Laparoscopy Instruments Market Report Scope & Overview:

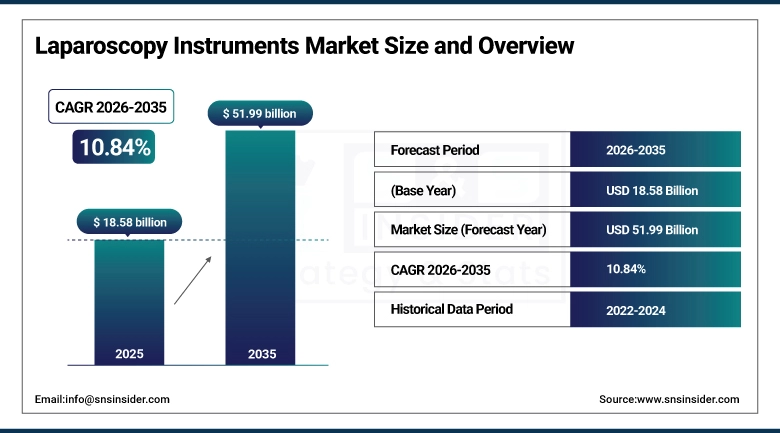

The Laparoscopy Instruments Market was valued at USD 18.58 Billion in 2025 and is expected to reach USD 51.99 Billion by 2035, growing at a CAGR of 10.84% from 2026 to 2035.

Laparoscopic surgery has become the default choice for a growing share of abdominal and gynecological procedures, largely because it trades a single large incision for a handful of small ones guided by a camera and a set of precision instruments. Patients tend to leave the hospital sooner, heal with less scarring, and face a lower infection risk than they would after open surgery, which is why hospitals keep steering more of their surgical caseload this way. Rising rates of gallbladder disease, obesity, and gynecological disorders are adding to that caseload every year, while newer 4K imaging, single-incision platforms, and robotic assistance keep expanding what laparoscopy can be used for. A study published in the Journal of Minimally Invasive Surgery in February 2024 found a 34% drop in post-operative complications among laparoscopic colorectal patients versus open-surgery cohorts, lending further clinical weight to the shift. Equipment costs and the training surgeons need before operating solo remain the main things holding broader adoption back.

Market Size and Forecast

-

Market Size in 2026E: USD 20.58 Billion

-

Market Size by 2035: USD 51.99 Billion

-

CAGR: 10.84% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Laparoscopy Instruments Market - Request Free Sample Report

Laparoscopy Instruments Market Trends

-

Hospitals continue to favor minimally invasive pathways over open surgery, since patients recover faster and see fewer complications.

-

More operating rooms are installing 4K and 3D visualization towers, giving surgeons a sharper view of the operative field.

-

Single-use instruments are gaining ground as infection-control protocols tighten and hospitals look to simplify sterilization workflows.

-

AI-guided robotic platforms are drawing interest for how much they ease surgeon fatigue during longer procedures.

-

Bariatric and metabolic surgery volumes keep climbing alongside global obesity rates, with laparoscopy as the default approach.

-

Newer energy devices, like ultrasonic dissectors and advanced bipolar sealers, are cutting operative time by combining sealing and cutting in one pass.

The U.S. Laparoscopy Instruments Market Outlook

The U.S. Laparoscopy Instruments Market was valued at approximately USD 7.18 Billion in 2025 and is expected to reach approximately USD 20.14 Billion by 2035, growing at a CAGR of approximately 10.89%.

A few things keep U.S. growth ahead of the global pace: a heavy volume of elective and bariatric procedures each year, a dense network of ambulatory surgical centers, and payer policy, both CMS and private insurers, that generally leans toward laparoscopic techniques where they are clinically appropriate. Hospital systems keep investing in newer laparoscopic towers, energy platforms, and robotic-assisted systems, and the FDA's approval pathway is mature enough that new instruments often reach American operating rooms before they reach anywhere else. Intuitive Surgical's da Vinci 5 platform, cleared by the FDA in January 2025, is one recent example, adding AI-assisted anatomical landmark recognition to an already large installed base of robotic systems across U.S. hospitals.

Laparoscopy Instruments Market Segment Analysis

-

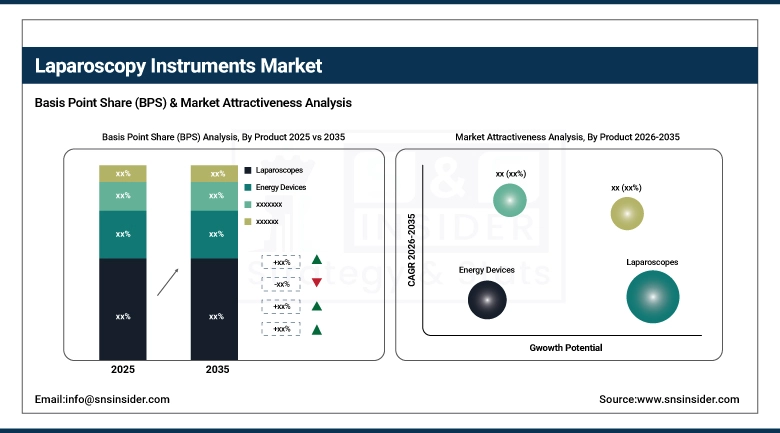

By Product, the laparoscopes segment dominated the laparoscopy instruments market with approximately 29.45% share in 2025, while the energy devices segment is the fastest growing with a CAGR of approximately 11.62%.

-

By Application, the general surgery segment dominated the laparoscopy instruments market with a 31.28% revenue share in 2025, while the bariatric surgery segment is the fastest growing with a CAGR of approximately 12.15%.

-

By Usage, the reusable segment dominated the laparoscopy instruments market with approximately 61.35% share in 2025, while the disposable segment is the fastest growing with a CAGR of approximately 12.47%.

-

By End-use, the hospitals segment dominated the laparoscopy instruments market with a 67.82% revenue share in 2025, while the ambulatory surgical centers segment is the fastest growing with a CAGR of approximately 12.31%.

By Product, laparoscopes dominate, energy devices grow fastest

Laparoscopes led the product segment in 2025, holding roughly 29.45% of the market. Every laparoscopic procedure needs one regardless of surgical specialty, which keeps demand steady across hospitals and ambulatory centers alike, even as procedure volumes shift between specialties year to year. Older optical systems are steadily giving way to HD and 4K-enabled scopes, and flexible, articulating designs built to reach difficult anatomy are becoming the norm, reinforcing the category's central place in operating room budgets.

Energy devices are growing faster than any other product category, with a CAGR near 11.62% expected through 2035. Ultrasonic dissectors and advanced bipolar sealers that cut and seal tissue in a single pass are shaving time off procedures, and rising bariatric and oncology surgery volumes are adding steady demand for single-use versions built specifically for those cases, a trend suppliers are increasingly designing around.

By Application, general surgery dominates, bariatric surgery grows fastest

General surgery held the largest share of the application segment in 2025, at 31.28%, driven mostly by sheer volume: cholecystectomies, hernia repairs, and appendectomies happen routinely across both hospitals and ambulatory centers. These procedures are comparatively simple, cost-efficient, and backed by decades of safety data, which is why the category has stayed on top even as other applications expand faster in percentage terms.

Bariatric surgery is set to grow fastest among applications, with a CAGR near 12.15% expected between 2026 and 2035. Climbing obesity rates worldwide, more accredited bariatric programs, and easier patient access to weight-loss surgery are together pushing up demand for the trocars, energy sealers, and endoscopic staplers this kind of surgery depends on, particularly as insurance coverage for these procedures widens.

By Usage, reusable instruments dominate, disposable instruments grow fastest

Reusable instruments accounted for about 61.35% of the usage segment in 2025. Cost is the main driver here: reusable sets are cheaper across high-volume settings, hospitals already have the sterilization infrastructure in place, and surgeons know these instrument sets well, an advantage reinforced by group purchasing deals that lower long-term ownership costs for hospital systems operating at scale.

Disposable instruments are catching up fast, with a projected CAGR near 12.47% through 2035. Infection-control protocols that tightened during the pandemic haven't loosened much since, and a wider range of affordably priced disposable trocars, graspers, scissors, and clip appliers is making the switch easier to justify financially, especially in high-turnover operating rooms.

By End-use, hospitals dominate, ambulatory surgical centers grow fastest

Hospitals accounted for about 67.82% of the end-use segment in 2025, reflecting their capacity to handle complex cases, staff full surgical teams, and commit larger budgets to advanced instrumentation, particularly at teaching hospitals that tend to adopt new laparoscopic platforms first, well ahead of smaller community facilities.

Ambulatory surgical centers are the fastest-growing end-use setting, with a CAGR near 12.31% projected through 2035. Cost pressure keeps pushing procedures out of the hospital altogether, CMS reimbursement keeps expanding for outpatient laparoscopic work, and patients increasingly prefer same-day surgery when it's an option, a preference that shows little sign of reversing.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

92.0% |

|

Europe |

Germany |

24.0% |

|

Asia Pacific |

China |

35.0% |

|

Middle East & Africa |

UAE |

26.0% |

|

Latin America |

Brazil |

40.0% |

North America Laparoscopy Instruments Market Insights

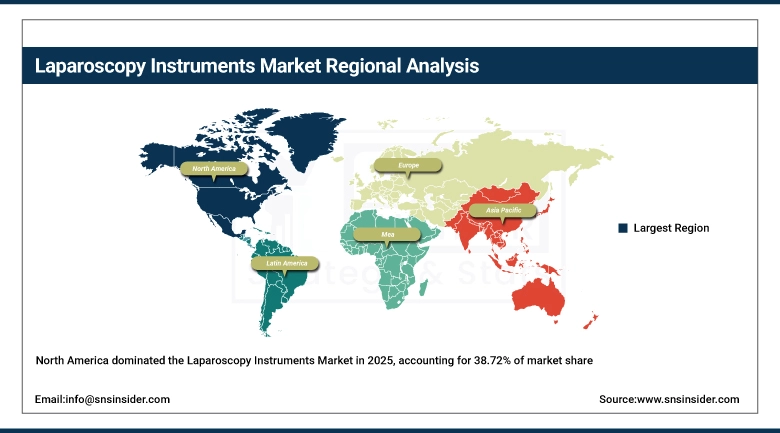

North America led the global laparoscopy instruments market in 2025, with more than 38.72% of total revenue. That lead comes down to a high rate of surgical procedures per capita, solid reimbursement coverage from both private and public payers, and an early appetite for robotic-assisted platforms. The U.S. alone made up over 92% of regional revenue, a reflection of just how many hospitals, ambulatory centers, and major device makers are clustered there. Canada is seeing steady growth too, as public hospital investment in minimally invasive surgical departments expands.

Companies like Intuitive Surgical, Medtronic, and Ethicon, part of J&J MedTech, tend to launch their newest robotic and energy-based platforms in North America first, which keeps the region ahead on both innovation and case volume. Intuitive Surgical's da Vinci 5 platform, cleared by the FDA in January 2025 with AI-assisted anatomical landmark recognition, is a recent example of that pattern. Deep hospital capital budgets and well-established surgeon training programs should keep North America out front through 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Laparoscopy Instruments Market Insights

Europe is the second-largest regional market for laparoscopy instruments, built on strong adoption of evidence-based minimally invasive protocols across Germany, France, the UK, and Italy. Germany carries the biggest share of regional demand, helped by public healthcare policy that favors laparoscopic techniques as a way to ease pressure on hospital bed capacity and overall treatment costs. The UK and France remain significant secondary markets, backed by well-established hospital networks.

The EU's medical device regulation keeps quality standards high across the board, and national surgical training programs keep producing credentialed laparoscopic surgeons at a steady clip. Medtronic expanded CE Mark-approved deployments of its Hugo robotic-assisted system across seven more European markets in April 2024, widening regional access to robotic laparoscopic capability. Cross-border research collaboration and shared technology funding should keep supporting growth across the continent.

Asia Pacific Laparoscopy Instruments Market Insights

Asia Pacific is set to post the fastest regional CAGR, somewhere around 13.15% through 2035. Surgical infrastructure is modernizing quickly, governments are pouring more money into tertiary healthcare facilities, and patient volumes across China, India, Japan, and South Korea are climbing fast. A huge population dealing with gallbladder disease, gynecological conditions, and obesity-related illness sits behind a lot of that demand, and hospital construction across the region is not slowing down.

China holds the largest share within the region, helped by the scale of its hospital network and a fast-growing domestic device industry. Medical tourism built around affordable laparoscopic surgery, expanding domestic manufacturing in China and India, and wider health insurance coverage across ASEAN countries are all adding momentum, alongside government-led digitalization of hospital infrastructure that is extending laparoscopic capability into smaller regional hospitals.

MEA & Latin America Laparoscopy Instruments Market Insights

The Middle East and Africa remain an early-stage market for laparoscopy instruments, with the UAE leading through continued investment in advanced hospital infrastructure and Saudi Arabia expanding its healthcare sector under its Vision 2030 diversification plan. Cheaper laparoscopic instrument kits from Asian manufacturers are helping extend access across the wider region, especially at secondary and tertiary care facilities in underserved areas that previously relied on open surgical techniques.

Latin America's growth is steadier, led by Brazil, where hospital networks and private healthcare providers are investing in laparoscopic capacity to keep pace with rising surgical demand. Mexico comes in second regionally, supported by growing private healthcare investment and a larger pool of surgeons trained in minimally invasive techniques, with slowly improving reimbursement frameworks adding further support across both public and private facilities.

Market Dynamics

Growth Drivers: Rising global surgical burden and chronic disease incidence

More people needing surgery is, in the simplest terms, one of the biggest forces behind this market. Gallbladder disease, endometriosis, colorectal cancer, urological disorders, and severe obesity are all becoming more common, and the World Health Organization puts the number of major surgeries performed globally each year above 310 million, with roughly 65% of elective abdominal procedures in high-income countries now done using minimally invasive methods.

That shift shows up directly in rising use of trocars, insufflators, hand instruments, and laparoscopes across surgical departments everywhere. The American College of Surgeons noted in July 2024 that laparoscopic cholecystectomy now accounts for over 92% of all cholecystectomies performed in U.S. hospitals, close to 1.2 million procedures a year, a clear sign of how far surgical practice has already moved toward laparoscopic instrumentation.

Restraints: High capital costs and surgeon training requirements limiting adoption

The clinical case for laparoscopic surgery is well established at this point, but the price tag on the equipment still shuts out a lot of smaller hospitals, especially in developing countries. A robotic-assisted platform typically runs USD 1.5 million to USD 2.5 million, and even a standard laparoscopic tower costs USD 80,000 to USD 250,000, numbers that put advanced instrumentation out of reach for plenty of resource-constrained facilities.

On top of that, laparoscopic surgery has a genuinely steep learning curve. Surgeons need standardized residency training, simulation-based competency checks, and formal credentialing before they can operate solo, and that combination of high upfront cost and a long training runway keeps adoption slower in smaller and rural healthcare settings, even where demand for these procedures is otherwise strong.

Opportunities: AI-integrated robotic platforms creating new growth avenues

Pairing artificial intelligence with laparoscopic instruments opens up a real opportunity: real-time guidance during surgery, automatic tissue identification, and predictive analytics on surgical outcomes. Early results suggest surgical time can drop by as much as 27%, alongside better recognition of critical anatomical landmarks and fewer accidental organ injuries, which adds up to real value for hospitals and payers alike.

As of March 2024, AI-integrated laparoscopic guidance systems were already running in roughly 41% of tertiary-care robotic surgery centers across North America, a sign of how quickly institutions are picking this up. Investors have noticed too: the surgical robotics and minimally invasive technology startup space pulled in more than USD 3.2 billion in venture funding in 2023 alone, which should keep next-generation laparoscopic platforms well funded through 2035.

Recent Developments:

-

2025: Intuitive Surgical, Inc. received FDA clearance for its next-generation da Vinci 5 platform, featuring enhanced instrument force feedback, real-time fluorescence imaging, and AI-assisted anatomical landmark recognition, expanding its footprint across colorectal, bariatric, and urological laparoscopic procedures.

-

2024: Medtronic plc expanded CE Mark-approved deployments of its Hugo robotic-assisted surgery system across seven additional European markets, pairing the rollout with a laparoscopic instrument accessory bundle aimed at general and gynecological surgery departments.

-

2024: Johnson & Johnson MedTech's Ethicon division launched the ENSEAL X1 Curved Jaw Tissue Sealer, an advanced vessel-sealing device for laparoscopic hysterectomy and colorectal procedures that has shown meaningfully lower seal-failure rates than earlier-generation devices in post-market clinical evaluation.

Laparoscopy Instruments Market key players are:

-

Intuitive Surgical, Inc.

-

Medtronic plc

-

Johnson & Johnson MedTech (Ethicon)

-

Stryker Corporation

-

Karl Storz SE & Co. KG

-

Olympus Corporation

-

B. Braun Melsungen AG

-

CONMED Corporation

-

Richard Wolf GmbH

-

Teleflex Incorporated

-

Applied Medical Resources Corporation

-

Becton, Dickinson and Company (BD)

-

Microline Surgical, Inc.

-

Integra LifeSciences Corporation

-

Aesculap AG (B. Braun Group)

-

Surgical Innovations Group plc

-

LaproSurge Ltd.

-

Purple Surgical International Ltd.

-

Ackermann Instrumente GmbH

-

Gimmi GmbH

Laparoscopy Instruments Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.58 Billion |

| Market Size by 2035 | USD 51.99 Billion |

| CAGR | CAGR of 10.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Laparoscopes, Video Laparoscopes, Fiber Laparoscopes, Energy Devices, Insufflators, Suction Systems, Closure Devices, Hand Instruments, Access Devices, Laparoscopic Accessories) • by Application (Gynecological Surgery, Urological Surgery, Colorectal Surgery, Bariatric Surgery, General Surgery, Pediatric Surgery, Other Applications) • by Usage (Disposable, Reusable) • by End-use (Hospitals, Ambulatory Surgical Centers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Intuitive Surgical, Inc., Medtronic plc, Johnson & Johnson MedTech (Ethicon), Stryker Corporation, Karl Storz SE & Co. KG, Olympus Corporation, B. Braun Melsungen AG, CONMED Corporation, Richard Wolf GmbH, Teleflex Incorporated, Applied Medical Resources Corporation, Becton, Dickinson and Company (BD), Microline Surgical, Inc., Integra LifeSciences Corporation, Aesculap AG (B. Braun Group), Surgical Innovations Group plc, LaproSurge Ltd., Purple Surgical International Ltd., Ackermann Instrumente GmbH, Gimmi GmbH |

Frequently Asked Questions

The Laparoscopy Instruments Market is expected to grow at a CAGR of 10.84% from 2026 to 2035.

A rising global surgical burden, combined with the ongoing shift from open to minimally invasive procedures, is the primary factor driving demand for laparoscopy instruments.

The Laparoscopy Instruments Market was valued at USD 18.58 Billion in 2025.

North America dominated the Laparoscopy Instruments Market in 2025 with over 38.72% market share.

Laparoscopes dominated with approximately 29.45% share in 2025.

Get in Touch