Millimeter Wave Technology Market Report Scope & Overview:

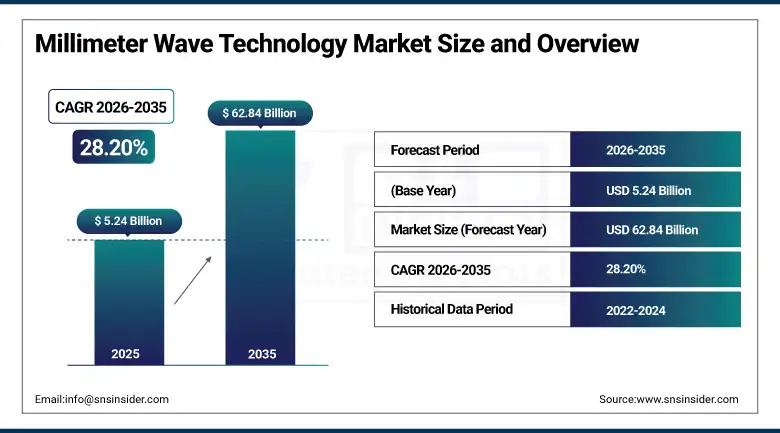

The Millimeter Wave Technology Market was valued at USD 5.24 Billion in 2025 and is expected to reach USD 62.84 Billion by 2035, growing at a CAGR of 28.20% from 2026–2035.

Millimeter wave technology operates across the electromagnetic frequency range of 30 to 300 GHz, occupying the spectral territory between conventional microwave frequencies and the terahertz domain, and delivers a combination of high bandwidth availability, precise beam directionality, and short wavelength propagation characteristics that uniquely enable the ultra-high-speed wireless data transmission, high-resolution imaging, and precise distance and velocity measurement that define the most commercially compelling technology frontiers of the current decade. The commercial significance of millimeter wave frequencies rests on their enormous available bandwidth, which exceeds that of all lower radio frequencies combined across the 30 to 300 GHz range, enabling wireless data throughput rates of multiple gigabits per second per link that 5G cellular, and satellite communications systems require to serve the exponentially growing demand for mobile data bandwidth.

In Q2 2025, Qorvo acquired mmWave startup TenX for USD 120 million to strengthen its position in the 5G and wireless infrastructure market, integrating TenX's millimeter wave chip technology into Qorvo's radio frequency semiconductor portfolio. The acquisition reflected the strategic importance of millimeter wave semiconductor expertise in the 5G infrastructure supply chain whose base station, backhaul, and customer premises equipment markets represent multi-billion-dollar annual procurement from wireless carriers whose 5G network densification investment creates sustained demand for millimeter wave front-end module components.

Market Size and Forecast

-

Market Size in 2026E: USD 6.71 Billion

-

Market Size by 2035: USD 62.84 Billion

-

CAGR: 28.20% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Millimeter Wave Technology Market - Request Free Sample Report

Millimeter Wave Technology Market Trends

-

Rapid 5G network expansion is driving investments in millimeter wave infrastructure to deliver ultra-high-speed connectivity in dense urban areas.

-

Fixed wireless access (FWA) solutions are gaining traction as cost-effective alternatives to fiber broadband deployment.

-

Increasing adoption of millimeter wave radar in vehicles is supporting advanced driver assistance systems (ADAS) and autonomous driving technologies.

-

Growing deployment of millimeter wave security screening systems is enhancing threat detection in airports and critical infrastructure facilities.

-

Advances in semiconductor integration and chip miniaturization are enabling broader adoption of millimeter wave technology across consumer, automotive, industrial, and defense applications.

The U.S. Millimeter Wave Technology Market Outlook

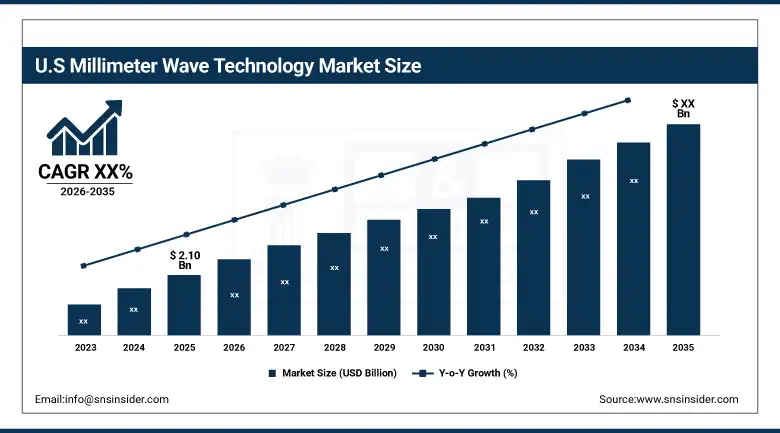

The U.S. Millimeter Wave Technology Market was valued at approximately USD 2.10 Billion in 2025 and is expected to grow significantly through 2035. North America held the highest millimeter wave technology market share of 40.1% in 2024, driven by significant investments in advanced telecommunications infrastructure and the early adoption of 5G technology.

The United States millimeter wave technology market is driven by the FCC's allocation of millimeter wave spectrum in the 24 GHz, 28 GHz, 39 GHz, and 47 GHz bands for 5G use whose commercial licensing by Verizon, AT&T, and T-Mobile has initiated the world's largest millimeter wave 5G network deployment programme. Verizon's Ultra Wideband network using millimeter wave spectrum in major metropolitan areas demonstrates the commercial viability of millimeter wave 5G for stadium, arena, and dense urban venue connectivity whose gigabit-speed indoor and outdoor coverage requirements exceed what sub-6 GHz 5G can deliver at equivalent base station density.

In January 2024, Qualcomm launched the Snapdragon X70 modem incorporating enhanced millimeter wave connectivity with AI-powered dynamic signal optimization, improving millimeter wave 5G coverage continuity and data throughput in mobile handset applications whose beam management and handoff challenges between dense small cells had previously constrained the consumer experience of millimeter wave 5G relative to sub-6 GHz alternatives. The modem's AI-driven beam tracking maintained millimeter wave connection continuity across user movement scenarios that prior-generation mmWave modems handled with connectivity interruptions.

Millimeter Wave Technology Market Segment Analysis

-

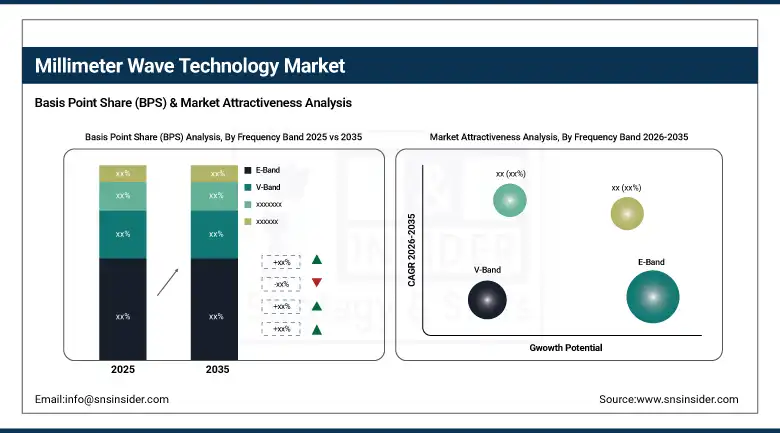

By Frequency Band, E-Band segment dominated the millimeter wave technology market with approximately 61.2% share in 2025, while the V-Band segment is the fastest growing frequency band driven by its growing use in wireless broadband, unlicensed 5G, and short-range communications.

-

By Component, telecommunication equipment segment dominated the millimeter wave technology market with approximately 55.3% share in 2025, while the imaging & scanning systems segment is the fastest growing component driven by advances in medical imaging, security screening, and industrial inspection applications.

-

By End User, telecommunications segment dominated the millimeter wave technology market with approximately 46.7% share in 2025, while the military & defense segment is the fastest growing end user driven by advancements in radar, surveillance, and secure communication systems.

By Frequency Band, E-Band dominates, V-Band grows fastest

E-Band retained the dominant frequency band position with approximately 61.2% of the millimeter wave technology market in 2025. E-Band's commercial primacy reflects its widespread adoption in point-to-point microwave backhaul links whose licensed 71-76 GHz and 81-86 GHz spectrum bands. Combined with the atmospheric window that minimizes oxygen absorption at these frequencies, enable high-capacity, long-range wireless backhaul links whose combination of gigabit-class capacity and multi-kilometer reach makes them the preferred wireless backhaul technology for connecting 5G base stations to fiber network access points in the dense urban environments where millimeter wave 5G is most commercially deployed.

V-Band is growing fastest driven by the growing commercialization of unlicensed 60 GHz spectrum for wireless broadband, indoor wireless LAN enhancement, and short-range device interconnection applications whose low infrastructure cost and license-free operation make V-Band technology accessible to enterprise, residential, and consumer electronics markets beyond the carrier-grade E-Band backhaul market. The IEEE 802.11ad and 802.11ay Wi-Fi standards whose 60 GHz operation enables multi-gigabit wireless LAN are creating V-Band adoption in high-performance Wi-Fi applications, while fixed wireless access systems operating at 60 GHz are creating a growing residential broadband delivery market in dense apartment and commercial building environments.

By End User, telecommunications dominates, military & defense grows fastest

Telecommunications retained the dominant end user position with approximately 46.7% of the millimeter wave technology market in 2025, driven by the global 5G network deployment whose millimeter wave spectrum allocation, base station procurement, and backhaul infrastructure investment collectively represent the largest single commercial millimeter wave technology demand category by revenue. The telecommunications sector's millimeter wave demand encompasses 5G new radio base stations operating at 28 GHz and 39 GHz, E-Band microwave backhaul links connecting base stations to fibre, fixed wireless access customer premises equipment, and satellite ground station equipment whose combined procurement scales with the global wireless network investment cycle that is at its most active phase since the 3G rollout of the early 2000s.

Military and defense is growing fastest as the strategic and tactical communication, radar surveillance, precision targeting, and electronic warfare applications of millimeter wave frequencies create government-funded procurement whose national security budget independence from commercial economic cycles provides growth consistency that telecommunications investment cannot sustain through the capital expenditure cycles of carrier network build programmes. Millimeter wave radar for missile defence systems, airborne synthetic aperture radar for reconnaissance, and vehicle-mounted counter-IED systems each represent premium-priced defence procurement categories whose millimeter wave component requirements sustain a high-value military demand segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Asia Pacific |

China |

38.5% |

|

Europe |

Germany |

28.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Millimeter Wave Technology Market Insights

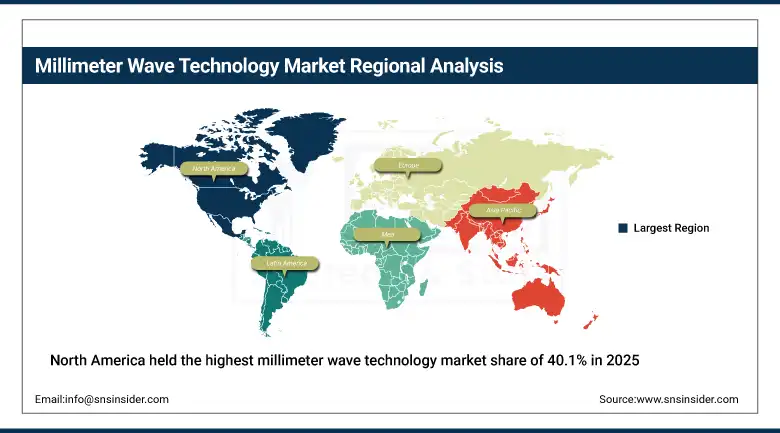

North America held the highest millimeter wave technology market share of 40.1% in 2025, driven by the world's most advanced millimeter wave 5G network deployment programme whose Verizon Ultra Wideband, AT&T mmWave, and T-Mobile millimeter wave investments are creating the largest commercial millimeter wave base station infrastructure in the world. The United States accounts for approximately 82.5% of North American revenues through its combined telecommunications infrastructure investment, defence procurement, and semiconductor industry development of millimeter wave integrated circuit technology whose commercial availability drives adoption across multiple application categories. Canada contributes supplementary demand through its millimeter wave 5G spectrum auction activity and growing fixed wireless access deployment in urban and suburban markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Millimeter Wave Technology Market Insights

Asia Pacific is the fastest-growing regional millimeter wave technology market, driven by China's world-leading 5G deployment scale whose mid-band dominance is progressively supplemented by millimeter wave deployment in high-traffic urban venues, Japan's mature millimeter wave 5G network whose carrier investment has created advanced urban millimeter wave coverage, and South Korea's 5G leadership whose early millimeter wave spectrum assignment created one of the world's first commercial millimeter wave 5G networks. China accounts for approximately 38.5% of Asia Pacific revenues through the scale of its domestic 5G infrastructure investment, the commercial presence of Huawei and ZTE whose millimeter wave equipment portfolios serve both domestic and international markets, and the government's strategic investment in millimeter wave technology as a national competitiveness priority.

Japan and South Korea each contribute premium regional demand through their mature millimeter wave 5G networks, automotive radar technology leadership from Toyota, Honda, Samsung, and Hyundai, and the consumer electronics industries whose millimeter wave Wi-Fi integration in premium laptops and gaming devices creates growing consumer market demand. India is the most commercially dynamic emerging millimeter wave market within Asia Pacific where spectrum auction activity and 5G network rollout are creating new infrastructure investment demand.

Europe Millimeter Wave Technology Market Insights

Europe held a significant share of the global millimeter wave technology market in 2025. Germany, Finland, Sweden, the United Kingdom, and the Netherlands are the leading national markets whose telecommunications equipment manufacturing, 5G network deployment, and aerospace and defence sectors create diverse millimeter wave demand. Germany accounts for approximately 28.5% of European revenues through the commercial presence of Ericsson, Nokia, and Rohde & Schwarz whose millimeter wave equipment and test and measurement capabilities sustain European market development, and the German automotive industry's advanced driver assistance system radar sensor procurement.

MEA & Latin America Millimeter Wave Technology Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its advanced 5G network deployment across Abu Dhabi and Dubai, government investment in smart city millimeter wave sensing infrastructure, and the military procurement of millimeter wave radar and communications systems. Saudi Arabia's Vision 2030 digital transformation programme and its growing telecommunications infrastructure investment create expanding millimeter wave demand.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its 5G spectrum auction activity and progressive carrier network investment, with Claro, TIM, and Vivo each deploying millimeter wave capability in major urban venues. Mexico and Chile contribute growing secondary market demand through their telecommunications modernization programmes.

Market Dynamics

Growth Drivers: Global 5G network deployment creating massive millimeter wave infrastructure investment and automotive radar sensor proliferation driven by safety mandate regulations

The millimeter wave technology market's extraordinary growth rate is driven by two simultaneously accelerating demand forces whose commercial scale and technology specificity create a sustained multi-year investment cycle. Global 5G network deployment is simultaneously creating millimeter wave demand at the base station level, where dense urban coverage requires millimeter wave small cell infrastructure whose scale of deployment across major metropolitan areas represents the largest commercial millimeter wave system installation programme in history, and at the backhaul level, where E-Band microwave links connecting 5G cells to fibre create per-cell millimeter wave backhaul investment that multiplies with small cell count expansion. Automotive millimeter wave radar's simultaneous proliferation as a safety-critical sensing technology, driven by NHTSA mandatory automatic emergency braking requirements in the United States and Europe.

Restraints: High atmospheric attenuation of millimeter wave signals requiring dense infrastructure deployment and line-of-sight propagation constraints limiting coverage area per base station

Millimeter wave propagation's fundamental physics creates coverage challenges that require dense base station infrastructure investment disproportionate to the area covered relative to sub-6 GHz alternatives, creating higher per-square-kilometre network deployment cost whose economics limit millimeter wave 5G coverage buildout to the highest-traffic urban environments where the additional revenue from ultra-high-speed service justifies the infrastructure density investment. Rain, fog, and atmospheric moisture create signal attenuation that reduces link reliability in heavy precipitation conditions, requiring adaptive modulation and link budget margin planning that adds system complexity and reduces link efficiency. Building material penetration limitations of millimeter wave signals create indoor coverage challenges that require outdoor-to-indoor repeater systems or indoor small cell deployment for interior millimeter wave 5G coverage whose additional infrastructure cost compounds the per-location deployment economics.

Opportunities: Fixed wireless access broadband delivery and millimeter wave automotive sensing innovation represent high-growth commercial frontiers beyond 5G telecommunications

Fixed wireless access at millimeter wave frequencies represents the most commercially scalable near-term broadband market opportunity for millimeter wave technology beyond mobile 5G, enabling gigabit-speed broadband delivery to residential and enterprise customers in dense urban environments without the civil infrastructure disruption and construction timeline of fibre deployment. Each apartment building, office tower, or commercial district that receives millimeter wave fixed wireless access service creates a permanent broadband infrastructure whose revenue sustainability supports the initial deployment investment at economics that deteriorating customer concentration advantages over greenfield fibre in dense urban contexts. Millimeter wave automotive sensing innovation encompassing corner radar for parking assistance, long-range forward radar for adaptive cruise control and emergency braking, and the emerging 4D imaging radar whose angular resolution approaches camera performance creates a growing per-vehicle millimeter wave content.

Recent Developments:

-

2025: Qorvo acquired mmWave startup TenX for USD 120 million to strengthen its 5G and wireless infrastructure market position, integrating TenX's millimeter wave chip technology into Qorvo's RF semiconductor portfolio for telecommunications infrastructure applications.

-

2024: Qualcomm launched the Snapdragon X70 modem with AI-powered millimeter wave connectivity optimisation, improving mmWave 5G coverage continuity and data throughput through machine learning-enhanced beam management and tracking in mobile handset applications.

-

2024: Ericsson and Verizon expanded their millimeter wave 5G network deployment partnership, advancing the installation of dense urban mmWave small cell infrastructure across major U.S. metropolitan markets including New York, Chicago, and San Francisco whose data traffic density requires millimeter wave spectrum capacity.

Millimeter Wave Technology Market Key Players

-

Qualcomm Incorporated

-

Nokia Corporation

-

Ericsson AB

-

Samsung Electronics Co., Ltd.

-

Huawei Technologies Co., Ltd.

-

NEC Corporation

-

Fujitsu Limited

-

Intel Corporation

-

Keysight Technologies, Inc.

-

Anritsu Corporation

-

Texas Instruments Incorporated

-

NXP Semiconductors N.V.

-

Infineon Technologies AG

-

Analog Devices, Inc.

-

Qorvo, Inc.

-

Broadcom Inc.

-

Movandi Corporation

-

Siklu Communication Ltd.

-

Aviat Networks, Inc.

-

L3Harris Technologies, Inc.

Millimeter Wave Technology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.24 Billion |

| Market Size by 2035 | USD 62.84 Billion |

| CAGR | CAGR of 28.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Frequency Band (E-Band, V-Band, W-Band, D-Band, Others) • By Component (Telecommunication Equipment, Imaging & Scanning Systems, Radar & Satellite Systems, Others) • By End User (Telecommunications, Military & Defense, Automotive, Healthcare, Consumer Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Qualcomm Incorporated, Nokia Corporation, Ericsson AB, Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., NEC Corporation, Fujitsu Limited, Intel Corporation, Keysight Technologies, Inc., Anritsu Corporation, Texas Instruments Incorporated, NXP Semiconductors N.V., Infineon Technologies AG, Analog Devices, Inc., Qorvo, Inc., Broadcom Inc., Movandi Corporation, Siklu Communication Ltd., Aviat Networks, Inc., and L3Harris Technologies, Inc. |

Frequently Asked Questions

The Millimeter Wave Technology Market is expected to grow at a CAGR of 28.20% from 2026 to 2035.

The Millimeter Wave Technology Market was valued at USD 5.24 Billion in 2025.

Rapid global 5G deployment, increasing adoption of automotive radar sensors for vehicle safety, growing demand for fixed wireless access broadband solutions, and rising defense investments in advanced radar and communication systems are driving the Millimeter Wave Technology Market.

The E-Band segment dominated the Millimeter Wave Technology Market with approximately 61.2% share in 2025 through its widespread adoption in point-to-point 5G backhaul infrastructure, while the V-Band segment is the fastest growing.

North America dominated the Millimeter Wave Technology Market in 2024 with 40.1% of global market share.

Get in Touch