Mobile Communication Antenna Market Size Analysis:

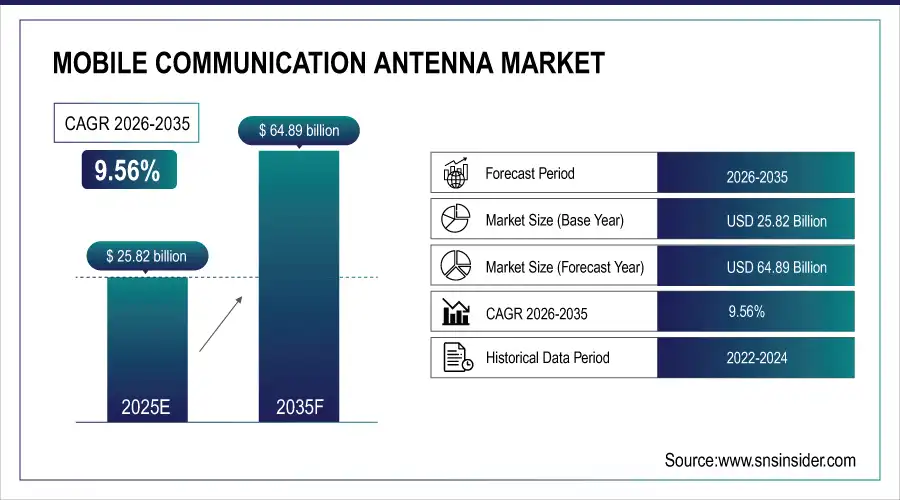

The Mobile Communication Antenna Market was valued at USD 25.82 billion in 2025E and is expected to reach USD 64.89 billion by 2035, growing at a CAGR of 9.56% from 2026-2035.

The global market is segmented by type, application, material, type and end-user, and region. Some of the very important factors propelling the growth of the market are rise in demand for intelligent communication, regional wireless network expansion and elevated adoption of smart devices globally. It also discusses leading operators, latest market developments and future growth opportunities, providing deep insights about the changing landscape of communication antenna value chain.

For instance, over 12,000 new patents related to communication antennas were filed globally between 2022 and 2024.

Mobile Communication Antenna Market Size and Forecast

-

Market Size in 2025: USD 25.82 Billion

-

Market Size by 2035: USD 64.89 Billion

-

CAGR: 9.56% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Mobile Communication Antenna Market - Request Free Sample Report

Mobile Communication Antenna Market Trends

-

Rising demand for high-speed mobile connectivity and expanding smartphone usage is driving the mobile communication antenna market.

-

Growing deployment of 4G and 5G networks is boosting demand for advanced, high-performance antenna solutions.

-

Expansion of IoT devices, connected vehicles, and smart infrastructure is fueling antenna adoption.

-

Increasing focus on compact, lightweight, and multi-band antennas is shaping design and deployment trends.

-

Advancements in MIMO, beamforming, and small-cell technologies are enhancing network capacity and coverage.

-

Rising investments by telecom operators in network densification are supporting market growth.

-

Collaborations between antenna manufacturers, telecom equipment vendors, and network operators are accelerating innovation and global rollout.

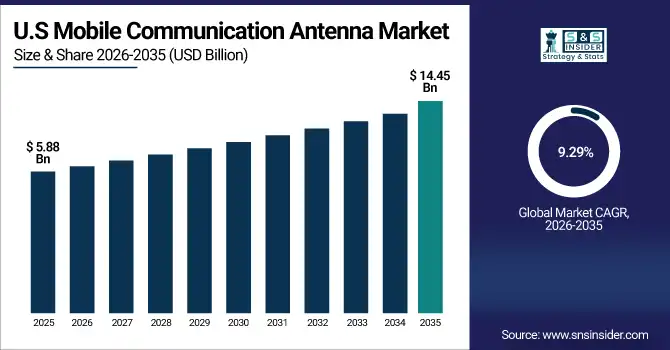

The U.S. Mobile Communication Antenna Market was valued at USD 5.88 billion in 2025 and is expected to reach USD 14.45 billion by 2035, growing at a CAGR of 9.29% from 2026-2035.

The U.S. Market is driven by rapid adoption of 5G technology and growing investments for telecommunication infrastructure. The growing demand for high-speed internet connectivity, development of smart city projects, along with substantial government support for advanced communication systems, also plays a major role in the growth of the market. The a forementioned factors together augment the deployment of advanced antenna solutions in various industries, thereby fostering Mobile Communication Antenna Market growth in U.S.

For instance, 5G antenna deployments reduced network latency by up to 30% in major metropolitan areas.

Mobile Communication Antenna Market Growth Drivers:

-

Increasing Adoption of 5G and Wireless Technologies Boosts Market Growth

Increasing deployment of 5G networks and demand for high-speed wireless communication is primarily driving the market. Advance antenna installation due to higher need to connect it well in urban as well as rural areas. Increase in IoT For example, the ever-growing amount of IoT devices, growth of mobile broadband, and smart infrastructure necessitates robust antenna systems capable of sustaining higher data rates and lower latency. The telecom operators and enterprises are extensively deploying antennas as a result of this adoption, resulting in global market growth.

For instance, over 70% of urban and 40% of rural areas worldwide have upgraded antenna infrastructure for better connectivity.

Mobile Communication Antenna Market Restraints:

-

Stringent Regulatory Norms and Spectrum Allocation Issues Hamper Expansion

Market growth is restrained due to regulatory challenges such as spectrum licensing and compliance with electromagnetic radiation standards. Long authorisation procedures and the differing regulations by region present challenges for manufacturers and service providers. Such constraints hampers product launches and infrastructure upgrades, hindering overall market development. In the urban landscapes, aesthetic and safety concerns also tighten reins on the communication antenna networks by way of restricting antenna placements.

Mobile Communication Antenna Market Opportunities:

-

Expansion of Satellite and Space Communication Networks Creates New Avenues

Growing demand for specialized antennas that can handle high-frequency and long-distance communication is supported by increasing investments in satellite communication and the space exploration industry. Which is why we are seeing more satellite constellations launched by governments and private enterprises for broadband, navigation and defense applications. Such an expansion opens up markets for high-end antenna technologies which can be tailored for space and unlocks a whole new realm of research and development as well as new entrants within the communication antenna space.

For instance, average lifespan of communication satellites has increased by 20% due to advancements in antenna technology.

Mobile Communication Antenna Market Challenges:

-

Supply Chain Disruptions Affecting Raw Material Availability and Production

Availability of essential raw materials, including dedicated metals and composites used in antenna fabrication, is affected by global supply chain problems. The production schedule gets disrupted due to price changes in goods or parts delays, impacting supply in the market and delivery times. Further, these disruptions also make meeting the rising demand in a time-bound manner impossible, which leads to loss of revenue and stalling of market expansion, especially in regions where companies import essential components for manufacturing.

Mobile Communication Antenna Market Segmentation Analysis:

By Type

In 2025, the wireless antenna segment, with a revenue share of nearly 26.50% held the largest Mobile Communication Antenna Market share. The ubiquity of wireless antennas for mobile communications, broadband networks, and IoT devices gives this dominance clout. These mesh networks are the preferred technology for global wireless infrastructure expansion due to their plug-and-play nature, scalability, and cost-effectiveness.

The array antenna segment is anticipated to achieve highest CAGR of nearly 10.74% during the forecast period during 2026 to 2035. The increasing integration of beamforming technology in 5G networks and radar systems, which require accurate signal directionality as well as higher performance, is expected to drive rapid growth for these applications.

By Application

The Wi-Fi Systems segment accounted for a leading revenue share of around 24.6% in the Mobile Communication Antenna Market during 2025. As Wi-Fi connects nearly every home, office and public place, and proliferation of various smart devices to use, this segment is leading the market revenue.

The Connected Vehicles segment is predicted to rapidly expand at a highest CAGR of 11.32% during 2026 to 2035. This rapid growth is driven by increasing investments in autonomous vehicles, vehicle-to-everything (V2X) communication technologies, and rising demand for safer and connected transportation solutions. A major player in antenna solutions for connected vehicle applications, Aptiv.

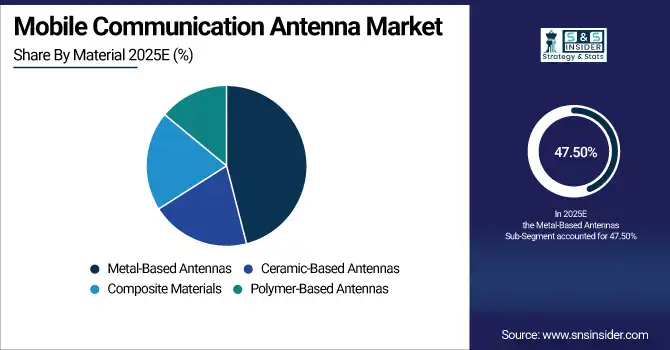

By Material

Metal Based Antennas segment held the largest revenue share of approximately 47.50% in 2025 and is expected to dominate the Mobile Communication Antenna Market. Given the unrivaled electrical conductivity and inexpensive nature of metals such as copper and aluminum, antennas based on metal tend to be used in most communication systems due to their long service life.

The Composite Materials segment is anticipated to register the highest CAGR of around 10.32% over the forecasted years 2026 to 2035. The need for lightweight, corrosion-resistant antennas, particularly in aerospace & defense and in sophisticated communication applications with durable but flexible materials is fueling this. Laird Connectivity, a leading provider of composite material antenna technologies.

By End-User

The Mobile Communication Antenna Market generated the highest revenue of around 28.40% in 2025, which is attributed to the growth of the consumer electronics segment (aviation, automotive, industrial, and home electronics) in the Mobile Communication Antenna Market. A booming adoption of smartphones, tablets and wearables with integrated antennas, and constant innovation and refresh cycles in consumer electronics, is driving growth.

The Aerospace & Defense segment is anticipated to have the fastest CAGR growth of approximately 10.87% during the forecast period from 2026 to 2035. Recent years have witnessed significant growth in this segment due to various factors such as rising defense budgets, communication infrastructure modernization, and increasing aerospace activities, thereby requiring batter and reliable antenna solutions.

Mobile Communication Antenna Market Regional Analysis:

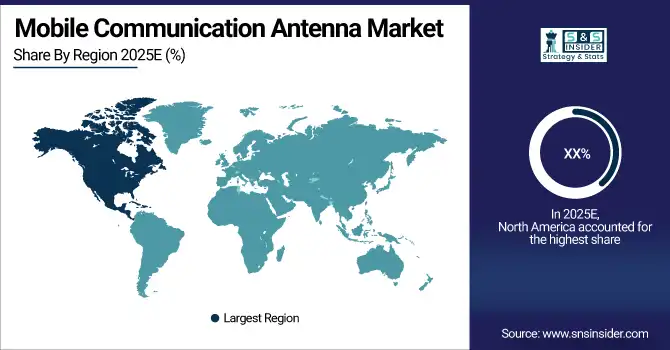

North America Mobile Communication Antenna Market Insights

The North America Mobile Communication Antenna Market is driven by growing demand for high speed connectivity, strong joint telecom infrastructure investments and rapid adoption of 5G technology. Technological developments along with government initiatives to promote smart city and IoT develops are aiding the growth in the region. The presence of major players and the increasing innovation of startups allow North America to be one of the key contributors to the Mobile Communication Antenna Market growth globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

-

The U.S. dominates North America due to its early 5G rollout, robust telecom infrastructure, significant R&D investments, and strong government support for advanced communication technologies, driving widespread adoption of innovative antenna solutions across various industries.

Asia Pacific Mobile Communication Antenna Market Insights

Asia Pacific held the largest revenue share of over 32.80% and is likely to register the fastest CAGR of nearly 10.27% from 2026-2035, owing to rapid urbanization, infrastructural development, and growing adoption of wireless technologies, particularly in China, India, and Japan. There are also major contributions from government initiatives and growing telecom investments.

-

China leads Asia Pacific because of massive telecom infrastructure expansion, government-backed 5G deployment, high smartphone penetration, and large-scale smart city projects, which collectively fuel strong demand for communication antennas and related technologies across the region.

Europe Mobile Communication Antenna Market Insights

The Europe Mobile Communication Antenna Market is expanding steadily, supported by increasing 5G network deployments and investments in smart infrastructure. Growing demand for reliable wireless connectivity in automotive, industrial automation, and public safety sectors drives market growth. Stringent regulations on quality and safety standards push innovation, while key players focus on developing advanced antenna technologies to cater to evolving communication needs across European countries.

-

Germany dominates the Europe Mobile Communication Antenna Market due to its advanced telecom infrastructure, early 5G adoption, strong industrial sector, and significant investments in smart city and IoT projects, driving high demand for innovative communication antenna solutions across the country.

Middle East & Africa and Latin America Mobile Communication Antenna Market Insights

The Middle East & Africa and Latin America Mobile Communication Antenna Market is experiencing steady growth due to increasing mobile subscriptions, network expansions, and 4G/5G deployment. Rising demand for reliable connectivity, government initiatives for digital infrastructure, and adoption of advanced antenna technologies are driving market expansion. Urbanization and growing IoT applications further boost regional opportunities, enhancing network performance and coverage.

Mobile Communication Antenna Market Competitive Landscape:

CommScope Holding Company, Inc.

CommScope is a global infrastructure solutions provider specializing in network connectivity for wireless, broadband, enterprise, and data center environments. The company has historically been a major supplier of mobile communication antennas, DAS, microwave backhaul antennas, and outdoor wireless infrastructure. CommScope focuses on enabling scalable, high-capacity mobile networks through advanced RF, antenna, and fiber solutions supporting 4G, 5G, and evolving wireless standards.

-

In 2025, CommScope completed the divestiture of its Outdoor Wireless Networks and DAS businesses to Amphenol, reshaping ownership of mobile antenna infrastructure assets.

-

In 2024, CommScope introduced a new dual-band 6/11 GHz ValuLine HX microwave backhaul antenna to support higher capacity and future-ready mobile networks.

Ericsson

Ericsson is a leading global provider of telecommunications equipment, software, and services, with a strong focus on mobile network infrastructure. Its portfolio includes radio systems, antennas, core networks, and mission-critical communication solutions. Ericsson plays a key role in advancing 5G and critical communications through high-performance antenna technologies designed for coverage optimization, spectrum efficiency, and resilient connectivity in public safety and enterprise network environments.

-

In 2025, Ericsson launched next-generation Antenna 1005 and 1006, designed for mission-critical mobile networks, enhancing coverage, resilience, and spectrum support for public safety.

Amphenol Corporation

Amphenol Corporation is a global manufacturer of interconnect systems, antennas, and sensor solutions serving communications, industrial, automotive, aerospace, and defense markets. The company has a strong antenna portfolio supporting cellular, broadband, and RF applications. Through strategic acquisitions, Amphenol continues to expand its mobile communication antenna and network infrastructure capabilities, strengthening its position across wireless access, DAS, and related RF technologies.

-

In 2024, Amphenol announced its agreement to acquire CommScope’s mobile networks businesses, including antenna and DAS solutions, expanding its wireless infrastructure portfolio.

Nokia Corporation

Nokia is a global telecommunications technology leader providing network infrastructure, software, and services for mobile, fixed, and cloud networks. The company develops advanced antenna solutions for 5G radio access, fixed wireless access, and integrated passive-active antenna systems. Nokia’s antenna innovations focus on improving coverage, capacity, and deployment efficiency, supporting operators in expanding broadband access and enhancing next-generation mobile network performance.

-

In 2024, Nokia expanded its 5G FWA portfolio with high-gain antenna-equipped devices to extend coverage and improve broadband delivery.

-

In 2023, Nokia deployed Interleaved Passive Active Antennas across Oceania, supporting large-scale 5G expansion and improved spectrum utilization.

Key Players

Some of the Mobile Communication Antenna Market Companies

-

CommScope Holding Company, Inc.

-

Amphenol Corporation

-

Rohde & Schwarz GmbH & Co KG

-

HUBER+SUHNER AG

-

Laird Connectivity

-

TE Connectivity Ltd.

-

Huawei Technologies Co., Ltd.

-

Ericsson

-

Nokia Corporation

-

Qualcomm Incorporated

-

ZTE Corporation

-

Motorola Solutions, Inc.

-

MTI Wireless Edge Ltd.

-

Airgain, Inc.

-

Southwest Antennas

-

Radiall SA

-

PCTEL, Inc.

-

Antcom Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.82 Billion |

| Market Size by 2035 | USD 64.89 Billion |

| CAGR | CAGR of 9.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Wireless antenna, Aperture antenna, Reflector antenna, Microstrip antenna, Array antenna and Lens antenna) • By Application (Wi-Fi Systems, RADAR Systems, Connected Vehicles, Satellite Tracking, Radio Astronomy and Others) • By Material (Metal-Based Antennas, Ceramic-Based Antennas, Polymer-Based Antennas and Composite Materials) • By End-User (Industrial, Healthcare, Consumer Electronics, Aerospace & Defense and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia,Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | CommScope Holding Company, Inc., Amphenol Corporation, Cobham Limited, Rohde & Schwarz GmbH & Co KG, HUBER+SUHNER AG, Laird Connectivity, TE Connectivity Ltd., Kathrein SE, Huawei Technologies Co., Ltd., Ericsson, Nokia Corporation, Qualcomm Incorporated, ZTE Corporation, Motorola Solutions, Inc., MTI Wireless Edge Ltd., Airgain, Inc., Southwest Antennas, Radiall SA, PCTEL, Inc. and Antcom Corporation. |

Get in Touch