Medical Robotics Market Report Scope & Overview:

The Medical Robotics Market was valued at USD 23.50 billion in 2025 and is expected to reach USD 102.75 billion by 2035, growing at a CAGR of 16.19% from 2026-2035.

The Global Medical Robotics Market reflects transformative growth propelled by converging trends of increasing burden of chronic disease, rising ageing of global population, accelerating tech innovation, increasing healthcare system emphasis on precision, efficiency and better patient outcomes. Such applications include surgical robotic systems, rehabilitation robots, hospital logistics robots, and pharmacy automation platforms, all of which transform clinical workflows in hospitals, ambulatory surgery centers, and rehabilitation facilities around the globe.

The U.S. Food and Drug Administration (FDA) has laid the groundwork to support this expansion by creating focused regulatory pathways for medical robotic devices such as the De Novo pathway that meant approval of the Virtual Incision's MIRA miniaturized robotic surgery system in February 2024 as the first of its kind and the 510(k) clearance of Intuitive Surgical's da Vinci 5 in March 2024, showing the FDA was alive and well in driving next-generation medical robotics technology to clinical practice.

Also, the Centers for Medicare & Medicaid Services (CMS) has steadily increased the reimbursement coverage for robotic-assisted surgical procedures in numerous specialties (urology, gynecology, orthopedics, and general surgery) in the ambulatory surgery center environments, thereby removing an economic barrier to adoption and stimulating investment in robotic surgical platforms at US health care facilities.

Medical Robotics Market Size and Forecast

-

Market Size in 2025: USD 23.50 Billion

-

Market Size by 2035: USD 102.75 Billion

-

CAGR: 16.19% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Medical Robotics Market - Request Free Sample Report

Medical Robotics Market Trends

-

Rapid adoption of robotic-assisted surgical systems across urology, gynecology, orthopedics, and general surgery is expanding clinical indications and procedure volumes for surgical robotics globally.

-

Growing integration of artificial intelligence and machine learning into surgical guidance, intraoperative imaging, and clinical decision support is enhancing surgical precision and safety outcomes.

-

Expansion of rehabilitation robotics for neurological, musculoskeletal, and post-surgical recovery applications is creating significant new demand driven by aging population demographics.

-

Rising deployment of hospital logistics robots for medication delivery, disinfection, patient transport, and materials management is improving healthcare facility operational efficiency.

-

Development of compact, lower-cost robotic platforms specifically designed for ambulatory surgery centers is democratizing access to robotic-assisted surgical capabilities beyond major academic medical centers.

-

Increasing investment in surgeon training platforms including simulation and virtual reality systems is accelerating the expansion of the robotic-procedure-trained surgeon community globally.

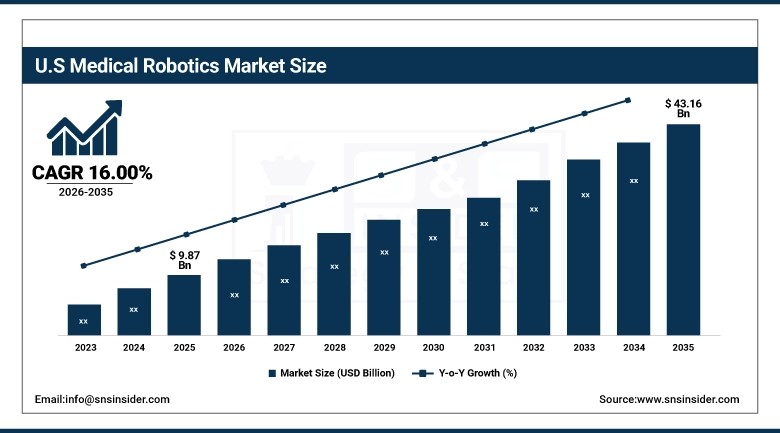

U.S. Medical Robotics Market Size Outlook:

The U.S. Medical Robotics Market was valued at USD 9.87 billion in 2025 and is expected to reach USD 43.16 billion by 2035, growing at a CAGR of 16.00% from 2026-2035. The US represents the largest Medical Robotics Market globally, featuring the highest number of robotic surgical system installations, prominent clinical research programs, and the global headquarters of numerous market leaders (e.g., Intuitive Surgical, Stryker, Medtronic and Zimmer Biomet). The confluence of CMS reimbursement policies that back robotic-assisted procedures over an expanding range of balanced surgical applications, plus high volume surgical case loads at larger U.S. hospital systems, render the setting of an especially advantageous commercialization market place.

There were more than 2.63 million robotic-assisted surgical procedures performed in the United States in 2024 alone, as reported by Intuitive Surgical and the American Hospital Association which highlights the extraordinary depth of current clinical adoption, combined with its high-volume platform for continued market expansion.

This leadership position continues to be buttressed by the persistent funding of the U.S. National Institutes of Health (NIH) for research into robotic-assisted surgical techniques, rehabilitation robotics for neurological recovery, and exoskeleton technology for the mobility-impaired patient population — maintaining a pipeline of clinical evidence and translational innovation that continues to underwrite the competitive advantage of the U.S. market in the development and clinical use of medical robotics technology.

Medical Robotics Market Segment Highlights

-

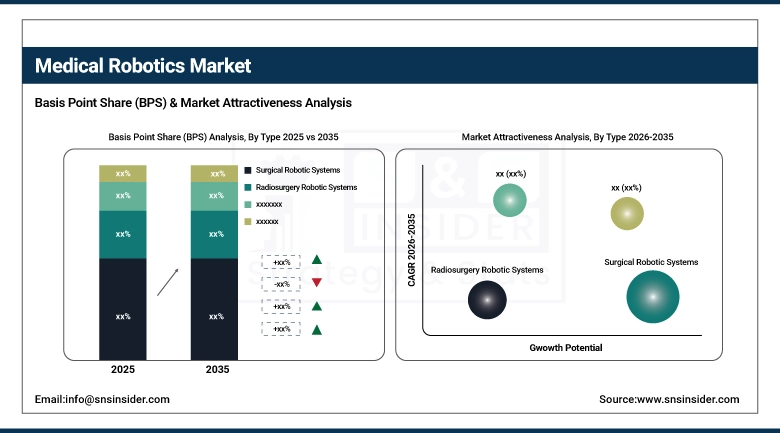

By Type, Surgical Robotic Systems dominated with 44% share in 2025; Rehabilitation Robotic Systems fastest growing (CAGR 18.31%).

-

By End User, Hospitals & Clinics dominated with 45% share in 2025; Ambulatory Surgery Centers fastest growing (CAGR 18.70%).

By Type, Surgical Robotic Systems segment dominates the Medical Robotics Market, Rehabilitation Robotic Systems segment expected to grow fastest

Research has classified the Medical Robotics Market into three segments; Surgical Robotic Systems, Ancillary Surgical Robotic Systems, and Non-Invasive Robotic Surgery Tools / Systems. Surgical Robotic Systems accounted for the leading segment share of around 44% in 2025, driven by widespread and increasing adoption of robotic-assisted surgery in various high-volume clinical specialties. These systems allow surgeons to perform complex sur-gery through small incisions with greater dexterity, superior 3D imaging, and the ability to eliminate filtered tremor which combine to enable higher precision and better patient outcomes for surgeries like prostatectomies and hysterectomies. However, with a leadership of Intuitive Surgical's da Vinci platform as the global surgical robotics system, sustained procedure volume growth across the base of established indications, and a new wave of competitive offerings with expanded niches from Medtronic, Stryker, and Johnson & Johnson, the potential for even greater overall adoption rates fueled by devices is evident as OEMs from adjacent and traditional industries either innovate in surgical robotics or price pressure these traditional niches, expanding competitive options.

Analysis By 2035, the Rehabilitation Robotic Systems segment is projected to witness the greatest CAGR of around 18.31%, driven by the combined effect of an aging global population with an increasing burden of neurological disorders, stroke, musculoskeletal disorders and, post-restorative surgery requirements that exceeds the capacity of traditional therapy resources. Such systems are providing physiotherapy protocols that are becoming more tailored to the patient, the real-time monitoring of patient progress and adaptive resistance that are extensively improving the functional recovery outcome with AI-enabled Rehabilitation Robots. The growth of home-based rehabilitation robotics allowing patients to conduct therapy outside of clinical environments is creating an immense new addressable market which will significantly enhance segment growth throughout the forecast period.

By End User, Hospitals & Clinics segment dominates the Medical Robotics Market, Ambulatory Surgery Centers segment expected to grow fastest

Hospitals & Clinics segment accounted for the largest share 45% among the other end users in the Medical Robotics Market in 2025 owing to these institutions being able to implement all the models of the spectrum of the technology from complex multi-arm surgical systems, to hospital logistics robots, and pharmacy automation platforms. Furthermore, large hospital systems are the primary early adopters of medical robotics, having the requisite financial resources, surgical case volumes, training infrastructure, and patient population characteristics to optimize the economics of high-capital robotic system investments in their entirety as opposed to individual health-care providers or community hospitals . The presence of the da Vinci robotic surgical system in thousands of hospitals around the world is an example of the extent to which robotic technology is integrated into the hospital end-user segment on a worldwide scale.

This segment is likely to grow at the highest CAGR of 18.70% during the forecast period, owing to increasing patient preference for outpatient care in Ambulatory Surgery Centers (ASCs). Pressure on costs, coupled with high patient preference for same-day surgical procedures, has been pushing expansion outpatient surgical infrastructure globally and is supporting a rapid increase in ASC adoption of robotic surgical systems. The expansion of CMS reimbursement has gradually added higher-acuity robotic-assisted procedures to ASC coverage lists, facilitating a migration of certain procedures from hospital to an ASC setting. Both more precise robotic systems with smaller footprints and lower overall consumable costs specifically designed for use in ASC environments, all contribute to creating a sustainable future robotic surgery market, yet continue to bring a larger portion of the rapidly growing millions of ASC procedures performed every calendar year internationally.

Medical Robotics Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

85% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

UAE |

32% |

|

Latin America |

Brazil |

52% |

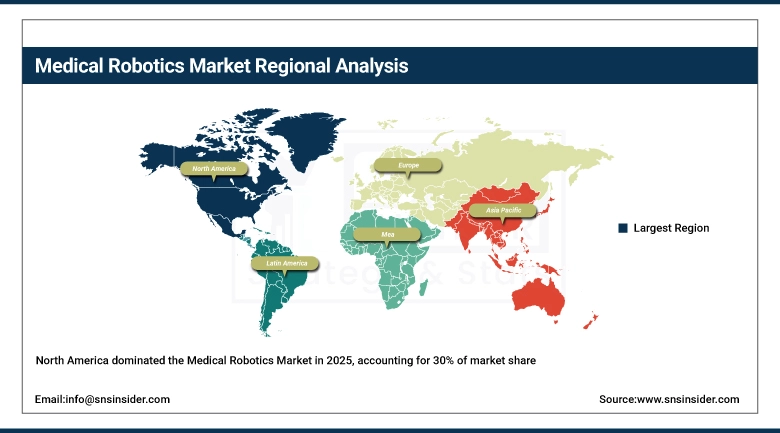

North America Medical Robotics Market Insights

The strong concentration of surgical robotics installations, rehabilitation robotics programs, and presence of advanced medical technology developers, particularly in the U.S., resulted in North America contributing roughly 30% of the global Medical Robotics Market in 2025. Europe has a strong healthcare infrastructure, reimbursements and early acceptance of minimally invasive robotic-assisted procedures. Innovation, economies of scale, and technological development across surgical, rehabilitation, and hospital automation robotics continues to be bolstered by the presence of leading companies like Intuitive Surgical, Medtronic, Stryker and Zimmer Biomet.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Medical Robotics Market Insights

Europe had 18% of the global Medical Robotics Market in 2025, supported by established healthcare systems and surgical robotics being implemented in Germany, France, the UK, Italy and Nordic countries. Regulatory frameworks like the EU Medical Device Regulation (MDR 2017/745) guarantee that robotic systems are of high standards regarding safety and quality, nurturing confidence on robots in the clinical arena. Germany remains a linchpin of regional expansion, and EU-supported programs such as Horizon Europe still fuel innovation in a variety of AI-assisted surgical systems, rehabilitation robotics and new hospital automation technologies.

Asia Pacific Medical Robotics Market Insights

The Asia Pacific Region approximately acquired 28% of the global Medical Robotics Market in 2025 and still dominate the fastest-growing region in this market due to the growing demand for healthcare infrastructure, huge ageing population, and growth in healthcare expenditures. Japan, China, South Korea and India are the top markets driving the adoption of robotic-assisted procedures. Surgical robotics in Japan is the most widely utilized, whilst the current regulatory environment in China is extremely favorable, and coupled with government funding parties are investing smartly in healthcare to increase local innovation and implementation of medical robotic systems as part of the ecosystem of its hospitals.

Middle East & Africa Medical Robotics Market Insights

The Medical Robotics Market was valued at 11.52 billion in the Middle East & Africa region in 2025, contributing approximately 9% worldwide, driven by ongoing healthcare modernization and increasing investments in advanced medical technologies. The regional adoption of robotic-assisted surgical systems and hospital automation solutions is being led by countries including UAE, Saudi Arabia, and Israel where government-led healthcare initiatives and increasing medical tourism is creating demand for hospital automation and surgical instruments.

Latin America Medical Robotics Market Insights

Latin America held approximately 15% of the global Medical Robotics Market in 2025, due to the advancement in healthcare infrastructure along with the adoption of new surgical technologies in the region. The region is led by Brazil, with its vast health system and a growing investment in robotic surgery. Continuous expansion in the private healthcare networks and rising awareness over the benefits of minimally invasive procedures across the region is also aiding the market growth.

Medical Robotics Market Growth Drivers:

-

Rising global burden of chronic diseases and aging populations creating structural demand growth for robotic-assisted surgery, rehabilitation robotics, and healthcare automation systems

The rapid increase in incidence of chronic diseases such as cardiovascular diseases, musculoskeletal disorders, neurologic disorders, and cancers increases the pool of patients who require complex surgical and rehabilitative treatments relying on new robotic technologies. At the same time, the dramatic change in global population demographics towards older age structures is eliciting increasing surgical demand and concurrently the urgent challenge of rehabilitative capacity that robotic systems are uniquely well-suited to address. By decreasing surgical trauma and recovery time, medical robots allow for more involved procedures to be performed on patients too unstable for traditional open surgery, effectively broadening the eligible patient population.

According to the World Health Organization (WHO), the population aged 60 years and older will double from 1 billion to 2.1 billion by 2050, and the number aged 80 years and older will triple the increased number of elderly patient broke out a large-scale and sustained structural demand driver for medical robots in surgical, rehabilitation, mobility assistance, and care support market applications for all applications throughout the forecast period and beyond..

Medical Robotics Market Restraints:

-

High capital investment requirements for robotic surgical systems and specialized training programs limiting adoption among smaller healthcare facilities and institutions in resource-constrained emerging markets

High fixed costs involved in the procurement, servicing, and staffing of surgical teams to effectively deliver advanced medical robotic technology poses a meaningful structural barrier to market entry, mainly in small community hospitals and rural healthcare organisations, along with health systems in low-middle income courtiers. Robotic surgical platforms introduce capital inputs of several million dollars and ongoing proprietary consumables, annual service contracts, and staff and surgeon training packs, all very costly. This financial burden breeds a two-tier market that places sophisticated robotic capabilities in urban tertiary care centres with adequate resources while denying corresponding technology access to the community hospitals and rural facilities that serve the vast majority of surgical patients worldwide, sustaining geographic and socioeconomic disparity in the quality of surgical care.

Medical Robotics Market Opportunities:

-

Rapid advancement of AI-integrated medical robotics and telesurgery technologies opening transformative new growth pathways for remote surgical access and personalized robotic-assisted care globally

Advances in artificial intelligence, remote connectivity via the cloud and 5G telecommunications has allowed medical robotic systems to provide the next revolutionary leap in robotic-assisted care to previously underserved geographic areas via telesurgery and through remote robotic guidance platforms. Machine learning for surgical planning, intraoperative decision support and robotics is gradually diminishing the thresholds of degrees of surgeon skill required for effectively utilising robotic systems and thereby expanding the range of the clinician base, who can perform successful robotic surgery. When falling hardware costs, sparked by new entrants and design innovation, meet expanding reimbursement coverage and growing clinical evidence supporting robotic outcomes advantages, the combination is quickly driving the economic feasibility of medical robotics investment to broader scales both in terms of the types of healthcare facilities and the geographic markets it makes sense.

Recent Developments:

-

2025: In February 2025, Intuitive Surgical introduced an upgraded da Vinci surgical system with enhanced imaging capabilities and AI-assisted workflow optimization, improving procedural accuracy and efficiency for complex minimally invasive surgeries across North America and Europe.

-

2025: Medtronic expanded the URO clinical trial — the largest of its kind for robotic-assisted urologic surgery — in April 2025, demonstrating excellent safety and efficacy outcomes for the HUGO robotic-assisted surgery system and supporting expanded global regulatory submissions.

-

2024: In March 2024, Intuitive Surgical received FDA 510(k) clearance for da Vinci 5, the company's next-generation multiport robotic surgical system, incorporating enhanced force feedback, improved visualization, and advanced data analytics capabilities for complex minimally invasive procedures.

-

2024: In February 2024, Virtual Incision Corporation received FDA De Novo pathway authorization for the MIRA Surgical System — the world's first miniaturized robotic-assisted surgery device — cleared for adult colectomy procedures and designed specifically to enable robotic surgery in space-constrained settings.

-

2024: Stryker expanded its Mako SmartRobotics platform in June 2024 with next-generation software enhancements and real-time intraoperative data capabilities, strengthening its position in robotic-assisted orthopedic joint replacement procedures across global hospital networks.

-

2023: Medtronic received FDA approval in November 2023 for its Symplicity Spyral minimally invasive renal denervation system for hypertension management, expanding the medical robotics portfolio into a new therapeutic indication with immediate U.S. commercial launch.

Medical Robotics Companies are:

-

Medtronic plc

-

Stryker Corporation

-

Zimmer Biomet Holdings, Inc.

-

Johnson & Johnson (Ethicon/DePuy Synthes)

-

Smith & Nephew plc

-

NuVasive, Inc.

-

Ekso Bionics Holdings, Inc.

-

ReWalk Robotics Ltd.

-

Asensus Surgical, Inc.

-

Omnicell, Inc.

-

Renishaw plc

-

Cyberdyne Inc.

-

Bionik Laboratories Corp.

-

Lifeward, Inc.

-

Zap Surgical Systems, Inc.

-

DIH Holdings US, Inc.

-

Arxium, Inc.

-

Accuray Incorporated

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 23.50 Billion |

| Market Size by 2035 | USD 102.75 Billion |

| CAGR | CAGR of 16.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Surgical Robotic Systems, Rehabilitation Robotic Systems, Radiosurgery Robotic Systems, Hospital & Pharmacy Robotic Systems) • By End User (Hospitals & Clinics, Ambulatory Surgery Centers, Pharmacies, Rehabilitation Centers, Other End Users) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intuitive Surgical, Inc., Medtronic plc, Stryker Corporation, Zimmer Biomet Holdings, Inc., Johnson & Johnson (Ethicon/DePuy Synthes), Smith & Nephew plc, Globus Medical, Inc., NuVasive, Inc., Ekso Bionics Holdings, Inc., ReWalk Robotics Ltd., Asensus Surgical, Inc., Omnicell, Inc., Renishaw plc, Cyberdyne Inc., Bionik Laboratories Corp., Lifeward, Inc., Zap Surgical Systems, Inc., DIH Holdings US, Inc., Arxium, Inc., Accuray Incorporated |

Frequently Asked Questions

Ans: Asia Pacific is the fastest-growing region in the Medical Robotics Market.

Ans: North America dominated the Medical Robotics Market in 2025.

Ans: The Surgical Robotic Systems segment dominated the Medical Robotics Market with approximately 44% share in 2025.

Ans: The Medical Robotics Market was valued at USD 23.50 billion in 2025

Ans: The Medical Robotics Market is expected to grow at a CAGR of 16.19% from 2026 to 2035.

Get in Touch