Laser Sensor Market Report Scope & Overview:

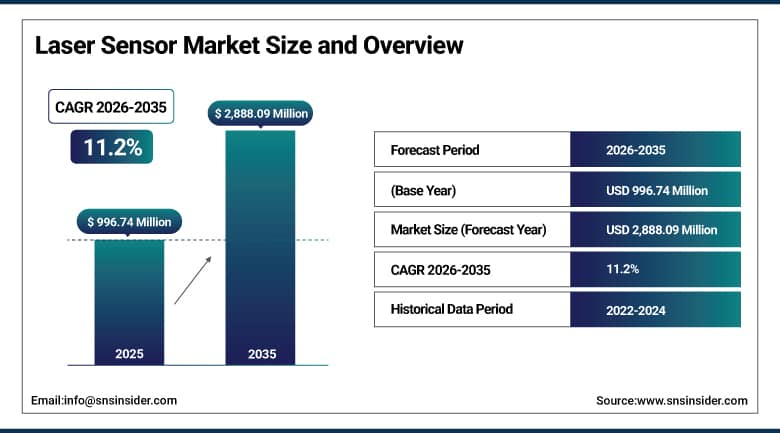

The Laser Sensor Market size was valued at USD 996.74 Million in 2025 and is expected to reach USD 2,888.09 Million by 2035, growing at a CAGR of 11.2% from 2026–2035.

The global laser sensor market is growing at a sustained and commercially significant pace. Laser sensors are precision measurement and detection devices that utilize coherent monochromatic laser light for non-contact distance measurement, displacement monitoring, object detection, presence sensing, and dimensional measurement across industrial, automotive, medical, and consumer applications. The market is growing rapidly driven by increasing adoption in industrial automation, automotive, and healthcare for precision measurement, quality control, and surveillance. Advancements in 3D laser scanning, fiber optic sensors, and AI-integrated IoT-enabled solutions are enhancing efficiency across industries, while rising demand for non-contact measurement systems and Industry 4.0 investments further boost growth.

In October 2023, Leica Geosystems unveiled the BLK2GO PULSE, a revolutionary first-person laser scanner that simplifies the process of capturing accurate and detailed full-color 3D point clouds. The wearable scanning system enables walk-through facility capture at 420,000 points per second whose continuous scan during normal facility walkthrough eliminates the setup time that tripod-mounted scanner alternatives require, creating workflow efficiency that sustains premium specification in architectural, construction, and facility management scanning applications.

Market Size and Forecast:

-

Market Size in 2026E: USD 1,108.38 Million

-

Market Size by 2035: USD 2,888.09 Million

-

CAGR: 11.2% from 2026 to 2035

-

Fastest Growing Region: North America (11.5% CAGR)

-

Largest Region: Asia Pacific (~40%)

To Get More Information On Laser Sensor Market - Request Free Sample Report

Laser Sensor Market Trends:

-

AI-integrated laser sensor systems are enabling automated inspection, defect detection, and quality control by combining real-time sensing data with advanced machine learning algorithms

-

Ongoing miniaturization of laser sensors is expanding adoption in compact applications such as medical devices, smartphones, wearable electronics, and small robotic systems

-

Growing deployment of LiDAR technologies in autonomous vehicles is driving significant demand for laser sensors used in navigation, obstacle detection, and environmental mapping

-

Integration of IO-Link connectivity is enhancing laser sensor functionality by enabling real-time data exchange, predictive maintenance, and Industry 4.0 automation capabilities

-

Development of long-range laser sensing technologies is supporting advanced applications in autonomous mobility, drones, industrial inspection, and large-scale monitoring systems requiring high-precision distance measurement over extended ranges

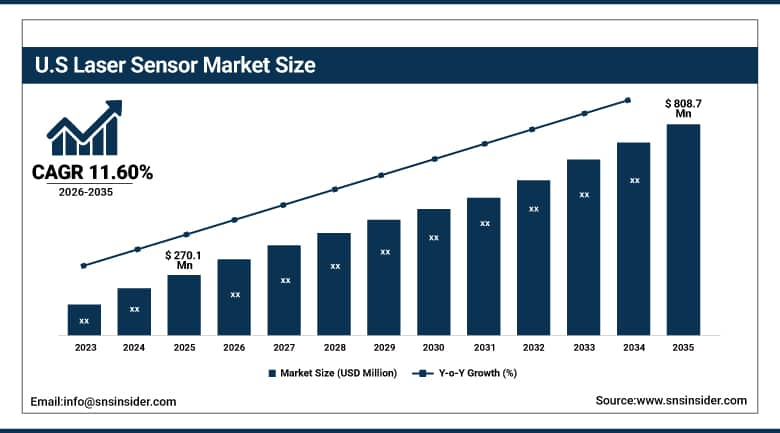

U.S. Laser Sensor Market Size Outlook:

The U.S. Laser Sensor Market is estimated to be USD 270.1 Million in 2025 and is projected to reach USD 808.7 Million by 2035, growing at a CAGR of 11.60% during 2026–2035.

The U.S. Laser Sensor Market is the most commercially significant national market within the fastest-growing North American region at 11.5% CAGR. SICK AG’s North American operations, Keyence Corporation’s U.S. commercial presence, Rockwell Automation’s industrial sensing portfolio, and Leica Geosystems’ U.S. operations collectively serve the domestic industrial, automotive, and healthcare laser sensor markets. The U.S.’s advanced manufacturing sector’s Industry 4.0 investment, the autonomous vehicle industry’s LiDAR adoption, and the AI-enabled healthcare diagnostics’ imaging sensor procurement create the most commercially diverse national laser sensor application deployment globally.

SICK AG launched its new deTec4 Core safety laser scanner family in 2024 with enhanced resolution and response time for collaborative robot workspace protection, providing safe human-robot collaboration monitoring at speeds up to 10 cm/s for robot approach detection. The product’s certified safety function integration creates compliant human-robot collaboration infrastructure whose safety performance creates institutional adoption motivation in manufacturing operations where worker safety and robot deployment coexist.

Laser Sensor Market Segment Analysis:

-

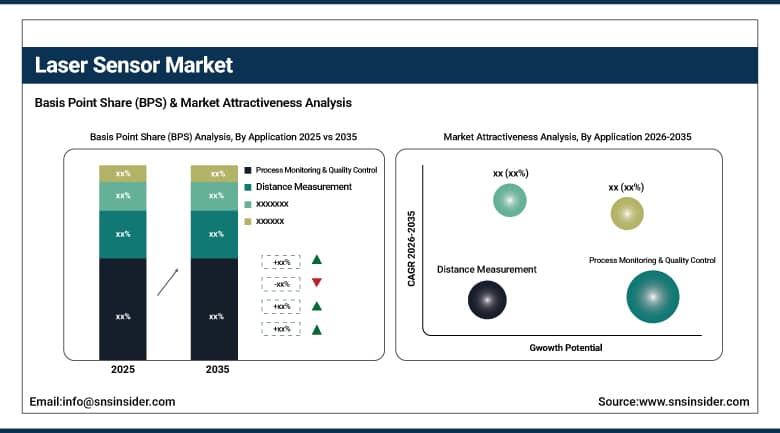

By Application, the Process Monitoring & Quality Control segment dominated the Laser Sensor Market in 2025, while the Distance Measurement segment is the fastest growing.

-

By Type, the Laser Displacement Sensors segment dominated the Laser Sensor Market with approximately 35% share in 2025, while the Laser Scanners/LiDAR segment is the fastest growing.

-

By End User, the Industrial Automation & Manufacturing segment dominated the Laser Sensor Market with approximately 42% share in 2025, while the Automotive segment is the fastest growing.

By Application, process monitoring dominates, distance measurement grows fastest

Process monitoring and quality control retained the dominant application position in the laser sensor market in 2025. The manufacturing industry’s systematic adoption of non-contact in-line measurement for dimensional verification, surface defect detection, and assembly confirmation creates consistent laser sensor procurement whose quality control ROI measurement in defect escape prevention and scrap reduction sustains investment. Automotive body panel gap and flush measurement, semiconductor wafer thickness control, PCB component presence verification, and food packaging fill level detection collectively represent process monitoring and quality control applications whose combined commercial scale creates the most commercially significant laser sensor application category.

Distance measurement is the fastest-growing application because autonomous vehicle LiDAR’s 3D environmental mapping, drone obstacle avoidance and landing zone detection, and construction’s BIM point cloud capture create new volume application categories that industrial quality control inspection cannot match by unit growth rate. Each autonomous vehicle whose sensor suite includes multiple LiDAR units creates laser scanner procurement whose aggregate across the growing autonomous fleet creates commercial scale. Construction’s progressive BIM adoption creating 3D site documentation procurement sustains distance measurement sensor growth beyond autonomous vehicle adoption alone.

By Type, displacement sensors dominate, LiDAR grows fastest

Laser displacement sensors retained the dominant type position with approximately 35% of the laser sensor market in 2025. Displacement sensor’s commercial primacy reflects its role as the standard precision measurement device for industrial applications requiring sub-micron accuracy in position, thickness, gap, and dimensional measurement. Keyence’s LK, LJ, and IL series, SICK’s OD series, and Micro-Epsilon’s optoNCDT product lines collectively demonstrate the commercial breadth of laser displacement sensor’s specification across semiconductor, electronics, automotive, and precision manufacturing. The semiconductor industry’s extraordinary capital investment creates above-average displacement sensor procurement whose measurement precision requirement creates premium per-unit commercial value.

Laser scanners and LiDAR are the fastest-growing type because autonomous vehicle, industrial robot guidance, and facility management scanning applications create demand whose unit count expansion substantially exceeds displacement sensor replacement cycles. Each new autonomous vehicle model that specifies LiDAR creates above-average scanner procurement, and each new robot installation that requires 3D environment awareness creates laser scanner demand. Velodyne, Ouster, Luminar, and Innoviz’s automotive LiDAR programmes collectively demonstrate the commercial investment whose production ramp-up creates extraordinary scanner market growth.

By End User, industrial automation dominates, automotive grows fastest

Industrial automation and manufacturing retained the dominant end-user position with approximately 42% of the laser sensor market in 2025. The manufacturing sector’s systematic quality control investment, precision assembly verification requirement, and predictive maintenance sensing creates consistent laser sensor procurement whose ROI measurement in defect prevention and production efficiency sustains investment across economic cycles. Semiconductor fabrication’s nanometer-precision measurement requirement, electronics assembly’s component placement verification, and automotive body manufacturing’s dimensional inspection collectively create industrial automation’s commercial leadership.

Automotive is the fastest-growing end user because ADAS object detection, autonomous driving LiDAR’s 3D environment mapping, and advanced manufacturing’s AI quality control create multiple simultaneous above-average growth vectors within a single industry vertical. Each new vehicle model’s ADAS feature expansion creates laser sensor procurement whose aggregate across global vehicle production creates commercial scale. Each automotive OEM’s Level 3+ autonomous driving programme creates LiDAR procurement whose per-vehicle sensor suite value substantially exceeds conventional automotive sensor alternatives.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

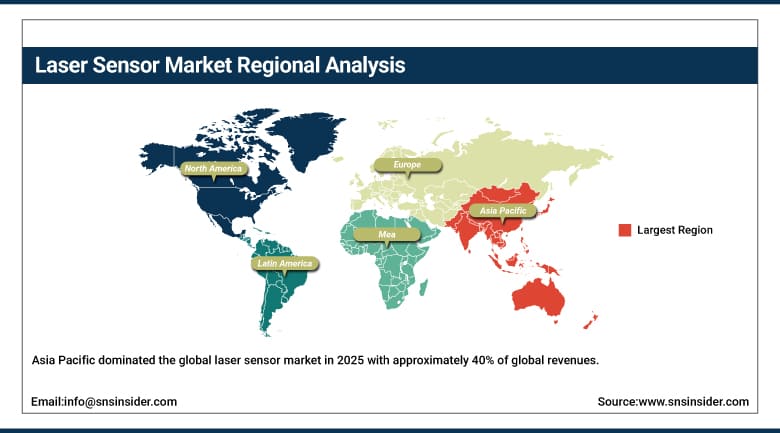

Asia Pacific Laser Sensor Market Insights

Asia Pacific dominated the global laser sensor market in 2025 with approximately 40% of global revenues. China accounts for approximately 44.8% of Asia Pacific revenues through its world-class electronics and semiconductor manufacturing requiring precision measurement, the automotive industry’s quality control investment, and the industrial automation sector’s laser sensor adoption. Companies including Keyence and Panasonic are actively expanding laser sensor solutions in the Asia Pacific region.

Japan’s advanced manufacturing sector, South Korea’s semiconductor and electronics industry, and India’s rapidly growing manufacturing sector create significant secondary markets whose combined procurement sustains Asia Pacific’s commercial dominance.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Laser Sensor Market Insights

North America is the fastest-growing regional laser sensor market with 11.5% CAGR, driven by autonomous vehicle LiDAR adoption, AI-enabled healthcare solutions, and strong investments in smart factories and industrial automation. The United States accounts for approximately 87.4% of North American revenues through SICK AG, Keyence, Rockwell Automation, and Leica Geosystems’ commercial operations.

Canada contributes approximately 12.6% of North American revenues through its manufacturing sector’s quality control investment, the automotive industry’s precision measurement adoption, and the resource sector’s 3D scanning application.

Europe Laser Sensor Market Insights

Europe is a technically sophisticated laser sensor market where SICK AG’s German headquarters, TRUMPF’s laser technology leadership, and the manufacturing industry’s precision measurement culture create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its world-class automotive and precision engineering sector’s laser sensor adoption, SICK AG’s domestic commercial presence, and the industrial automation sector’s Industry 4.0 investment.

France, Italy, and Switzerland are significant secondary markets where aerospace, precision manufacturing, and pharmaceutical quality control create consistent laser sensor procurement.

MEA & Latin America Laser Sensor Market Insights

UAE leads MEA revenues at approximately 38.4% through its advanced manufacturing investment, the smart infrastructure monitoring programme, and the oil and gas sector’s precision measurement adoption. Brazil leads Latin American revenues at approximately 44.2% through its automotive manufacturing sector’s quality control investment, the industrial automation adoption, and the growing electronics sector’s laser sensor procurement.

Market Dynamics:

Growth Drivers: Industrial automation and Industry 4.0 investment and autonomous vehicle LiDAR adoption

Increasing adoption of industrial automation, smart manufacturing, and AI-powered precision measurement technologies is SNS Insider’s confirmed primary growth driver. Each new industrial automation programme that specifies non-contact laser measurement for quality control, presence detection, or dimensional verification creates laser sensor procurement whose ROI measurement in defect prevention and production efficiency sustains investment. The industry 4.0 investment’s systematic sensor density increase creates multiple laser sensor procurement per production line that compounds with manufacturing sector’s continuous automation investment.

Autonomous vehicle LiDAR adoption is creating the most commercially transformative near-term volume demand driver whose per-vehicle sensor suite investment creates commercial scale at global vehicle production volumes. Each new autonomous vehicle programme’s production ramp creates LiDAR procurement whose aggregate compounds with autonomous vehicle adoption’s extraordinary pace. The U.S.’s autonomous vehicle investment, China’s NEV programme’s sensor mandate, and European automotive OEM’s Level 3 deployment collectively create structured LiDAR procurement that sustains above-market laser scanner growth.

Restraints: High initial cost and integration complexity for SMEs

Laser sensor’s higher initial cost relative to conventional inductive, capacitive, and optical proximity sensor alternatives creates adoption barriers for small and medium enterprises whose investment economics create ROI justification challenges. Each SME manufacturer whose production volume creates insufficient measurement ROI to justify premium laser sensor investment creates specification preference for lower-cost alternatives that moderates laser sensor market growth below the addressable precision measurement opportunity.

Integration complexity in brownfield industrial environments whose legacy control systems, communication protocols, and physical installation constraints create deployment challenges that reduce adoption below the technically optimal precision measurement deployment density.

Opportunities: AI-integrated smart laser sensor systems and healthcare medical imaging laser adoption

AI-integrated smart laser sensor systems combining point cloud generation with real-time machine learning analysis represent the most commercially innovative near-term market development whose autonomous defect detection and dimensional analysis capability creates quality control automation that labor-intensive manual inspection cannot match equivalently. Each AI-integrated laser quality system that demonstrates measurable inspection accuracy improvement creates adoption momentum.

Healthcare medical laser sensor adoption for non-contact vital sign monitoring, surgical navigation, and diagnostic imaging creates premium procurement whose medical grade specification sustains above-industrial commercial value. Each FDA-cleared medical laser sensor application creates clinical adoption whose evidence base sustains institutional procurement.

Recent Developments:

-

2023: Leica Geosystems unveiled the BLK2GO PULSE first-person laser scanner in October 2023 that simplifies full-color 3D point cloud capture at 420,000 points per second during normal facility walkthrough, eliminating tripod setup requirements for architectural, construction, and facility management scanning.

-

2024: SICK AG launched its new deTec4 Core safety laser scanner family in 2024 with enhanced resolution and response time for collaborative robot workspace protection, providing certified human-robot collaboration safety monitoring for industrial manufacturing applications.

-

2024: Keyence Corporation launched its new LJ-X8000 series 3D laser displacement scanner in 2024 with 4x faster scan speed and enhanced high-speed 3D profiling for semiconductor, electronics, and precision manufacturing inline quality inspection applications.

Laser Sensor Companies are:

-

SICK AG

-

Micro-Epsilon Messtechnik GmbH & Co. KG

-

Pepperl+Fuchs SE

-

Omron Corporation

-

Baumer Group

-

Ifm Electronic GmbH

-

Panasonic Corporation (Industrial Automation)

-

Cognex Corporation

-

Leuze Electronic GmbH + Co. KG

-

Leica Geosystems AG (Hexagon)

-

Datalogic S.p.A.

-

Velodyne Lidar Inc. (Ouster)

-

Luminar Technologies Inc.

-

FANUC Corporation

-

Rockwell Automation Inc.

-

Balluff GmbH

-

Turck Group

-

Wenglor sensoric GmbH

Laser Sensor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 996.74 Million |

| Market Size by 2035 | USD 2,888.09 Million |

| CAGR | CAGR of 11.2% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Laser Displacement Sensors, Laser Photoelectric Sensors, Laser Distance/Time-of-Flight Sensors, Laser Scanners/LiDAR, Laser Barcode Scanners, Others) • by Application (Process Monitoring & Quality Control, Distance Measurement, Safety & Security/Surveillance, Motion & Guidance, Manufacturing Plant Management, Others) • by End User (Industrial Automation & Manufacturing, Automotive, Consumer Electronics, Healthcare & Medical, Aerospace & Defense, Food & Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Keyence Corporation, SICK AG, Micro-Epsilon Messtechnik GmbH & Co. KG, Pepperl+Fuchs SE, Omron Corporation, Banner Engineering Corp., Baumer Group, Ifm Electronic GmbH, Panasonic Corporation (Industrial Automation), Cognex Corporation, Leuze Electronic GmbH + Co. KG, Leica Geosystems AG (Hexagon), Datalogic S.p.A., Velodyne Lidar Inc. (Ouster), Luminar Technologies Inc., FANUC Corporation, Rockwell Automation Inc., Balluff GmbH, Turck Group, Wenglor sensoric GmbH |

Frequently Asked Questions

The Laser Sensor Market is expected to grow at a CAGR of 11.2% from 2026 to 2035.

The Laser Sensor Market was valued at USD 996.74 Million in 2025.

Increasing adoption of industrial automation, smart manufacturing, and AI-powered precision measurement technologies across industries, and rising demand for non-contact measurement systems from Industry 4.0 investments and autonomous vehicle LiDAR adoption.

Process Monitoring & Quality Control dominated the Laser Sensor Market in 2025 as confirmed by SNS Insider, while Distance Measurement is the fastest growing.

Asia Pacific dominated the Laser Sensor Market in 2025 with approximately 40% of global revenues, while North America is the fastest-growing region with an 11.5% CAGR.

Get in Touch