Network Transformation Market Key Insights:

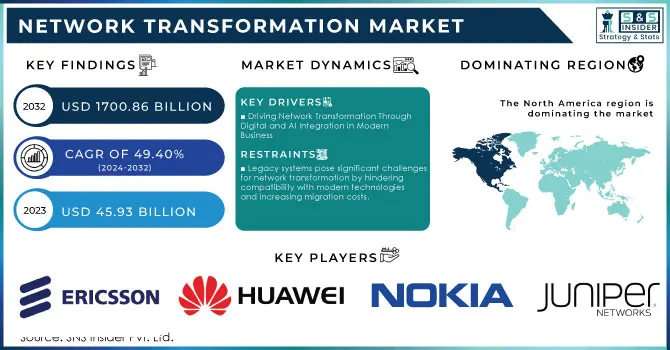

The Network Transformation Market size was valued at USD 45.93 Billion in 2023 and is expected to reach USD 1700.86 Billion by 2032 and grow at a CAGR of 49.40% over the forecast period 2024-2032. The network transformation market is undergoing significant growth, fueled by the increasing adoption of digital technologies across various sectors. Organizations are keen on enhancing operational efficiency and improving customer experiences through innovative networking solutions. The evolution of digital currencies, especially Central Bank Digital Currencies (CBDCs), is closely linked to the broader theme of network transformation in the financial landscape. As countries like Canada transition to digital currencies, traditional financial systems are undergoing significant changes to accommodate this shift. Currently, less than 5% of Canada’s overall money supply exists in physical currency, while 10% to 20% of Canadians are unbanked or underbanked, creating an impetus for enhanced financial inclusion through digital solutions.

To Get More Information on Network Transformation Market - Request Sample Report

The implementation of CBDCs, such as the Central Bank of The Bahamas’ Sand Dollar or Nigeria’s e-Naira, reflects a response to the need for more efficient and accessible financial services. These digital currencies promise faster transactions compared to traditional payment methods, which can take days to process. Moreover, they facilitate lower-cost international transfers, operate 24/7, and enable efficient government payments, thereby transforming how individuals and businesses interact with money. However, the transition to digital currencies is not without its challenges. The volatility associated with cryptocurrencies can hinder their acceptance by businesses, while the development costs of establishing a CBDC can be significant, particularly in jurisdictions where the concept is still theoretical. This approach aligns with the ongoing network transformation in finance, emphasizing the need for secure, efficient, and user-friendly digital payment systems. As countries continue to explore and implement CBDCs, the convergence of digital currency and network transformation could redefine the future of financial transactions, promoting greater efficiency and accessibility while addressing the existing challenges of traditional banking systems. The growing interest in the digital currency market, along with advancements in financial technology (fintech) and cryptocurrency adoption, suggests a significant shift in how global financial markets operate, ultimately paving the way for a more inclusive digital economy.

Market Dynamics

Drivers

- Driving Network Transformation Through Digital and AI Integration in Modern Business

One of the key drivers for the network transformation market is the growing demand for digital transformation across various industry sectors, particularly as organizations increasingly recognize the need to integrate cutting-edge technology into their operations. The Stanford Seed Transformation Network (SSTN) conference, themed “SMART Africa: Leapfrogging the Conventional and Transforming Business with AI,” highlights this shift, highlighting how businesses can leverage Artificial Intelligence (AI) to innovate and scale efficiently. As industries such as construction face significant challenges due to legacy systems and decentralized data, the push for digitalization becomes critical. According to McKinsey’s research, companies embracing digital transformation can achieve productivity increases of 14-15% and reduce costs by 4-6%. This evidence illustrates that adopting advanced technologies is no longer optional but essential for survival in a competitive market. The recent launch of Huawei's fully upgraded Xinghe Intelligent Network solutions emphasizes this trend, demonstrating how enterprises can harness AI to accelerate their digital and intelligent transformations. Organizations are motivated to streamline operations and improve efficiency, as highlighted during significant industry events like GITEX GLOBAL 2024. The integration of AI network products and solutions not only facilitates ubiquitous connectivity but also enhances data transmission efficiency and security. These advancements enable businesses to overcome barriers to digital adoption, transforming traditional operational models into agile, data-driven ecosystems. As the Network transformation market continues to evolve, the convergence of AI, digital transformation, and industry-specific innovations will play a pivotal role in shaping the future of IT management. Companies that prioritize these transformations will not only gain a competitive edge but also create sustainable growth in an increasingly digital world.

Restraints

- Legacy systems pose significant challenges for network transformation by hindering compatibility with modern technologies and increasing migration costs.

Legacy systems pose a significant restraint in the network transformation market, significantly hindering the transition to modern technologies. Many organizations are heavily reliant on outdated systems that are incompatible with contemporary digital solutions. This reliance creates substantial barriers to effective digital transformation. The complexity and cost associated with migrating or replacing these legacy systems can be daunting for businesses, often resulting in delays and increased expenditures. For instance, organizations report spending up to 75% of their IT budgets on maintaining legacy systems, which limits funds available for new technology investments. Additionally, approximately 80% of businesses struggle with data integration due to their reliance on these outdated systems, complicating efforts to implement more agile and innovative network infrastructures. The emotional attachment to these legacy systems can cause resistance among employees, further complicating transformation efforts. As organizations strive to adopt advanced technologies such as Artificial Intelligence (AI) and analytics, existing systems' lack of interoperability makes implementation increasingly challenging. Consequently, businesses may miss numerous advantages that modern network solutions can offer, including enhanced efficiency, improved customer experience and increased competitiveness in the digital age. Addressing this restraint will require a strategic approach to legacy system management, emphasizing phased migrations, employee training, and investment in adaptable technologies. By doing so, companies can pave the way for a smoother transition to a digitally transformed network, ultimately positioning themselves for long-term success.

Market Segmentation Analysis

By Services

The network transformation market has experienced considerable activity, with companies launching innovative solutions to meet rising demands. In 2023, solutions accounted for about 60% of total revenue in this market, encompassing advanced software for network management, security, and optimization. The swift adoption of technologies such as Artificial Intelligence (AI), Internet of Things (IoT), and 5G networks has created a need for robust solutions that can effectively integrate and support complex systems. Companies are increasingly looking for comprehensive solutions that enable the transition from traditional to agile and scalable network architectures. Notable launches include Cisco's Crosswork Network Controller, introduced in late 2023 to simplify and automate network operations; Juniper Networks' Cloud-Grade Networking Solutions, launched in early 2024, which focus on AI-driven automation for enterprise-level digital transformation; and Hewlett Packard Enterprise's Aruba Central, an AI-powered cloud-based platform designed to enhance network performance through advanced analytics. Looking ahead, the demand for flexible, scalable, and secure solutions is expected to grow, driven by the integration of cloud technologies and improved cybersecurity. This trend underscores the significance of the solutions segment in maintaining dominance in the network transformation market.

By Solution

In the network transformation market, the 5G networks segment has established itself as a significant player, accounting for approximately 46% of total revenue in 2023. This impressive share underscores the growing reliance on advanced communication technologies to meet the evolving needs of businesses and consumers. The introduction of 5G has marked a pivotal shift in connectivity, offering faster speeds, lower latency, and enhanced capacity, thereby becoming integral to modern network infrastructure. The surge in the 5G networks segment is largely fueled by the rising demand for high-speed internet and the rapid expansion of connected devices. Sectors such as telecommunications, healthcare, and automotive are harnessing 5G capabilities to drive innovations, including smart cities, autonomous vehicles, and improved remote healthcare services. Additionally, the proliferation of Internet of Things (IoT) solutions has amplified the need for robust network infrastructures. Key industry players are making substantial investments in 5G technology. Verizon has rolled out its 5G Ultra Wideband service in various cities, enhancing connectivity for consumers and businesses. Similarly, Ericsson has launched its 5G RAN solutions, focusing on cloud-native offerings, while Nokia's AirScale portfolio emphasizes advanced radio access for 5G deployment. As organizations embrace digital transformation, the demand for 5G networks is poised for exponential growth, positioning them as essential for future network architectures.

Regional Analysis

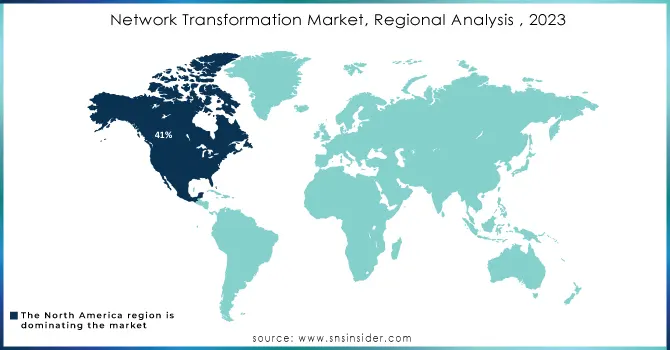

In 2023, North America solidified its position as the leading region in the network transformation market, capturing around 41% of total revenue. This dominant share is indicative of the region’s strong technological infrastructure, the presence of major telecommunications players, and an aggressive approach to implementing advanced networking solutions. The surge in demand for digital transformation across various sectors, including telecommunications, healthcare, finance, and manufacturing, has been a key driver of growth. North America's leadership include the swift rollout of 5G networks, substantial investments in cloud computing, and the rapid expansion of Internet of Things (IoT) devices. Telecommunications giants like Verizon and AT&T are significantly investing in 5G infrastructure, enhancing connectivity and supporting improved business operations through advanced data transmission and real-time analytics. The region’s commitment to research and development has also spurred innovation in networking technologies, with companies such as Cisco and Juniper Networks leading the charge in providing solutions that enable smooth transitions from legacy systems to modern architectures. Additionally, regulatory initiatives promoting digitalization further enhance market growth. As awareness of digital transformation's significance rises, North America is poised to maintain its leadership in the network transformation market, continually shaping global trends and innovations.

In 2023, the Asia Pacific region emerged as the fastest-growing market for network transformation, driven by rapid technological advancements and substantial investments in digital infrastructure. Key factors fueling this growth include the widespread adoption of 5G technology, the increasing number of Internet of Things (IoT) devices, and a strong focus on digital transformation across diverse industries. Leading countries such as China, India, and Japan are at the forefront, capitalizing on their robust telecommunications sectors and government initiatives to enhance connectivity and promote innovation. The demand for advanced networking solutions in telecommunications, healthcare, and manufacturing is escalating, as organizations seek faster data processing and greater operational efficiency. In response to this demand, major companies in the region are launching innovative products. For example, Huawei unveiled its Cloud Campus 3.0 in late 2023, offering AI-driven solutions to enhance enterprise-networking capabilities and improve performance and security. Additionally, Samsung rolled out its 5G end-to-end solutions to support smart city applications, focusing on low latency and high reliability for critical services. Furthermore, NTT Communications has introduced its Smart Data Platform, which integrates IoT and AI to enhance analytics and decision-making in business operations.

Do You Need any Customization Research on Network Transformation Market - Inquire Now

Recent Developments

-

On October 15, 2024, during the Association of the U.S. Army’s Annual Meeting and Exposition, Army Undersecretary Gabe Camarillo highlighted the U.S. Army's commitment to advancing its network transformation by simplifying and unifying its communication systems while leveraging existing private sector technologies. He emphasized the importance of enhancing institutional processes to effectively adopt and integrate these innovations, unlocking their potential for improved command and control capabilities.

-

On October 23, 2024, Ericsson announced a partnership with Singtel to streamline network service procurement for operators and enterprise customers. By integrating Singtel’s Paragon platform with Ericsson’s Service Orchestration and Assurance platform, the collaboration aims to simplify the acquisition of new network solutions.

-

On July 10, 2024, Walmart's Executive Vice President of Supply Chain Operations, Dave Guggina, emphasized the company's commitment to supply chain modernization to enhance customer options. He noted the growing popularity of Walmart's delivery services and innovative in-store and online experiences as shoppers increasingly seek ways to save money and improve their lifestyles.

-

On November 14, 2024, a live webinar titled "Diversity at the Edge: Metro Network Transformation in the Era of Intelligent Coherent Pluggables" will explore the increasing importance of efficient optical transport as bandwidth surges across residential, business, and mobile networks. The discussion will focus on how the edge of the optical transport network can effectively manage diverse traffic types and service requirements to enhance flexibility, scalability, and overall network economics.

Key Players

Some of the Major key Players in Network Transformation with their products:

-

Cisco Systems, Inc. (Cisco Nexus Series Switches)

-

Nokia Corporation (Nokia 5G AirScale)

-

Juniper Networks, Inc. (Juniper MX Series Routers)

-

Arista Networks, Inc. (Arista 7280R Series Switches)

-

Hewlett Packard Enterprise (HPE) (HPE Aruba Networking Solutions)

-

Huawei Technologies Co., Ltd. (Huawei 5G RAN Solutions)

-

Ericsson (Ericsson Radio System)

-

Dell Technologies Inc. (Dell EMC Networking)

-

Extreme Networks, Inc. (ExtremeCloud IQ)

-

IBM Corporation (IBM Cloud Pak for Network Automation)

-

VMware, Inc. (VMware NSX)

-

ZTE Corporation (ZTE 5G Core)

-

Ciena Corporation (Ciena 6500 Packet-Optical Platform)

-

CommScope Holding Company, Inc. (CommScope Ruckus Wireless)

-

F5 Networks, Inc. (F5 BIG-IP)

-

Netgear, Inc. (Netgear Nighthawk M5 5G Mobile Router)

-

Silver Peak (part of HPE) (Silver Peak Unity EdgeConnect)

-

Mitel Networks Corporation (Mitel MiCloud Connect)

-

Riverbed Technology, Inc. (Riverbed SteelHead)

-

Palo Alto Networks, Inc. (Palo Alto Networks Next-Generation Firewalls)

List of 10 potential customers of network transformation solutions, along with specific companies from various industries:

-

Verizon Communications Inc.

Industry: Telecommunications

-

Amazon Web Services (AWS)

Industry: Cloud Service Provider

-

JPMorgan Chase & Co.

Industry: Financial Services

-

Kaiser Permanente

Industry: Healthcare

-

Siemens AG

Industry: Manufacturing

-

Walmart Inc.

Industry: Retail

-

NASA (National Aeronautics and Space Administration)

Industry: Government Agency

-

Harvard University

Industry: Education

-

FedEx Corporation

Industry: Transportation and Logistics

-

Duke Energy Corporation

Industry: Energy and Utilities

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 45.93 Billion |

| Market Size by 2032 | USD 1700.86 Billion |

| CAGR | CAGR of 49.40% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (5G Networks, C-RAN, Network Automation, SDN & NFV) • By Service (Professional Service and Managed Service) • By Enterprise Size (Large Enterprise and Small & Medium Enterprise) • By End User (BFSI, Energy & Utility, Government, Healthcare, IT & Telecom, Manufacturing, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cisco Systems, Inc., Nokia Corporation, Juniper Networks, Inc., Arista Networks, Inc., Hewlett Packard Enterprise (HPE), Huawei Technologies Co., Ltd., Ericsson, Dell Technologies Inc., Extreme Networks, Inc., IBM Corporation, VMware, Inc., ZTE Corporation, Ciena Corporation, CommScope Holding Company, Inc., F5 Networks, Inc., Netgear, Inc., Silver Peak (part of HPE), Mitel Networks Corporation, Riverbed Technology, Inc., and Palo Alto Networks, Inc. |

| Key Drivers | • Driving Network Transformation Through Digital and AI Integration in Modern Business |

| RESTRAINTS | • Legacy systems pose significant challenges for network transformation by hindering compatibility with modern technologies and increasing migration costs. |

Frequently Asked Questions

Solution is dominating in Network Transformation Market in 2023

North America is dominate region in Network Transformation market in 2023.

The segments covered in the Network Transformation Market report for study are based on Solution, Service, Enterprise Size, and End User.

Ans: The major key driver in the Network Transformation Market is the increasing demand for higher network performance and efficiency due to the rise of digitalization and cloud computing.

The Network Transformation Market size was valued at USD 45.93 Billion in 2023 and is expected to reach USD 1700.86 Billion by 2032 and grow at a CAGR of 49.40% over the forecast period 2024-2032.

Get in Touch