Medical Device Testing Services Market Report Scope & Overview:

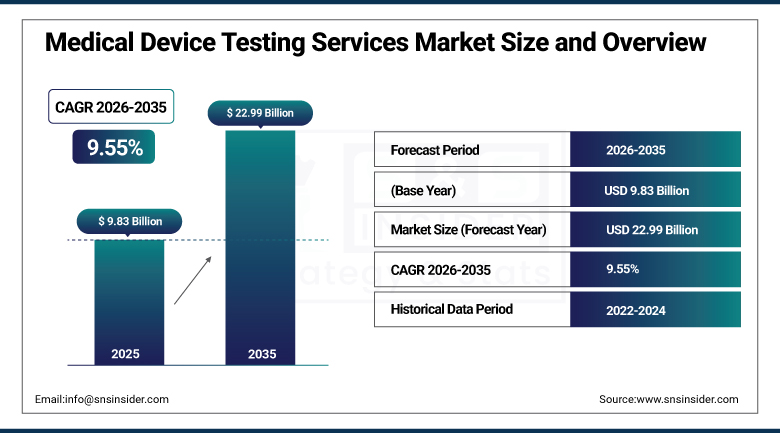

The Medical Device Testing Services Market was valued at USD 9.83 Billion in 2025 and is expected to reach USD 22.99 Billion by 2035, growing at a CAGR of 9.55% from 2026 to 2035.

This report identifies the prevalence and incidence of medical device related problems, which are creating a growing need for end to end testing and quality assurance services. The research analyzes healthcare expenditure on testing services by region, with significant differences driven by local healthcare infrastructures and regulatory frameworks. It also investigates regulatory and compliance trends, with a focus on changing standards and certifications needed for medical device approval. The study also considers technology and innovation's place in medical device testing, such as developments in testing processes, automation, and AI uses that boost efficiency and accuracy across the global testing services landscape.

In October 2024, NAMSA, a leader in MedTech Contract Research Organization offering end to end market access services, and TERUMO, a global player in medical technology, partnered to expand the regulatory approval and commercialization of Terumo's product portfolio. The partnership demonstrates the growing commercial value of integrated CRO services that combine clinical trial management, regulatory strategy, and testing capability under a single vendor relationship, reducing the coordination burden that medical device manufacturers face when navigating multi region regulatory approval pathways.

Market Size and Forecast:

-

Market Size in 2026E: USD 10.77 Billion

-

Market Size by 2035: USD 22.99 Billion

-

CAGR: 9.55% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Medical Device Testing Services Market - Request Free Sample Report

Medical Device Testing Services Market Trends:

-

Increasing incorporation of artificial intelligence and machine learning in testing services is enabling quicker, more precise medical device assessments, with AI based simulations and predictive analysis automating preclinical and clinical testing to save time and expense.

-

Growing popularity of telemedicine and remote healthcare devices is generating demand for advanced testing services, especially for wearable devices such as blood glucose meters and heart rate monitors requiring rigorous safety and accuracy validation.

-

Expanding healthcare infrastructure of emerging economies like India and China is offering key opportunities for medical device testing services providers to enter a fast increasing customer base across both domestic and export oriented manufacturing.

-

Stricter regulatory oversight of laboratory developed tests is classifying many diagnostic assays as medical devices, requiring manufacturers and laboratories to meet registration, reporting, and review requirements that drive greater demand for validation and compliance testing.

-

Growing focus on cybersecurity validation and digital twin simulations for connected medical devices is reshaping testing service portfolios as device manufacturers integrate software components requiring specialized security assessment alongside conventional safety testing.

U.S. Medical Device Testing Services Market Outlook:

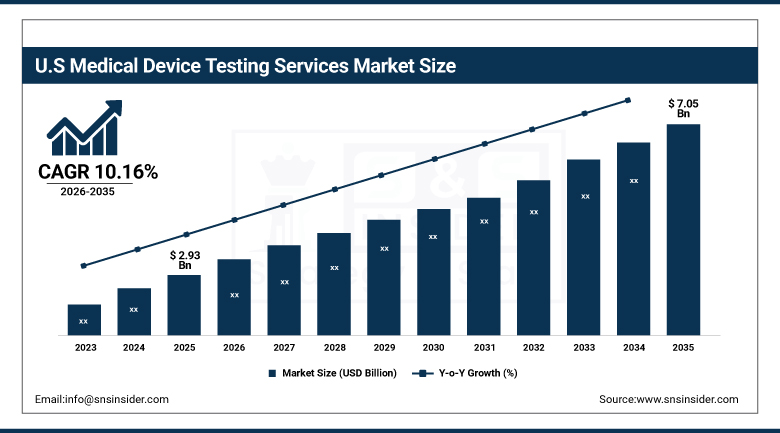

The U.S. Medical Device Testing Services Market was valued at approximately USD 2.93 Billion in 2025 and is expected to reach approximately USD 7.05 Billion by 2035, growing at a CAGR of approximately 10.16%.

In the United States, the medical device testing services industry is growing substantially because of rigorous regulation needs, increasing healthcare spending, and increased investment in technological advancements to guarantee the safety and efficacy of devices. The FDA's Medical Device Reporting regulation has obligated manufacturers to guarantee adherence to safety requirements, sustaining structured demand for testing services. The increasing incidence of chronic diseases, including diabetes and cardiovascular diseases, drives demand for products like glucose monitors, pacemakers, and diagnostic tools, further stimulating testing service needs across the country's extensive medical device manufacturing base.

In June 2023, NAMSA entered into a partnership with Terumo Aortic aimed at facilitating the market entry of Terumo Aortic's advanced aortic disease products. Within the framework of this partnership, NAMSA intended to provide Terumo Aortic with access to a network of clinical professionals and its highly specialized teams of experts in the field of cardiovascular healthcare, demonstrating the commercial value of specialized therapeutic area expertise within the broader medical device testing services landscape.

Medical Device Testing Services Market Segment Analysis:

-

By Service, the Biocompatibility Tests segment dominated the Medical Device Testing Services Market with approximately 34.00% share in 2025, while the Microbiology and Sterility Test segment is the fastest growing.

-

By Phase, the Preclinical segment dominated the Medical Device Testing Services Market with approximately 61.00% share in 2025, while the Clinical segment is the fastest growing.

By Service, biocompatibility tests dominate, chemistry tests grow fastest

Biocompatibility tests held the largest proportion of the medical device testing services market at 40.2% in 2025. The reason behind this is the paramount need for biocompatibility testing to ensure that medical devices are safe to use on humans. Since medical devices come into direct contact with the body, biocompatibility testing is necessary to determine possible toxicological hazards and make sure that the device does not trigger any adverse reactions. Increasing regulation and the number of medical device clearances worldwide have had a major role in increasing the demand for biocompatibility tests, with ISO 10993 requirements applying across all device classes creating non discretionary testing volume that sustains the segment's commercial dominance. Due to their importance for product compliance and safety, biocompatibility tests are anticipated to continue holding a strong grip on the market in the coming years.

Chemistry testing is the fastest growing segment in the medical device testing services sector. Chemistry testing is critical for analyzing the chemical composition and integrity of medical devices to establish that materials utilized in product development are harmless, durable, and operational. The industry is anticipated to develop at high speed as the complexity of devices used in healthcare increases, with growing demand for analysis of leachables and extractables, material characterization, and polymer composition validation that more sophisticated implantable and combination products require. Each new device material innovation that creates novel chemical compositions requiring characterization sustains chemistry testing's accelerating growth trajectory throughout the forecast period.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Medical Device Testing Services Market Insights

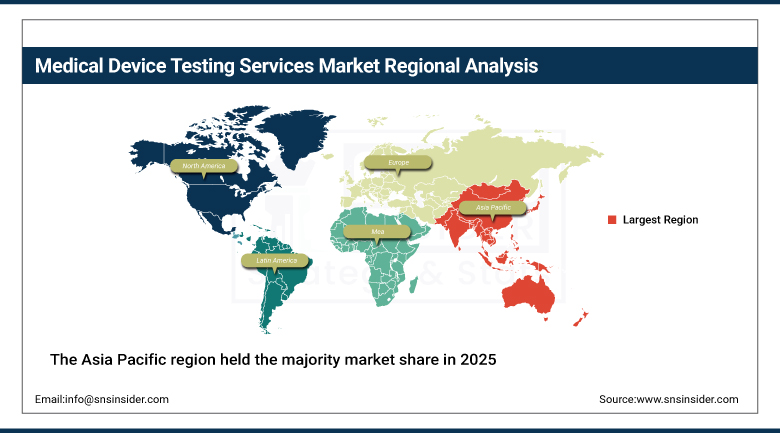

The Asia Pacific region held the majority market share in 2025 within the medical device testing services market, inspired by the rising demand for medical devices as well as the greater emphasis on regulatory compliance in markets such as China, India, and Japan. The region's strong healthcare infrastructure, increasing healthcare spending, and increasing manufacturing capacity for medical devices are the reasons for dominance. The increasing trend of outsourcing in nations such as China and India has driven the demand for test services further, with China accounting for approximately 44.8% of Asia Pacific revenues through its strict product approval standards and significant global export volume of medical devices.

India represents the most commercially dynamic emerging market within Asia Pacific where contract research organizations are investing heavily due to lower cost and availability of skilled labor, with the country's Central Drugs Standard Control Organization mandating third party lab testing for higher risk device classes that sustains above average regional testing services procurement growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Medical Device Testing Services Market Insights

The North American region for medical device testing services, on the contrary, is expected to have the highest CAGR during the forecast period. This growth is largely due to strict regulatory requirements imposed by the FDA and other regulatory authorities, which compel a high need for testing services to maintain compliance, alongside the world's most extensive network of FDA registered testing laboratories. The United States accounts for approximately 87.4% of North American revenues through Eurofins Scientific, SGS SA, Pace Analytical Services, and NAMSA's commercial operations.

Canada contributes complementary North American revenue through its growing medical device manufacturing sector and increasing collaboration with U.S. based testing laboratories for cross border regulatory approval pathways.

Europe Medical Device Testing Services Market Insights

Europe is a technically sophisticated medical device testing services market where re certification traffic from the Medical Device Regulation continues creating structured institutional demand that will persist into the late 2020s. Germany accounts for approximately 22.3% of European revenues through its strong medical device manufacturing base and rigorous notified body certification ecosystem.

The United Kingdom and France are significant secondary markets where harmonized EU regulations and strong medical device R&D activities create consistent procurement. TÜV SÜD's German headquarters and SGS's Swiss operations sustain regional commercial supply across the continent's testing services landscape.

MEA & Latin America Medical Device Testing Services Market Insights

The UAE leads MEA revenues through its growing medical device import and regulatory approval sector requiring third party testing validation across Gulf healthcare markets, free trade zone manufacturing hubs, and expanding hospital infrastructure. Saudi Arabia's Vision 2030 healthcare modernization program adds substantial complementary regional demand across both public and private healthcare systems. Brazil leads Latin American revenues through its growing domestic medical device manufacturing sector and ANVISA regulatory testing requirements. Mexico's expanding medical device export industry and Argentina's growing healthcare infrastructure investment collectively sustain regional market development through 2035.

Market Dynamics:

Growth Drivers: Rising medical device demand and stringent regulatory testing requirements

As healthcare infrastructure all over the world is evolving, the demand for effective and safe medical devices has grown significantly. The FDA and CE regulate stringent testing standards for approval, driving the need for expert testing services. The FDA's Medical Device Reporting regulation has obligated manufacturers to guarantee adherence to safety requirements, thus increasing demand for testing services. The increasing incidence of chronic diseases, including diabetes and cardiovascular diseases, drives demand for products like glucose monitors, pacemakers, and diagnostic tools, further stimulating testing service needs.

Advances in medical devices, such as wearables and AI driven solutions, require new testing methodologies, contributing to demand. The growth of personalized medicine and the trend toward home healthcare are contributing factors, as more devices must undergo rigorous testing for both safety and efficacy before they can reach consumers, sustaining structured testing services demand growth that compounds with the global medical device industry's overall innovation trajectory.

Restraints: High testing costs and multi-jurisdictional regulatory complexity

Medical device testing services, particularly those that entail extensive clinical trials or equipment specializations, may be exorbitantly costly. This limits small businesses from fully testing products, thus excluding them from market participation. It may cost upwards of USD 30 million to bring a medical device to market, with lengthy testing stages. Dealing with intricate regulations in various regions presents an additional level of complexity, as manufacturers have to deal with different standards such as FDA regulations in the United States and CE markings in Europe, which can slow down product development and drive up testing expenses.

This regulatory complexity is especially daunting for startups or small manufacturers, as they do not have the resources to handle multiple compliance requirements in international markets. These financial and regulatory problems can limit the growth of testing services in the medical device industry, particularly among smaller manufacturers whose limited capital budget constrains their ability to pursue comprehensive multi market regulatory testing pathways simultaneously.

Opportunities: AI integration and emerging market healthcare infrastructure expansion

The incorporation of artificial intelligence and machine learning in testing services is a thrilling prospect for quicker, more precise medical device assessments. AI based simulations and predictive analysis can automate preclinical and clinical testing, saving time and expense. The development of personalized medicine also creates new possibilities, as medical devices for individual patient requirements demand new test methods to guarantee their safety and effectiveness.

The increasing popularity of telemedicine and remote healthcare devices generates demand for advanced testing services, especially for wearable devices such as blood glucose meters and heart rate monitors. Growing the healthcare infrastructure of emerging economies like India and China also offers key opportunities for medical device testing services providers to enter a fast increasing customer base, with the increasing emphasis on maximizing patient outcomes as well as curtailing healthcare expenditure also offering favorable conditions for increasing the size of the medical device testing services market.

Recent Developments:

-

2024: NAMSA partnered with TERUMO in October 2024 to expand the regulatory approval and commercialization of Terumo's product portfolio, providing access to NAMSA's clinical professional network.

-

2025: Nelson Labs launched a groundbreaking rapid sterility testing capability in March 2025 to notably expedite product sterility results for medical device manufacturers.

-

2025: Medistri announced expansion in Hungary in January 2025 to improve access to healthcare solutions, providing sterilization capacity of more than 15,000 pallets per year.

-

2023: NAMSA entered into a partnership with Terumo Aortic in June 2023 to facilitate market entry of Terumo Aortic's advanced aortic disease products through specialized clinical and testing expertise.

-

2024: UPM Biomedicals introduced FibGel in October 2024, a natural injectable hydrogel for permanent implantable medical devices, expanding the materials requiring biocompatibility and chemistry testing validation.

Medical Device Testing Services Market Key Players:

-

Eurofins Scientific SE

-

SGS SA

-

Intertek Group plc

-

Pace Analytical Services LLC

-

WuXi AppTec Co. Ltd.

-

TÜV SÜD AG

-

Sterigenics International LLC

-

American Preclinical Services LLC

-

North American Science Associates Inc.

-

Charles River Laboratories International Inc.

-

Toxikon Inc.

-

NAMSA

-

Nelson Laboratories LLC

-

Medistri SA

-

BSI Group

-

DEKRA SE

-

Underwriters Laboratories Inc.

-

Element Materials Technology

-

WuXi Diagnostics

- Boston Analytical

Medical Device Testing Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.83 Billion |

| Market Size by 2035 | USD 22.99 Billion |

| CAGR | CAGR of 9.55% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Service (Biocompatibility Tests, Chemistry Test, Microbiology and Sterility Test, and Package Validation) • by Phase (Preclinical and Clinical) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Eurofins Scientific SE, SGS SA, Intertek Group plc, Pace Analytical Services LLC, WuXi AppTec Co. Ltd., TÜV SÜD AG, Sterigenics International LLC, American Preclinical Services LLC, North American Science Associates Inc., Charles River Laboratories International Inc., Toxikon Inc., NAMSA, Nelson Laboratories LLC, Medistri SA, BSI Group, DEKRA SE, Underwriters Laboratories Inc., Element Materials Technology, WuXi Diagnostics, Boston Analytical |

Frequently Asked Questions

The Medical Device Testing Services Market is expected to grow at a CAGR of 9.55% from 2026 to 2035.

The Medical Device Testing Services Market was valued at USD 9.83 Billion in 2025.

Growing demand for effective and safe medical devices driven by evolving global healthcare infrastructure, alongside stringent FDA and CE regulatory testing standards that obligate manufacturers to guarantee adherence to safety requirements and drive structured demand for expert testing services.

Biocompatibility Tests dominated the Medical Device Testing Services Market with a 40.2% share in 2025, while the Chemistry Test segment is the fastest growing.

Asia Pacific held the majority market share in 2025, while North America is expected to register the highest CAGR through 2035 due to stringent FDA regulatory requirements.

Get in Touch