Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Report Scope & Overview:

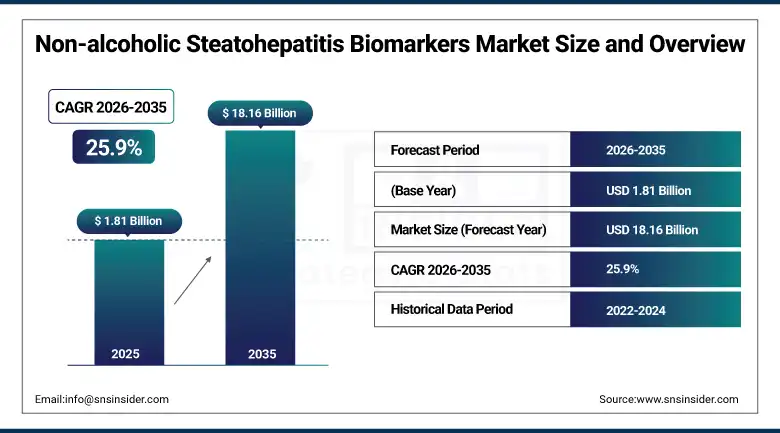

The Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market was valued at USD 1.81 Billion in 2025 and is expected to reach USD 18.16 Billion by 2035, growing at a CAGR of 25.9% from 2026–2035.

The global NASH biomarkers market is growing at an exceptional pace. Non-alcoholic steatohepatitis is a serious variant of non-alcoholic fatty liver disease characterised by liver inflammation and hepatocyte damage that can progress to cirrhosis, liver failure, and hepatocellular carcinoma. NASH affects approximately 20% of the general population globally and is expected to become the leading cause of liver transplantation in the U.S. within this decade. The increasing global prevalence of NASH, coupled with the rising adoption of non-invasive diagnostic tools to replace costly and complication-ridden traditional liver biopsies, is significantly driving market growth.

In 2024, GENFIT launched NASHnext through its exclusive U.S. and Canada distribution partnership with Labcorp, using its proprietary NIS4 technology—a novel blood-based molecular biomarker test validated in The Lancet Gastroenterology and Hepatology—to detect at-risk NASH patients with significant fibrosis. The commercial launch represents the first widely accessible non-invasive NASH biomarker test whose clinical validation and laboratory distribution infrastructure creates the diagnostic pathway that Rezdiffra's prescription requires, directly linking the drug approval event to biomarker test commercial demand.

Market Size and Forecast

-

Market Size in 2026E: USD 2.28 Billion

-

Market Size by 2035: USD 18.16 Billion

-

CAGR: 25.9% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Non-alcoholic Steatohepatitis Biomarkers Market - Request Free Sample Report

Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Trends

-

The FDA approval of Rezdiffra for NASH treatment is increasing demand for companion diagnostic biomarkers.

-

AI-powered diagnostic platforms are improving the accuracy of NASH detection through advanced analysis of multi-analyte biomarker data.

-

Non-invasive biomarker tests are increasingly replacing liver biopsy for NASH diagnosis and disease staging.

-

Growing use of biomarker-based endpoints in pharmaceutical clinical trials is driving demand for validated NASH biomarker assays..

-

Development of wearable and continuous monitoring technologies for metabolic disease biomarkers is expanding future diagnostic possibilities.

U.S. Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Outlook

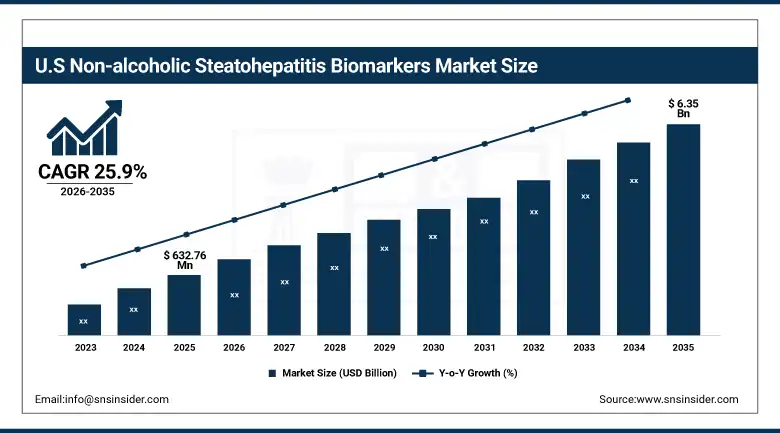

The U.S. Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market was valued at approximately USD 632.76 Million in 2025 and is expected to reach approximately USD 6.35 Billion by 2035, growing at a CAGR of approximately 25.9%.

The U.S. is the world's most commercially advanced NASH biomarkers market within North America's 40% global revenue dominance. The Rezdiffra approval creates a commercial inflection point whose prescription volume, estimated at 300,000-500,000 eligible U.S. patients in the initial launch period, creates proportional companion diagnostic biomarker demand. GENFIT's NASHnext through Labcorp, Prometheus Laboratories' Prometheus Detect panel, and Quest Diagnostics' NASH testing services collectively define the commercial NASH biomarker testing infrastructure whose procurement scales with Rezdiffra prescription volume and the growing NAFLD screening programme's diagnostic assessment requirements.

Madrigal Pharmaceuticals received FDA approval for Rezdiffra (resmetirom) in March 2024, the first approved treatment specifically for NASH with liver fibrosis in adults. The approval creates a validated treatment pathway that fundamentally transforms the NASH biomarker market by requiring FIB-4 score and liver biopsy or non-invasive test confirmation of NASH with significant fibrosis before treatment initiation, creating structured clinical biomarker assessment procurement for each treated patient across the approved indication population.

Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Segment Analysis

-

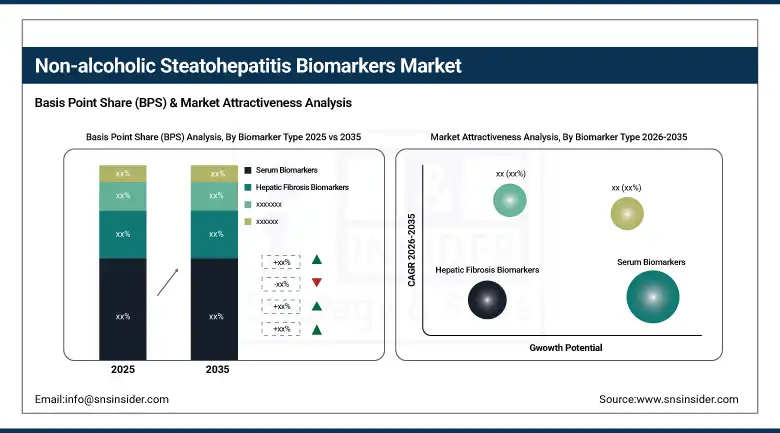

By Biomarker Type, the Serum Biomarkers segment dominated the Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market with approximately 32.51% share in 2025, while the Hepatic Fibrosis Biomarkers segment is the fastest growing.

-

By Diagnostic Technique, the Serum-Based Testing segment dominated the Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market with approximately 56.80% share in 2025, while the Imaging Biomarkers segment is the fastest growing.

-

By Application, the Drug Development segment dominated the Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market with approximately 44.20% share in 2025, while the Clinical Diagnosis segment is the fastest growing.

-

By End User, the Pharmaceutical Companies & CROs segment dominated the Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market with approximately 51.60% share in 2025, while the Hospitals & Diagnostic Centres segment is the fastest growing.

By Biomarker Type, serum biomarkers dominate, hepatic fibrosis biomarkers grow fastest

Serum biomarkers retained the dominant biomarker type position with approximately 32.51% of the NASH biomarkers market in 2025. Their commercial primacy reflects the clinical accessibility and established laboratory infrastructure for blood-based liver function test procurement whose routine integration into metabolic disease management creates the largest aggregate NASH biomarker testing volume. Traditional serum biomarkers including alanine transaminase and aspartate transaminase, whose elevations indicate hepatocellular injury, provide initial NASH screening at standard laboratory cost. Novel serum biomarkers including CK-18-M30, whose elevation correlates with active NASH’s hepatocyte apoptosis, and FGF-21, whose dysregulation reflects NASH metabolic pathway disruption, create above-standard laboratory procurement whose clinical validation is progressively establishing their routine clinical use alongside traditional liver function tests.

Hepatic fibrosis biomarkers are the fastest-growing biomarker type because Rezdiffra’s prescribing information requirement for fibrosis stage assessment before treatment initiation creates structured clinical demand for validated fibrosis biomarker assessment in every eligible patient. FIB-4 score calculation, Enhanced Liver Fibrosis panel, Pro-C3 measurement, and GENFIT’s NIS4 technology each represent validated fibrosis assessment approaches whose clinical adoption is growing with Rezdiffra’s commercial rollout. Each patient prescribed Rezdiffra creates a defined hepatic fibrosis biomarker procurement requirement whose commercial scale compounds with the drug’s prescription volume growth across the initially approved 300,000-500,000 eligible U.S. patient population.

By Application, drug development dominates, clinical diagnosis grows fastest

Drug development retained the dominant application position in the NASH biomarkers market in 2025. The pharmaceutical industry’s extraordinary clinical investment in NASH therapeutics, encompassing dozens of phase 2 and phase 3 programmes across multiple mechanism classes, creates the most commercially concentrated institutional biomarker procurement of any application category. Each NASH clinical trial requires biomarker testing at enrolment for patient stratification, at multiple timepoints during treatment for pharmacodynamic assessment, and at endpoint for regulatory efficacy demonstration whose per-patient biomarker testing cost multiplied across trial participant counts creates programme-level biomarker procurement of substantial commercial value.

Clinical diagnosis is the fastest-growing application because Rezdiffra’s commercial launch is converting the NASH biomarker market from a pharmaceutical research-dominated procurement model toward a mixed model where routine clinical diagnostic testing creates a new and rapidly growing revenue stream. Each hepatologist and gastroenterologist who adopts non-invasive NASH diagnostic testing as part of routine NAFLD patient management creates ongoing diagnostic biomarker procurement whose aggregate across the hepatology clinical community compounds with growing NASH awareness and screening programme adoption.

By Diagnostic Technique, serum-based dominates, imaging grows fastest

Serum-based testing retained the dominant diagnostic technique position in the NASH biomarkers market in 2025. The simplicity and accessibility of blood-based NASH assessment creates the most widely deployable diagnostic approach whose infrastructure requirement of a standard clinical laboratory venipuncture capability creates availability across the full range of clinical settings from academic medical centres through primary care offices. Each laboratory that adds NASH biomarker panels to its standard test menu creates a new clinical testing channel whose procurement compounds with patient volume growth. BioPredictive’s FibroTest, GENFIT’s NIS4, and Enhanced Liver Fibrosis panel each represent validated serum-based NASH assessment tools whose laboratory distribution through major diagnostic networks creates accessible commercial procurement.

Imaging biomarkers are the fastest-growing diagnostic technique because FibroScan’s controlled attenuation parameter for steatosis quantification and magnetic resonance elastography for fibrosis assessment are providing non-invasive liver structure characterisation whose diagnostic accuracy in experienced hands approaches liver biopsy performance for fibrosis staging. Each new FibroScan installation at a hepatology centre creates imaging biomarker procurement that compounds with the growing number of clinical sites adopting point-of-care hepatic elastography as standard NASH evaluation infrastructure.

By End User, pharma & CROs dominate, hospitals grow fastest

Pharmaceutical companies and CROs retained the dominant end user position in the NASH biomarkers market in 2025. The pharmaceutical industry’s pipeline of NASH drug candidates whose clinical development requires validated biomarker assessment at multiple trial stages creates the most commercially concentrated institutional procurement in the market. Companies including Madrigal Pharmaceuticals, AstraZeneca, Gilead Sciences, and Novo Nordisk’s clinical teams collectively create biomarker test procurement whose combined trial programme volume defines the pharmaceutical end user category’s commercial scale. CROs supporting these programmes add procurement volume that sustains the category’s dominant commercial position.

Hospitals and diagnostic centres are the fastest-growing end user because Rezdiffra’s commercial rollout is creating routine clinical NASH biomarker testing infrastructure investment at hepatology centres, gastroenterology practices, and hospital-based liver disease programmes whose combined procurement growth is the most commercially dynamic expansion in the market. Each hospital that establishes a structured NASH clinical pathway creates biomarker testing procurement whose annual volume scales with the liver disease patient population whose NAFLD and NASH assessment is progressively incorporated into metabolic disease management protocols.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Insights

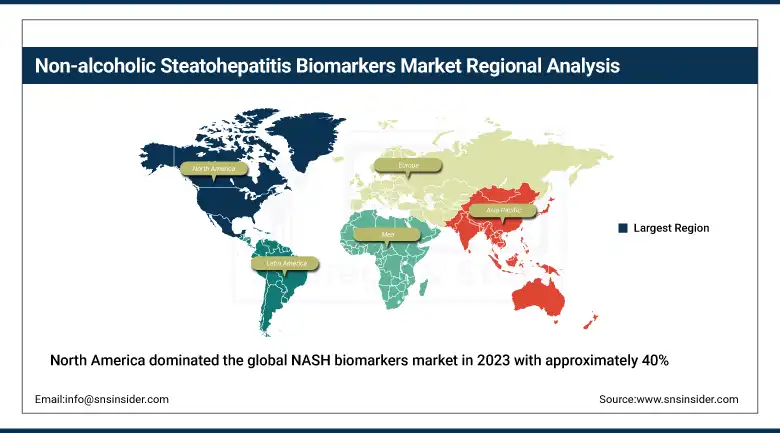

North America dominated the global NASH biomarkers market in 2023 with approximately 40% of overall market share. The United States accounts for approximately 87.4% of North American revenues through its well-developed healthcare infrastructure, significant R&D expenditure, and high NASH prevalence resulting from obesity and metabolic disorders. Rezdiffra’s FDA approval creates the most commercially transformative demand driver in the market’s history whose prescription volume is progressively establishing routine clinical NASH biomarker testing infrastructure across U.S. hepatology and gastroenterology clinical practice.

Canada contributes approximately 12.6% of North American revenues through its publicly funded healthcare system’s growing NASH diagnostic investment, active liver disease research community, and GENFIT’s NASHnext test’s Canadian market access through the Labcorp distribution partnership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Insights

Europe is a technically sophisticated NASH biomarkers market where GENFIT’s French headquarters, EU regulatory pathway for non-invasive liver diagnostic tests, and the European Association for the Study of the Liver’s clinical practice guidelines create a structured institutional adoption environment. Germany accounts for approximately 22.3% of European revenues through its advanced hospital hepatology infrastructure, pharmaceutical industry’s clinical trial activity, and the growing private laboratory network’s NASH biomarker panel adoption.

The United Kingdom and France are significant secondary markets where NHS gastroenterology programme investment, GENFIT’s French commercial presence, and active hepatology clinical research communities create consistent NASH biomarker procurement. The EMA’s progressive evaluation of resmetirom for European approval will create the same companion diagnostic demand driver in Europe that Rezdiffra’s U.S. approval has created.

Asia Pacific Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Insights

Asia Pacific is the fastest-growing regional NASH biomarkers market due to rapidly rising NAFLD and NASH burden across China, India, Japan, South Korea, and Southeast Asia whose dietary transition toward high-calorie processed food and increasingly sedentary lifestyle is creating above-average NASH incidence growth. China accounts for approximately 44.8% of Asia Pacific revenues through its large patient population whose NAFLD prevalence is estimated at 30%, creating the world’s largest national NASH patient burden whose diagnostic assessment creates substantial unmet biomarker testing demand.

India and Japan represent commercially significant secondary markets where NASH prevalence is growing with metabolic disease burden and the healthcare system’s progressive capability to assess and treat liver disease is creating structured biomarker procurement. The growing clinical trial activity for NASH therapeutics in Asia Pacific is simultaneously creating pharmaceutical industry biomarker procurement whose contribution compounds with clinical diagnostic adoption.

MEA & Latin America Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Insights

The Middle East and Africa and Latin America are growing NASH biomarkers markets where obesity prevalence, metabolic disease burden, and healthcare infrastructure development are creating structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through its above-average obesity prevalence whose NASH burden creates diagnostic demand, the advanced hospital system’s hepatology capability, and pharmaceutical company clinical trial activity.

Brazil leads Latin American revenues at approximately 44.2% through its large hospital network’s hepatology infrastructure, growing pharmaceutical industry’s clinical research activity, and the Brazilian population’s above-average NAFLD prevalence whose diagnostic assessment creates structured NASH biomarker procurement across the country’s major liver disease centres.

Market Dynamics

Growth Drivers: First NASH drug approval creating companion diagnostic demand and rising NASH prevalence creating diagnostic unmet need

The FDA approval of Rezdiffra in March 2024 is the single most commercially transformative event in the NASH biomarkers market’s history. Before drug approval, NASH biomarker testing was primarily a pharmaceutical research procurement activity. After approval, each new Rezdiffra prescription creates a defined clinical biomarker assessment requirement whose aggregate across the drug’s growing prescription volume creates a new and rapidly growing routine diagnostic biomarker demand stream that is independent of research activity. The estimated 17 million Americans with NASH fibrosis who may be eligible for treatment creates a commercial biomarker testing opportunity whose scale substantially exceeds the pre-approval market.

Rising global NASH prevalence driven by the obesity epidemic’s progression in both developed and developing economies creates a structurally growing diagnostic unmet need whose biomarker solution market grows with the patient population’s diagnosis and clinical management requirements. The WHO’s projection that 50% of the global adult population will be overweight by 2030 creates a demographic trajectory whose metabolic disease cascade toward NAFLD and NASH sustains biomarker market growth independent of any individual drug approval event.

Restraints: Lack of FDA-approved companion diagnostic and need for clinical validation of novel biomarker panels

The absence of FDA-approved companion diagnostic tests specifically indicated for Rezdiffra patient selection creates regulatory uncertainty about which biomarker tests satisfy the prescribing information’s diagnostic requirement. Clinicians’ variable interpretation of acceptable non-invasive fibrosis assessment creates inconsistent biomarker test specification that limits the structured commercial adoption that a formally approved companion diagnostic would create. Each clinical practice guideline update that specifies validated non-invasive test alternatives builds the procurement clarity that sustains consistent commercial growth.

Novel NASH biomarker panel clinical validation requires the prospective study evidence that regulatory agencies and payer coverage decisions demand before widespread clinical adoption creates structured commercial procurement. Each new biomarker assay that enters clinical validation requires multi-centre studies whose combined enrolment and follow-up duration extends commercialisation timelines by 3-7 years from initial assay development, creating a commercial reality where innovation pipeline and current market demand are separated by a validation timeline that requires sustained R&D investment patience.

Opportunities: Rezdiffra companion diagnostic development and multi-omics NASH biomarker panel commercialisation

Rezdiffra companion diagnostic development represents the most commercially premium near-term NASH biomarker opportunity whose FDA approval would create the most structured and defensible biomarker procurement requirement in the market. A formally approved companion diagnostic whose label indication specifically requires testing before Rezdiffra prescription creates a mandatory procurement event that eliminates the clinical practice variability that currently moderates biomarker test specification. Each pharmaceutical company pursuing NASH drug approval simultaneously has commercial motivation to develop companion diagnostic tests whose regulatory approval creates both patient selection utility and commercial market exclusivity.

Multi-omics NASH biomarker panel commercialisation using combined genomic, proteomic, metabolomic, and lipidomic analysis is creating next-generation diagnostic products whose sensitivity and specificity for NASH detection and staging substantially exceed any individual biomarker approach. AI-powered platform analysis of multi-analyte data creates diagnostic accuracy approaching liver biopsy performance whose non-invasive delivery creates the commercial value proposition that sustains premium diagnostic test pricing and drives clinical adoption acceleration.

Recent Developments:

-

2024: GENFIT launched NASHnext through an exclusive U.S. and Canada distribution partnership with Labcorp in 2024, using NIS4 technology to detect at-risk NASH patients with significant fibrosis through a novel blood-based molecular biomarker test validated in The Lancet Gastroenterology and Hepatology.

-

2024: Madrigal Pharmaceuticals received FDA approval for Rezdiffra (resmetirom) in March 2024 as the first approved treatment specifically for NASH with liver fibrosis, fundamentally transforming the NASH biomarker market by creating a validated treatment pathway requiring companion biomarker assessment for patient selection.

-

2024: Prometheus Laboratories expanded its Prometheus Detect NASH assessment panel commercial availability in 2024 through additional clinical laboratory network partnerships, increasing non-invasive NASH diagnostic test accessibility for hepatologists and gastroenterologists managing NAFLD patient populations across U.S. clinical practice settings.

Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market Key Players

-

GENFIT S.A.

-

Prometheus Laboratories Inc.

-

Quest Diagnostics

-

Labcorp Holdings

-

Siemens Healthineers

-

BioPredictive S.A.S.

-

Madrigal Pharmaceuticals

-

Gilead Sciences

-

Novo Nordisk

-

AstraZeneca

-

Pfizer Inc.

-

Bristol-Myers Squibb

-

Abbott Laboratories

-

Roche Diagnostics

-

Hologic Inc.

-

Exalenz Bioscience Ltd.

-

Norgine B.V.

-

Novartis AG

-

Allergan (AbbVie)

-

Intercept Pharmaceuticals

Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.81 Billion |

| Market Size by 2035 | USD 18.16 Billion |

| CAGR | CAGR of 25.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Biomarker Type (Serum Biomarkers, Hepatic Fibrosis Biomarkers, Oxidative Stress Biomarkers, Apoptosis Biomarkers, Genomic/Proteomic Biomarkers, Others) • by Diagnostic Technique (Imaging Biomarkers, Serum-Based Testing, Histological Biomarkers) • by Application (Drug Development, Clinical Diagnosis, Research Applications) • by End User (Pharmaceutical Companies & CROs, Research Institutes & Academics, Hospitals & Diagnostic Centres) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | GENFIT S.A., Prometheus Laboratories Inc., Quest Diagnostics, Labcorp Holdings, Siemens Healthineer, BioPredictive S.A.S., Madrigal Pharmaceuticals, Gilead Sciences, Novo Nordisk, AstraZeneca, Pfizer Inc., Bristol-Myers Squibb, Abbott Laboratories, Roche Diagnostics, Hologic Inc., Exalenz Bioscience Ltd., Norgine B.V., Novartis AG, Allergan (AbbVie), Intercept Pharmaceuticals |

Frequently Asked Questions

The Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market is expected to grow at a CAGR of 25.9% from 2026 to 2035.

The Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market was valued at USD 1.81 Billion in 2025.

Rising global NASH prevalence driven by the obesity epidemic creating a structurally growing diagnostic unmet need.

Serum Biomarkers dominated the Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market with approximately 32.51% share in 2025, while Hepatic Fibrosis Biomarkers is the fastest growing.

North America dominated the Non-Alcoholic Steatohepatitis (NASH) Biomarkers Market in 2023 with approximately 40% of overall market share, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch