Logic IC Market Report Scope & Overview:

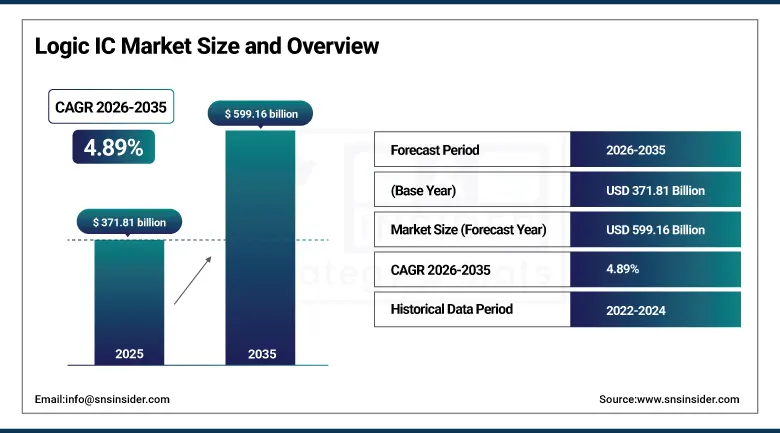

The Logic IC Market was valued at USD 371.81 billion in 2025 and is expected to reach USD 599.16 billion by 2035, growing at a CAGR of 4.89% from 2026-2035.

Logic IC Market growth is due to high demand for consumer electronics, smartphones, and smart devices with highly efficient semiconductors that ensure good performance and energy efficiency. High growth rate in demand for logic ICs is being fueled due to increased use of artificial intelligence (AI), internet of things (IoT), 5G network, and automation systems. Growing usage of logic ICs in automotive electronics, industrial automation, and data center industries is contributing to market growth. Moreover, innovations in semiconductor industry and digital transformation are also boosting global market growth.

The U.S. CHIPS ecosystem, a government-backed semiconductor initiative, has attracted over USD 645 billion in investments across 140+ projects in 30 states, primarily focused on advanced logic IC fabrication and AI chip production, strengthening domestic semiconductor manufacturing capabilities and supply chain resilience.

Market Size and Forecast

-

Market Size in 2025: USD 371.81 Billion

-

Market Size by 2035: USD 599.16 Billion

-

CAGR: 4.89% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Logic IC Market - Request Free Sample Report

Logic IC Market Trends

-

Rising demand for high-performance computing, consumer electronics, and automotive electronics is driving the logic IC market.

-

Growing adoption in smartphones, IoT devices, data centers, and industrial automation systems is boosting market growth.

-

Expansion of AI, 5G networks, and cloud computing infrastructure is fueling advanced logic chip deployment.

-

Increasing focus on energy efficiency, miniaturization, and faster processing speeds is shaping adoption trends.

-

Advancements in semiconductor fabrication nodes, chip architecture, and system-on-chip (SoC) integration are enhancing performance.

-

Rising investments in semiconductor manufacturing capacity and supply chain resilience are supporting market expansion.

-

Collaborations between chip designers, foundries, and OEMs are accelerating innovation and global adoption.

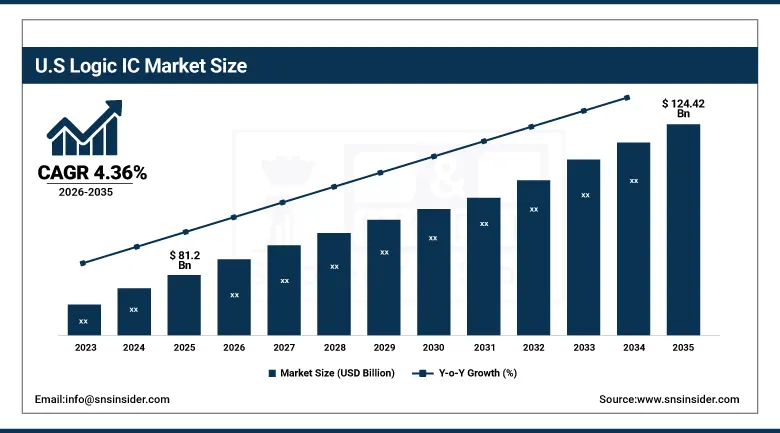

U.S. Logic IC Market was valued at USD 81.2 billion in 2025 and is expected to reach USD 124.42 billion by 2035, growing at a CAGR of 4.36% from 2026-2035.

U.S. Logic IC Market is growing due to increasing demand for sophisticated computers, artificial intelligence, and consumer electronics. Adoption of 5G, Internet of Things (IoT), and automation technology is also contributing toward market growth. Moreover, research and development in semiconductors, increased investment in data centers, and automotive electronics are fueling growth in the market.

Logic IC Market Segment Highlights

-

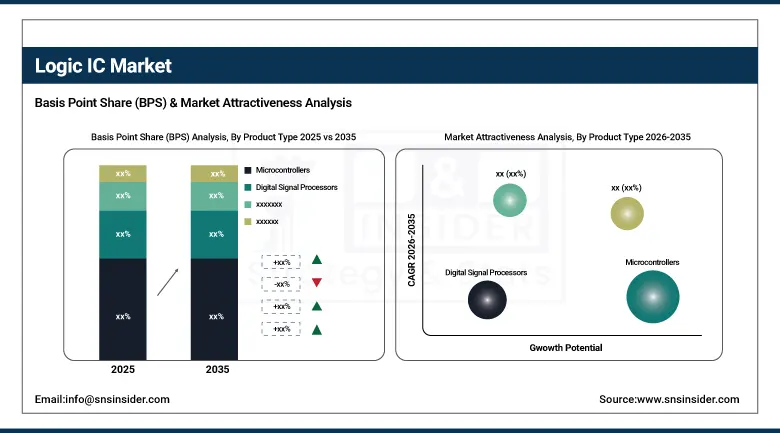

By Product Type, Microcontrollers segment dominated the Logic IC Market in 2025 with approximately 34% share; Programmable Logic Devices segment fastest growing (CAGR).

-

By Application, Combinational Logic segment dominated the Logic IC Market in 2025 with approximately 42% share; Programmable Logic segment fastest growing (CAGR).

-

By Technology, CMOS segment dominated the Logic IC Market in 2025 with approximately 68% share; GaAs Technology segment fastest growing (CAGR).

-

By End-User, Consumer Electronics segment dominated the Logic IC Market in 2025 with approximately 39% share; Automotive segment fastest growing (CAGR).

Logic IC Market Segment Analysis

By Product Type, Microcontrollers segment dominates the Logic IC Market, Programmable Logic Devices segment expected to grow fastest

The microcontrollers segment held the major share in the Logic IC Market in 2025 as microcontrollers have been widely used in embedded systems, automation systems, consumer electronics, and industrial control applications. The advantages that come with using microcontrollers include high level of integration, lower levels of energy usage, and cost-effectiveness that make microcontrollers an ideal choice of product for use in numerous compact electronic items and smart electronics. The adaptability of microcontrollers in computing, control, and communications makes them increasingly popular and thus leading the segment.

The programmable logic devices segment is projected to grow at the highest CAGR during the forecast period. This can be attributed to the rising demand for computing solutions that are flexible and can be customized after manufacturing. Programmable logic devices can adapt to any changes brought about by the developments of advanced technological trends in telecommunications, data centers, and automation of industrial facilities. Increasing application of AI, machine learning, and 5G technologies is further driving growth in the programmable logic devices segment.

By Application, Combinational Logic segment dominates the Logic IC Market, Programmable Logic segment expected to grow fastest

Combinational Logic segment accounted for largest share of Logic IC Market in 2025 because of their extensive use in various digital applications whose output is based on inputs present at the instant of operation like arithmetic circuits, multiplexers, and data processing circuits. Because of their ease of operations, efficiency, and reliability, these circuits are crucial in almost all kinds of electronic devices. Growing need of efficient digital computations in various electronic applications has played a significant role in the dominance of combinational circuits in Logic ICs.

Programmable Logic segment has emerged as fastest growing segment because of growing demand for flexible digital designs. Programmable logic enables manufacturers to design circuits which can be altered after manufacturing according to requirements, thus saving costs and cutting down time for production. Rising complexity in electronics as well as the growing deployment of these designs in applications like AI computing, automotive electronics, and high speed communications have played a key role in accelerating demand.

By Technology, CMOS segment dominates the Logic IC Market, GaAs Technology segment expected to grow fastest

In 2025, the CMOS segment accounted for largest share in Logic IC Market due to low power consumption, high resistance to noise interference, and excellent scalability, thereby making it an ideal choice among other technologies that could be incorporated into contemporary ICs. The segment comprises microprocessor, memory devices, and digital logic circuits used in consumer electronic products, computers, and communication systems. Being more economical and highly scalable, CMOS technology became industry norm, while fast expansion in the portable electronics sector bolstered the position of CMOS segment further.

The fastest-growing segment during the forecast period is GaAs Technology. Superior electron mobility and effectiveness in high-frequency operations account for popularity of GaAs-based logic ICs. In addition, GaAs Technology is widely used in RF devices, satellite communications, radars, and 5G infrastructure. Increasing number of applications requiring high-speed and power-efficient operation leads to increasing demand for GaAs logic ICs. Technological developments and growing implementation in aerospace and military sectors stimulate further growth.

By End-User, Consumer Electronics segment dominates the Logic IC Market, Automotive segment expected to grow fastest

Consumer Electronics is the dominating segment in the Logic IC market during 2025 because of the increasing demand for smartphones, tablets, laptops, smart TVs, and wearables. The role of logic ICs is vital in carrying out process control and connectivity operations in these products. Consumption in this sector has been highly influenced by rapid digitization, higher disposable incomes, and constant product innovation. In addition, the growing preference for smart home gadgets and IoT-enabled electronics further consolidated the prominence of the consumer electronics segment in the logic IC market.

Automotive is fast-growing sector mainly attributed to increased installation of advanced electronics in automobiles such as ADAS, infotainment, electric propulsion, and autonomous technologies. Modern cars depend on logic ICs for performing data processing, safety measures, and connectivity functionalities. Increased deployment of autonomous and electric vehicles, stringent safety rules, and consumer demand for smart transportation technology are the primary factors influencing the adoption of advanced logic ICs in Automotive sector.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

45.2% |

|

North America |

United States |

91.6% |

|

Europe |

United Kingdom |

23.4% |

|

Middle East & Africa |

UAE |

12.5% |

|

Latin America |

Brazil |

49.7% |

Asia Pacific Logic IC Market Insights

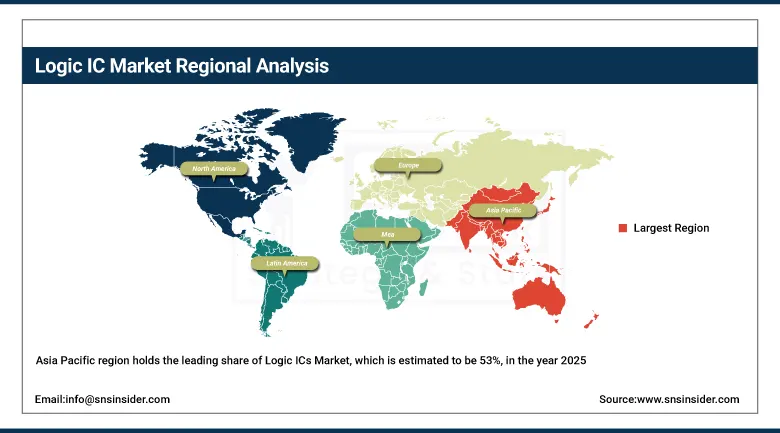

The Asia Pacific region holds the leading share of Logic ICs Market, which is estimated to be 53%, in the year 2025. The reasons for dominance include good manufacturing ability and demand for consumer electronics in the region. Besides, fast industrialization, automobile manufacturing, and the application of advanced technology like 5G, IoT, and AI contribute positively to regional development. There are also the benefits of having many semiconductor foundries and electronics manufacturers, which enhance the supply chain. Furthermore, growing spending on smart devices, industrial automation, and digital infrastructure contribute immensely to this trend.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Logic IC Market Insights

The North America Logic IC Market is witnessing consistent growth because of the rising need for advanced computing systems, AI applications, and high-end consumer electronics. The use of automation technologies, cloud computing, and 5G network infrastructure will continue to fuel the demand for logic integrated circuits. The presence of top semiconductor companies, coupled with continuous research and development activities, will contribute to chip innovation and manufacturing. Furthermore, the increasing uses in the automotive electronics industry, data center industry, and industrial applications will be significant contributors to the region’s market growth.

Europe Logic IC Market Insights

The Europe Logic IC Market is experiencing steady growth due to increased demand for automotive electronics, industrial automation, and smart manufacturing systems. Growing emphasis on energy efficient semiconductor technology and digitization infrastructure is fueling demand in the market. The presence of the established automotive sector in the region is playing a key role in the deployment of logic ICs in areas such as electrical vehicles, safety applications, and infotainment systems. Additionally, increasing R&D spend on semiconductors and growing demand for IoT-based devices are boosting market growth.

Middle East & Africa and Latin America Logic IC Market Insights

Middle East & Africa and Latin America Logic IC Market is witnessing steady growth owing to rising digital transformation and electronics adoption. The increasing requirement for consumer electronics, communications, and automation systems is leading to greater penetration into these regions. Increasing expenditure on smart infrastructure, telecommunication, and data center applications is further bolstering the demand for logic integrated circuits. Moreover, increasing urbanization along with enhanced adoption of technology and industrial growth is offering significant opportunities to semiconductor manufacturers.

Market Growth Drivers:

Rising Demand for High-Performance Computing and Smart Electronic Devices Driving Global Expansion of Logic Integrated Circuit Market Rapidly: Rising demand for high-performance computing systems, intelligent devices, and electronic components has played an important role in contributing to the expansion of the Logic IC market all around the world. The increasing usage of smartphones, tablets, wearable electronics, and internet of things enabled devices is creating demand for efficient and small logic integrated circuits. The growing innovation in the field of consumer electronics and technology innovations is adding on to the demand for fast and power-efficient IC solutions. Usage of automated systems and AI applications is also fueling market growth. Furthermore, growing integration of semiconductors into automotive, industrial, and communication electronics is contributing to market expansion.

Market Restraints:

High Manufacturing Complexity and Rising Production Costs Restricting Large-Scale Expansion of Logic IC Industry Across Global Semiconductor Ecosystem: The Logic ICs industry faces high restraints due to high complexities in manufacturing and high production costs. Manufacturing of advanced semiconductors requires complex equipment, clean room manufacturing facilities and huge capital costs; therefore, the manufacturing costs will be high. Small scale of integrated circuits coupled with increasing complexity during design adds to the complexities in manufacturing. Supply chain disturbances coupled with lack of raw materials have also affected the efficiency of production. Rapid changes in technology mean that fabrication processes need constant upgrading, adding on to costs of operations by manufacturers.

Market Opportunities:

Increasing Adoption of AI, IoT, and 5G Technologies Creating Strong Demand for Advanced Logic IC Solutions Across Emerging Digital Ecosystems: Faster adoption of artificial intelligence, internet of things, and 5G technology provides substantial scope for logic ICs that are highly advanced. Technologies such as AI, IoT, and 5G are demanding faster data processing speed, less latency, and power efficiency, which results in increased demand for advanced ICs. The proliferation of smart infrastructure, connected devices, and cloud computing is another factor contributing to the increased demand for logic ICs. Increase in data center operations, automation technologies, and edge computing is likely to drive the growth of the market as well. Besides, innovations in semiconductor design and investment in digital transformation are anticipated to fuel market growth.

Recent Developments:

-

2026: Intel expanded its AI-driven logic IC roadmap with Xeon 6 and next-gen AI PC processors. The company focused on advanced logic architectures optimized for data centers and edge computing, improving performance-per-watt and strengthening its position in high-performance logic semiconductor solutions.

-

2026: TSMC expanded advanced logic node manufacturing capacity in Europe and Asia, supporting 3nm and 2nm-class chip production. The company focused on logic IC scaling for AI accelerators, CPUs, and GPUs driven by hyperscale computing demand.

-

2025: AMD introduced advanced Ryzen and EPYC processors built on optimized logic IC designs, improving compute density and AI acceleration capabilities. The company focused on chiplet-based architecture to enhance scalability and power efficiency in data center logic systems.

-

2025: Qualcomm expanded Snapdragon SoC platforms integrating advanced logic ICs for mobile AI processing. The company enhanced CPU-GPU-NPU integration for on-device intelligence, improving smartphone and edge computing performance.

-

2024: Intel launched Gaudi 3 AI accelerators and Xeon 6 processors, strengthening its logic IC portfolio for AI data centers. These chips improved high-performance logic computation for generative AI workloads and cloud infrastructure.

Logic IC Market Key Players

-

Intel Corporation

-

Advanced Micro Devices (AMD)

-

NVIDIA Corporation

-

Qualcomm Incorporated

-

Broadcom Inc.

-

Texas Instruments Incorporated

-

STMicroelectronics N.V.

-

NXP Semiconductors N.V.

-

Infineon Technologies AG

-

MediaTek Inc.

-

Samsung Electronics Co., Ltd.

-

Taiwan Semiconductor Manufacturing Company (TSMC)

-

Renesas Electronics Corporation

-

Microchip Technology Inc.

-

Marvell Technology, Inc.

-

ON Semiconductor (onsemi)

-

Toshiba Electronic Devices & Storage Corporation

-

Analog Devices, Inc.

-

Arm Holdings plc

-

Lattice Semiconductor Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 371.81 Billion |

| Market Size by 2035 | USD 599.16 Billion |

| CAGR | CAGR of 4.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Microcontrollers, Digital Signal Processors, Application-Specific Integrated Circuits and Programmable Logic Devices) • By Application (Combinational Logic, Sequential Logic and Programmable Logic) • By Technology (CMOS, BiCMOS, Bipolar, GaAs Technology) • By End-User (Consumer Electronics, Automotive, Telecommunications and Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intel Corporation, Advanced Micro Devices (AMD), NVIDIA Corporation, Qualcomm Incorporated, Broadcom Inc., Texas Instruments Incorporated, STMicroelectronics N.V., NXP Semiconductors N.V., Infineon Technologies AG, MediaTek Inc., Samsung Electronics Co., Ltd., Taiwan Semiconductor Manufacturing Company (TSMC), Renesas Electronics Corporation, Microchip Technology Inc., Marvell Technology, Inc., ON Semiconductor (onsemi), Toshiba Electronic Devices & Storage Corporation, Analog Devices, Inc. (ADI), Arm Holdings plc and Lattice Semiconductor Corporation. |

Frequently Asked Questions

Asia Pacific dominated the Logic IC Market in 2025.

The Microcontrollers segment dominated the Logic IC Market in 2025.

Rising Demand for High-Performance Computing and Smart Electronic Devices Driving Global Expansion of Logic Integrated Circuit Market Rapidly.

The Logic IC Market was valued at USD 371.81 billion in 2025.

The Logic IC Market is expected to grow at a CAGR of 4.89% from 2026 to 2035.

Get in Touch