Lithium-Sulfur Battery Market Report Scope & Overview:

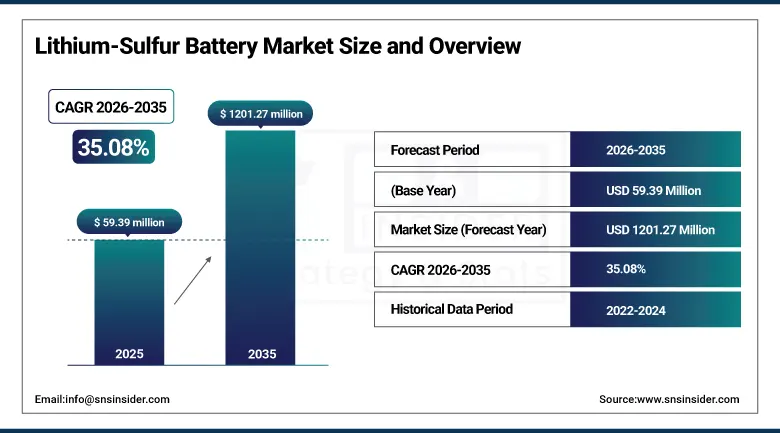

The Lithium-Sulfur Battery Market size was valued at USD 59.39 Million in 2025 and is expected to reach USD 1201.27 Million by 2035, growing at a CAGR of 35.08% from 2026 to 2035.

The Lithium-Sulfur Batteries Market is in its most critical phase of evolution, moving from sophisticated laboratory experiments and demonstration phases to initial commercialization in numerous mission-critical application segments. These batteries utilize sulfur as the cathode and lithium metal as the anode. The theoretical energy density offered by these batteries far exceeds the energy density of any current lithium-ion battery chemistry. Due to their superior energy density, these batteries have considerable appeal to industries where lightness is paramount, along with extended operational periods.

Several technology developers, including Sion Power, Lyten, and OXIS Energy, have reported energy densities exceeding 400 to 500 Wh/kg under controlled conditions, validating the technology's commercial potential. As manufacturing processes mature and scale-up investments increase, cost per kilowatt-hour is expected to decline meaningfully, broadening the addressable market beyond niche aerospace and defense applications into mainstream automotive and stationary storage segments.

Lithium-Sulfur Battery Market Size and Forecast

-

Market Size in 2025: USD 59.39 Million

-

Market Size by 2035: USD 1201.27 Million

-

CAGR: 35.08% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Lithium-Sulfur Battery Market - Request Free Sample Report

Lithium-Sulfur Battery Market Trends

-

Accelerating R&D investment in sulfur cathode engineering and lithium metal anode stabilization to extend cycle life toward commercial requirements.

-

Growing interest from electric vehicle manufacturers in adopting lithium-sulfur cells to achieve greater driving range without increasing battery pack weight.

-

Rising deployment of lithium-sulfur batteries in drone and UAV programs where lightweight, high-energy power sources are essential for extended flight endurance.

-

Increasing involvement of aerospace and defense contractors evaluating lithium-sulfur technology for next-generation unmanned platforms and soldier-portable systems.

-

Emergence of solid-state and semi-solid lithium-sulfur variants that address polysulfide shuttle challenges while improving safety and thermal stability.

-

Expansion of pilot-scale and early commercial production facilities by key technology developers seeking to demonstrate manufacturing scalability.

-

Growing ecosystem of government-backed funding programs, including the U.S. Battery500 Consortium and European battery research alliances, supporting lithium-sulfur commercialization pathways.

U.S. Lithium-Sulfur Battery Market Size Outlook:

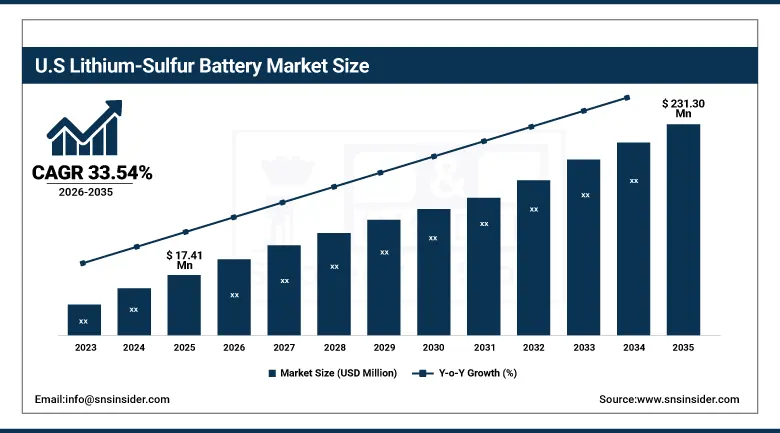

The U.S. Lithium-Sulfur Battery Market was valued at USD 17.41 Million in 2025 and is expected to reach USD 231.30 Million by 2035, registering a CAGR of 33.54% during 2026–2035.

The US enjoys the largest market share in terms of lithium sulfur batteries globally, contributing up to 37% of the overall revenue for this market in 2025. The US dominance in this regard stems from its unmatched number of research institutes, experts in the technology of designing and manufacturing advanced batteries, as well as military organizations interested in energy storage technology of the future. Indeed, the US has been running various programs for the development of lithium sulfur batteries funded by such bodies as the Defense Advanced Research Projects Agency and the Department of Energy since the beginning of the last decade.

Private sector investment has accelerated significantly, with companies such as Sion Power, Lyten, and PolyPlus Battery Company attracting substantial venture and strategic capital to advance lithium-sulfur technology from laboratory demonstration toward pilot-scale production.

Lithium-Sulfur Battery Market Segment Insights

-

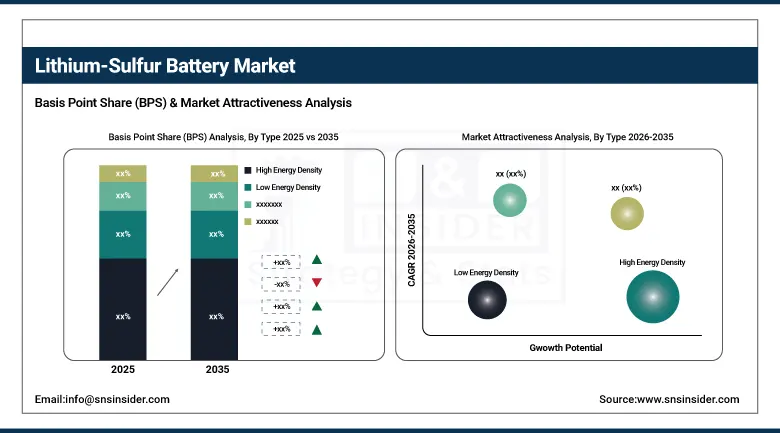

Based on Type, High Energy Density segment accounted for the largest market share at 73.60% in 2025; Low Energy Density segment expected to be the fastest-growing at a CAGR of 37.80%.

-

Based on Capacity, Above 1000 mAh segment held the dominant share in 2025; Below 500 mAh segment expected to be the fastest-growing at a CAGR of 37.38%.

-

Based on Application, Aviation & UAV segment accounted for the largest market share at 33.70% in 2025 and is also expected to register the highest CAGR through 2035.

-

Based on End Use, Aerospace segment led the market with 31.60% share in 2025 and is also expected to be the fastest-growing end-use segment through 2035.

-

Based on Region, North America dominated the global market in 2025; Asia Pacific expected to register the highest CAGR during the forecast period.

By Type, High Energy Density segment dominates the Lithium-Sulfur Battery Market, Low Energy Density segment expected to grow fastest

Segmentation on the basis of energy density revealed that High Energy Density constituted the dominant market share of 73.60% during 2025 owing to the significant influence of high gravimetric energy performance as the prime motivator behind increased adoption rates of lithium-sulfur batteries. The high energy density batteries are designed using sophisticated sulfur cathodes and electrochemical designs which offer the high gravimetric power density necessary for aerospace, military, and electric vehicles. The leading manufacturers of high energy density lithium-sulfur batteries include Sion Power with its Licerion battery platform recording more than 500 Wh/kg energy density, and OXIS Energy targeting the development of high energy density batteries for aviation applications.

Low Energy Density batteries will record the highest CAGR of 37.80% during the period 2026-2035. Although the low energy density batteries provide less energy, they serve a wide range of cost-sensitive applications in the form of IoT devices, smart cards, wearable electronics, and medical devices where energy output is secondary to cost efficiency and size considerations. With improved production technologies and reduced material prices, low energy density lithium-sulfur batteries can start challenging their existing counterparts in the portable electronic devices and sensors industry.

By Capacity, Above 1000 mAh segment dominates the Lithium-Sulfur Battery Market, Below 500 mAh segment expected to grow fastest

The Above 1000 mAh capacity segment ruled in 2025, accounting for a majority of the market due to application needs of power-hungry technologies like EV battery packs, aerospace powertrains, and unmanned aerial vehicle systems. Such technologies need a constant source of power for sustained periods, which makes the above 1000 mAh segment an ideal choice when it comes to using lithium sulfur batteries in engineering design. Programs for EV-grade battery modules form a major part of the segment as automotive firms consider the use of lithium sulfur technology in range extenders.

The Below 500 mAh segment will see a fast growth rate at a CAGR of 37.38%, with the most growth expected till 2035. There is an increasing demand for high-performance batteries in the manufacture of lightweight consumer gadgets, biomedical devices, tiny sensors, and lightweight military equipment. Some companies like PolyPlus and Imprint Energy are working hard to make thin, small format lithium sulfur cells to meet the rising demand from a high-growth segment.

By Application, Aviation & UAV segment dominates the Lithium-Sulfur Battery Market

Aviation & UAV application accounted for the largest market share in 2025 of 33.70% due to the importance of energy density and battery weight reduction in the segment. In fixed-wing UAVs, electric vertical take-off and landing aircraft, and high-altitude long-endurance UAVs, energy density can be translated into higher mission range and carrying capacity, resulting in savings on missions. Major global players are investigating the use of lithium-sulfur cells in next-generation aircraft and drones, and thus the Aviation & UAV application becomes the largest pull for lithium-sulfur batteries.

The Automotive & EVs segment provides one of the largest opportunities for lithium-sulfur batteries in terms of growth in the long run, although currently, activity in this segment will grow only when lithium-sulfur batteries show enough durability to become qualified for automotive use. Other rapidly growing applications include Energy Storage Systems, which benefit from the cost advantage that comes from using sulfur cathode over nickel and cobalt cathode of Li-ion batteries.

By End Use, Aerospace segment dominates the Lithium-Sulfur Battery Market

Lithium-sulfur batteries were most preferred in the Aerospace end-use application segment accounting for a revenue market share of 31.60% in 2025. This high preference level can be attributed to the perfect fit of the performance attributes of lithium-sulfur batteries in relation to the needs of aerospace systems that require weight reduction. In aerospace systems, the use of lighter lithium-sulfur batteries as opposed to lithium-ion batteries while maintaining similar capacity and ranges is an attractive concept.

In addition to having the highest anticipated market growth rates, the Automotive end-use application segment benefits greatly from the development in technology since lithium-sulfur batteries become more competitive in terms of their cycle lives and temperature performances according to the standards specified by automotive manufacturers. Another end-use application with tremendous growth opportunities includes Energy & Utilities which comprises of power grids and renewable energy buffers.

Lithium-Sulfur Battery Market Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

91% |

|

Europe |

Germany |

35% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

50% |

North America Lithium-Sulfur Battery Market Insights

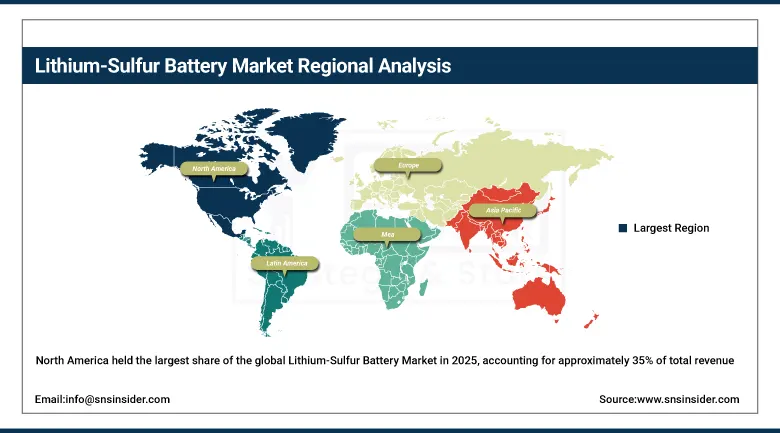

North America held the largest share of the global Lithium-Sulfur Battery Market in 2025, accounting for approximately 35% of total revenue. The United States is overwhelmingly the dominant contributor within the region, driven by a combination of government-backed research programs, active private sector venture investment, and strong demand pull from the defense and aerospace sectors. The U.S. Department of Energy's Battery500 Consortium, DARPA-funded advanced energy programs, and service branch research initiatives have collectively built a substantive national capability in lithium-sulfur battery research over the past decade, creating a pipeline of technologies now entering early commercial deployment.

Defense contractors including Lockheed Martin and Northrop Grumman are actively evaluating lithium-sulfur solutions for unmanned systems, further supporting near-term commercial demand. The region is expected to retain its global market leadership through 2035 while Asia Pacific gains share through high-volume manufacturing scale-up.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Lithium-Sulfur Battery Market Insights

The Asia Pacific region is estimated to witness the fastest CAGR in the Global Lithium-Sulfur Battery Market during the forecast period from 2026 to 2035 on account of its established battery manufacturing capabilities, vast electric vehicle market, and substantial government backing in advanced battery research. As per the report, China constitutes the largest national market in the Asia Pacific region with respect to market revenue, contributing approximately 48% to the region's revenue in 2025. Major players like CATL and BYD from China are working on developing lithium-sulfur batteries within their next-gen battery strategies, while LG Energy Solutions of South Korea has plans to establish pilot production facilities between 2026 and 2028.

Countries such as Japan and South Korea offer significant research efforts into the technology, and some of the larger organizations in these countries working on lithium-sulfur projects include Samsung SDI and Panasonic, among others. The region's battery technology leadership through governmental policies ensures that R&D in the technology continues despite unfavorable commercial prospects for the product. The rise of electric aviation and advanced drone technology in China is expected to be a source of significant demand for lithium-sulfur cells.

Europe Lithium-Sulfur Battery Market Insights

Europe represents about 30% of global lithium-sulfur batteries market revenues by 2025 and features the presence of research institutions, battery industry growth through initiatives like the European Battery Alliance, and supportive policies aimed at developing advanced energy storage solutions in line with the European clean energy strategy. Germany is the leading country market in Europe, contributing some 35% of regional revenues, owing to the dominant position of the country's automotive industry, substantial investments into battery research made by Fraunhofer and Helmholtz research organizations, and cooperation programs with major OEM companies like BMW and Volkswagen.

One of the leading developers of lithium-sulfur technology in Europe is OXIS Energy, which now operates as Johnson Matthey Battery Systems. Lithium-sulfur battery solutions are being researched in the European aviation market, with Airbus' programs focusing on evaluating alternative lithium-sulfur batteries for use in hybrid or purely electric air vehicles. EU financing through Horizon Europe and battery competitiveness programs in member states supports Europe's ambitions to become capable of independent lithium-sulfur batteries manufacturing outside of Asia.

Middle East & Africa and Latin America Lithium-Sulfur Battery Market Insights

The Middle East & Africa and Latin American regions hold a comparatively smaller but increasing share of the Global Lithium-Sulfur Battery Market as well. This comes about due to increased government and industry investments aimed at adopting advanced technology in their infrastructure systems. In the Middle East region, activities mainly occur in countries such as the UAE and Saudi Arabia due to sovereign wealth funds and national energy corporations becoming interested in the development and application of advanced batteries. The near-term defense procurement interests of countries within the Gulf states in regard to UAVs and other unmanned systems may lead to an increase in the application of the technology.

Activities in the Latin American region occur in only one country, Brazil. This occurs mainly as research activities in institutions and development of early stage clean energy infrastructure. Overall, the two regions do not contribute significantly to the Lithium-Sulfur Battery Market currently compared to North America, Europe, and Asia Pacific. However, as time goes on, these regions may become significant contributors in the future, especially when more awareness is created concerning this advanced technology.

Growth Drivers: High energy density and lightweight design meeting critical performance requirements in aerospace, defense, and electric mobility

The foundational growth driver for the Lithium-Sulfur Battery Market is the technology's exceptional theoretical energy density, which sits significantly above that of conventional lithium-ion batteries at comparable weight. For applications where the mass of the power source directly constrains system performance, such as long-endurance drones, electric aircraft, lightweight electric vehicles, and portable soldier systems, the ability to store more energy per kilogram is a decisive design advantage. This performance characteristic creates a clear and durable commercial rationale for continued investment in lithium-sulfur development even while the technology remains in the early stages of commercialization.

The abundance and low cost of sulfur as a raw material provides a secondary but meaningful advantage, offering the prospect of battery packs that are both lighter and potentially cheaper than cobalt-dependent lithium-ion alternatives at scale. Government and corporate decarbonization commitments are accelerating the urgency of developing higher-performance energy storage solutions, creating a favorable policy and investment environment for lithium-sulfur technology developers to attract capital and advance their commercialization roadmaps. These structural demand drivers are expected to sustain the market's high growth trajectory throughout the 2026 to 2035 period.

Restraints: Cycle life limitations and polysulfide shuttle effect constraining commercial deployment timelines

The main hurdle to greater lithium-sulfur battery utilization lies in its present inability to match up with the cycle life capability compared to other more mature lithium-ion battery technologies. This arises due to the polysulfide shuttle effect where the soluble polysulfides produced as part of the electrochemical reactions are able to move around from cathode to anode during cycling, resulting in gradual degradation of the active materials and subsequent fading of the batteries' capacity. Although substantial advancements have been made scientifically with regards to the mitigation of this issue via optimization of the batteries' cathode design, electrolyte chemistry and separation membranes, commercially relevant cycle life figures for the automotive industry and stationary energy storage applications have not yet been shown convincingly. This results in a current concentration of commercialization efforts in areas requiring fewer cycles like single-use military and aerospace deployments and R&D testing applications. Commercial utilization of the battery system in the larger consumer and grid energy storage market segments will only be possible when the cycle life issues are adequately addressed.

Opportunities: Expanding electric aviation and UAV programs creating high-value near-term commercial deployment pathways

Electrified aviation, ranging from commercial short-haul electric airplanes to the booming eVTOL sector, is among the commercially most viable deployment vectors for lithium-sulfur batteries. The electrified aviation sector is especially weight-sensitive because each additional kilogram of battery weight decreases cargo capacity and flight range, and the rationale behind deploying lithium-sulfur over lithium-ion becomes evident at only moderate gains in performance. More than 18 eVTOL manufacturers worldwide were estimated to have been assessing lithium-sulfur batteries in the last couple of years, and more such programs are anticipated to enter the development phase as prototypes and certification approaches are advanced. UAVs and drones offer an even more imminent opportunity due to the less demanding cycle life and the better range-to-weight ratio for energy-dense batteries. Defense agencies in the United States, Europe, and Asia purchase UAVs and drones in large numbers, and they are prepared to pay a premium price for performance enhancement.

Recent Developments:

-

2026: Multiple lithium-sulfur battery developers announced progress toward pilot-scale cell production, with several programs reporting improved cycle stability through advanced carbon-sulfur composite cathode architectures and novel electrolyte systems designed to suppress the polysulfide shuttle effect.

-

2025 (March): Sion Power announced significant advances in its Licerion lithium-sulfur battery platform, reporting energy densities exceeding 500 Wh/kg and targeting commercial supply agreements with electric vehicle and aerospace customers for evaluation programs.

-

2025 (March): Giner, Inc. reported continued progress in its lithium-sulfur battery research program focused on enhancing cycle life and energy density specifically for electric vehicle and grid storage applications, backed by U.S. Department of Energy funding.

Lithium-Sulfur Battery Companies are:

-

OXIS Energy

-

Lyten, Inc.

-

PolyPlus Battery Company

-

Gelion Technologies PLC

-

LG Energy Solution

-

Samsung SDI Co., Ltd.

-

Panasonic Energy Co., Ltd.

-

Amprius Technologies

-

CATL (Contemporary Amperex Technology)

-

BYD Co., Ltd.

-

Giner, Inc.

-

Zeta Energy LLC

-

Li-S Energy Limited

Lithium-Sulfur Battery Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 59.39 Million |

| Market Size by 2035 | USD 1201.27 Million |

| CAGR | CAGR of 35.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (High Energy Density, Low Energy Density) • By Capacity (Below 500 mAh, 500–1000 mAh, Above 1000 mAh) • By Application (Aviation & UAVs, Automotive & EVs, Consumer Electronics, Energy Storage Systems, Defense & Military, Others) • By End Use (Aerospace, Automotive, Electronics, Energy & Utilities, Defense) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sion Power Corporation, OXIS Energy, Lyten, Inc., PolyPlus Battery Company, NexTech Batteries, Gelion Technologies PLC, LG Energy Solution, Samsung SDI Co., Ltd., Panasonic Energy Co., Ltd., Amprius Technologies, CATL (Contemporary Amperex Technology), BYD Co., Ltd., Giner, Inc., Zeta Energy LLC, Li-S Energy Limited. |

Frequently Asked Questions

North America dominated the Lithium-Sulfur Battery Market in 2025, accounting for approximately 35% of global revenue share, with the United States as the primary contributor.

The High Energy Density segment dominated the Lithium-Sulfur Battery Market in 2025, accounting for 73.60% of total market share.

The major growth factors are the high energy density and lightweight design of lithium-sulfur batteries, increasing demand for sustainable energy storage solutions, and strong investment from aerospace, defense, and electric vehicle sectors requiring superior power-to-weight performance.

The Lithium-Sulfur Battery Market was valued at USD 59.39 Million in 2025.

The Lithium-Sulfur Battery Market is expected to grow at a CAGR of 35.08% from 2026 to 2035.

Get in Touch