Machine-to-Machine (M2M) Market Report Scope & Overview:

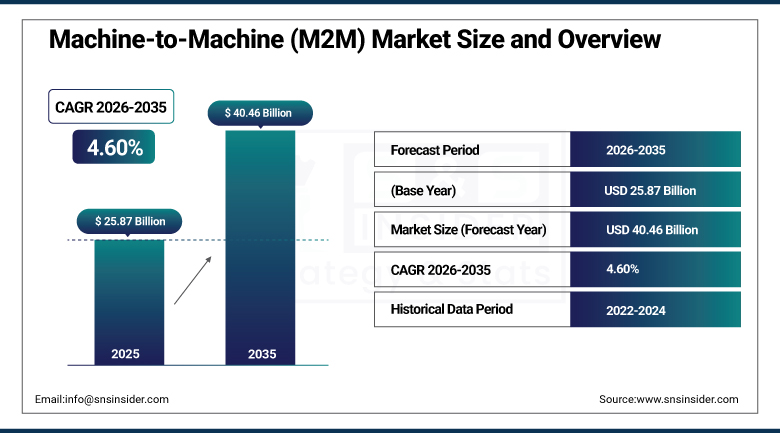

The Machine-to-Machine (M2M) Market was valued at USD 25.87 Billion in 2025 and is expected to reach USD 40.46 Billion by 2035, growing at a CAGR of 4.60% from 2026–2035.

The global Machine-to-Machine (M2M) Market is advancing steadily. M2M enables direct device-to-device communication without human intervention across manufacturing, healthcare, automotive, utilities, and logistics. Increasing demand for automation is a primary market driver. M2M helps companies improve efficiency, reduce operational costs, and automate processes. Integration of smart systems in industrial automation, telemedicine, and connected vehicles is accelerating adoption. Asia Pacific leads 5G, AI, and IoT adoption that is driving M2M connectivity infrastructure. Growing consumer demand for smart devices and connected services, alongside data privacy and cybersecurity challenges, defines the current commercial landscape globally.

Verizon Business launched an enhanced M2M platform with dedicated 5G-enabled IoT connectivity modules in 2024, targeting industrial automation and smart city applications. The platform offers sub-millisecond latency and integrated edge computing that enables real-time M2M data exchange at industrial scale. The launch reflects the commercial transition from 4G LTE-based M2M toward 5G-native architectures whose performance characteristics unlock latency-sensitive industrial applications that 4G networks cannot serve with equivalent reliability.

Market Size and Forecast:

-

Market Size in 2026E: USD 27.06 Billion

-

Market Size by 2035: USD 40.46 Billion

-

CAGR: 4.60% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Machine-to-Machine (M2M) Market- Request Free Sample Report

Machine-to-Machine (M2M) Market Trends:

-

5G network deployment is enabling ultra-low-latency M2M communication that unlocks time-critical industrial automation, autonomous vehicle coordination, and real-time healthcare monitoring applications previously constrained by 4G latency.

-

Edge computing integration with M2M infrastructure is enabling local data processing that reduces bandwidth requirements, improves response time, and maintains operational continuity when cloud connectivity is interrupted.

-

AI and machine learning integration is enabling predictive maintenance, anomaly detection, and automated operational decision-making that reduces unplanned downtime in manufacturing and utilities applications.

-

LPWAN technologies including NB-IoT and LTE-M are expanding M2M connectivity to low-power, low-cost devices in smart metering, asset tracking, and agricultural monitoring that cellular networks cannot serve cost-effectively.

-

Smart city programmes are deploying M2M infrastructure across traffic management, public safety, waste management, and environmental monitoring creating large-scale institutional M2M procurement globally.

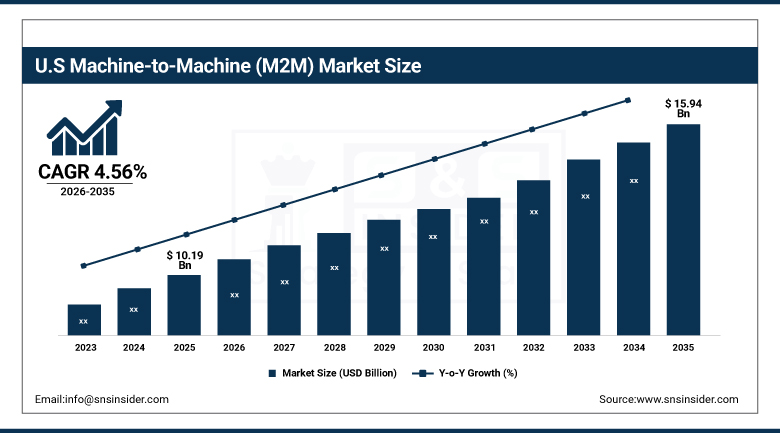

U.S. Machine-to-Machine (M2M) Market Outlook:

The U.S. Machine-to-Machine (M2M) Market was valued at approximately USD 10.19 Billion in 2025 and is expected to reach approximately USD 15.94 Billion by 2035, growing at a CAGR of approximately 4.56%.

The U.S. is the world’s largest M2M market. The North America contributed around 45% of global M2M revenue with the U.S. at the majority. Verizon, AT&T, and Cisco dominate enterprise M2M deployment across healthcare, automotive, and logistics. Federal investment in smart grid, connected transportation, and industrial IoT sustains above-average government procurement. Healthcare M2M adoption for remote patient monitoring and medical device telemetry is creating above-average growth. Regulatory frameworks increasingly mandate connected device data reporting across the U.S. healthcare sector.

AT&T expanded its FirstNet M2M connectivity platform in 2025, adding dedicated M2M data channels for first responder vehicle telemetry, medical device connectivity, and public safety infrastructure monitoring. The expansion reflects the growing institutional requirement for dedicated M2M connectivity whose quality-of-service guarantees cannot be met by shared commercial network capacity during emergency response scenarios.

Machine-to-Machine (M2M) Market Segment Analysis:

-

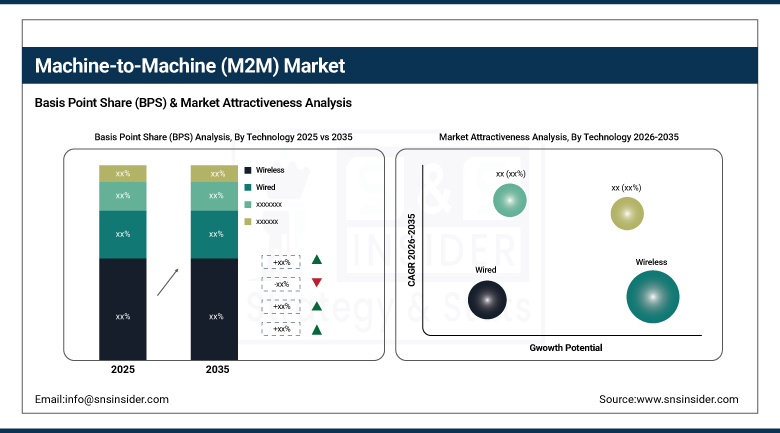

By Technology, the Wireless segment dominated the Machine-to-Machine (M2M) market with approximately 62% share in 2025, while the Wired segment maintains approximately 38% share with stable industrial automation deployment in factories and fixed network infrastructure.

-

By Component, the Hardware segment dominated the Machine-to-Machine (M2M) market with approximately 62% share in 2025 due to extensive use of embedded modules, routers, and gateways, while the Software segment is the fastest growing with a CAGR of approximately 7.2% as platform, analytics, and application management software create above-average recurring revenue.

-

By Application, the Industrial Automation segment dominated the Machine-to-Machine (M2M) market with approximately 33% share in 2025 as the highest-density M2M deployment environment, while the Healthcare segment is the fastest growing with a CAGR of approximately 6.8% driven by remote patient monitoring and medical device telemetry adoption.

-

By End User, the Manufacturing segment dominated the Machine-to-Machine (M2M) market with approximately 28% share in 2025 as the primary institutional M2M adopter, while the Transportation & Logistics segment is the fastest growing with a CAGR of approximately 6.5% as fleet telematics and cargo monitoring expand globally.

By Technology, wireless dominates, wired maintains significant presence

Wireless retained the dominant technology position with approximately 62% of the Machine-to-Machine (M2M) market in 2025. Its commercial primacy reflects the operational flexibility that wireless M2M connectivity provides across mobile assets, remote installations, and environments where wired infrastructure is cost-prohibitive. Cellular M2M through 4G LTE and progressively 5G networks serves the majority of industrial IoT, fleet management, and remote monitoring applications. LPWAN including NB-IoT and LTE-M creates new wireless M2M for low-power sensor devices whose applications were previously unserved by cost-effective wireless alternatives.

Wired M2M maintains a significant 38% share in factory automation, power grid SCADA systems, and building management networks where Ethernet, industrial fieldbus, and fibre optic connectivity deliver deterministic latency, bandwidth, and reliability that mission-critical industrial control applications require. The installed base of wired industrial networks whose replacement cycle extends across decades of capital equipment lifetime sustains wired M2M’s commercial presence in manufacturing and utility sectors that wireless cannot fully displace within the forecast period.

By Application, industrial automation dominates, healthcare grows fastest

Industrial automation retained the dominant application position with approximately 33% of the Machine-to-Machine (M2M) market in 2025. Manufacturing’s M2M deployment density reflects the operational value that machine-to-machine communication delivers in production environments where inter-system coordination, sensor data collection, and process control automation require continuous high-volume data exchange. Industry 4.0 adoption is accelerating industrial M2M deployment through integration of production machines, quality sensors, material handling systems, and enterprise IT into unified connected architectures whose value is measured in uptime improvement and defect reduction.

Healthcare is the fastest-growing application at approximately 6.8% CAGR because clinical evidence for remote patient monitoring’s efficacy in reducing readmissions, FDA medical device connectivity guidance, and healthcare system financial motivation to reduce in-person visit costs are converging. Each chronic disease patient enrolled in an M2M-connected remote monitoring programme creates recurring connectivity and device procurement that compounds with programme enrolment growth independently of facility capital investment cycles.

By Component, hardware dominates, software grows fastest

Hardware retained the dominant component position with approximately 62% of the Machine-to-Machine (M2M) market in 2025. Embedded modules, routers, gateways, and M2M terminal devices represent the primary capital procurement category whose deployment across industrial, utility, and consumer M2M applications creates the foundational installed base upon which software and service revenue compounds. Leading companies have launched advanced multi-mode 4G/5G modules for automotive, industrial, and energy device integration. The increasing adoption of high-performance ruggedised and compact hardware has reinforced hardware’s leadership.

Software is the fastest-growing component at approximately 7.2% CAGR because the M2M platform, analytics, and application management software market is capturing growing recurring revenue from the expanding connected device installed base. Each M2M hardware device deployed generates ongoing software subscription, data management, and platform service revenue whose recurring nature creates commercial value that substantially exceeds the one-time hardware transaction. AI-integrated M2M software platforms that provide predictive maintenance and operational analytics are commanding premium pricing that sustains above-average segment growth.

By End User, manufacturing dominates, transportation grows fastest

Manufacturing retained the dominant end user position with approximately 28% of the Machine-to-Machine (M2M) market in 2025. The manufacturing sector’s M2M adoption reflects Industry 4.0’s systematic deployment of connected sensors, robotic control systems, and production monitoring infrastructure across factory environments. Each new smart manufacturing programme creates M2M hardware, connectivity, and software procurement that compounds with industrialisation investment pace. The manufacturing sector’s above-average technology budget and clear productivity ROI calculation sustain consistent M2M procurement across economic cycles.

Transportation and logistics are the fastest-growing end user at approximately 6.5% CAGR because fleet telematics regulatory mandates, cargo condition monitoring requirements, and logistics efficiency motivation are creating structured M2M adoption across trucking, rail, and maritime transport. Electronic logging device mandates in the U.S. and equivalent regulations in Europe and Australia create mandatory fleet M2M connectivity procurement for commercial vehicle operators. Each percentage point increase in logistics automation investment creates proportional M2M connectivity and tracking device procurement.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Machine-to-Machine (M2M) Market Insights

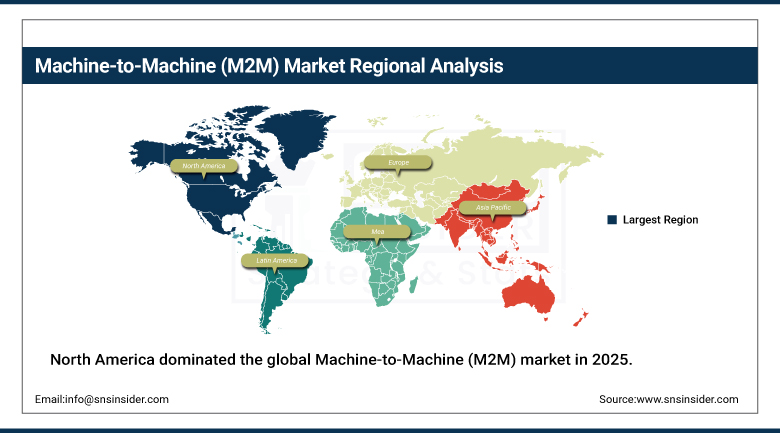

North America dominated the global Machine-to-Machine (M2M) market in 2025, contributing approximately 45% of total revenue. The United States accounts for approximately 87.4% of North American revenues through Verizon, AT&T, and Cisco’s M2M platform infrastructure, healthcare remote monitoring adoption, and manufacturing Industry 4.0 investment. Federal smart grid and connected transportation investment creates institutional procurement that sustains North America’s leadership across both private sector and government M2M channels.

Canada contributes approximately 12.6% of North American revenues through its mining, energy, and manufacturing sectors’ M2M investment, smart city programmes, and federal government digital infrastructure investment creating consistent public sector M2M connectivity procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe M2M Market Insights

Europe is a sophisticated Machine-to-Machine (M2M) market where Industry 4.0 adoption across German automotive and manufacturing, smart metering mandates, and EU Connected and Automated Mobility regulation create structured commercial demand. Germany accounts for approximately 22.3% of European revenues through dense industrial automation deployment, automotive OEM connected vehicle infrastructure, and Siemens, Bosch, and Deutsche Telekom’s M2M platform presence.

The United Kingdom, France, and Sweden are significant secondary markets where smart grid investment, connected healthcare programmes, and logistics fleet telematics create consistent M2M procurement independent of technology adoption cycle variation.

Asia Pacific M2M Market Insights

Asia Pacific is the fastest-growing regional Machine-to-Machine (M2M) market, driven by China’s 5G infrastructure investment, India’s smart city programme, Japan’s factory automation, and South Korea’s connected manufacturing. China accounts for approximately 44.8% of Asia Pacific revenues through extraordinary manufacturing M2M scale, government smart city investment, and the world’s largest 5G network whose M2M connectivity capacity creates the foundation for accelerated industrial and consumer M2M adoption.

India is the most commercially dynamic emerging market within Asia Pacific, where the Smart Cities Mission creates institutional M2M procurement across traffic, utilities, and public safety, and rapid manufacturing industrialisation creates growing industrial M2M deployment demand across tier-2 and tier-3 cities.

MEA & Latin America M2M Market Insights

The Middle East and Africa and Latin America are growing Machine-to-Machine (M2M) market where smart city investment, utilities digitalisation, and agricultural IoT create structured demand. UAE leads MEA at approximately 38.4% through smart city infrastructure, oil and gas remote monitoring, and the UAE government’s digital economy programme. Brazil leads Latin America at approximately 44.2% through connected vehicle fleet, agricultural IoT, and ANEEL-mandated smart electricity meter rollout.

Saudi Arabia’s Vision 2030 investment in smart infrastructure and South Africa’s utility M2M deployment represent significant secondary MEA market contributors, while Chile and Colombia are growing Latin American M2M markets driven by mining sector telemetry and urban infrastructure digitalisation investment.

Market Dynamics:

Growth Drivers: Industrial automation demand and 5G enabling latency-sensitive M2M applications

Industrial automation demand is the M2M market’s most commercially reliable growth driver. Every new Industry 4.0 programme creates M2M connectivity, device, and platform procurement whose scale compounds with industrial digitalisation pace globally. M2M delivers 22% reduction in machine downtime, 18% lower energy consumption, and 15% improved resource utilisation in controlled smart manufacturing implementations, providing quantifiable ROI that sustains procurement through economic cycle variation.

5G deployment creates technical infrastructure enabling M2M applications previously impossible on 4G. Ultra-reliable low-latency communication for industrial robot coordination, autonomous vehicle safety, and remote surgical device control requires sub-millisecond latency that 5G network slicing delivers. Each 5G coverage expansion creates the prerequisite for new M2M applications whose commercial adoption compounds with network availability growth.

Restraints: Cybersecurity risk and M2M protocol fragmentation creating integration complexity

Cybersecurity risk is the M2M market’s most significant adoption constraint. M2M networks generate continuous data streams from sensitive industrial, healthcare, and infrastructure assets whose compromise creates operational disruption, safety risk, and regulatory penalty. Each high-profile M2M security incident creates procurement hesitation across peer organisations whose risk assessment extends deployment timelines for new programmes.

M2M protocol standardisation fragmentation creates interoperability complexity that raises integration cost across multi-vendor deployments. Industrial M2M environments where equipment from different manufacturers communicates through incompatible protocols require middleware investment that adds technical complexity beyond hardware and connectivity procurement.

Opportunities: Healthcare remote monitoring and LPWAN enabling low-power M2M

Healthcare remote monitoring represents one of the most commercially compelling M2M growth opportunities. Remote patient monitoring for heart failure, diabetes, COPD, and hypertension demonstrates readmission reduction outcomes whose financial value to payers creates structured reimbursement motivation sustaining M2M medical device procurement.

LPWAN including NB-IoT and LTE-M creates commercially accessible M2M for billions of low-power devices. Smart metering, agricultural sensor networks, and supply chain asset tracking represent LPWAN M2M applications whose combined device count substantially exceeds industrial automation M2M in addressable market scope.

Recent Developments:

-

2024: Verizon Business launched an enhanced M2M platform with 5G-enabled IoT connectivity modules, targeting industrial automation and smart city applications with sub-millisecond latency and integrated edge computing.

-

2025: AT&T expanded its FirstNet M2M connectivity platform with dedicated channels for first responder vehicle telemetry, medical device connectivity, and public safety infrastructure monitoring with guaranteed quality of service.

-

2024: Cisco launched its IoT Operations Dashboard with enhanced M2M device management, real-time anomaly detection, and automated policy enforcement enabling enterprise operators to manage millions of M2M endpoints from a single AI-powered platform.

Machine-to-Machine (M2M) Market Key Players:

-

Verizon Communications

-

AT&T Inc.

-

Cisco Systems

-

Deutsche Telekom

-

Vodafone Group

-

Telenor Group

-

Telefonica S.A.

-

NTT Data Corporation

-

Intel Corporation

-

Sierra Wireless

-

Huawei Technologies

-

Ericsson

-

Nokia

-

Qualcomm

-

Texas Instruments

-

u-blox

-

Telit Cinterion

-

Murata Manufacturing

-

Gemalto (Thales)

-

Aeris Communications

Machine-to-Machine (M2M) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.87 Billion |

| Market Size by 2035 | USD 40.46 Billion |

| CAGR | CAGR of 4.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Wired, Wireless) • By Component (Hardware, Software, Services) • By Application (Industrial Automation, Utilities, Healthcare, Automotive, Retail, Others) • By End User (Manufacturing, Transportation & Logistics, Energy & Utilities, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Verizon Communications, AT&T Inc., Cisco Systems, Deutsche Telekom, Vodafone Group, Telenor Group, Telefonica S.A., NTT Data Corporation, Intel Corporation, Sierra Wireless, Huawei Technologies, Ericsson, Nokia, Qualcomm, Texas Instruments, u-blox, Telit Cinterion, Murata Manufacturing, Gemalto (Thales), and Aeris Communications |

Frequently Asked Questions

The Machine-to-Machine (M2M) Market is expected to grow at a CAGR of 4.60% from 2026 to 2035.

The Machine-to-Machine (M2M) Market was valued at USD 25.87 Billion in 2025.

Industrial automation demand creating measurable operational ROI, and 5G network deployment enabling ultra-low-latency M2M applications in manufacturing, healthcare, and autonomous vehicle sectors.

Hardware dominated the Machine-to-Machine (M2M) Market with approximately 62% share in 2025, while Software is the fastest growing with a CAGR of approximately 7.2%.

North America dominated the Machine-to-Machine (M2M) Market in 2025 with approximately 45% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch