Livestock Insurance Market Report Scope & Overview:

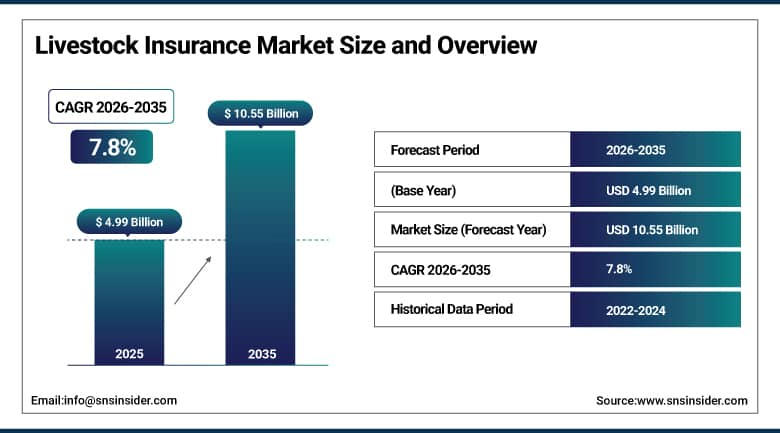

The Livestock Insurance Market was valued at USD 4.99 Billion in 2025 and is expected to reach USD 10.55 Billion by 2035, growing at a CAGR of 7.8% from 2026 to 2035.

The Livestock Insurance Market is expected to grow due to the rise in the economic value of livestock and the rising need to mitigate risks that result in loss of money to farmers due to outbreaks of disease, accidents, natural disasters, thefts, and death of livestock. The increase in commercial livestock farming especially in the areas of cattle, poultry, swine, and dairy farming has led to an increased need for livestock risk management services in order to ensure protection of farm income and business.

Furthermore, there is an increase in concern with regard to climate changes, weather conditions, and outbreak of infections that can affect animals. Technological advancements in livestock monitoring, use of satellite data and risk evaluation through data analysis have enabled insurers to offer customized coverage plans. Increase in investments in advanced livestock husbandry and awareness of the advantages of financial protection has boosted the growth of the global livestock insurance market.

Market Size and Forecast:

-

Market Size in 2026E: USD 5.38 Billion

-

Market Size by 2035: USD 10.55 Billion

-

CAGR: 7.8% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

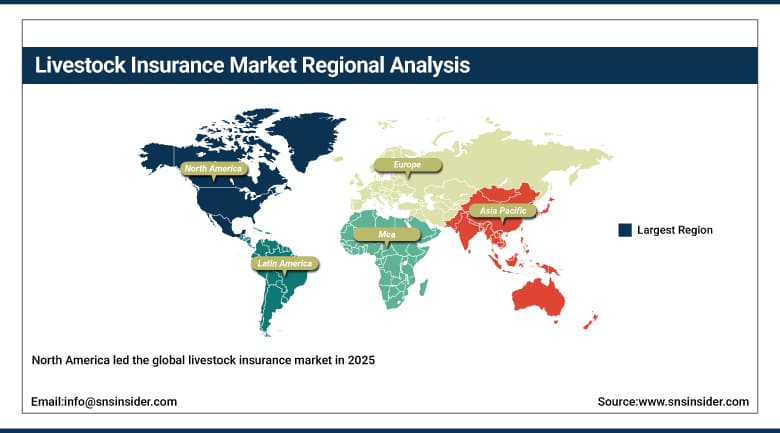

Largest Region: North America

To Get More Information On Livestock Insurance Market - Request Free Sample Report

Livestock Insurance Market Trends:

-

Index-based livestock insurance is gaining adoption, using satellite and weather data to enable faster and more accessible payouts for farmers.

-

AI, remote sensing, drones, and livestock tracking technologies are improving underwriting accuracy and risk assessment.

-

Demand for epidemic and disease outbreak coverage is increasing due to concerns over avian influenza, foot-and-mouth disease, and other livestock diseases.

-

Government-private partnership programs and premium subsidy schemes are expanding livestock insurance penetration in emerging markets.

-

Parametric insurance products are growing in popularity by offering automated, data-triggered payouts and faster claim settlements

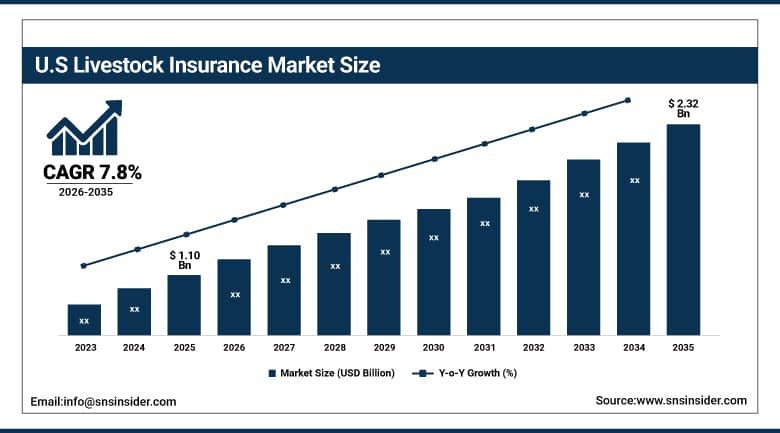

U.S. Livestock Insurance Market Outlook:

The U.S. Livestock Insurance Market was valued at approximately USD 1.10 Billion in 2025 and is expected to reach approximately USD 2.32 Billion by 2035, growing at a CAGR of approximately 7.8%.

The United States is home to the world's most commercially developed livestock insurance market, which represents roughly 22% of the total world's market share by combining the factors of large commercial livestock herds, risk management knowledge and awareness, and the USDA Risk Management Agency's comprehensive Federal Crop and Livestock Insurance Programs. Livestock Risk Protection and Livestock Gross Margin programs offer revenue insurance on cattle, hogs, and dairy operations at subsidized premiums, ensuring the broad acceptance of commercial farmers. The enormous volumes of cattle, poultry, and pork in the US ensure premium volumes that make up global benchmarks for commercial livestock insurance.

In 2024, HPAI A(H5) avian influenza affected a significant number of U.S. poultry farms, generating substantial indemnity claims under federal livestock insurance programmes and demonstrating the critical role of government-backed coverage in enabling rapid herd restocking and farm operation recovery following catastrophic disease outbreak events.

Livestock Insurance Market Segment Analysis:

-

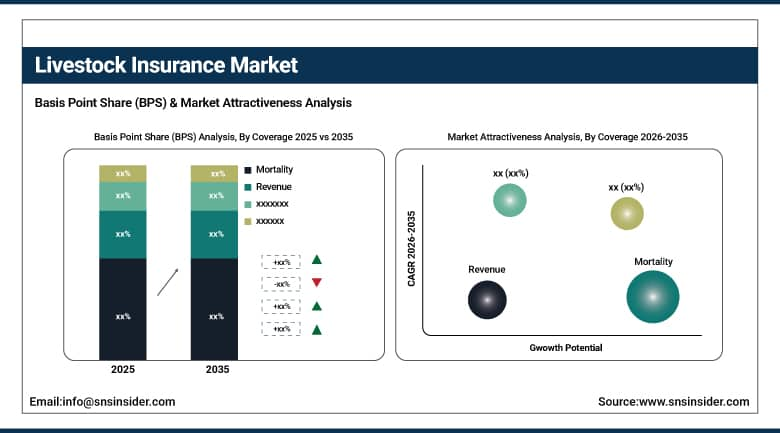

By Coverage, the Mortality segment dominated the livestock insurance market with approximately 39% share in 2025, while the Revenue segment is the fastest growing as commercial livestock producers increasingly seek comprehensive income protection that covers price volatility and production shortfalls beyond mortality events.

-

By Animal Type, the Bovine segment dominated the livestock insurance market with the largest share in 2025, while the Poultry segment is the fastest growing due to the HPAI avian influenza epidemic's devastating impact on poultry operations globally.

-

By Distribution Channel, the Agency/Broker segment dominated the livestock insurance market with the largest share in 2025, while the Bancassurance segment is the fastest growing as agricultural lending institutions bundle livestock insurance with farm financing products.

By Coverage, mortality dominates, revenue grows fastest:

The mortality cover maintained its place as the major coverage type with a 39% market share for livestock insurance in 2025. The cornerstone of insurance coverage in terms of the livestock market is a product that covers the full replacement value of the livestock against the risk of their death due to accidents, diseases, and natural calamities which have financial losses of an irreversible nature.

The revenue cover is the fastest-growing cover type since commercial livestock operators understand that protection against price changes and the increase in production costs requires additional protection compared to the mortality-only cover. Every cattle feeder, who depends on the difference between the cost of buying cattle and selling fed cattle, needs the livestock gross margin coverage.

By Animal Type, bovine dominates, poultry grows fastest

The bovine animal type retained dominance in the livestock insurance market in 2025. Bovines have a high individual value of each animal, which makes commercial breeding herds and feed lot bovine animals valuable enough to warrant comprehensive insurance, while the long production period of bovine livestock of 18 to 24 months creates constant financial exposure to which commercial livestock operators consistently hedge their losses through insurance.

The animal type with the highest CAGR is the poultry animal type due to the continuous destructive effect of the HPAI (highly pathogenic avian influenza) avian influenza epidemic on commercial poultry operations throughout the world, making commercial operators seek to hedge their losses by purchasing insurance. Every time an HPAI avian influenza outbreak occurs and wipes out millions of chickens or turkeys in the matter of days after the first detection of the disease.

By Distribution Channel, agency/broker dominates, bancassurance grows fastest

The agent and broker distribution channels continued to maintain the dominant status of the distribution channels for livestock insurance in 2025. Agricultural insurance brokers and specialists in farm insurance are able to provide the technical expertise regarding livestock evaluation, the evaluation of farm risks, and coverage development which is required due to the complexity of the underwriting process associated with the livestock insurance. Every specialist who has knowledge of agronomy, livestock production, and insurance products provides the quality of insurance coverage placement which cannot be provided by direct-channel distribution serving general commercial insurance consumers.

The fastest-growing distribution channel is bancassurance since the insurance distribution of agricultural lending organizations embedded into the credit creation process generates the efficiency of placement of insurance at the time of maximum motivation of the commercial farmers. Every farm which obtains livestock finance or credit becomes the subject of bancassurance distribution with the minimal effort of the credit organization which needs the insurance protection of its exposures.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

80.2% |

|

Europe |

Germany |

24.3% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

South Africa |

30.1% |

|

Latin America |

Brazil |

43.8% |

North America Livestock Insurance Market Insights

North America led the global livestock insurance market in 2025 due to the commercial extent of the United States’ livestock industry along with the most developed government backed livestock insurance infrastructure in the world. United States is responsible for about 80.2% of the North American revenue share from its USDA Risk Management Agency’s federally backed livestock insurance programs which include Livestock Risk Protection, Livestock Gross Margin and Livestock Forage Disaster Program which facilitates structured buying among the commercial cattle, hogs and dairy farms.

Canada is responsible for about 19.8% of the North American revenue share from its AgriInsurance provincial programs, Canadian Agricultural Partnership risk management program and commercial livestock insurance for the cattle, hogs and poultry sectors.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Livestock Insurance Market Insights

Europe is another important livestock insurance market that derives from EU Common Agricultural Policy risk management subsidies, national co-insurance programs, and increased livestock losses as a result of the climatic risk that has created structured insurance adoption. In Europe, Germany forms the largest insurance market at around 24.3% in revenues, with its huge dairy and beef cattle farming industry, high level of disease-risk swine and poultry farming, and its agricultural insurers like Vereinigte Hagelversicherung and AXA Agri.

France, Netherlands, Spain, and Denmark are other important livestock insurance markets in Europe that derive from intensive livestock farming practices, EU agricultural subsidies co-insurance requirement programs, and increasing awareness about climate risk among professional farmers.

Asia Pacific Livestock Insurance Market Insights

The Asia Pacific is currently the fastest-growing regional market for livestock insurance thanks to the mandatory increase in the livestock insurance program by the Chinese government, the rise of the national livestock insurance scheme in India, and increasing concern about animal losses due to climate change in Southeast Asian livestock farming systems. The country constitutes nearly 48.6% of the revenues made in Asia Pacific owing to its livestock insurance subsidy program implemented by the central government, which helps foster structured adoption of insurance programs in commercial and smallholder swine, cattle, and poultry farming.

India is the most commercially vibrant emerging market in Asia Pacific owing to its national livestock mission insurance component, increased risk management investment in its commercial dairy and poultry industry, and agricultural risk management policy focus by the government.

MEA & Latin America Livestock Insurance Market Insights

Leading the way in MEA revenues is South Africa, which generates about 30.1%, thanks to its commercial cattle and sheep production, growing awareness of losses due to drought and extensive agricultural insurance portfolio. The KLIP program of Kenya covers 90,000 cattle per year, showing how indexed insurance can be scalable in East Africa. Leading the way in Latin American revenues is Brazil, which generates about 43.8% revenues, thanks to its leading commercial beef cattle production, government subsidization of agricultural insurance and swine and poultry productions.

Market Dynamics:

Growth Drivers: Climate change-driven extreme weather events increasing livestock loss frequency and government subsidy programmes expanding insurance accessibility

Climate change is the most structural growth driver in the livestock insurance market by increasing the frequency of losses in the weather-related perils comprising droughts, floods, heatwaves, and hurricanes that altogether destroy livestock businesses across the world. The fact that 93% of days between January and September 2024 have been considered to be extreme weather events, resulting in nearly 9,457 livestock fatalities and heavy damage to crops and property, proves that climate change is the main factor of agricultural risks that need insurance products.

Subsidized government programs and mandatory insurance programs lead to the creation of non-discretionary procurement of livestock insurance that extends the insurance market to include farmers who do not have an intention to buy commercial livestock insurance on their own. Livestock insurance products provided by USDA RMA, subsidized livestock insurance products in China, national livestock mission insurance program in India, and risk management tools from the EU CAP all together create a structure for procurement.

Restraints: High premium cost limiting smallholder farmer adoption and complex claims assessment creating settlement delays

Higher premiums are the biggest business impediment in the growth of livestock insurance market penetration, especially in developing countries, where small-scale farmers whose livestock make up their main source of production and income cannot afford high-cost premiums of commercial insurance products. The rise in climate risks in drought- and flood-prone areas causes actuarially rational premium rises, which lower even more the affordability of insurance products to those farmer communities that need them the most.

The complex nature of assessing claims for traditional indemnity livestock insurance leads to longer claims settlement processes, thus undermining the willingness of farmers to pay premiums for insurance products, whose benefits are not clear for them. Every visit to the farm for verifying the mortality of individual animals, every veterinary certificate issued for claim assessment in case of diseases, and every inspection needed for documenting losses caused by natural disasters cause cost and time burdens that are hard for insurers to cover without raising premiums.

Opportunities: Microinsurance and parametric product innovation expanding smallholder coverage and digital distribution reducing administrative cost

Innovation in microinsurance products will provide a highly commercially viable near-term development in the livestock insurance industry because it will solve the problem of affordability that keeps the world's largest number of livestock farmers uninsured. In the case of Pula microinsurance which covers 20 million farmers in Africa, Asia and Latin America with claims worth USD 120 million, we see that microinsurance based on satellite imagery and AI models is commercially sustainable and makes it possible to offer coverage without the costs of field assessment.

Innovation in parametric and index-based products will make it possible to achieve administrative efficiency to offer commercially viable coverage at premiums that smallholder farmers can afford. This is evident in the case of Kenya Livestock Insurance Programme's IBLI model that provides coverage for 90,000 cattle worth over USD 30 million every year and pays claims worth USD 10 million every year.

Recent Developments:

-

2024: Hurricane Milton caused agricultural losses exceeding USD 190 million in Florida in 2024, impacting approximately 5.7 million acres of agricultural land including livestock operations, generating substantial insurance claims under USDA-backed and commercial livestock insurance programmes.

-

2024: HPAI A(H5) avian influenza continued to affect U.S. poultry farms in 2024, driving record livestock insurance claim volumes and prompting USDA Risk Management Agency programme participation increases among commercial poultry operators seeking protection against epidemic-scale bird losses.

-

2024: Pula microinsurance surpassed 20 million farmer coverage in Africa, Asia, and Latin America in 2024, with cumulative claims paid exceeding USD 120 million, demonstrating AI and satellite-based indexed livestock and crop insurance scalability across smallholder agricultural markets.

Livestock Insurance Market Key Players:

-

Zurich Insurance Group AG

-

Allianz SE

-

AXA S.A.

-

Swiss Re AG

-

Munich Re Group

-

Chubb Limited

-

American Agricultural Insurance Company

-

Tokio Marine Holdings Inc.

-

QBE Insurance Group Ltd.

-

Sompo Holdings Inc.

-

ICICI Lombard General Insurance Company Ltd.

-

New India Assurance Company Ltd.

-

Ping An Insurance Group Co.

-

China Life Insurance Group

-

Fairfax Financial Holdings Ltd.

-

Agro General Insurance Company

-

Archer Daniels Midland Company (ADM Crop Risk Services)

-

Pula Advisors Ltd.

-

ProAg (Tokio Marine Group)

-

PICC Property and Casualty Company Ltd.

Livestock Insurance Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.99 Billion |

| Market Size by 2035 | USD 10.55 Billion |

| CAGR | CAGR of 7.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Animal Type (Bovine, Poultry, Swine, Sheep & Goats, Others) • By Coverage (Mortality, Revenue, Others) • By Distribution Channel (Direct, Agency/Broker, Bancassurance, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zurich Insurance Group AG, Allianz SE, AXA S.A., Swiss Re AG, Munich Re Group, Chubb Limited, American Agricultural Insurance Company, Tokio Marine Holdings Inc., QBE Insurance Group Ltd., Sompo Holdings Inc., ICICI Lombard General Insurance Company Ltd., New India Assurance Company Ltd., Ping An Insurance Group Co., China Life Insurance Group, Fairfax Financial Holdings Ltd., Agro General Insurance Company, Archer Daniels Midland Company (ADM Crop Risk Services), Pula Advisors Ltd., ProAg (Tokio Marine Group), and PICC Property and Casualty Company Ltd. |

Frequently Asked Questions

The Livestock Insurance Market is expected to grow at a CAGR of 7.8% from 2026 to 2035.

The Livestock Insurance Market was valued at USD 4.99 Billion in 2025.

Rising frequency and severity of climate-driven extreme weather events and infectious disease outbreaks increasing livestock loss exposure, and government subsidy programmes expanding insurance accessibility to commercial and smallholder farming operations across developed and emerging agricultural economies.

Mortality dominated with approximately 39% share in 2025, while Revenue is the fastest growing coverage segment driven by commercial livestock producer demand for comprehensive income protection.

North America dominated in 2025 through the U.S. USDA RMA's federally supported livestock insurance programmes and the extraordinary commercial scale of U.S. cattle, poultry, and swine production, while Asia Pacific is the fastest growing region.

Get in Touch