Lab-Based IVD Market Size & Trends:

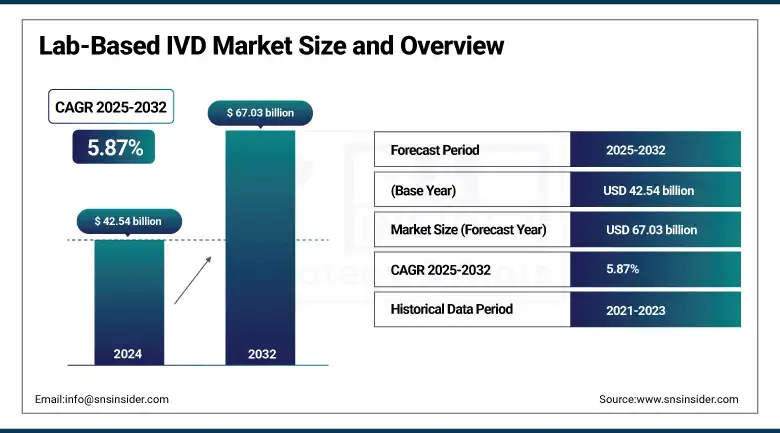

The Lab-Based IVD Market size was valued at USD 42.54 billion in 2024 and is expected to reach USD 67.03 billion by 2032, growing at a CAGR of 5.87% over 2025-2032.

The global lab-based IVD market is growing at a fast pace, driven by the growing prevalence of chronic diseases, awareness of early diagnosis, and technological advancements in testing. Growing geriatric population and increased use of molecular diagnostics are impelling demand for lab-based IVDs, particularly in developed regions, such as the U.S. The U.S. lab-based IVD market has witnessed a jump in the adoption rate on account of the rising penetration of health insurance and favorable reimbursement plans.

To Get more information On Lab-Based IVD Market - Request Free Sample Report

Abbott introduced its Alinity m STI assay in April 2024, which is capable of detecting CT/NG/MG/TV at the same time in the same assay (multiplexed diagnostics is becoming mainstream in the lab-based IVD market).

Indeed, one of the main drivers of market expansion has been Medicare’s broad coverage of lab tests based on next-generation sequencing (NGS). Furthermore, the OECD states that global R&D investment in health and well-being totaled over USD 220 billion in 2023, much of which was indirectly earmarked for diagnostic innovation. Investment activity has also been impressive. VC investment in diagnostics topped USD 6 billion in 2023. Regulators, such as the FDA, are accelerating lab-developed test (LDT) approvals, improving the accuracy and pace of clinical diagnostics. This sort of regulatory certainty is also prompting lab-based IVD companies to ramp up product pipelines and clinical trials, as evidenced by both Roche and Abbott, which each grew their lab-based testing platforms in 2024. Moreover, the lab-based IVD market analysis reads of quick uptake in liquid biopsies and infectious disease testing, driven by increased post-pandemic monitoring.

CE-IVDR clearance of its extended digital pathology offering was obtained by Roche Diagnostics in May 2024, marking a move toward AI-enhanced diagnostics driving the global lab-based IVD market.

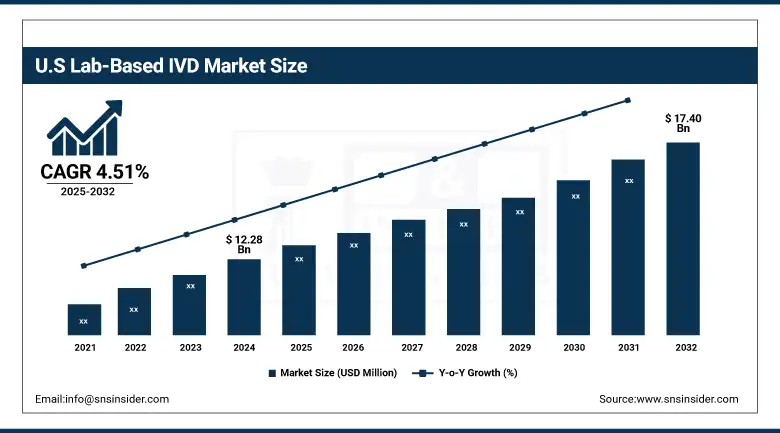

The U.S. lab-based IVD market size was valued at USD 12.28 billion in 2024 and is expected to reach USD 17.40 billion by 2032, growing at a CAGR of 4.51% from 2025 to 2032. The U.S. dominates the region following high R&D expenditure, strong regulatory avenues (CLIA and FDA approval), and leading industry players Abbott, Thermo Fisher, and Quest Diagnostics in the region. The U.S. is also a leading adopter of molecular diagnostic and automation platforms in the region, these being other robust contributors to the region, including dominance. There is increasing demand for infectious disease and genetic testing in Canada, in part because of heightened awareness of public health and investment in diagnostics infrastructure. Mexico is seeing greater access to laboratory diagnostics through healthcare reforms and in international collaboration, providing a boost to regional development.

Lab-Based IVD Market Dynamics:

Drivers:

-

Technological Innovation, Precision Diagnostics, And Healthcare Digitization Are Fueling the Lab-Based IVD Market Growth

Rising demand for early and accurate diagnosis, owing to the surge in non-communicable diseases boosting the lab-based IVD market growth declining share for hospital-based diagnostics. The lab-based IVD is the dominating technique in the global IVD market. Increasing use of molecular diagnostics, immunoassays, and next-generation sequencing in the clinical laboratory is changing the face of diagnostic precision. The lab-based IVD market trends related to laboratory-based IVDs indicate a growing trend toward automation and AI integration in the laboratory workflow.

For instance, Thermo Fisher’s Ion Torrent Genexus Dx Integrated Sequencer, an advanced AI-based automated NGS platform which is scheduled to be launched in 2024, is enabling same-day reporting, improved patient outcomes, and greater lab efficiency.

By contrast, global healthcare R&D spending reached nearly USD 243 billion in 2023, the World Bank states, where an ever-increasing fraction is from diagnostics, due to rising demand. Legislation such as the U.S. VALID Act, which offers clarification on the regulation of lab-developed tests, is also having a favorable effect on adoption, she reported. Further, pandemic-related public and private investments into the lab testing infrastructure and the supply chain stabilization actions have positioned a more responsive lab network to nurture deeper and richer lab-based IVD market analysis. The growing awareness and availability of diagnostics in low- and middle-income countries, in addition to the penetration of digital health, also continue to contribute to the increasing lab-based IVD market in different clinical areas.

Restraints:

-

Regulatory Complexity, Cost Constraints, and Supply-Chain Inefficiencies are Limiting Adoption in Several Regions, Hampering the Market Expansion

Although the lab-based IVD market is growing strongly, it is constrained by a complex regulatory environment and the high associated costs for developing, validating, and deploying new tests. Regulatory obstacles and inconsistent oversight, especially across international markets, can slow down approval processes.

For instance, increased requirements on the part of the FDA concerning LDTs under the 2024 Final Rule have brought compliance challenges for smaller diagnostic labs.

Additionally, the expense of molecular and genetic testing methods has restricted their availability in resource-limited settings. The average out-of-pocket expense in 2023 for advanced diagnostics tests in developing countries was USD 150-300, resulting in a gap in affordability. Moreover, lab-based IVD market analysis reveals that there continue to be some issues with the supply chain for key reagents and equipment that are delaying sample processing in remote labs. In addition, there is a lack of trained lab professionals predicted to exceed 500,000 as a global gap by 2026 (WHO estimate), leading to capacity bottlenecks.

Such systemic limitations not only lower the efficiency of testing but also limit the expansion of the lab-based IVD market share in low-resource areas. Data privacy concerns, especially for digital diagnostics, continue to hamper adoption downward even as technology makes its mark on lab-based IVD market dynamics.

Lab-Based IVD Market Segmentation Analysis:

By Product Type

The reagents & consumables segment held the largest share of the global lab-based IVD market in 2024, which is 63% of the market. This domination is influenced by the repetitive, exploitative use of reagents in high-throughput diagnostic tests, often in clinical laboratories and medical centers. Increasing necessity for credible diagnostic kits and disease-specific testing panels drives the demand.

The instruments segment, in the meantime, is expected to witness the fastest growth, supported by the growing automation, technological advances, and mounting installations of high-throughput diagnostic analyzers in developed and developing health care systems.

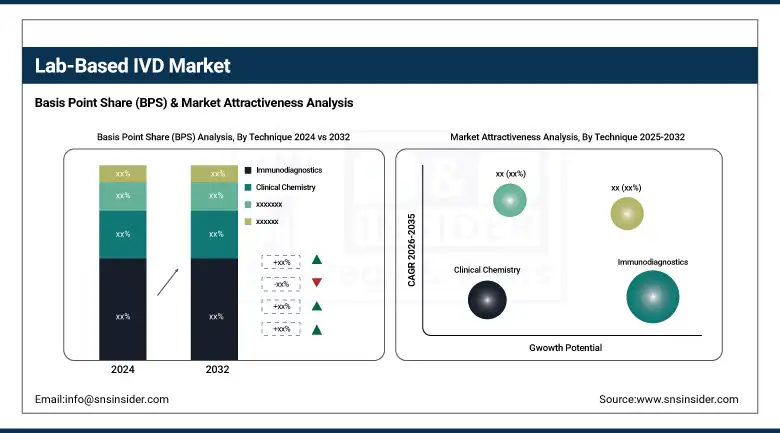

By Technique

Immunodiagnostics was the leading technology in 2024, with over 38% of the market share, as it is sensitive, provides quick results, and is widely used for both infectious disease and chronic disease testing.

The market is driven by the rising prevalence of blood-related diseases globally and technological advancements in the field of hematological analyzers that enable multi-parameter testing and provide enhanced accuracy.

By Sample Type

In 2024, the blood sample segment was the largest in the lab-based IVD market, which accounted for 47% of the total share due to the prevalence of use in a number of diagnostic assays, especially in immunodiagnostics, molecular testing, and hematology. Its superiority is further supported due to ease of access and increased diagnostic yield.

Blood segment is also the fastest growing category, owing to its ease of use and compatibility with most of the automated analyzers and multi-analyte tests.

By Application

The market share for infectious diseases accounted for 42% of the global lab-based IVD total. The growth is mainly attributed to the extensive number of tests after the pandemic outbreak, escalated surveillance, and rising demand for effective pathogen detection technologies.

The others application segment, which includes endocrinology, nephrology, and rare disease diagnostics, is expected to register the highest growth rate due to increased clinical awareness, availability of a large number of tests, and the shift toward personalized medicine.

By End-User

Clinical laboratories held more than 54% share of the market in 2024 due to their inclination to perform high-volume and complex tests with specific infrastructure. Their scalability, automation, and integration with hospital systems are some of the reasons they are ahead in the race. This segment is also anticipated to be the fastest-growing due to the increasing demand for centralized diagnostic services and the surge in lab-diagnostics companies' partnerships for specialized testing.

Lab-Based IVD Market Regional Insights:

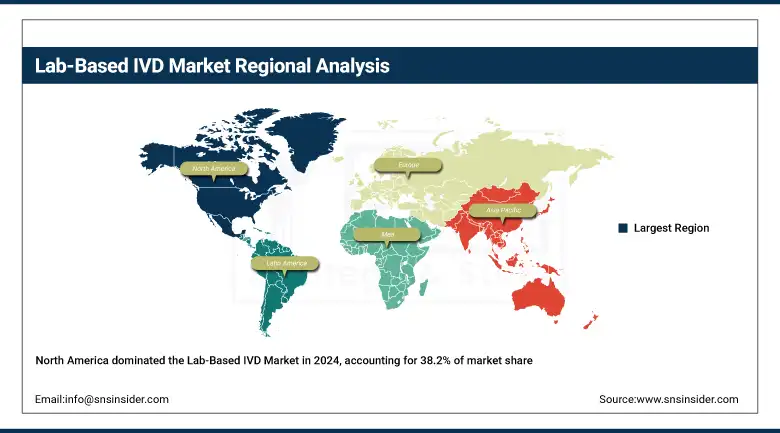

North America held the largest share in the global lab-based IVD market in 2024, with a 38.2% share, owing to advanced healthcare facilities and substantial reimbursement policies, along with an inclination toward sophisticated diagnostic technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second largest region in the global lab-based IVD market, due to the growing elderly population, the national programs of screening, and the high public health care spending. Countries, such as Germany and the U.K. have the largest market for POC testing as there the laboratory networks are very strong plus governments in these regions are investing in diagnostic management practices with a strong focus on early disease diagnosis, prevention, and management with rapid testing techniques that get results within minutes, use of immunodiagnostics and blood tests (hematology testing).

In the early stage, firstly, Germany directly benefits as a capital infrastructure player in computerized and AI-driven laboratory solutions, already 75% of the clinical lab market is already operating with sophisticated diagnostic equipment. Quality and safety standards are bolstered by the CE-IVDR. France and Italy continue to demonstrate demand growth, and Poland and Turkey are investing significantly in the modernization of their healthcare systems, driving regional growth.

The lab-based IVD market in Asia Pacific is expected to grow at the highest CAGR during the forecast period due to the growing patient population, rapidly increasing geriatric population, and favorable government initiatives. China is leading the pack in the region, with aggressive efforts on healthcare digitization, indigenous manufacture of diagnostic devices, and increased public-private partnerships. Since 2022, more than 30% of hospitals in the country have introduced automatic diagnostic laboratories.

India is growing fast on account of the increased focus on preventive healthcare, the proliferation of diagnostics chains, and government schemes, including Ayushman Bharat, where diagnostics is part of public cover. Japan is experiencing continuous growth due to its well-developed healthcare system and high interest in genetic and geriatric testing. South Korea and Singapore have the highest utilization of cutting-edge technologies such as NGS and digital pathology. They also continue to enjoy conducive regulatory environments and innovation-led ecosystems, which propel the region’s good momentum in the lab-based IVD market.

Key Players in the Lab-Based IVD Market:

Leading lab-based IVD companies operating in the market are F. Hoffmann-La Roche Ltd., Abbott, Thermo Fisher Scientific Inc., Sysmex Corporation, Siemens Healthineers AG, BD, QIAGEN, Bio-Rad Laboratories Inc., Seegene Inc., DiaSorin S.p.A., and Quest Diagnostics Incorporated.

Recent Developments in the Lab-Based IVD Market:

In April 2025, Seegene unveiled CURECA, its next-generation platform that automates PCR workflows and sample handling, reflecting a broader industry shift toward laboratory efficiency and automation within lab-based IVD market analysis.

In February 2024, Quest Diagnostics introduced MelaNodal Predict, a cutting-edge gene-expression assay designed to personalize melanoma treatment decisions by assessing the risk of lymph node metastasis, highlighting how lab-based IVD market trends increasingly emphasize precision medicine.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 42.54 billion |

| Market Size by 2032 | USD 67.03 billion |

| CAGR | CAGR of 5.87% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Instruments, Reagents, and Consumables) • By Technique (Immunodiagnostics, Clinical Chemistry, Molecular Diagnostics, Hematology, and Others) • By Sample Type (Blood, Urine, Saliva, Tissue, and Others) • By Application (Infectious Diseases, Cardiology, Oncology, Gastroenterology, Allergy, Autoimmunity, Prenatal Screening, and Others) • By End-User (Hospitals, Clinical Laboratories, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | F. Hoffmann-La Roche Ltd., Abbott, Thermo Fisher Scientific Inc., Sysmex Corporation, Siemens Healthineers AG, BD, QIAGEN, Bio-Rad Laboratories Inc., Seegene Inc., DiaSorin S.p.A., and Quest Diagnostics Incorporated. |

Frequently Asked Questions

North America dominated the Lab-Based IVD market.

Although the lab-based IVD market is growing strongly, it is constrained by a complex regulatory environment and the high associated costs for developing, validating, and deploying new tests.

Rising demand for early and accurate diagnosis, owing to the surge in non-communicable diseases boosting the lab-based IVD market growth declining share for hospital-based diagnostics.

The market is expected to reach USD 67.03 billion by 2032, increasing from USD 42.54 billion in 2024.

The Lab-Based IVD market is anticipated to grow at a CAGR of 5.87% from 2025 to 2032.

Get in Touch