Inverter Duty Motor Market Report Scope & Overview:

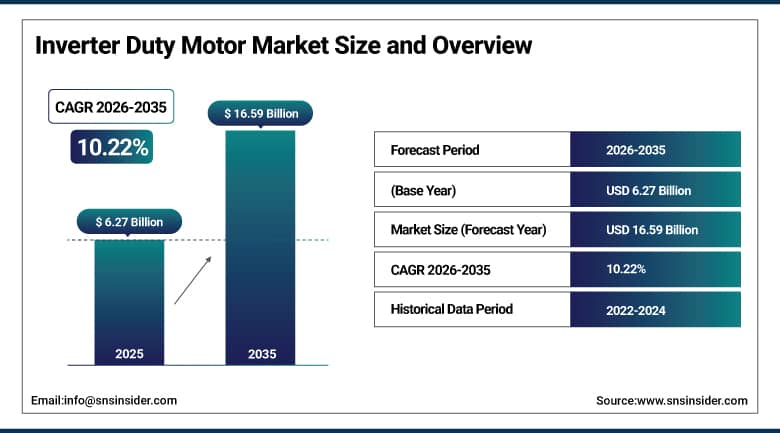

The Inverter Duty Motor Market was valued at USD 6.27 Billion in 2025 and is expected to reach USD 16.59 Billion by 2035, growing at a CAGR of 10.22% from 2026–2035.

The Inverter Duty Motor Market is witnessing rapid growth owing to rising use of variable frequency drives (VFD) in industrial sectors to optimize energy consumption, better process control, and enhance reliability. The trend of industrial automation, along with increasing manufacturing activities and investment in smart factories, is driving the demand for inverter-duty motors in different industries. Moreover, energy efficiency policies and increasing focus on sustainable practices are also prompting industries to shift from traditional motors to efficient inverter-duty motors. The rising use of such motors in water and wastewater treatment plants, HVAC installations, oil & gas production facilities, and material handling operations is fueling their market growth.

According to the International Energy Agency, electric motors account for approximately 45% of global electricity consumption, highlighting the importance of motor efficiency in reducing industrial energy use. The agency also reports that industrial sectors consume around 37% of global final energy demand, reinforcing the need for energy-efficient motor technologies and automation systems that optimize operational performance and support sustainability objectives.

Inverter Duty Motor Market Size and Forecast:

-

Market Size in 2026E: USD 6.91 Billion

-

Market Size by 2035: USD 16.59 Billion

-

CAGR: 10.22% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Inverter Duty Motor Market - Request Free Sample Report

Inverter Duty Motor Market Trends:

-

IE4 and IE5 super-premium efficiency motor mandates are accelerating inverter duty motor specification upgrades across European and North American industrial facilities.

-

Integrated motor-drive package certification is creating optimised inverter duty motor and VFD combinations replacing separately sourced component assemblies.

-

Predictive maintenance integration with smart motor condition monitoring is extending inverter duty motor operational lifespan through early fault detection.

-

Permanent magnet synchronous motor adoption in inverter duty configurations is improving efficiency at partial load duty cycles versus standard induction motor equivalents.

-

Water and wastewater sector’s smart pump control investment is creating growing inverter duty motor demand for variable-flow municipal treatment infrastructure.

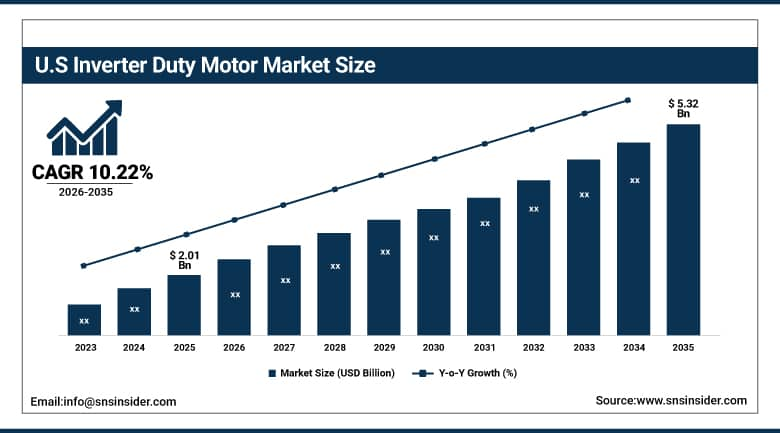

U.S. Inverter Duty Motor Market Outlook:

The U.S. Inverter Duty Motor Market was valued at approximately USD 2.01 Billion in 2025 and is expected to reach approximately USD 5.32 Billion by 2035, growing at a CAGR of approximately 10.22%.

The United States leads North American inverter duty motor revenues through the Department of Energy’s motor energy efficiency standards requiring NEMA Premium efficiency (IE3 equivalent) for industrial motors, the large manufacturing and processing sector’s VFD retrofit programme investment, and the water and wastewater infrastructure’s variable flow pump control adoption. ABB, Nidec, Regal Rexnord, and Rockwell Automation’s Allen-Bradley motor series sustain U.S. market leadership through their comprehensive inverter duty motor portfolios spanning fractional to large frame sizes.

According to the U.S. Department of Energy Motor Systems Program, energy-efficient motor systems can reduce motor energy consumption by 20–30% or more when integrated with variable frequency drive (VFD) technologies.

Inverter Duty Motor Market Segment Analysis:

-

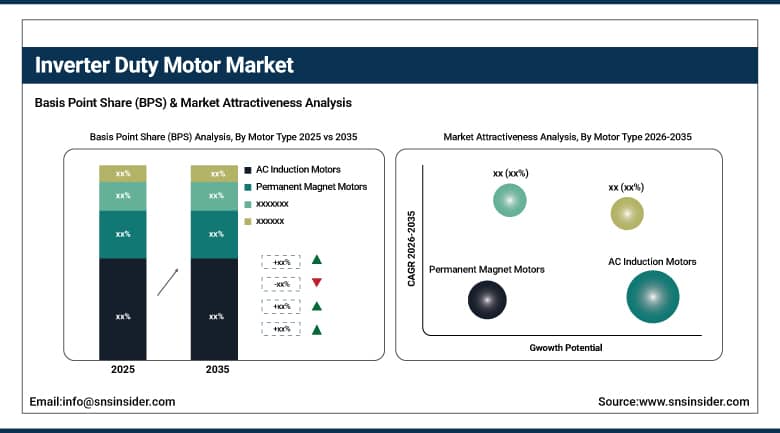

By Motor Type, AC Induction Motors segment dominated the Inverter Duty Motor Market in 2025 with 58% share; Permanent Magnet Motors segment is the fastest growing segment.

-

By Phase, Three Phase segment dominated the market in 2025 with 81% share; Single Phase segment is the fastest growing segment.

-

By Voltage, Low Voltage segment dominated the market in 2025 with 64% share; Medium Voltage segment is the fastest growing segment.

-

By Application, Pumps segment dominated the market in 2025 with 24% share; HVAC Systems segment is the fastest growing segment.

-

By End-User Industry, Manufacturing segment dominated the market in 2025 with 29% share; Water & Wastewater Treatment segment is the fastest growing segment.

By Motor Type, AC induction motors segment dominates the inverter duty motor market, while permanent magnet motors segment is the fastest-growing segment

AC Induction Motors dominated the Inverter Duty Motor Market in 2025 because of their proven reliability, cost-effectiveness, and universal compatibility with variable frequency drives (VFDs). This type of motor has been widely used in manufacturing operations, HVAC installations, pump installations, and material handling, where energy efficiency is essential. They are known for being highly durable and having low maintenance needs and being able to function under tough industrial conditions, hence being favored by industrial users.

Permanent Magnet Motors are the fastest growing segment due to their higher energy efficiency, smaller size, and high power density when compared to other motor types. Due to their ability to provide energy savings, industries have adopted permanent magnet motors to help them save more energy and achieve their sustainability goals. The efficient speed regulation offered by these motors has made them popular among industries, leading to their fast growth.

By Phase, three phase segment dominates the inverter duty motor market, while single phase segment is the fastest-growing segment

The Three Phase segment dominated the market in 2025 due to its ability to deliver high efficiency, produce more power, and perform more effectively compared to a single-phase system. Industrial plants have been using three-phase power infrastructure to effectively run pumps, compressors, conveyors, and other heavy machinery. The use of three-phase inverter duty motors makes them reliable due to better torque features in continuous duty operations. Thus, they have gained a major market share due to their wide use in manufacturing and process industries.

The Single Phase segment is experiencing the fastest growth owing to growing demand in commercial facilities, residential complexes, and small scale industries. Adoption of small automation devices, HVAC, and energy efficient machines requires the use of inverter duty motors for single-phase infrastructure. Moreover, infrastructure upgrades along with growth in small business firms have been contributing to high adoption of single phase motors.

By Voltage, low voltage segment dominates the inverter duty motor market, while medium voltage segment is the fastest-growing segment

Low Voltage motors dominated the Inverter Duty Motor Market in 2025 owing to their widespread utilization in different industries, utilities, and commercial applications. The motors are well-balanced in terms of performance, energy consumption, and cost of installation, which makes them ideal for various purposes such as pumps, fans, compressors, and conveyors. Wide use across industries and easy integration into current electrical installations have helped the segment establish itself at the forefront of the market. Investment in automation and efficient devices has helped consolidate the segment’s position in the market.

Medium Voltage motors represent the fastest growing segment owing to the growing need for motors with higher output capacity in industries. Application areas for such motors include mining, electricity production, oil and gas extraction, water treatment plants, among others. Such motors enable loss reduction and increased process reliability in energy-intensive settings. Industrial expansion and modernization around the world have provided ample opportunities for the segment to develop.

By Application, pumps segment dominates the inverter duty motor market, while hvac systems segment is the fastest-growing segment

The Pumps segment dominated the market in 2025 owing to the fact that pumps happen to be some of the most widely used applications that demand accurate speed control and energy optimization capabilities. Inverter duty motors facilitate efficient adjustment of the system's output in accordance with the demand, thus ensuring energy savings. Various industries depend upon the usage of pumps for the accomplishment of essential tasks. Increasing emphasis on efficient fluid handling solutions is fueling the dominance of the segment.

HVAC Systems are the fastest growing application segment owing to growing demand for energy-efficient climate control solutions in commercial, residential, and industrial spaces. Inverter duty motors enable efficient performance optimization by virtue of their ability to provide adjustable speeds to fans and compressors. Growing urbanization, increasing regulatory pressures for energy efficiency, and rising focus towards smart building projects have fueled growth in HVAC installations across the world.

By End-User Industry, manufacturing segment dominates the inverter duty motor market, while water & wastewater treatment segment is the fastest-growing segment

The Manufacturing segment dominated the Inverter Duty Motor Market in 2025 due to widespread use of automation, assembly lines, conveyor systems, and processing equipment. The manufacturing companies are now resorting to inverter duty motors to increase efficiency, reduce energy costs, and ensure better process control. As the world gradually shifts towards automation and smart manufacturing techniques, the usage of motors with high-levels of process control has been on the rise. Consequently, the manufacturing sector has been able to dominate the market.

Water & Wastewater Treatment is the fastest growing end-user industry due to significant investments being made in water infrastructure by municipalities and utility firms. Inverter Duty Motors have found several applications in water & wastewater treatment equipment, including pumps and aeration systems. The rising focus on sustainable utility management, increasing water scarcity, and stringent environmental regulations have prompted the use of inverter duty motors.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

22.8% |

|

Latin America |

Brazil |

43.8% |

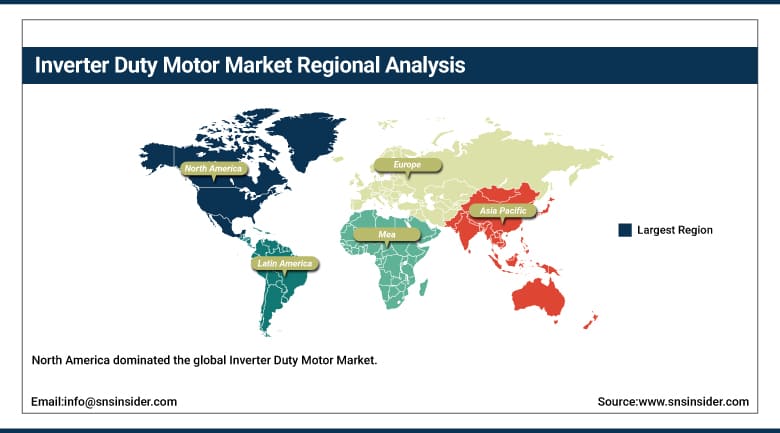

North America Inverter Duty Motor Market Insights

North America dominated the global Inverter Duty Motor Market through its strict DOE motor efficiency standards, the large industrial manufacturing and water treatment sector’s VFD retrofit programme investment, and the commercial building sector’s variable air volume HVAC upgrade adoption. The United States accounts for approximately 82.5% of North American revenues through ABB, Nidec, Regal Rexnord, and Rockwell Automation’s comprehensive inverter duty motor portfolios serving the full industrial application spectrum.

The DOE also states that electric motor-driven systems account for nearly 70% of industrial electricity use in the United States, emphasizing the critical role of high-efficiency motors in reducing operational costs and energy consumption. Furthermore, the U.S. Energy Information Administration identifies manufacturing as one of the largest electricity-consuming sectors, further driving the adoption of inverter-duty motors that enhance energy efficiency, reliability, and productivity across industrial operations.

Canada contributes supplementary North American revenues through its large mining, oil sands, and pulp and paper industrial sectors’ inverter duty motor procurement, the growing municipal water infrastructure’s VFD pump control adoption, and the commercial building sector’s energy efficiency regulation compliance creating HVAC motor upgrade investment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Inverter Duty Motor Market Insights

Europe is a technically advanced inverter duty motor market where the EU’s ErP Directive mandating IE3 minimum efficiency for motors above 0.75kW since 2023 and the progressive implementation of IE4 requirements create structured regulatory demand for premium efficiency inverter duty motors. Germany accounts for approximately 24.6% of European revenues through its large manufacturing sector, Siemens’ industrial motor commercial leadership, and ABB’s European production facilities serving continental European industrial procurement.

According to the European Commission, electric motor systems account for approximately 70% of industrial electricity consumption within the European Union, highlighting the importance of energy-efficient motor technologies in reducing industrial power usage.

Asia Pacific Inverter Duty Motor Market Insights

Asia Pacific is the fastest-growing regional inverter duty motor market, driven by China’s manufacturing sector’s progressive energy efficiency upgrade investment under national energy conservation regulations, India’s BEE Star label energy efficiency standards for motors creating incentive-driven IE3 adoption, and the growing automation investment across Asian manufacturing sectors. China accounts for approximately 44.8% of Asia Pacific revenues through its massive industrial motor installed base and growing domestic inverter duty motor manufacturing.

National Bureau of Statistics of China reports that China remains the world's largest manufacturing economy, generating over 25% of global manufacturing output, which continues to support substantial demand for inverter-duty motors across a wide range of industrial applications.

MEA & Latin America Inverter Duty Motor Market Insights

Saudi Arabia leads MEA revenues at approximately 22.8% through its large petrochemical, desalination, and oil processing sectors’ pump and compressor inverter duty motor procurement, the industrial energy efficiency programme’s motor upgrade investment, and the growing manufacturing sector’s automation investment. UAE’s advanced building automation and infrastructure sectors contribute growing regional demand.

Brazil leads Latin American revenues at approximately 43.8% through its large manufacturing sector’s motor procurement, the energy efficiency programme’s Procel label creating inverter duty motor specification incentives, and the oil and gas sector’s Petrobras pump and compressor installation. Mexico’s large manufacturing export sector creates growing inverter duty motor adoption aligned with North American efficiency standards.

Market Dynamics:

Growth Drivers: Energy efficiency regulations mandating premium motor performance and industrial automation expansion creating structured inverter duty motor adoption

The inverter duty motor market’s growth is driven by the global regulatory environment’s systematic tightening of motor efficiency requirements, where EU ErP Directive’s IE3 minimum mandate, DOE’s NEMA Premium efficiency standard for U.S. commercial and industrial motors, and India’s BEE Star rating system collectively create compliance-driven motor upgrade procurement across the world’s three largest industrial motor markets simultaneously. Each motor replacement event in regulated markets creates an inverter duty motor procurement specification opportunity whose conversion from IE1 standard efficiency to IE3 or IE4 creates measurable energy cost savings that utility incentive programmes frequently co-fund, reducing the capital cost barrier that sustains motor upgrade programme momentum.

Restraints: High upfront premium versus standard motors and complex motor-drive system integration requirements creating adoption barriers in cost-sensitive markets

Inverter duty motors’ price premium of 20 to 40% over equivalent-rated standard induction motors creates capital expenditure approval barriers in cost-sensitive industrial markets whose procurement decisions prioritise acquisition cost over lifecycle energy efficiency economics. Each facility whose capital budget review process applies simple payback analysis without capturing full lifetime energy cost savings creates an adoption decision that may favour the lower-cost standard motor specification despite the inverter duty motor’s superior long-term economics. Commodity chemical and food processing markets whose narrow margins create strong procurement cost pressure create adoption barriers that energy efficiency programme incentives partially address.

Opportunities: Smart motor integration with IIoT condition monitoring and permanent magnet motor efficiency advancement creating premium inverter duty motor categories

Smart inverter duty motor systems integrating embedded vibration sensors, winding temperature monitoring, and bearing condition assessment with IIoT connectivity represent the most commercially significant near-term market development opportunity, where the motor’s transformation from a passive mechanical output device into an active condition reporting asset creates predictive maintenance value above the VFD energy efficiency benefit alone. Each industrial facility that deploys connected motor monitoring capable of detecting bearing wear, winding insulation degradation, and mechanical imbalance before catastrophic failure creates maintenance cost savings and production continuity benefits whose documented ROI sustains premium connected motor specification above standard inverter duty motor economics.

Recent Developments:

-

2024: ABB launched its IE5 ultra-premium efficiency inverter duty synchronous reluctance motor series for industrial pump and fan applications, achieving 40% fewer losses than IE2 motors with an integrated drive system certification ensuring optimised motor-VFD interaction performance.

-

2023: Regal Rexnord launched its Marathon Blue Max Ultra Plus inverter duty motor series with 2100V peak voltage insulation capability for long cable-run VFD installations where reflected wave phenomena create transient voltages exceeding standard 1600V inverter duty motor specifications.

-

2023: WEG Industries launched its W22 IE4 Super Premium efficiency inverter duty motor range with integrated vibration sensor compatibility for IIoT predictive maintenance connectivity, enabling motor condition monitoring integration within existing plant digitalisation programmes.

Inverter Duty Motor Market Key Players are:

-

ABB

-

Siemens

-

WEG

-

Nidec Motor Corporation

-

Regal Rexnord Corporation

-

Rockwell Automation

-

General Electric

-

Toshiba Industrial Products

-

TECO-Westinghouse

-

TMEIC

-

Yaskawa Electric Corporation

-

Mitsubishi Electric Corporation

-

Brook Crompton

-

FUKUTA Electric & Machinery Co., Ltd.

-

Bodine Electric Company

-

Bison Gear & Engineering Corporation

-

KEB Automation

-

Fuji Electric Co., Ltd.

-

Schneider Electric

-

Havells India Limited

Inverter Duty Motor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.27 Billion |

| Market Size by 2035 | USD 16.59 Billion |

| CAGR | CAGR of 10.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Motor Type (AC Induction Motors, Permanent Magnet Motors, Servo Motors, Synchronous Motors, DC Motors) • By Phase (Single Phase, Three Phase) • By Voltage (Low Voltage, Medium Voltage, High Voltage) • By Application (Pumps, Fans & Blowers, Compressors, Conveyors & Material Handling, HVAC Systems, Machine Tools, Others) • By End-User Industry (Manufacturing, Oil & Gas, Chemical & Petrochemical, Power Generation, Water & Wastewater Treatment, Food & Beverage, Automotive, Mining & Metals, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB, Siemens, WEG, Nidec Motor Corporation, Regal Rexnord Corporation, Rockwell Automation, General Electric, Toshiba Industrial Products, TECO-Westinghouse, TMEIC, Yaskawa Electric Corporation, Mitsubishi Electric Corporation, Brook Crompton, FUKUTA Electric & Machinery Co., Ltd., Bodine Electric Company, Bison Gear & Engineering Corporation, KEB Automation, Fuji Electric Co., Ltd., Schneider Electric, Havells India Limited |

Frequently Asked Questions

The Inverter Duty Motor Market is expected to grow at a CAGR of 10.22% from 2026 to 2035.

The Inverter Duty Motor Market was valued at USD 6.27 Billion in 2025.

Energy efficiency regulations, industrial automation, VFD adoption, predictive maintenance integration, and variable flow control drive growth.

The Pumps segment dominated the Inverter Duty Motor Market with the largest share in 2025.

North America dominated the Inverter Duty Motor Market.

Get in Touch