Mobile Phone Semiconductor Market Report Scope & Overview:

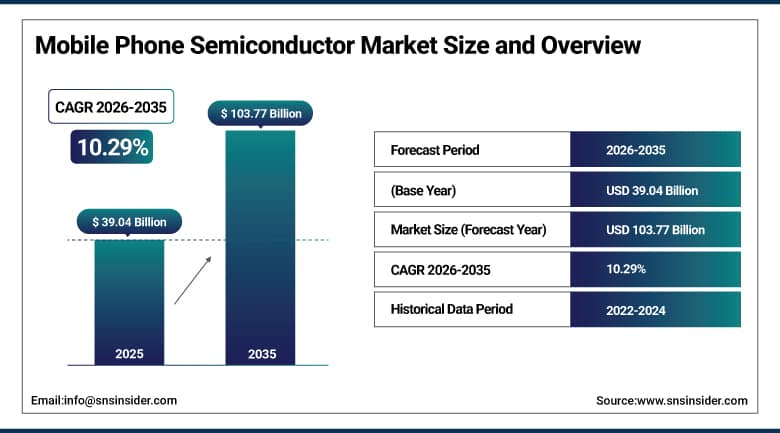

The Mobile Phone Semiconductor Market was valued at USD 39.04 billion in 2025 and is expected to reach USD 103.77 billion by 2035, growing at a CAGR of 10.29% from 2026–2035.

The mobile phone semiconductor market is witnessing strong growth in the global market owing to rising smartphone penetration and 5G expansion. Increasing demand for high-performance processors is driving strong chipset adoption across devices. Growing usage of AI-enabled mobile applications is improving semiconductor complexity and design innovation. Rising deployment of System on Chip solutions is supporting integration efficiency in smartphones. Increasing demand for power-efficient components is accelerating battery optimization technologies. Continuous advancements in mobile connectivity standards are further boosting market expansion.

According to the International Telecommunication Union World Mobile Statistics Report 2025, there were more than 8.6 billion mobile cellular subscriptions worldwide, and the percentage of smartphone adoption was more than 78% of the total number of mobile connections. According to the U.S. Semiconductor Industry Association 2025 Manufacturing Indicators, mobile and wireless applications contribute to more than 30% of the total semiconductor usage in terms of volume across the globe. According to the data on Digital Development provided by the World Bank, more than 95% of the world’s population has access to mobile broadband services.

Market Size and Forecast:

-

Market Size 2026E: USD 42.98 billion

-

Market Size 2035: USD 103.77 billion

-

CAGR (2026 - 2035): 10.29%

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Mobile Phone Semiconductor Market - Request Free Sample Report

Mobile Phone Semiconductor Market Trends:

-

The rapid proliferation of 5G infrastructure creates an increased demand for innovative semiconductors for mobile and radio frequency technologies.

-

Increased funding in telecom infrastructure modernization projects leads to faster deployment of next-gen chipsets with greater processing speed.

-

Increasing number of connected devices leads to the high demand for advanced semiconductor solutions for mobile and telecommunication systems.

-

The growing popularity of wearable devices leads to increased demand for low-power semiconductors worldwide.

-

The growth of IoT enabled ecosystems creates the increased demand for advanced connectivity semiconductors for smart home and health care applications.

-

The continuous development of wireless technologies drives innovations in semiconductors for energy efficiency, compact size, and fast connectivity solutions.

U.S. Mobile Phone Semiconductor Market Outlook:

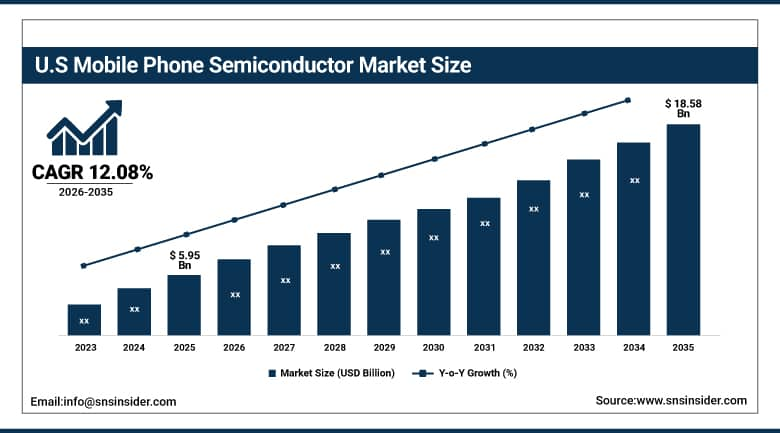

The U.S. Mobile Phone Semiconductor Market was valued at USD 5.95 billion in 2025 and is expected to reach around USD 18.58 billion by 2035, growing at a CAGR of 12.08% from 2026–2035.

The U.S. mobile phone semiconductor market is growing steadily owing to strong smartphone demand and 5G rollout. Increasing adoption of advanced processors is enhancing mobile computing performance across devices. Expansion of premium smartphone ecosystem is supporting high value semiconductor integration. Strong presence of leading chip designers is driving innovation in mobile architectures. Growing demand for AI enabled mobile applications is accelerating chipset complexity. Continuous technological advancements in wireless connectivity are further boosting market expansion.

According to U.S. Census Bureau Semiconductor and Other Electronic Component Manufacturing statistics and U.S. International Trade Commission 2025 Industry Profile statistics, semiconductors constitute over 25% of all electronic components shipped in the United States where integrated circuits are the main components used in mobile phones. According to the U.S. Department of Commerce CHIPS Program Office, over 80% of semiconductor fabrication capabilities have been developed in East Asia while the United States retains about 10% of the world’s fabrication capabilities, resulting in high import dependency of mobile phone chipsets. According to the Federal Communications Commission, over 97% of adults in the United States own a mobile phone.

Mobile Phone Semiconductor Market Segment Analysis:

-

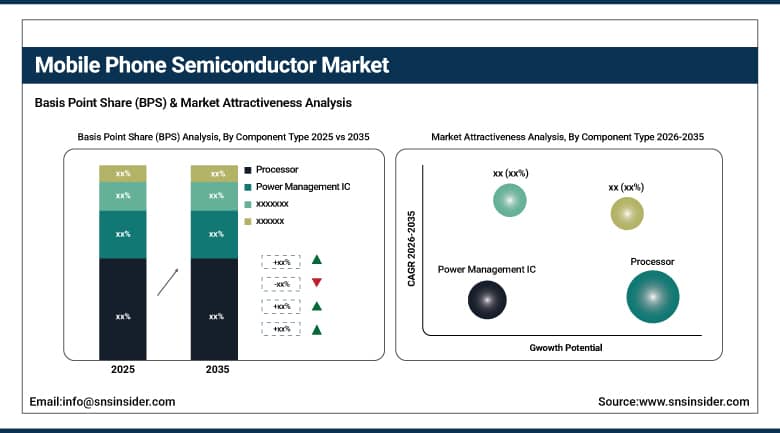

By Component Type, processor dominated the market with 38.50% share in 2025; while power management IC are the fastest growing segment with CAGR of 12.74% during 2026 to 2035.

-

By Application, smartphones dominated the market with 78.60% share in 2025; while wearable devices are the fastest growing segment with CAGR of 15.45% during 2026 to 2035.

-

By Technology, complementary metal-oxide-semiconductor dominated the market with 56.20% share in 2025; while system on chip is the fastest growing segment with CAGR of 12.72% during 2026 to 2035.

-

By Manufacturing Process, front-end dominated the market with 61.40% share in 2025; while back-end are the fastest growing segment with CAGR of 13.38% during 2026 to 2035.

By Component Type, processor dominated the mobile phone semiconductor market in 2025, while power management IC is the fastest growing segment.

Processor segment led the mobile phone semiconductor market by earning the highest share in terms of revenue in 2025, owing to growing need for high-performance computing in smartphone applications. Contemporary devices require sophisticated CPU and application processor to perform multitasking and AI applications. With increasing utilization of multi-core architecture and advanced fabrication technology, the popularity of this segment has risen immensely.

Power Management IC Segment is projected to register the fastest CAGR between 2026 and 2035, due to growing demand for energy-efficient smartphones and improved battery life. Growing use of 5G and AI applications has increased power consumption of smartphones. The role played by Power Management IC in optimizing energy distribution and improving battery performance has made it crucial in future mobile device development.

By Application, smartphones dominated the mobile phone semiconductor market in 2025, while wearable devices are the fastest growing segment.

The smartphone market segment is expected to lead in terms of revenue shares in the mobile phone’s semiconductor market in 2025 due to the large number of consumers worldwide and the advancement in technology of the same. Rising demand for efficient processors, memory chips and other components is driving the use of semiconductors. Increasing use of 5G smartphones and AI technology is driving the inclusion of semiconductors in these smartphones. High turnover rates and release of new premium smartphones is further driving the market.

The wearable devices market segment is anticipated to experience the fastest growth rate between 2026 and 2035 due to the growing demand for health and fitness tracking devices worldwide. The increasing demand for smart watches and wireless earbuds is driving the development of semiconductors. Increasing innovations in IoT technologies and sensors is further contributing to the advancement in the functioning of these devices.

By Technology, complementary metal-oxide-semiconductor dominated the mobile phone semiconductor market in 2025, while system on chip is the fastest growing segment.

The complementary metal oxide semiconductor segment accounted for the dominated revenue share in the global mobile phone semiconductor market in 2025 due to high efficiency, scalability, and cost-effectiveness for mass-scale manufacturing of mobile semiconductors. It finds wide application in processors, memory chips, and imaging chips of smartphones due to advanced fabrication process and continuous developments in technology, which provide high performance and energy-efficiency of the semiconductor. High integration in mass-scale mobile phones also contributes to the domination of the segment in the global market.

The system on chip segment is anticipated to register the fastest CAGR during 2026 to 2035 owing to growing demand for compact semiconductor chips. The SoC consists of several functions such as processing, graphics and connectivity, combined into a single chip. Increased demand for energy efficiency and high performance of semiconductors drives the growth of the SoC segment. The increase in 5G and AI-enabled smartphones boosts the use of SoCs in premium and mid-range smartphones.

By Manufacturing Process, front-end dominated the mobile phone semiconductor market in 2025, while back-end is the fastest growing segment.

The front end segment dominated the mobile phone semiconductor market in terms of revenue share in 2025 due to extensive wafer fabrication and high demands for chip design & integration. The use of high-performance processors and SoC is driving the significance of front end manufacturing. Complexity of mobile chips and lithography innovations are facilitating revenue leadership in the semiconductor manufacturing segments.

Back end segment is anticipated to witness fastest CAGR from 2026–2035. Growth in this segment is due to increasing demand for packaging, testing, and assembly in semiconductor manufacturing process. Use of 3D packaging and wafer level packaging is enhancing the efficiency of devices. Increasing demands for miniaturization and thermal management in smartphones is contributing to back end manufacturing adoption. The trend of semiconductor outsourcing is driving the growth of back end manufacturing.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

87.60% |

|

Europe |

Germany |

28.40% |

|

Asia Pacific |

China |

44.10% |

|

Middle East & Africa |

UAE |

17.60% |

|

Latin America |

Brazil |

46.80% |

Asia Pacific Mobile Phone Semiconductor Market Insights.

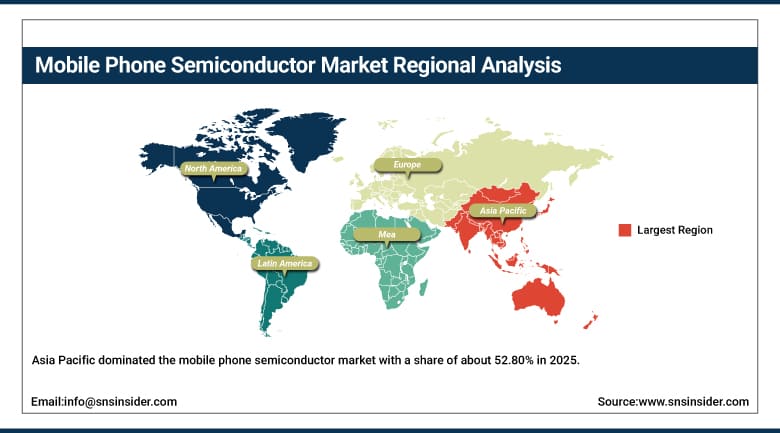

Asia Pacific dominated the mobile phone semiconductor market with a share of about 52.80% in 2025 owing to large scale smartphone manufacturing and consumption base. Increasing production of mobile devices in China, India, South Korea, and Japan is driving semiconductor demand. Strong presence of leading foundries and OSAT providers is supporting supply chain efficiency. Rising adoption of 5G and AI enabled smartphones is accelerating chipset innovation across the region.

As per the International Telecommunication Union and GSMA Mobile Economy 2025 indicators, the Asia Pacific region is home to more than 55% of the total number of mobile connections worldwide, where smartphones have penetrated over 75% in the region. As per the OECD analysis of semiconductor value chain assessment and the assessment of critical mineral elements by the United States Geological Survey, more than 70% of the capacity for the production of semiconductors, which allows the manufacture of mobile devices, is located in East Asia.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Mobile Phone Semiconductor Market Insights.

North America is expected to register the fastest CAGR of about 11.89% during 2026–2035 in the mobile phone semiconductor market owing to strong smartphone demand and advanced chip design capabilities. The region benefits from high adoption of premium smartphones and early integration of AI enabled processors. Presence of leading fabless semiconductor companies is supporting continuous innovation and design leadership. Rising deployment of 5G infrastructure is driving advanced chipset consumption across devices and applications.

According to the U.S. International Trade Commission and the Semiconductor Industry Association 2025 policy briefings, the United States accounts for approximately 10% of global semiconductor fabrication capacity while relying on imports for over 80% of advanced logic chips used in mobile devices. As per the U.S. Department of Commerce CHIPS Program Office updates, over 50% of new semiconductor manufacturing projects announced under federal incentives are focused on advanced-node fabrication relevant to mobile processors.

Europe Mobile Phone Semiconductor Market Insights.

Europe mobile phone semiconductor market is characterized by stable growth in 2025 owing to strong demand for mid-range and premium smartphones. Key countries include Germany, France, United Kingdom, and Italy. Increasing adoption of energy efficient mobile processors is supporting semiconductor demand. Rising focus on 5G network expansion is further boosting chipset integration. Expansion of automotive and consumer electronics ecosystem is indirectly supporting semiconductor consumption.

As per DESI 2025 of European Commission and ICT usage figures of Eurostat, smartphone adoption rate in European Union is more than 88% of population, whereas, mobile broadband subscriptions are in excess of 92 subscriptions per 100 people. According to European Semiconductor Strategy of EU Chips Act, Europe will raise its share in global semiconductor manufacturing capacity from current levels, which are in advanced packaging and automobile semiconductor products to 20 percent in year 2030. Eurostat data reveals that more than 70% of European Union families depend on mobile phones for internet connection.

Middle East & Africa and Latin America Mobile Phone Semiconductor Market Insights.

The Middle East & Africa along with Latin America regions are experiencing steady growth due to increasing smartphone penetration and expanding digital connectivity. Key contributing countries include Brazil, Mexico, UAE, Saudi Arabia, and South Africa. Rising adoption of affordable smartphones is driving demand for memory and power efficient chips. Expanding telecom infrastructure is supporting mobile device adoption across emerging economies. Increasing digital transformation initiatives are further boosting semiconductor usage.

As per the ICT indicators 2025 report from the International Telecommunication Union and the Mobile Economy report from GSMA, the penetration rate of smartphones in Latin America exceeds 78%, while that in the Middle East is above 72% and around 46% in Africa, which shows that there is a tremendous increase in the demand for mobile semiconductors.

Market Dynamics:

Growth Drivers: Expansion of 5G infrastructure and rapid adoption of next generation mobile communication technologies

The fast deployment of 5G networks in developed and developing countries has created a significant demand for mobile semiconductors. The need for high-speed data connectivity is creating an increased requirement for radio-frequency semiconductors and chips. There are significant investments being made by operators for upgrading their networks and expanding their spectra. This development has resulted in the increased use of new-generation chipsets that are more efficient and capable of processing. The growing number of connected devices has also played a key role in increasing the demand for semiconductors.

As per ITU and GSMA Mobile Economy 2025 statistics, the number of global 5G connections exceeded 2.0 billion, which is more than 25% of total mobile connections, with a significant growth rate in 2025 in Asia-Pacific and North America. In accordance with U.S. Federal Communications Commission broadband deployment statistics, the number of U.S. residents who have access to any one 5G network is more than 95%. The OECD report on digital infrastructure states that the growth rate of mobile data traffic has been over 30% per year in the recent past years.

Restraints: Supply chain disruptions and dependence on limited global semiconductor manufacturing hubs

The excessive dependence on some geographic locations for the manufacture of semiconductors results in risks for the global supply chain. Logistics problems, geopolitical risks, and export prohibitions can adversely influence the delivery time of the products. The lack of diversification of the capacities for manufacturing of advanced chips poses additional market risks. The shortage of semiconductors during the period of their high demand hampers the manufacture of smartphones. The excessive dependence on Asian foundries raises the risks of regional concentration.

Opportunities:Expansion of wearable devices and IoT enabled mobile ecosystems across global markets

The rise in the number of wearable devices, like smart watches and fitness bands, is opening up new semiconductor demand opportunities. The growing use of IoT-enabled mobile ecosystems is fueling the demand for low-power and highly efficient semiconductors. The increase in health monitoring applications is contributing to the rise in demand for sensors and connectivity semiconductors. The rise in smart homes and connected devices is further adding to integration needs. Semiconductor companies are investing in energy-efficient designs and miniaturization. Constant improvements in wireless connectivity standards are helping with ecosystem development.

As per the Indicators for ITU Measuring Digital Development 2025, mobile broadband penetration around the globe has reached more than 95 subscriptions per 100 people, with 80% of the world’s population being covered by 4G or above technology. According to GSMA Mobile Economy 2025, the number of unique mobile users worldwide is more than 5.6 billion, while Internet-of-Things connectivity numbers are above 18 billion devices.

Recent Developments:

-

2026: Apple expanded M-series chip architecture integration across iPad and Mac ecosystems, strengthening on-device AI processing and unified silicon strategy.

-

2025: MediaTek taped out next-generation flagship chip on TSMC advanced node to boost AI performance and smartphone efficiency.

-

2025: Qualcomm launched Snapdragon 8 Elite Gen 5 mobile platform, strengthening Samsung partnership and expanding AI-enabled flagship smartphone ecosystem globally.

-

2024: Samsung Electronics introduced Exynos 2400 processor featuring AMD RDNA3 graphics for improved AI and gaming performance.

Mobile Phone Semiconductor Market Key Players are:

-

Qualcomm

-

MediaTek

-

Apple

-

Samsung Electronics

-

Intel

-

Advanced Micro Devices

-

NVIDIA

-

Broadcom

-

Skyworks Solutions

-

Qorvo

-

Texas Instruments

-

NXP Semiconductors

-

STMicroelectronics

-

Infineon Technologies

-

Marvell Technology

-

Sony Semiconductor Solutions

-

Onsemi

-

Analog Devices

-

UNISOC

-

Renesas Electronics

Mobile Phone Semiconductor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 39.04 Billion |

| Market Size by 2035 | USD 103.77 Billion |

| CAGR | CAGR of 10.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type (Processor, Memory Chip, Power Management IC, Radio Frequency Component) • By Application (Smartphones, Feature Phones, Wearable Devices) • By Technology (Complementary Metal-Oxide-Semiconductor, Radio Frequency Integrated Circuit, System on Chip) • By Manufacturing Process (Front-End, Back-End, Packaging) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Qualcomm, MediaTek, Apple, Samsung Electronics, Intel, Advanced Micro Devices, NVIDIA, Broadcom, Skyworks Solutions, Qorvo, Texas Instruments, NXP Semiconductors, STMicroelectronics, Infineon Technologies, Marvell Technology, Sony Semiconductor Solutions, Onsemi, Analog Devices, UNISOC, Renesas Electronics |

Frequently Asked Questions

The mobile phone semiconductor market is expected to grow at a CAGR of 10.29% from 2026 to 2035.

The Smartphones segment dominated the market in 2025 due to high penetration, 5G adoption, advanced chips demand, and frequent upgrades.

Major growth factors include rising smartphone penetration, 5G expansion, demand for high performance processors, AI applications, SoC adoption, and need for power efficient semiconductor components across mobile devices globally.

The mobile phone semiconductor market was valued at USD 39.04 billion in 2025.

Asia Pacific dominated the mobile phone semiconductor market in 2025 due to large-scale manufacturing, strong supply chain, and high demand.

Get in Touch