Robotic Warfare Market Report Scope & Overview:

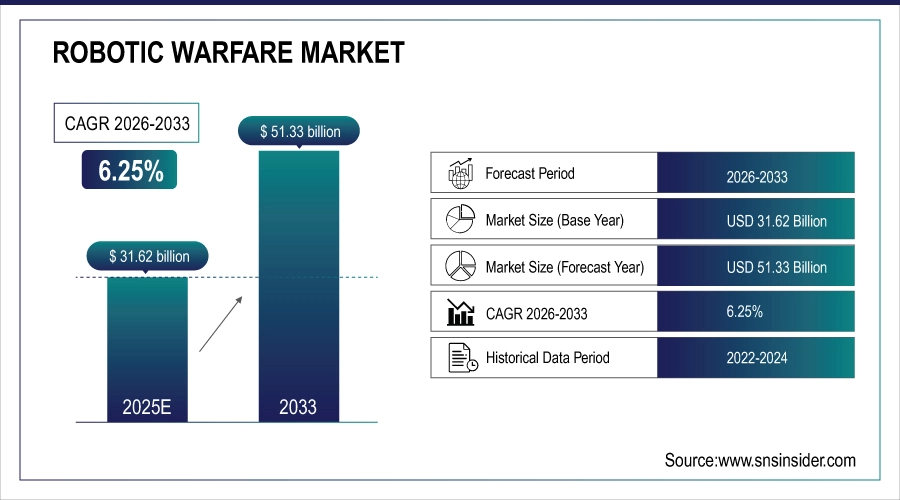

The Robotic Warfare Market size was valued at USD 31.62 Billion in 2025E and is projected to reach USD 51.33 Billion by 2033, growing at a CAGR of 6.25% during 2026-2033.

The robotic warfare market is experiencing robust growth driven by increasing demand for autonomous combat systems, electronic warfare capabilities, and enhanced battlefield efficiency. Including advanced sensors, AI-enabled decision-making and multi-domain operability these platforms are able to execute vital missions such as reconnaissance, targeting, logistics support, and electronic signal disruption. Higher defense budgets and armed aggression in some countries, coupled with the trend for minimal human intervention from a safety viewpoint (force protection), are propelling adoption within land, air and maritime sectors.

Robotic Warfare Market Size and Forecast:

-

Market Size in 2025E: USD 31.62 Billion

-

Market Size by 2033: USD 51.33 Billion

-

CAGR: 6.25% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Robotic Warfare Market - Request Free Sample Report

Key Trends in the Robotic Warfare Market:

-

Rising adoption of autonomous and semi-autonomous robotic systems for military and defense operations.

-

Increasing integration of AI, machine learning, and advanced sensor technologies in combat robots and unmanned vehicles.

-

Growing demand for power-efficient, lightweight, and durable robotic platforms suitable for harsh battlefield environments.

-

Rapid deployment of unmanned aerial vehicles (UAVs), unmanned ground vehicles (UGVs), and maritime robots for surveillance, reconnaissance, and combat missions.

-

Expansion of swarm robotics and networked robotic warfare systems to enhance coordinated operations and tactical efficiency.

-

Higher investment in research and development of advanced military robotics by governments and defense contractors.

-

Strategic collaborations and partnerships between defense technology firms and military organizations to accelerate innovation and deployment of robotic warfare solutions.

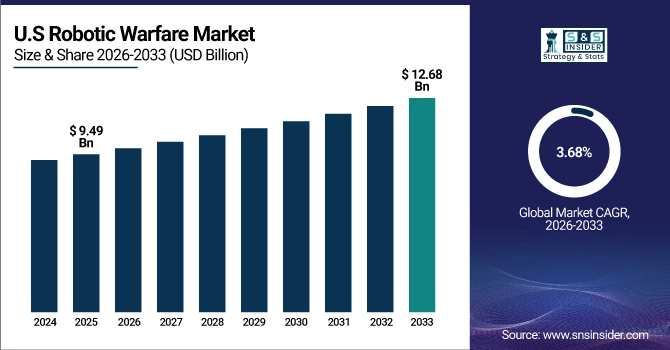

The U.S Robotic Warfare Market size was valued at USD 9.49 Billion in 2025E and is projected to reach USD 12.68 Billion by 2033, growing at a CAGR of 3.68% during 2026-2033. This Robotic Warfare Market growth is driven by rising investments in autonomous military systems, the need for advanced electronic warfare solutions and strategic push to reduce human intervention in war zones. These ongoing developments combined with novel AI process capabilities, real-time data turnaround and multi-domain intelligence interchange could potentially slosh even more robots into service as burgeoning robotic ecosystems become key elements in new warfare modernization policy initiatives.

The Robotic Warfare Market trends is driven by rapid advancements in AI, autonomous navigation, and electronic warfare integration. The trend towards a more multi-mission robotic system that takes care of everything from reconnaissance and close combat support to logistics and EW tasks with just enough human oversight has already started. Defence forces are progressively aiming at the modular, upgradable systems with open architecture that can adapt to ever-evolving threats posed by CBRN incident. Enhanced operational efficiency by leveraging lightweight, long-life battery and SWaP optimization Real time data fusion and increased interoperability with command networks are also emerging as critical capabilities defining the future of battlefield robotics.

Robotic Warfare Market Drivers:

-

Rising Adoption of Modular Unmanned Combat Systems in Naval Warfare

The growing emphasis on modular, missile-equipped unmanned systems is significantly driving the robotic warfare market. Types of defense forces are also going for wily operational systems which include multi-mission roles like surveillance, strike, electronic warfare and logistics support. Across the board, this move is driven by the need for increased force multipliers and minimization of human risks in more dangerous regions, to operate at a heightened level with maximal efficiency across contested spaces. A modular architecture provides fast payload integration and quick mission reconfigurations, which is combined with off-the-shelf commercial components that ensures quicker deployment to field and cost-effective manner. As navies and military worldwide update their fleets with autonomous systems, a growing need for AI-powered robotic warfare solutions will change the way combat is conducted.

The U.S. The MASC program was created by the Navy to field missile-armed unmanned warships that can carry out modular, multi-mission roles. For the U.S. Navy, this signals a significant move down the path to autonomous naval warfare strengthening fleet resilience and distributed lethality.

Robotic Warfare Market Restraints:

-

Operational Complexity and Cybersecurity Risks Limiting Deployment

The adoption of robotic warfare systems faces key restraints due to substantial operational complexity and a rise in cybersecurity concerns. Implementing AI-based autonomy, real-time processing of data and multi-platform coordination require a lot of backend infrastructure and trained personnel that many defense agencies do not have. These systems also suffer from a glut of networking, communications and software-derived functions -- those in turn can be hacked, jammed or electronically interfered with. Thus, it leads to potential mission failures and data breaches in high-risk environments. It further slows widespread adoption by adding the costs of secure system development, testing, and maintenance. Thus, while technologically capable, many countries do feel inhibited to utilize the full extent of their robo-warfare platforms in key military operations.

Robotic Warfare Market Opportunities:

-

Modular and Cost-Effective UGVs Enabling Scalable Battlefield Integration

The growing demand for affordable, modular, and AI-enabled unmanned ground vehicles (UGVs) presents a significant opportunity in the robotic warfare market. Modular UGVs provide unmatched operational flexibility to militaries that require rapidly deployable solutions for a range of combat scenarios from payload transport to mine detection and casualty evacuation. Hence, the personnel could be rapidly built on field with off-the-shelf components without logistic overheads and increasing mission readiness as well. This change represents a broader move to low-cost robotics systems, which will ultimately allow startups and defense innovators to modernize ground warfare in response to the emerging threat landscape.

NATO has invested €9 million in ARX Robotics to develop modular, AI-driven unmanned ground systems for modern combat. These autonomous robots support missions like payload transport, mine-sweeping, and casualty evacuation with rapid battlefield adaptability.

Robotic Warfare Market Challenges:

-

Regulatory, Ethical, and Tactical Barriers Hindering Full-Scale Robotic Warfare Adoption

The robotic warfare market faces critical challenges stemming from regulatory uncertainty, ethical concerns, and tactical limitations. The use of autonomous systems quickly cascades into difficult legal and ethical questions about responsibility, levels-of-autonomy, rules of engagement, compliance with international humanitarian laws etc. Also, standardizing a protocol for interoperability among allied forces is absent which makes the integration real-time communication in joint operations difficult. Operational reliability, which in this case is also limited since tactical constraints are involved such as vulnerability to electronic warfare, terrain adaptability and real-time decision making under combat pressure. Those factors give defense agencies pause, delaying procurement cycles and the large-scale deployment of weapon systems. Thus, in practice, the governance aspect of these systems keep holding back the full impact of robotic warfare capability even if it is otherwise technologically possible.

Robotic Warfare Market Segmentation Analysis:

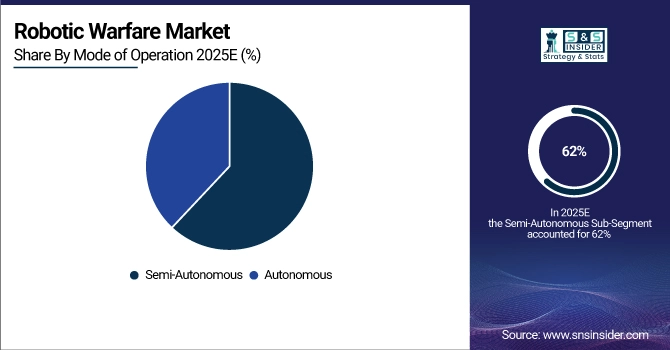

By Mode of Operation, Semi-Autonomous Segment Dominates Robotic Warfare Market with 62% Share in 2025, Autonomous Segment to Record Fastest Growth with 6.76% CAGR

The Semi-Autonomous segment held a dominant share of approximately 62% in 2025. This segment’s leadership is driven by the balance it offers between human control and machine efficiency, allowing remote operation with advanced decision-support systems. Semi-autonomous platforms are widely adopted due to their reliability, lower regulatory barriers compared to fully autonomous systems, and proven performance in reconnaissance, targeting, and logistics operations. As trust in autonomy grows gradually, semi-autonomous systems are expected to remain a preferred choice for militaries transitioning toward fully autonomous capabilities.

The Autonomous segment is expected to experience the fastest growth in the Robotic Warfare market over 2026–2033, with a CAGR of 6.76%. This growth is fueled by advancements in AI, sensor fusion, and machine learning, enabling robotic systems to operate independently in dynamic and hostile environments. Increasing defense investments in surveillance, targeting, logistics, and combat applications are accelerating adoption, as autonomous systems enhance operational efficiency and safety in high-risk missions.

By Capability, Unmanned Platforms & Systems Segment Dominates with 36% Share in 2025, Target Acquisition Systems to Record Fastest Growth with 13.37% CAGR

The Unmanned Platforms & Systems segment accounted for approximately 36% of the market in 2025. Its dominance is due to the ability of drones and unmanned vehicles to execute high-risk reconnaissance, logistics, and electronic warfare missions without endangering human personnel. Investments in AI, sensor integration, and modular payload systems are driving adoption, and the segment is expected to maintain a large market share due to adaptability, cost-effectiveness, and mission versatility.

The Target Acquisition Systems segment is projected to grow at the fastest CAGR of 13.37% over 2026–2033. Increasing integration of AI-powered vision systems, real-time data processing, and advanced sensors enhances precision in identifying, tracking, and engaging targets. These systems are becoming critical across aerial, ground, and naval platforms as modern warfare emphasizes automation, speed, and accuracy.

By Application, Intelligence, Surveillance & Reconnaissance (ISR) Segment Dominates with 28% Share in 2025, Combat & Operations to Record Fastest Growth with 9.32% CAGR

The ISR segment held a dominant share of 28% in 2025, reflecting its crucial role in enhancing situational awareness and mission planning. Autonomous drones, ground robots, and sensor-fusion systems are widely deployed to collect real-time battlefield intelligence, supporting data-driven decision-making. The importance of ISR is expected to grow as militaries prioritize precision, stealth, and early threat detection in complex combat environments.

The Combat & Operations segment is expected to witness the fastest growth over 2026–2033, with a CAGR of 9.32%. This growth is driven by the deployment of autonomous systems in frontline combat, including engagement, fire support, and tactical maneuvers. AI, weapon integration, and real-time coordination improve operational effectiveness, reducing human exposure while maintaining combat superiority.

By Domain, Land Segment Dominates with 41% Share in 2025, Airborne Segment to Record Fastest Growth with 9.10% CAGR

The Land segment accounted for approximately 41% of the market in 2025, driven by the widespread use of unmanned ground vehicles (UGVs) for reconnaissance, logistics, combat assistance, and explosive ordnance disposal. Border security, counter-insurgency, and urban warfare operations are accelerating the deployment of ground-based robotic platforms. Their adaptability, mobility, and modularity make them vital across diverse military scenarios.

The Airborne segment is projected to grow at the fastest CAGR of 9.10% over 2026–2033. Rising demand for UAVs in ISR, precision strike, and electronic warfare missions, coupled with investments in drone swarming, AI flight autonomy, and beyond-visual-line-of-sight (BVLOS) operations, is driving rapid adoption globally.

Robotic Warfare Market Regional Insights:

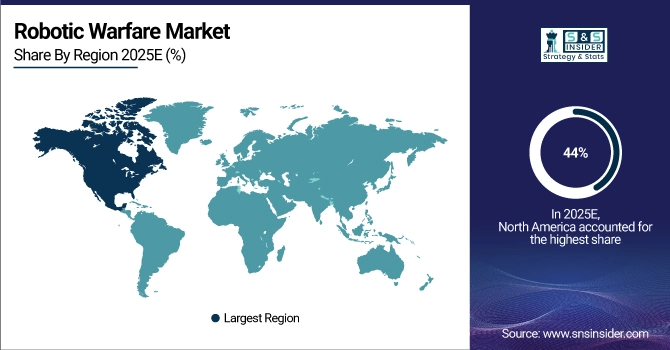

North America Dominates Robotic Warfare Market in 2025

In 2025, North America accounted for approximately 44% of the global Robotic Warfare market revenue, driven by high defense spending, rapid adoption of autonomous technologies, and the strong presence of leading defense contractors. The region’s focus on modernizing military infrastructure, expanding unmanned combat capabilities, and integrating AI across land, air, and naval platforms continues to fuel sustained market growth and innovation.

The United States dominates North America’s market due to its extensive defense budget, advanced research in autonomous systems, and robust defense contractor ecosystem. U.S. companies are actively developing next-generation unmanned platforms for surveillance, combat support, and logistics, reinforcing regional leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific to Witness Fastest Growth in Robotic Warfare Market over 2026–2033

Asia-Pacific is projected to grow at the fastest CAGR of 7.91% during 2026–2033. This growth is driven by increasing defense budgets, rising geopolitical tensions, and rapid advancements in indigenous unmanned technologies. Countries such as China, India, South Korea, and Japan are investing heavily in autonomous systems for surveillance, border security, and combat readiness, driving regional demand for robotic warfare solutions.

China and India are the key countries in Asia-Pacific, focusing on developing and deploying UAVs, UGVs, and autonomous naval systems. Japan and South Korea are also strengthening defense capabilities through advanced sensor integration and AI-enabled robotic platforms, collectively accelerating market expansion in the region.

Europe Robotic Warfare Market Insights, 2025

Europe held a significant portion of the Robotic Warfare market in 2025, supported by defense modernization programs and increasing investment in unmanned systems. The region is focusing on AI-driven autonomous platforms for surveillance, combat support, and logistics operations amid growing security concerns. Collaborative defense initiatives, funding from organizations such as NATO, and the presence of innovative defense tech startups are further accelerating adoption.

Germany, France, and the UK are the leading countries in Europe, leveraging strong defense research infrastructure and manufacturing capabilities to advance robotic warfare technologies. These nations are developing systems across land, air, and naval domains, reinforcing Europe’s position in the global market.

Middle East & Africa and Latin America Robotic Warfare Market Insights, 2025

Middle East & Africa (MEA) and Latin America (LATAM) are emerging markets for robotic warfare, experiencing steady growth driven by rising security concerns, border surveillance needs, and modernization of military forces. Adoption of unmanned systems for reconnaissance, counterterrorism, and urban combat operations is increasing, supported by government initiatives, rising defense budgets, and partnerships with international defense technology providers.

In LATAM, Brazil and Mexico are leading adoption of cost-effective, semi-autonomous, and modular robotic platforms to enhance tactical capabilities. In MEA, countries such as UAE, Saudi Arabia, and South Africa are investing in advanced unmanned systems to strengthen national security and defense readiness.

Key Players in the Robotic Warfare Market:

-

Elbit Systems Ltd.

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Rheinmetall AG

-

QinetiQ Group plc

-

BAE Systems plc

-

Raytheon Technologies Corporation

-

General Dynamics Corporation

-

Thales Group

-

Israel Aerospace Industries (IAI)

-

Kongsberg Gruppen ASA

-

Leonardo S.p.A.

-

Textron Inc.

-

L3Harris Technologies, Inc.

-

SAAB AB

-

Hanwha Aerospace Co., Ltd.

-

Turkish Aerospace Industries (TAI)

-

Milrem Robotics

-

EDGE Group

-

Boston Dynamics

Competitive Landscape for the Robotic Warfare Market:

Elbit Systems Ltd.

Elbit Systems Ltd. is an Israel-based leader in defense electronics and robotic warfare solutions, specializing in unmanned aerial, ground, and naval systems. With decades of experience, the company designs, engineers, and manufactures advanced autonomous and semi-autonomous platforms, including surveillance drones, combat UGVs, and remote weapon stations. Elbit Systems operates globally through direct contracts with defense agencies and international partners. Its role in the robotic warfare market is vital, providing innovative, reliable, and adaptable solutions that enhance operational efficiency, situational awareness, and mission success.

-

In 2025, Elbit Systems expanded its unmanned ground vehicle lineup, introducing enhanced AI-driven reconnaissance systems capable of operating in complex and hostile environments.

Lockheed Martin Corporation

Lockheed Martin Corporation is a U.S.-based global leader in aerospace, defense, and robotic warfare technologies, specializing in UAVs, autonomous systems, and integrated battlefield solutions. The company develops and deploys advanced robotic platforms with AI-enabled target acquisition, precision strike capabilities, and sensor integration. Lockheed Martin operates through direct government contracts and international collaborations, supporting both military and strategic operations worldwide. Its role in the robotic warfare market is central, delivering cutting-edge technology that enhances combat readiness and operational superiority.

-

In 2025, Lockheed Martin launched a new autonomous drone system designed for ISR (Intelligence, Surveillance, and Reconnaissance) and precision tactical missions, offering extended flight endurance and advanced sensor payloads.

Northrop Grumman Corporation

Northrop Grumman Corporation is a U.S.-based leader in defense and robotic warfare solutions, focusing on unmanned aerial vehicles, autonomous naval systems, and robotic platforms for combat and surveillance. The company integrates advanced AI, machine learning, and sensor fusion into its products to enhance autonomous decision-making and operational efficiency. Northrop Grumman serves defense agencies globally through direct contracts and collaborative projects. Its role in the robotic warfare market is significant, providing versatile, high-performance systems that support both offensive and defensive operations.

-

In 2025, Northrop Grumman introduced next-generation UAVs with enhanced autonomy and payload flexibility for ISR and combat applications, improving battlefield situational awareness and mission success.

Rheinmetall AG

Rheinmetall AG is a Germany-based leader in defense and security technologies, specializing in autonomous and semi-autonomous land systems, robotic combat vehicles, and unmanned support platforms. The company designs and manufactures robust, modular systems capable of operating in challenging combat environments. Rheinmetall AG operates through direct government contracts, joint ventures, and international partnerships. Its role in the robotic warfare market is crucial, offering scalable, reliable, and technologically advanced robotic solutions for modern defense forces.

-

In 2025, Rheinmetall AG expanded its robotic ground vehicle portfolio with AI-assisted autonomous systems for reconnaissance, combat support, and logistics operations.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 31.62 Billion |

| Market Size by 2033 | USD 51.33 Billion |

| CAGR | CAGR of 6.25% From 2026 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Capability(Unmanned platforms & systems, Exoskeleton & wearables, Target acquisition systems and Turret and weapon systems) • By Application(Intelligence, Surveillance & Reconnaissance (ISR), Logistics & Support, Search & Rescue, Tracking & Targeting, Combat & Operations and Others) • By Mode of Operation(Autonomous and Semi-Autonomous) • By Domain(Land, Marine and Airborne) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | The Robotic Warfare Market Companies are Elbit Systems, Lockheed Martin, Northrop Grumman, Rheinmetall, QinetiQ, BAE Systems, Raytheon Technologies, General Dynamics, Thales, Israel Aerospace Industries, Kongsberg Gruppen, Leonardo, Textron, L3Harris Technologies, SAAB, Hanwha Aerospace, Turkish Aerospace Industries, Milrem Robotics, EDGE Group, Boston Dynamics. and Others. |

Frequently Asked Questions

North America dominated the Robotic Warfare Market in 2025.

The “Unmanned platforms & systems” segment dominated the Robotic Warfare Market

Rising geopolitical tensions, increasing defense budgets, and growing demand for advanced surveillance, communication, and electronic warfare systems are key drivers of the Robotic Warfare Market.

The Robotic Warfare Market size was valued at USD 31.62 Billion in 2025 and is projected to reach USD 51.33 Billion by 2033

The Robotic Warfare Market is expected to grow at a CAGR of 6.25% during 2026-2033.

Get in Touch