Naphthalene Market Report Scope & Overview:

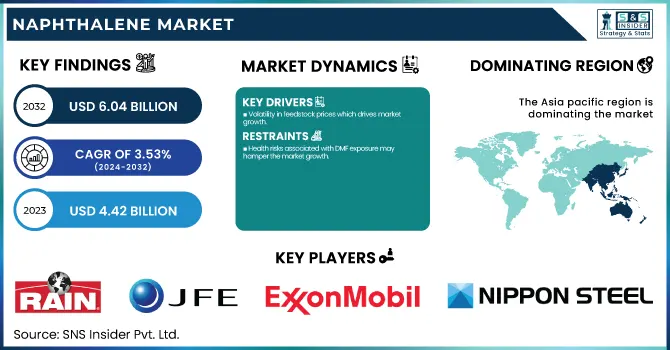

The Naphthalene Market size was USD 4.42 Billion in 2023 and is expected to reach USD 6.04 Billion by 2032 and grow at a CAGR of 3.53 % over the forecast period of 2024-2032. The report provides a comprehensive analysis of production capacity and utilization by country and type, highlighting key manufacturing hubs and efficiency levels. It examines feedstock price trends, regulatory impacts, and environmental metrics, including emissions data and sustainability initiatives. The report also explores innovation and R&D trends in naphthalene-based applications, such as superplasticizers and phthalic anhydride. Additionally, it covers market adoption across industries like construction, textiles, and agrochemicals, offering insights into emerging opportunities and challenges.

To Get more information on Naphthalene Market - Request Free Sample Report

Naphthalene Market Dynamics

Drivers

-

Volatility in feedstock prices which drives market growth.

It is extensively used in agrochemicals such as pesticides, insecticides, and fungicides supporting the naphthalene market growth. As the need for food production increases across the globe, farmers are now turning to agrochemicals to increase crop output and prevent them from contracting diseases and pests. Growing agricultural sectors in countries including India, China, and Brazil are seeing increased consumption of naphthalene-based agrochemicals, driven by state support for modern farming methods. Moreover, improvements in pesticide formulations, such as controlled-release and bio-based alternatives are also facilitating further uptake in agricultural applications for naphthalene derivatives.

Restraint

-

Health risks associated with DMF exposure may hamper the market growth.

One of the most prominent factors affecting the growth of the naphthalene market is the volatility of feedstock prices which have a significant effect on the production economics and market pricing, owing to the fact that coal tar and crude oil are the raw materials for the production of naphthalene. Because they are mostly obtained from coal tar or petroleum-based sources, the pricing of naphthalene lassos is highly volatile owing to supply chain interruptions, geopolitical tensions, and variations in crude oil prices. Rising feedstock costs present a challenge for manufacturers but also motivate innovations in production processes and research towards more cost-efficient refining technologies. Also, price fluctuations regularly result in changes in regional production and trade flows as companies look for a cheaper alternative or invest in higher-value naphthalene derivatives to keep profits intact.

Opportunity

-

Advancements in high-purity naphthalene for specialty chemicals create an opportunity in the market.

Advancements in high-purity naphthalene are creating significant opportunities in the specialty chemicals market, as industries increasingly require refined raw materials for high-performance applications. Phthalic anhydride, a key intermediate in the manufacture of plasticizers, resins, and dyes, needs high-purity naphthalene as a starting material. It is also critical for high-performance coatings, adhesives, and engineering polymers that need high quality and consistency. The continuous development of purification methods enables manufacturers to offer high-purity grades of naphthalene, which are more customized for use in pharmaceuticals, electronics, and fine chemicals. The increasing usage of high-performance materials in automotive, aerospace, and medical industries fuelling the demand for high-purity naphthalene is a wide lucrative segment of the market.

Challenges

-

Technological barriers in purification and refining may create a challenge for the market.

Technological barriers can be a major challenge to the naphthalene market especially in industries that require high-purity grades for application in pharmaceuticals, specialty chemicals, and high-performance polymers. Common purification techniques are distillation and crystallization; however, they tend to be ineffective at achieving the ultra-high purities required for higher-end applications. Impurities like sulfur compounds and other polycyclic aromatic hydrocarbons (PAHs) are present in the product, affecting product quality and its use in stringent industries. Furthermore, implementing new refining technologies requires very high capital investments against which small and mid-sized manufacturers cannot compete. Stringent quality standards imposed by regulatory authorities require firms to develop advanced purification technologies, leading to higher operating costs and increasing entry barriers for new players entering this market.

Naphthalene Market Segmentation Analysis

By Source

The coal tar segment held the largest market share around 68% in 2023. It is owing to its high availability from coke production, a byproduct of steel production. Naphthalene derived from coal tar is cheaper than petroleum-based naphthalene and is thus the raw material of choice for construction, textiles, plastics, agrochemicals, and more. Also, substantial worldwide production of naphthalene from coal tar is concentrated in the Asia-Pacific area where the primary production is found in nations like China, India, and Japan, taking advantage of enormous-scale steel generation. That favorable supply situation is exacerbated by a greater yield of naphthalene from coal tar than from petroleum derivatives, which solidifies its position as a market leader. However, even with increasing environmental awareness, the development of purification techniques and emission control measures have facilitated the continued dominance of coal tar-derived naphthalene in the industry.

By Application

Phthalic anhydride manufacturing held the largest market share around 32% in 2023. This is due to its high application rate for the production of plasticizers, unsaturated polyester resins (UPRs), and alkyd resins. One of its intermediates, phthalic anhydride is necessary in the production of flexible polyvinyl chloride, coatings, paints, and adhesives utilized in the construction, automotive, and packaging industries. The surging expansion of infrastructure construction in major economies and industrialization, especially in Asia-Pacific, has largely propelled the consumption of phthalic anhydride products. Also, it uses high-purity naphthalene-derived phthalic anhydride, which is chosen for performance applications requiring higher performance and a greater service life. Despite alternatives and regulatory challenges, phthalic anhydride continues to retain market dominance, backed up by increasing investments in plastics, resins, and polymer industries.

Naphthalene Market Regional Outlook

Asia pacific held the largest market share around 42% in 2023. It is owing to the presence of a strong industrial base, rapid urbanization, and high demand from construction, textiles, plastics, and agrochemicals. China, India, and Japan are some of the largest producers of naphthalene from coal tar, supported by the continuous availability of coal tar due to large-scale steel production in the region. Moreover, rapid growth in construction and infrastructure sectors in the region, particularly, China and India will continue to propel the demand for naphthalene-based superplasticizers in concrete admixtures. The growing use of naphthalene in textile, dye, agrochemicals, and resin production contributes to maintaining a leading position in the region. Asia-Pacific is dominating the global naphthalene market and the reasons attributing this are low production costs, easy availability of raw materials, and enrichment in domestic consumption.

North America held a significant market share in 2023. It is owing to the long-standing construction, automotive, and specialty chemicals industries in the region. This is primarily driven by rising demand for naphthalene-based superplasticizers for concrete admixtures which is supported by ongoing infrastructure refurbishment projects in the region both in U.S. and Canada. In addition, the presence of phthalic anhydride manufacturers in the region further contributes to the naphthalene consumption for the production of plasticizers, resins, and coatings. Additionally, the increase in the demand for specialty applications like pharmaceuticals and advanced polymers can also support the growth of the high-purity naphthalene market. Despite being partially displaced by some sustainable products due to environmental regulations, refining and purification technologies continue to evolve, allowing North America to cement its position within the international naphthalene market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Rain Carbon Inc. (Calcined Petroleum Coke, Coal Tar Pitch)

-

JFE Chemical Corporation (Naphthalene, Phthalic Anhydride)

-

ExxonMobil Corporation (Crude Oil, Petrochemicals)

-

CARBOTECH (Activated Carbon, Carbon Solutions)

-

Epsilon Carbon Private Limited (Hard Carbon Black, Coal Tar Pitch)

-

Koppers Inc. (Carbon Materials, Wood Treatment Chemicals)

-

Rütgers Group (Aromatic Chemicals, Resins)

-

Nippon Steel Chemical Co., Ltd. (Naphthalene, Benzene)

-

Baoshan Iron & Steel Co., Ltd. (Steel Products, Naphthalene)

-

Haldia Petrochemicals Limited (Polymers, Chemicals)

-

Daejung Chemicals & Metals Co., Ltd. (Naphthalene, Chemical Reagents)

-

Himadri Speciality Chemical Ltd. (Advanced Carbon Materials, Naphthalene)

-

Formosa Petrochemical Corporation (Petrochemical Products, Naphtha)

-

WUXI HENGLI PETROCHEMICALS CO., LTD. (Petrochemical Products, Naphthalene)

-

JFE Shoji Trade Corporation (Chemicals, Naphthalene)

-

Shandong Sanwei Trade Co., Ltd. (Chemical Products, Naphthalene)

-

RÜTGERS Belgium NV (Chemical Intermediates, Naphthalene)

-

Aum Chemicals (Naphthalene Balls, Industrial Chemicals)

-

Sinobioway Group Co., Ltd. (Biochemicals, Naphthalene)

-

Mangalore Chemicals & Fertilizers Limited (Sulphonated Naphthalene Formaldehyde, Urea)

Recent Development:

-

In October 2023, BASF collaborated with a prominent construction materials company to innovate next-generation asphalt sealants incorporating recycled naphthalene derivatives. This initiative supports circular economy principles by integrating recycled materials into infrastructure applications.

-

In November 2022, Sulzer Chemtech revealed its partnership with Dong-Suh Company in Indonesia to supply process engineering expertise and essential equipment. This collaboration focuses on establishing a cutting-edge separation unit at Dong-Suh's Serang facility, enhancing the production of high-purity naphthalene.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 4.42 Billion |

| Market Size by 2032 | USD 6.04 Billion |

| CAGR | CAGR of 3.53% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Source (Coal Tar, Petroleum) •By Application (Phthalic Anhydride, Naphthalene Sulfonates, Low-Volatility Solvents, Moth Repellent, Pesticides, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Rain Carbon Inc., JFE Chemical Corporation, ExxonMobil Corporation, CARBOTECH, Epsilon Carbon Private Limited, Koppers Inc., Rütgers Group, Nippon Steel Chemical Co., Ltd., Baoshan Iron & Steel Co., Ltd., Haldia Petrochemicals Limited, Daejung Chemicals & Metals Co., Ltd., Himadri Speciality Chemical Ltd., Formosa Petrochemical Corporation, WUXI HENGLI PETROCHEMICALS CO., LTD., JFE Shoji Trade Corporation, Shandong Sanwei Trade Co., Ltd., RÜTGERS Belgium NV, Aum Chemicals, Sinobioway Group Co., Ltd., Mangalore Chemicals & Fertilizers Limited. |

Frequently Asked Questions

Ans: Asia Pacific led the Naphthalene Market in the region with the highest revenue share in 2023.

Ans: Volatility in feedstock prices which drives market growth.

Ans: The coal tar will grow rapidly in the Naphthalene Market from 2024-2032.

Ans: The expected CAGR of the global Naphthalene Market during the forecast period is 3.53%

Ans: The Naphthalene Market was valued at USD 4.42 Billion in 2023.

Get in Touch