Healthcare Synthetic Data Market Report Scope & Overview:

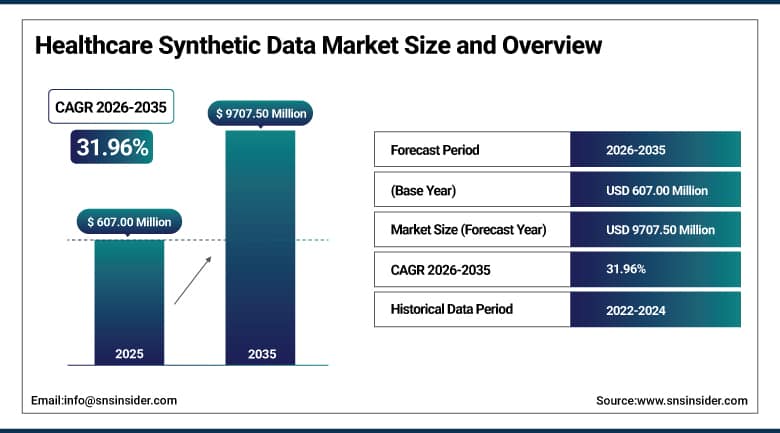

The Healthcare Synthetic Data Market was valued at USD 607.00 million in 2025 and is expected to reach USD 9707.50 million by 2035, growing at a CAGR of 31.96% from 2026–2035.

The healthcare synthetic data market is witnessing strong growth in the global market owing to increasing demand for privacy-preserving healthcare data. Rising adoption of artificial intelligence in clinical trials, drug discovery, and medical imaging is supporting market expansion. Healthcare organizations are increasingly using synthetic datasets to overcome real patient data limitations. Manufacturers and technology providers are focusing on advanced generative AI models for high-quality data creation. Growing regulatory pressure on data privacy and security is driving adoption across hospitals and pharmaceutical companies. Increasing investment in digital health infrastructure and AI-driven research is further accelerating market growth.

According to the World Health Organization Global Strategy on Digital Health and OECD Health Data 2025 indicators, over 90% of OECD countries have implemented national digital health systems with interoperable electronic health records, creating structured datasets for secondary use.

As per the U.S. Office of the National Coordinator for Health IT interoperability report, 96% of non-federal acute care hospitals use certified EHR systems. Additionally, WHO estimates that more than 60% of countries have adopted some form of health data governance framework, enabling regulated use of synthetic data generation for privacy-preserving medical research and AI model training applications globally.

Market Size and Forecast:

-

Market Size 2026E: USD 799.84 million

-

Market Size 2035: USD 9707.50 million

-

CAGR (2026 - 2035): 31.96%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Healthcare Synthetic Data Market - Request Free Sample Report

Healthcare Synthetic Data Market Trends:

-

The increasing use of generative AI technologies will help in the rapid creation of realistic synthetic patient data sets for health care applications.

-

Pharmaceutical firms are increasingly turning to synthetic data for quicker drug discovery, better clinical trials, and reduced costs of research.

-

Increasing regulation on data privacy issues is making health care entities seek out proper substitutes to facilitate the use of data.

-

Growing investment in precision medicines is leading to greater need for diverse synthetic data sets.

-

More healthcare firms are increasingly teaming up with technology companies to train their AI models through synthetic data.

-

Increased ethical data sharing is encouraging the increased use of synthetic data.

U.S. Healthcare Synthetic Data Market Outlook:

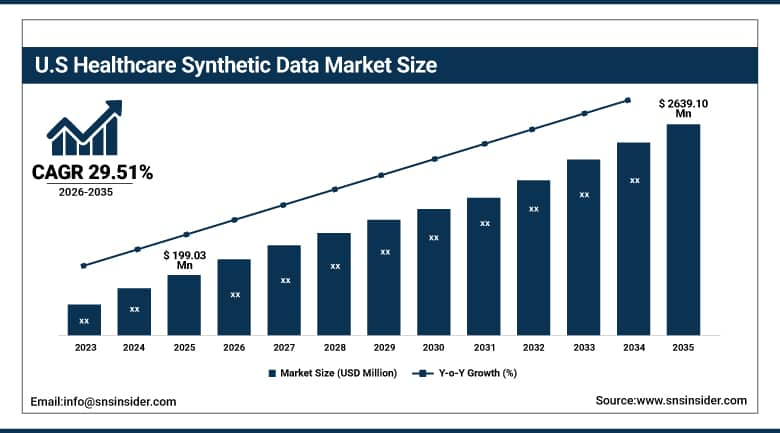

The U.S. Healthcare Synthetic Data Market was valued at USD 199.03 million in 2025 and is expected to reach around USD 2639.10 million by 2035, growing at a CAGR of 29.51% from 2026–2035.

The U.S. healthcare synthetic data market is growing rapidly owing to strong adoption of artificial intelligence in healthcare systems. Increasing use of synthetic data in clinical trials, drug discovery, and medical imaging is supporting market expansion. Healthcare organizations are focusing on privacy preserving data solutions to meet regulatory compliance requirements. Rising demand for AI training datasets in hospitals and pharmaceutical companies is accelerating adoption. Strong presence of advanced digital health infrastructure and major technology providers is further boosting market growth. Continuous investment in generative AI and healthcare analytics is driving long term market expansion.

According to the U.S. Department of Health & Human Services and the Office of the National Coordinator for Health IT 2025 Interoperability and Data Modernization Measures, greater than 96% of U.S. non-federal acute care hospitals utilize certified electronic health records systems, hence the creation of substantial amounts of clinical data.

As per the Centers for Disease Control and Prevention and FDA real-world evidence framework updates, more than 75% of clinical research organizations in the United States now utilize synthetic or de-identified datasets for secondary analysis and model training support.

Healthcare Synthetic Data Market Segment Analysis:

-

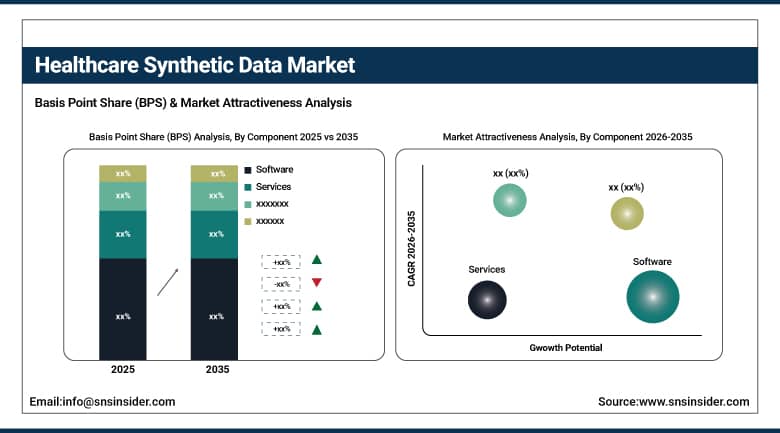

By Component, software dominated the market with 68.40% share in 2025; while services are the fastest growing segment with CAGR of 34.33% during 2026 to 2035.

-

By Application, medical imaging dominated the market with 34.75% share in 2025; while drug discovery is the fastest growing segment with CAGR of 36.94% during 2026 to 2035.

-

By Data Type, structured data dominated the market with 56.80% share in 2025; while unstructured data are the fastest growing segment with CAGR of 36.97% during 2026 to 2035.

-

By End-User, pharmaceutical & biotechnology companies dominated the market with 38.90% share in 2025; while research & academic institutions are the fastest growing segment with CAGR of 35.93% during 2026 to 2035.

By Component, software dominated the healthcare synthetic data market, while services are the fastest growing segment.

The Software segment led the healthcare synthetic data market with the dominated revenue share in 2025 owing to the fast-paced adoption of AI-enabled data generation software. These platforms are extensively used by hospitals and in the process of conducting research. High demand for scalable de-identified data sets. The need for regulatory compliance as per HIPAA regulations also fuels software adoption within the healthcare ecosystem. Continuous development in machine learning algorithms ensures high-quality data.

The Services segment is likely to expand at the fastest CAGR between 2026 and 2035 owing to increasing demand for customized synthetic data generation services. The healthcare organizations do not have the expertise in-house for advanced AI models and data engineering. Outsourcing of data privacy management and validation services increases the adoption rate. Development of cloud-based healthcare infrastructure and the need for continuous model training also contribute to growth in adoption of services in hospitals and research institutes.

By Application, medical imaging dominated the healthcare synthetic data market, while drug discovery is the fastest growing segment.

The Medical Imaging segment is the key contributor to the healthcare synthetic data market in terms of the dominated revenue share in 2025. The primary factor behind this is the significant reliance on imaging data in AI model training and diagnosis purposes. There is a high demand for medical imaging datasets for radiology, pathology, and disease detection applications. The healthcare industry produces a large amount of imaging data and, thus, is suitable for synthetic data generation to ensure patient confidentiality and AI accuracy.

Drug Discovery segment is likely to exhibit the fastest CAGR during 2026–2035. This is attributed to the rise in the use of AI in the drug discovery process and pharmaceutical research. Synthetic data enables simulation of clinical trials and molecular interaction studies without risking any patient data. This saves time and cost associated with drug discovery. Additionally, increasing focus on personalized medicine and innovations in the field of biotechnology are boosting the use of synthetic data in drug discovery process.

By Data Type, structured data dominated the healthcare synthetic data market, while unstructured data is the fastest growing segment.

The Structured Data Segment captured dominated revenue share in the healthcare synthetic data market in 2025 due to higher availability of data in electronic health record, insurance claim, and laboratory databases. Structured data is more feasible in terms of processing and integration into the algorithms for training AI and machine learning. Organizations operating in the healthcare industry opt for structured datasets to develop predictive analytics. Widespread adoption in clinical research and operational healthcare processes supports its dominant market position.

The Unstructured Data Segment is projected to register the fastest CAGR between 2026 and 2035 due to growing use of medical images, clinical notes, and diagnostic test reports. The growing usage of natural language processing and generative AI technology facilitates the utilization of unstructured data in the healthcare sector. Increasing demand for insights from complex datasets is also fueling the adoption rate. Growth in the AI-driven radiology, pathology, and clinical decision support systems is further boosting the market of this segment.

By End-User, pharmaceutical & biotechnology companies dominated the healthcare synthetic data market, while research & academic institutions are the fastest growing segment.

The Pharmaceutical & Biotechnology Companies segment led the healthcare synthetic data market in 2025 with the dominated market revenue share. The high demand of these companies for synthetic datasets used for drug discovery and development and other clinical trials is a major reason behind the high revenues in the market for these companies. Significant spending on Research and Development along with adoption of innovative AI technologies further reinforces the position of these companies in the market.

The Research & Academic Institutions segment will record the fastest CAGR from 2026-2035. Increasing use of synthetic data for medical research, AI training, and healthcare innovations is a key factor behind the high growth in the Research & Academic Institutions segment. Less availability of patient data is driving the demand for synthetic data in this segment. Collaboration between technology vendors and governments in funding research programs is driving the adoption rate in this segment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.35% |

|

Europe |

Germany |

28.40% |

|

Asia Pacific |

China |

43.20% |

|

Middle East & Africa |

UAE |

18.10% |

|

Latin America |

Brazil |

48.60% |

North America Healthcare Synthetic Data Market Insights.

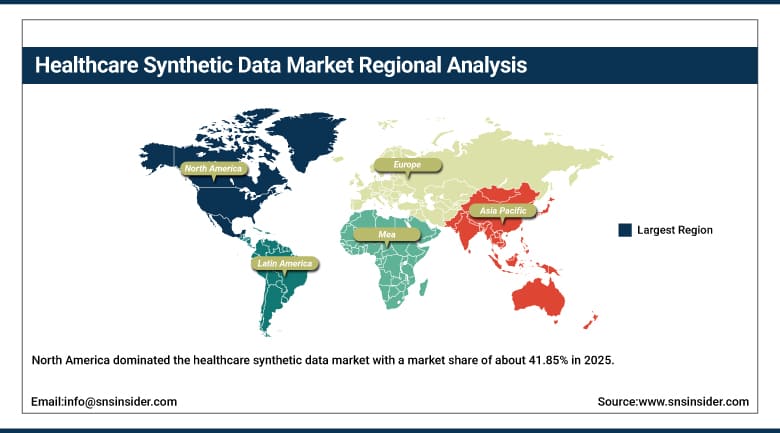

North America dominated the healthcare synthetic data market with a market share of about 41.85% in 2025 owing to increasing adoption of AI driven healthcare solutions. The region benefits from advanced digital health infrastructure and strong presence of leading technology companies. Rising use of synthetic data in clinical trials, drug discovery, and medical imaging is driving expansion across the United States and Canada. Increasing focus on data privacy regulations and HIPAA compliance is further supporting market growth. Strong R&D investments and early AI adoption are accelerating innovation in synthetic data technologies.

As per the Canadian Institute for Health Information digital health progress report, more than 80% of primary care physicians in Canada use electronic medical records. Additionally, U.S. National Institutes of Health data governance frameworks report increasing use of de-identified and synthetic datasets in over 30% of federally funded health AI research projects, supporting privacy-preserving data simulation in healthcare analytics.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Healthcare Synthetic Data Market Insights.

Europe healthcare synthetic data market is characterized by steady growth in 2025 owing to strict data privacy regulations and increasing healthcare digitalization. The major countries contributing towards demand include Germany, France, United Kingdom, and Italy. Rising adoption of AI in medical research and clinical trials is fueling market expansion. Increasing use of synthetic data in healthcare analytics and pharmaceutical research is further propelling growth across the region. Strong regulatory frameworks such as GDPR are driving secure data innovation.

As per the European Commission’s Digital Economy and Society Index and digital health indicators by Eurostat in 2025, over 93% of hospitals in the European Union had implemented electronic health records, thus making it an integral part of synthetic data creation process. Also, per health data governance by OECD, over 70% of healthcare organizations in Europe have adopted AI analytics.

Asia Pacific Healthcare Synthetic Data Market Insights.

Asia Pacific is expected to register the fastest growth in the healthcare synthetic data market with a CAGR of about 35.52% during 2026–2035 owing to rapid digital transformation in healthcare and expanding AI ecosystem. Strong demand is emerging across China, India, Japan, South Korea, and Southeast Asia. Increasing investments in clinical research and biotechnology are significantly boosting adoption. Growing need for cost effective healthcare data solutions is further accelerating market expansion and innovation across the region.

According to the World Health Organization Global Strategy on Digital Health and UN DESA Digital Transformation Indicators by 2025, more than 70% of countries in the Asia Pacific region have put into place their digital health strategies that include electronic health records and interoperable information systems. According to OECD health data and WHO eHealth surveys, the digitization rate of hospitals is higher than 65% in the Asia Pacific high-income countries like Japan, South Korea, and Australia.

Middle East & Africa and Latin America Healthcare Synthetic Data Market Insights.

The Middle East & Africa along with Latin American regions are experiencing steady growth due to expanding healthcare infrastructure and increasing digital transformation initiatives. Key contributing countries include Brazil, Mexico, UAE, Saudi Arabia, and South Africa. Rising investments in healthcare analytics and pharmaceutical research are supporting market growth. Increasing demand for AI based healthcare solutions is driving adoption of synthetic data across hospitals and research institutions.

According to WHO Global Health Observatory and UN DESA Digital Health Monitoring Framework 2025, Latin America has attained 81% urbanization and 70% health facilities in that region have at least the basic e-health systems while Africa still maintains an urbanization of 43% and digital health systems coverage of less than 50%.

As per OECD and WHO digital health interoperability indicators, fewer than 35% of low- and middle-income countries in these regions have fully integrated clinical data exchange systems.

Market Dynamics:

Growth Drivers: Rising demand for privacy preserving healthcare data solutions driven by strict regulatory compliance requirements globally.

Rising pressures with respect to regulatory aspects for privacy of patient data are leading to robust implementation of synthetic data technologies in the field of healthcare. The regulations like HIPAA, GDPR, or any other nationally set laws prevent access to patient data sets for analytics or research purposes. Healthcare organizations implement synthetic data technologies to ensure compliance as well as data utility. The risk of data breach and unauthorized data access is mitigated through this process. The increasing focus on ethical use of data and information sharing drives demand.

As per the World Health Organization Global Health Observatory and OECD Health Data 2025, more than 90% of all OECD countries have established their national digital health or health data governance structures, which include provisions for patients' data privacy and interoperability. According to GDPR compliance data by European Commission, more than 4,000 cases were registered each year from data protection authorities in EU member countries.

Restraints: High complexity in generating accurate and clinically reliable synthetic healthcare datasets across diverse medical applications.

Generation of good synthetic data in the field of healthcare requires sophisticated computation, expertise, and computing resources. The core issue in this case is to make sure that the datasets created do not distort the patient's status in any way and do not lead to bias creation. Erroneous synthetic data may affect the decision-making process and even performance of the AI models. Moreover, it is difficult to confirm the credibility of such datasets in healthcare facilities.

Opportunities:Expansion of AI driven drug discovery and clinical trial acceleration creating strong demand for synthetic patient datasets.

The rise in application of AI in drug discovery and design of clinical trials has created many prospects for the use of synthetic data. Pharma firms are using synthetic data sets in order to create virtual patients and speed up their research processes. They will be less reliant on recruiting actual patients and cut down their expenses. It becomes easier to test different hypotheses and improve efficiency in designing trials. Growing interest in precision medicines and customized medicines has widened their applications.

According to the OECD AI in Health policy framework, more than 70% of OECD member states have developed national AI policies with applications to health care. Furthermore, the WHO’s Digital Health Assessments reveal that more than 60% of countries have established data governance policies that allow secondary health data uses, thus facilitating drug discovery based on AI models and requiring synthetic patient datasets.

Recent Developments:

-

2026: Google partnered with CVS Health to launch Health100, an AI-powered platform integrating diverse healthcare data streams.

-

2025: Microsoft introduced new healthcare AI capabilities within Microsoft Cloud, expanding responsible data and analytics tools.

-

2025: Oracle partnered with Cleveland Clinic and G42 to develop an AI-driven healthcare platform and innovation hub.

-

2024: AWS strengthened healthcare analytics through Amazon HealthLake and generative AI services enabling synthetic data creation for clinical and research use.

Healthcare Synthetic Data Market Key Players are:

-

Syntegra

-

MDClone

-

Gretel.ai

-

MOSTLY AI

-

Hazy

-

Tonic.ai

-

Syntho

-

Datagen

-

NVIDIA

-

Microsoft

-

Google

-

Amazon Web Services

-

Oracle

-

IBM

-

SAS Institute

-

IQVIA

-

HealthVerity

-

TriNetX

-

Komodo Health

-

Epic Systems

Healthcare Synthetic Data Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 607.00 Million |

| Market Size by 2035 | USD 9707.50 Million |

| CAGR | CAGR of 31.96% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Application (Medical Imaging, Drug Discovery, Clinical Trials, Patient Data Management, Disease Modeling, Others) • By Data Type (Structured Data, Unstructured Data, Semi-Structured Data) • By End User (Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Research & Academic Institutions, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Syntegra, MDClone, Gretel.ai, MOSTLY AI, Hazy, Tonic.ai, Syntho, Datagen, NVIDIA, Microsoft, Google, Amazon Web Services, Oracle, IBM, SAS Institute, IQVIA, HealthVerity, TriNetX, Komodo Health, Epic Systems |

Frequently Asked Questions

Major growth factors include rising demand for privacy preserving data, AI adoption in clinical trials, drug discovery, medical imaging, regulatory pressure, digital health investments, and generative AI advancements.

The healthcare synthetic data market was valued at USD 607.00 million in 2025.

The healthcare synthetic data market is expected to grow at a CAGR of 31.96% from 2026 to 2035.

North America dominated the healthcare synthetic data market in 2025 due to advanced infrastructure, AI adoption, strong regulations, and investments.

Medical Imaging segment dominated in 2025 due to AI training needs, diagnostics, radiology use, and privacy compliant healthcare imaging data.

Get in Touch