacturers. IV iron therapy protocols are increasingly preferred over erythropoiesis-stimulating agents (ESAs) due to enhanced efficacy, tolerability, and pharmacoeconomic benefits, which are expected to sustain the market growth over the long term.

For instance, in February 2024, clinical data published in the New England Journal of Medicine confirmed that ferric carboxymaltose administered intravenously reduced hospitalization risk by 26% in patients with heart failure and iron deficiency, accelerating its adoption across cardiology and nephrology departments globally.

Intravenous Iron Drugs Market Size and Forecast:

-

Market Size in 2025: USD 3.57 billion

-

Market Size by 2035: USD 8.71 billion

-

CAGR: 9.31% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Intravenous Iron Drugs Market - Request Free Sample Report

Intravenous Iron Drugs Market Trends

-

Accelerating clinical adoption of ferric carboxymaltose and ferric derisomaltose due to their high-dose, single-infusion convenience, reducing hospital chair time and improving patient compliance across nephrology, oncology, and gastroenterology settings.

-

Growing body of evidence supporting IV iron use in heart failure patients with IDA, with landmark trials such as AFFIRM-AHF and IRONMAN driving guideline updates by the European Society of Cardiology (ESC) and American Heart Association (AHA).

-

Increased use of IV iron in perioperative anemia management (Patient Blood Management programs) to reduce allogeneic blood transfusions, with adoption growing at an estimated 14.2% annually in surgical centers across North America and Europe.

-

Expansion of biosimilar and generic IV iron formulations reducing treatment costs, with biosimilar iron sucrose capturing over 31% of the iron sucrose segment volume in 2024 across regulated markets.

-

Rising integration of IV iron therapy into outpatient infusion centers and ambulatory care settings, enabled by newer low-reactogenicity formulations that minimize serious adverse event risks.

-

Pharmaceutical manufacturers investing in next-generation IV iron complexes with improved stability, higher elemental iron content per dose, and reduced anaphylaxis risk to meet evolving prescriber and payer demands.

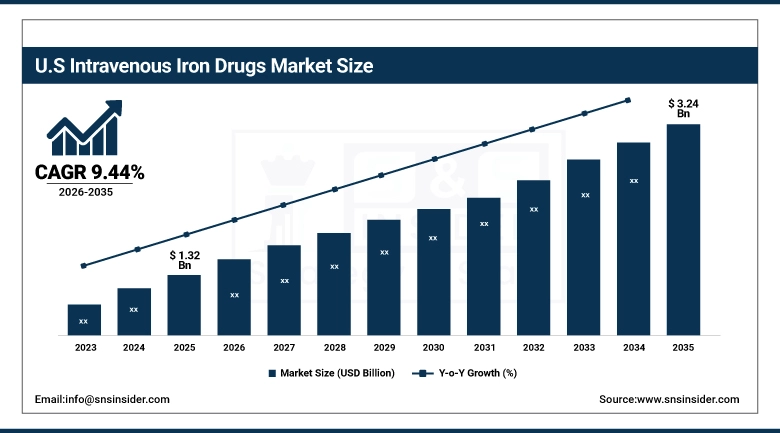

The U.S. Intravenous Iron Drugs Market is estimated at USD 1.32 billion in 2025 and is expected to reach USD 3.24 billion by 2035, growing at a CAGR of 9.44% from 2026–2035. The United States market represents the single largest country market for intravenous iron drugs, driven by a large patient burden of CKD patients, well-developed outpatient infusion services, comprehensive reimbursement coverage through Medicare Part B, and a well-developed pipeline of both branded and biosimilar IV iron products. The presence of market leaders such as American Regent, AMAG Pharmaceuticals, and Rockwell Medical, along with the growing market opportunity in cancer-related anemia and perioperative uses, continues to ensure the United States market leads the broader North American market.

Intravenous Iron Drugs Market Growth Drivers:

-

Rising Global Prevalence of Iron Deficiency Anemia and Chronic Disease Burden is Driving the Intravenous Iron Drugs Market Growth

The increasing global burden of iron deficiency anemia, chronic kidney disease, inflammatory bowel disease, and cancer is the strongest structural driver for the intravenous iron drug market. The Global Burden of Disease Study has estimated the global prevalence of iron deficiency anemia to be over 1.16 billion individuals. Among the 37.8% of the chronic kidney disease patient pool undergoing dialysis, IV iron formulations are a standard part of the care protocol. With the chronic kidney disease dialysis pool expected to rise to over 5.4 million by 2030 and the incidence of cancer growing steadily with 20 million new cases recorded in 2022 according to WHO statistics, the structural need for effective IV iron formulations is embedded in the healthcare delivery system worldwide. This growing pool of affected individuals structurally expands the addressable market for IV iron drug manufacturers across both branded and biosimilar IV iron drug manufacturers.

For instance, in July 2024, the U.S. Renal Data System (USRDS) reported that intravenous iron drug utilization among hemodialysis patients in the United States increased by 18.6% between 2021 and 2023, reflecting growing standard-of-care adoption and improving reimbursement pathways for IV iron therapy in end-stage renal disease management.

Intravenous Iron Drugs Market Restraints:

-

Risk of Hypersensitivity Reactions and Stringent Administration Requirements are Hampering the Intravenous Iron Drugs Market Growth

In spite of this significant clinical need, there is a significant restraint for the intravenous iron drugs market, which is represented by the risk of hypersensitivity and anaphylactic reactions, especially when using older-generation iron dextran formulations. This requires a controlled environment for infusion, increased time for observation of patients, and provision of emergency equipment for resuscitation, all of which increase the cost of delivery of intravenous iron therapy. The FDA, among other agencies, has also mandated risk evaluation and mitigation strategies for intravenous iron dextran, which limits their use to healthcare facilities that can provide management of anaphylaxis. This, in cost-sensitive healthcare systems or in low- to middle-income countries, becomes a significant restraint for the intravenous iron drugs market, especially for outpatient or primary care settings, where intravenous iron therapy can generate significant volume growth.

Intravenous Iron Drugs Market Opportunities:

-

Label Expansions into Heart Failure and Perioperative Anemia Applications Create Significant Future Growth Opportunities for the Intravenous Iron Drugs Market

The emerging clinical data for IV iron use in heart failure patients suffering from iron deficiency, irrespective of their anemia status, is probably one of the single-most significant growth opportunities for the IV iron drugs market. The ESC Heart Failure Guidelines 2021 and subsequent revisions now recommend IV iron therapy for symptomatic heart failure patients suffering from iron deficiency, which opens up a new patient universe of 50% of the total of about 64 million heart failure patients worldwide. At the same time, Patient Blood Management Programs requiring preoperative anemia correction are also increasing IV iron usage in the elective surgery setting, estimated at about 230 million major surgeries annually worldwide. These expanding usage opportunities for IV iron are also creating new revenue streams for IV iron manufacturers beyond their traditional use in CKD and IBD, expanding the commercialization opportunity for approved IV iron drugs and pipeline candidates beyond their traditional use.

For instance, in October 2024, CSL Vifor received expanded regulatory approvals in the European Union for Ferinject (ferric carboxymaltose) covering iron deficiency in chronic heart failure patients, immediately unlocking an estimated incremental addressable patient population of 11.2 million across the EU, representing a substantial upside to the existing market size projections.

Intravenous Iron Drugs Market Segment Analysis

-

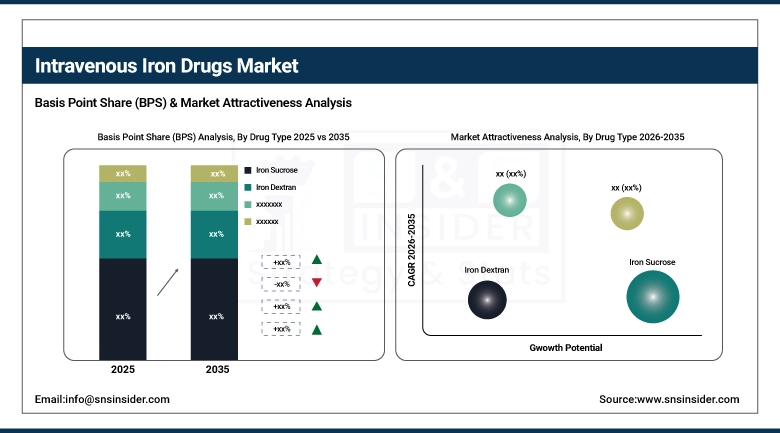

By drug type, iron sucrose held the largest share of approximately 38.42% in 2025, while the ferric carboxymaltose segment is expected to register the highest growth with a CAGR of 11.24% during the forecast period.

-

By application, chronic kidney disease accounted for the dominant share of around 44.86% in 2025, while the cancer segment is expected to register the highest growth with a CAGR of 10.45%.

-

By distribution channel, hospital pharmacies led the market with approximately 64.32% share in 2025, while online pharmacies are expected to register the highest growth with a CAGR of 12.18%.

By Drug Type, Iron Sucrose Leads the Market, While Ferric Carboxymaltose Registers Fastest Growth

The iron sucrose component was also found to hold the highest revenue share of about 38.42% in 2025, owing to its established safety and efficacy record of more than two decades, extensive use of generics, and inclusion of iron sucrose in national essential medicine lists of several countries. Iron sucrose is also the first choice of IV iron formulation in many dialysis units worldwide, especially in North America, Europe, and Asia Pacific, because of its established status of reimbursement and cost-effectiveness. On the other hand, the ferric carboxymaltose component is expected to register the highest CAGR of 11.24% during the period of 2026-2035, because of its unique advantage of delivering up to 1,000 mg of elemental iron in a single infusion of 15 minutes, thus reducing the number of infusion visits. The expanding base of approved indications for ferric carboxymaltose, including CKD, IBD, postpartum IDA, and now heart failure, coupled with ongoing investments in label expansion by CSL Vifor and AMAG Pharmaceuticals, ensures ferric carboxymaltose becomes the major revenue growth driver of the IV iron drugs market.

By Application, Chronic Kidney Disease Dominates, While Cancer Registers Fastest Growth

The chronic kidney disease segment held the largest share of the application segment market at around 44.86% in 2025, indicating the deeply entrenched use of IV iron therapy for the management of anemia in the setting of CKD, especially for dialysis-dependent individuals where the absorption of iron from the gastrointestinal tract is severely impaired by systemic inflammation and uremic toxins. In fact, the Kidney Disease Improving Global Outcomes (KDIGO) guidelines have specifically recommended IV iron therapy as the preferred option for the management of anemia in dialysis-dependent individuals. In contrast, the application segment for the treatment of cancer is likely to grow at the fastest CAGR of 10.45% from 2025 to 2035, driven by the increasing recognition of the impact of anemia on the toxicity and survival outcomes of chemotherapy regimens and the use of IV iron therapy for the management of anemia in the setting of cancer as an independent predictor of chemotherapy toxicity and survival outcomes.

By Distribution Channel, Hospital Pharmacies Lead, and Online Pharmacies Register Fastest Growth

Similarly, hospital pharmacies retained the highest distribution share of about 64.32% in the year 2025, as IV iron infusion is intrinsically a clinical procedure that requires the presence of trained nursing personnel, infusion equipment, and the capacity to manage anaphylaxis, which are only possible in the hospital and infusion clinic settings. The complex nature of IV iron drug preparation, storage, and administration makes the hospital pharmacy the most important and suitable route of distribution for IV iron infusion drugs. The online pharmacies segment, however, is likely to exhibit the highest growth rate of 12.18% during the forecast period, given the rise of specialty pharmacy platforms, the increasing trend of home infusion, and the growing role of online procurement in the healthcare sector, particularly in the case of infusion centers and ambulatory care facilities that procure IV iron via specialty pharmacy channels.

Intravenous Iron Drugs Market Regional Highlights:

North America Intravenous Iron Drugs Market Insights:

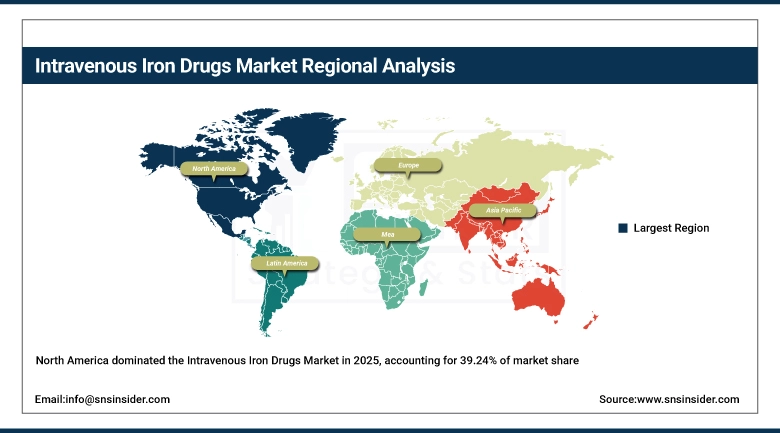

North America dominated the regional revenue share, i.e., more than 39.24%, in the intravenous iron drugs market during 2025. This is due to a large dialysis population, well-developed outpatient infusion services, a favorable Medicare and Medicaid system for IV iron drugs under the ESRD Prospective Payment System, and a favorable regulatory environment for ongoing label expansion. The dialysis market in the United States, treating more than 550,000 patients as of 2024, is a structurally recurring market for IV iron formulations. Furthermore, increasing use of IV iron for perioperative anemia management, postpartum iron deficiency anemia, and heart failure management is expanding the use of IV iron beyond traditional ESA-refractory anemia, creating a differentiated product opportunity for premium-priced branded IV iron formulations and biosimilar alternatives.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Intravenous Iron Drugs Market Insights:

Asia Pacific is the fastest-growing segment in the intravenous iron drug market; the segment is anticipated to grow at a CAGR of 11.47% during the forecast period (2020-2035). The growth drivers for the intravenous iron drug market in the Asia Pacific are the exceptionally high prevalence rate of iron deficiency anemia among women of reproductive age groups and dialysis patients in China, India, and Southeast Asian countries; high growth rate in healthcare infrastructure development; high rate of growth in healthcare expenditure; and government initiatives for the elimination of iron deficiency anemia among the population in these countries. Initiatives taken under the National Health Mission (NHM) for nutritional anemia among pregnant women and children in India are now being implemented with intravenous iron therapy for severe iron deficiency anemia patients; a high growth rate in the number of dialysis centers in China, with a forecasted figure of over 8,500 dialysis centers in the country during 2026; and the growing number of generic intravenous iron drug manufacturers in the Asia Pacific supply chain, such as Sun Pharmaceutical Industries Ltd., Aurobindo Pharma Ltd., and Cipla Ltd.

Europe Intravenous Iron Drugs Market Insights:

Europe is the second-largest regional market for intravenous iron drugs, with a well-established hematology and nephrology care framework, high adherence to guidelines issued by the ESC and ERA-EDTA that recommend IV iron for CKD and heart failure patients, and a growing rate of Patient Blood Management program adoption in the UK, Germany, France, and Nordic countries. The European market has been a key hub for clinical trials for next-generation IV iron products; for instance, Pharmacosmos A/S has initiated multiple pivotal clinical trials for ferric derisomaltose (Monofer) in the European market. Strong regulatory alignment among EU member states and positive NICE and HAS assessments for IV iron products for the treatment of cardiology and gastroenterology indications have helped sustain a high rate of revenue growth in Western European markets.

Latin America (LATAM) and Middle East & Africa (MEA) Intravenous Iron Drugs Market Insights:

In Latin America and the Middle East & Africa, the intravenous iron drugs market is growing out of a relatively nascent phase, driven by increasing investments in healthcare, the growing burden of CKD and nutritional anemia, and the improving pharmaceutical import and manufacturing ecosystem. The LATAM markets of Brazil and Mexico are the most significant markets, with increasing hospital-based IV iron usage driven by the expanding dialysis network and maternal health initiatives targeting pregnancy-associated IDA. The MEA markets of the Gulf Cooperation Council countries, including the UAE and Saudi Arabia, are investing in high-end kidney and cancer treatment facilities, where IV iron treatment protocols are becoming increasingly standardized, while the sub-Saharan African markets are considered to be long-term opportunities that are subject to the development of the healthcare infrastructure in the region.

Intravenous Iron Drugs Market Competitive Landscape:

CSL Vifor (founded in 1930, located in Switzerland) is a global leader in intravenous iron therapy with the broadest portfolio of approved IV iron products worldwide, including Ferinject (ferric carboxymaltose), Venofer (iron sucrose), and Injectafer. The company utilizes its strong relationships with key stakeholders in nephrology and cardiology, its Phase IV clinical evidence generation program, and its global commercial capabilities to sustain its leadership position in the IV iron category in both branded and reimbursed markets.

-

In October 2024, CSL Vifor received EMA approval for expanded Ferinject labeling covering iron deficiency in symptomatic chronic heart failure patients with reduced ejection fraction, estimated to add over 11 million newly addressable patients across the European Union.

Pharmacosmos A/S (founded 1965, Denmark), the company responsible for the development of the iron compound ferric derisomaltose (also called iron isomaltoside 1000), sold under the trade name Monofer for intravenous use outside the US and under the name Diafer for use in dialysis clinics, is a premium single-dose high-concentration iron solution for intravenous use in hospital and infusion clinics. Pharmacosmos is a dedicated iron company.

-

In March 2024, Pharmacosmos published results from the FERWALK trial demonstrating that a single infusion of ferric derisomaltose significantly improved 6-minute walk distance and quality of life scores in iron-deficient heart failure patients at 12 weeks, strengthening its cardiology indication pipeline.

American Regent, Inc. (est. 1946, U.S.) is a leading U.S.-based manufacturer of intravenous iron products including Venofer (iron sucrose) and INFeD (iron dextran), serving the dialysis, oncology, and hospital pharmacy segments. The company is a primary supplier to dialysis chains, outpatient infusion centers, and hospital systems through its established GPO and wholesaler network.

-

In June 2024, American Regent expanded its IV iron manufacturing capacity at its Shirley, New York facility by 35%, addressing growing domestic demand for iron sucrose across dialysis and non-dialysis CKD applications in the United States.

Intravenous Iron Drugs Market Key Players:

-

CSL Vifor (Vifor Pharma)

-

Pharmacosmos A/S

-

American Regent, Inc. (Luitpold Pharmaceuticals)

-

AMAG Pharmaceuticals (Covis Pharma)

-

Rockwell Medical, Inc.

-

Fresenius Medical Care AG

-

Akebia Therapeutics, Inc.

-

Shield Therapeutics plc

-

Daiichi Sankyo Company, Limited

-

Pfizer Inc.

-

Hikma Pharmaceuticals PLC

-

Sandoz International GmbH (Novartis)

-

Sun Pharmaceutical Industries Ltd.

-

Cipla Ltd.

-

Aurobindo Pharma Ltd.

-

Intas Pharmaceuticals Ltd.

-

Glenmark Pharmaceuticals Ltd.

-

Wockhardt Ltd.

-

Baxter International Inc.

-

Quimica Clinica Aplicada S.A. (QCA)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.57 Billion |

| Market Size by 2035 | USD 8.71 Billion |

| CAGR | CAGR of 9.31% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Type (Iron Dextran, Iron Sucrose, Ferric Carboxymaltose, Other Drug Types) • By Application (Chronic Kidney Disease, Inflammatory Bowel Disease, Cancer, Other Applications) • By Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Pharmacy) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | CSL Vifor (Vifor Pharma), Pharmacosmos A/S, American Regent, Inc. (Luitpold Pharmaceuticals), AMAG Pharmaceuticals (Covis Pharma), Rockwell Medical, Inc., Fresenius Medical Care AG, Akebia Therapeutics, Inc., Shield Therapeutics plc, Daiichi Sankyo Company, Limited, Pfizer Inc., Hikma Pharmaceuticals PLC, Sandoz International GmbH (Novartis), Sun Pharmaceutical Industries Ltd., Cipla Ltd., Aurobindo Pharma Ltd., Intas Pharmaceuticals Ltd., Glenmark Pharmaceuticals Ltd., Wockhardt Ltd., Baxter International Inc., Quimica Clinica Aplicada S.A. (QCA) |

Frequently Asked Questions

Ans: The Intravenous Iron Drugs Market is projected to reach USD 8.71 billion by 2035, growing from USD 3.57 billion in 2025.

Ans: The Intravenous Iron Drugs Market is expected to grow at a CAGR of 9.31% during the forecast period.

Ans: Iron sucrose leads the Intravenous Iron Drugs Market with a 38.42% share in 2025, while ferric carboxymaltose is the fastest-growing segment

Ans: North America dominates the Intravenous Iron Drugs Market with over 39.24% revenue share in 2025.

Ans: The Intravenous Iron Drugs Market is primarily driven by rising cases of iron deficiency anemia (affecting ~1.62 billion people globally) and increasing prevalence of chronic diseases like CKD and cancer.

Get in Touch