Nurse Call System Market Report Scope & Overview:

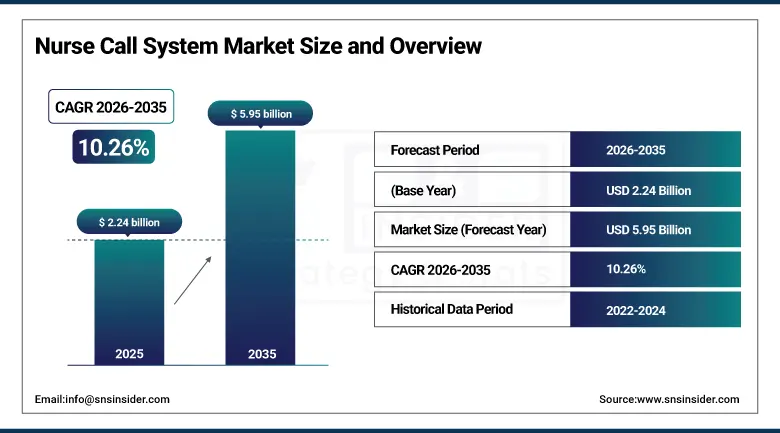

The Nurse Call System Market was valued at USD 2.24 Billion in 2025 and is expected to reach USD 5.95 Billion by 2035, growing at a CAGR of 10.26% from 2026–2035.

The global nurse call system market is experiencing a meaningful and broad-based expansion driven by the intersection of demographic ageing creating larger patient populations requiring institutional care, healthcare system-wide investment in patient safety infrastructure, and the progressive digitalization of clinical communication that is transforming nurse call from a simple call-and-respond alerting mechanism into an integrated clinical workflow platform connecting patients, nursing staff, physicians, and ancillary care providers in real-time communication ecosystems. The fundamental commercial driver underlying the market’s growth is the global imperative to improve patient response times and care communication quality in a healthcare delivery environment where nurse-to-patient ratios are under pressure from staffing shortages, patient acuity is rising as populations age and comorbidity prevalence grows, and regulatory frameworks in major healthcare markets are increasingly formalising patient response time standards and communication protocol requirements that advanced nurse call system capabilities are uniquely positioned to satisfy.

Sensio’s January 2025 long-term strategic agreement with Lovett Care to facilitate the development of sensor technology RoomMate and a digital nurse call system that integrates passive infrared and AI-based fall detection with nurse call alerting exemplifies the technology convergence that is defining the next generation of nurse call systems, where the traditional manual call-initiation model is being supplemented by AI-powered passive monitoring that detects patient distress conditions and generates nurse alerts automatically without requiring the patient to consciously activate a call mechanism.

Market Size and Forecast

-

Market Size in 2026E: USD 2.47 Billion

-

Market Size by 2035: USD 5.95 Billion

-

CAGR: 10.26% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Nurse Call System Market - Request Free Sample Report

Nurse Call System Market Trends

-

Accelerating integration of real-time location system technology within nurse call platforms, enabling automated patient location tracking that routes nurse call alerts to the nearest available care provider.

-

Growing adoption of mobile nurse call integration that routes patient alerts directly to staff smartphones and wireless handsets rather than requiring nurses to return to fixed stations for call receipt.

-

Rising deployment of AI-powered fall prevention and predictive risk monitoring integrated with nurse call alerting, where machine learning analysis of patient movement patterns, bed sensor data.

-

Expanding interoperability of nurse call systems with electronic health record platforms, patient monitoring systems, and building management systems through HL7 FHIR and standardised API integration.

-

Growing adoption of nurse call systems in homecare and remote care settings as the expansion of hospital-at-home programme models and independent living support technology creates demand for nurse call equivalent safety monitoring.

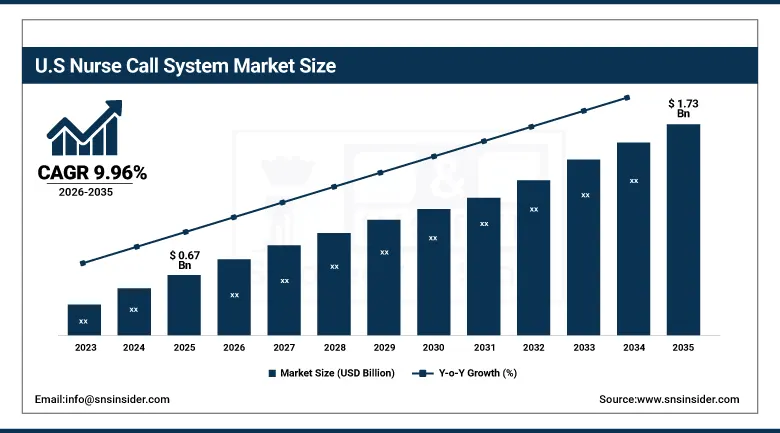

U.S. Nurse Call System Market Outlook

The U.S. Nurse Call System Market was valued at approximately USD 0.67 Billion in 2025 and is expected to reach approximately USD 1.73 Billion by 2035, growing at a CAGR of approximately 9.96%.

The United States nurse call system market is the world’s largest by value, driven by the country’s combination of the highest healthcare infrastructure capital investment per capita globally, the most comprehensive regulatory framework for patient safety standards including The Joint Commission’s national patient safety goals and CMS’s Conditions of Participation for Medicare-participating hospitals that create compliance-based demand for advanced nurse call and clinical communication systems, and the most commercially sophisticated healthcare technology procurement market whose value-based care reimbursement model creates strong institutional incentives to invest in operational efficiency and patient satisfaction improvement technologies.

The American Nurses Association’s 2025 workforce report documenting persistent nursing staff shortages across U.S. hospital systems, particularly in ICU, emergency department, and overnight shift coverage, is creating additional operational motivation for nurse call system technology investment that maximises the clinical communication efficiency and alert triage capability of the available nursing workforce, with systems that automatically prioritise alerts by clinical urgency, route alerts to the nearest available nurse, and provide context-aware clinical information at alert notification reducing the cognitive load and physical movement time that inefficient alert management imposes on already stretched nursing teams.

Nurse Call System Market Segment Analysis

-

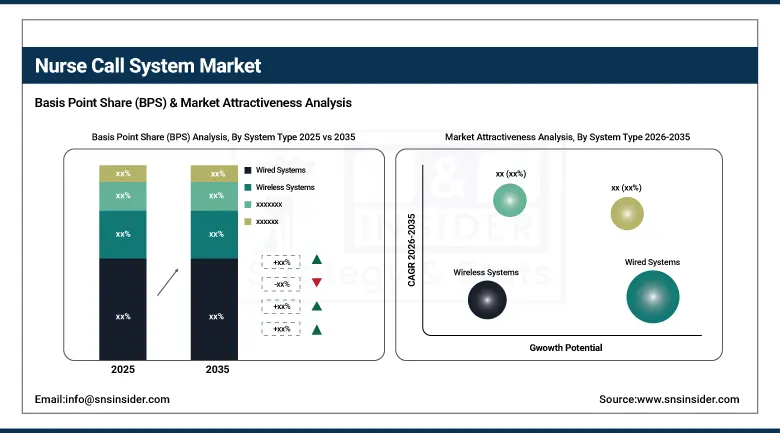

By System Type, wired systems led the nurse call system market with approximately 58.40% share in 2025 through their reliability, compatibility with existing cabling infrastructure in established healthcare facilities, and proven performance in large hospital environments where wired network infrastructure provides the signal integrity and network resilience that mission-critical patient safety alerting requires; wireless systems are the fastest-growing segment at a CAGR of approximately 11.60% as healthcare environments choose systems that offer installation flexibility, scalability without significant cabling investment, and compatibility with the mobile clinical communication ecosystem.

-

By Component, button systems held approximately 40.80% market share in 2025 owing to their simplicity, low cost, and excellent reliability for urgent help requests in acute care settings; mobile systems are the fastest-growing component driven by the increasing deployment of smartphone and wireless device-based nurse call alert receipt and acknowledgement that extends clinical communication beyond fixed station infrastructure.

-

By Application, emergency medical alarms dominated the market with approximately 36.70% share in 2025 owing to growing demand for urgent response systems in critical care and emergency departments; workflow support applications are the fastest-growing segment with a CAGR of approximately 12.30% as hospitals invest in systems that automate staff communication, task assignment, and clinical process coordination beyond simple patient-to-nurse alerting.

-

By End User, hospitals and clinics accounted for the largest share at approximately 46.50% in 2025 as the primary high-volume patient care settings requiring comprehensive nurse call infrastructure; nursing homes and assisted living centres showed the highest growth rate with a CAGR of approximately 10.90% as demographic ageing expands the elderly care facility population and regulatory requirements for patient safety communication systems in long-term care settings strengthen.

By System Type, wired systems dominate, wireless grows fastest

Wired systems retained the dominant system type position with approximately 58.40% of the nurse call system market in 2025, reflecting the established technology’s fundamental advantages in healthcare environments where reliability, signal integrity, and resistance to electromagnetic interference from medical equipment are mission-critical requirements whose failure consequences in patient safety alerting contexts are operationally unacceptable. The wired nurse call system’s commercial durability in the established hospital market reflects the large installed base of wired infrastructure whose replacement requires significant capital investment and operational disruption that healthcare facilities defer unless the capability limitations of existing systems create patient safety or operational efficiency problems of sufficient magnitude to justify transition. Modern wired nurse call systems from leading providers including Rauland-Borg, Ascom, and STANLEY Healthcare have evolved significantly beyond their legacy analogue predecessors, incorporating IP-network architecture, EHR integration, real-time location system connectivity, and mobile alert routing within a wired backbone infrastructure that delivers the reliability advantages of physical network connectivity alongside the advanced clinical workflow capabilities of modern digital healthcare communication platforms.

Wireless systems are the fastest-growing segment at a CAGR of approximately 11.60% through 2035, driven by the installation flexibility and scalability advantages that wireless nurse call architectures provide in three increasingly commercially important application contexts: new construction healthcare facilities whose architects and contractors prefer wireless systems for the cost and complexity reduction achieved by eliminating wired infrastructure during building construction; existing facility renovation and expansion scenarios where wireless systems enable nurse call capability deployment in newly commissioned clinical areas without the cabling disruption and cost that wired system extension would require; and the rapidly growing long-term care, assisted living, and homecare settings where the absence of existing wired healthcare network infrastructure makes wireless deployment the only practically viable nurse call implementation pathway.

By Application, emergency medical alarms dominate, workflow support grows fastest

Emergency medical alarms retained the dominant application position with approximately 36.70% of the nurse call system market in 2025, reflecting the fundamental and non-negotiable patient safety requirement for urgent clinical communication systems in acute care settings whose medical emergency frequency, patient vulnerability, and clinical outcome sensitivity to response time make reliable emergency alerting the core value proposition around which all nurse call system commercial relationships are built. The emergency alarm application’s market leadership reflects both the high-acuity nature of acute hospital care environments that generate the highest emergency alert volumes and the regulatory and accreditation requirements that mandate specific emergency alerting capabilities and response time standards across hospital, intensive care, emergency department, and surgical care environments in major healthcare markets. The technical sophistication of modern emergency alert management has advanced substantially beyond the simple call-and-acknowledge model, with smart alarm systems that distinguish between genuine clinical emergencies and nuisance activations, escalation logic that automatically involves additional staff when primary responders are unavailable, and real-time response time monitoring that provides nursing leadership with compliance visibility against regulatory standards and quality improvement targets.

Workflow support applications are the fastest-growing application segment at a CAGR of approximately 12.30% through 2035, propelled by healthcare system operators’ growing recognition that the most commercially valuable application of modern nurse call system technology is not the emergency alerting capability that basic systems have always provided but the operational workflow intelligence that connected, data-generating nurse call platforms enable when integrated with staff scheduling systems, electronic health records, patient flow management platforms, and hospital command centre operations. The workflow support application encompasses task communication and assignment management, care round coordination and documentation, housekeeping and environmental services request management, bed management and patient transport coordination, and the clinical team communication workflows whose fragmentation across disconnected tools is a primary source of operational inefficiency and care coordination error that integrated nurse call workflow platforms address by providing a unified communication and task management infrastructure for the full clinical team.

By End User, hospitals & clinics dominate, nursing homes grow fastest

Hospitals and clinics retained the dominant end user position with approximately 46.50% of the nurse call system market in 2025, as the combination of the highest patient volume, the most complex clinical communication requirements, the strongest regulatory compliance obligations, and the largest capital investment capacity of any healthcare facility category makes the acute hospital segment both the largest and most commercially sophisticated nurse call system procurement market. The hospital nurse call system market is characterised by enterprise-scale procurement decisions where health system IT leaders, clinical informatics teams, nursing leadership, and facilities management collectively evaluate nurse call platform alternatives against clinical workflow, integration, operational efficiency, and total cost of ownership criteria in procurement processes whose duration and rigour reflect the mission-critical nature of the infrastructure being selected and the multi-year contract terms that system replacement investments typically encompass. The growing convergence of nurse call with broader clinical communication and collaboration platform investments, where hospitals are simultaneously deploying nurse call, clinical alarm management, secure messaging, and real-time location system capabilities through vendor ecosystem relationships rather than independent point solution procurement, is creating commercial advantage for vendors including Ascom, STANLEY Healthcare, and Hill-Rom whose portfolio breadth enables integrated platform propositions that reduce the system integration complexity and total cost that multi-vendor clinical communication environments impose.

Nursing homes and assisted living centres are the fastest-growing end user segment at a CAGR of approximately 10.90% through 2035, propelled by the extraordinary demographic tailwind of ageing populations in high-income countries creating a rapidly expanding elderly care facility sector whose nurse call infrastructure requirements are being simultaneously elevated by strengthening regulatory patient safety standards, growing resident expectation for responsive care communication, and the operational efficiency pressure on facility operators whose staffing costs represent 60 to 70% of total operating expenses and whose nurse call system technology can meaningfully reduce through optimised care rounding, alert triage, and staff response coordination. Sensio’s January 2025 agreement with Lovett Care to integrate sensor technology RoomMate with digital nurse call capability for long-term care settings demonstrates the commercial momentum of technology innovation specifically targeted at the nursing home and assisted living segment’s distinctive clinical communication and patient monitoring requirements, where the combination of passive sensor-based fall detection and nurse call alerting addresses the highest-frequency adverse event in elderly care settings whose prevention delivers clinical benefit, liability reduction, and regulatory compliance simultaneously.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Nurse Call System Market Insights

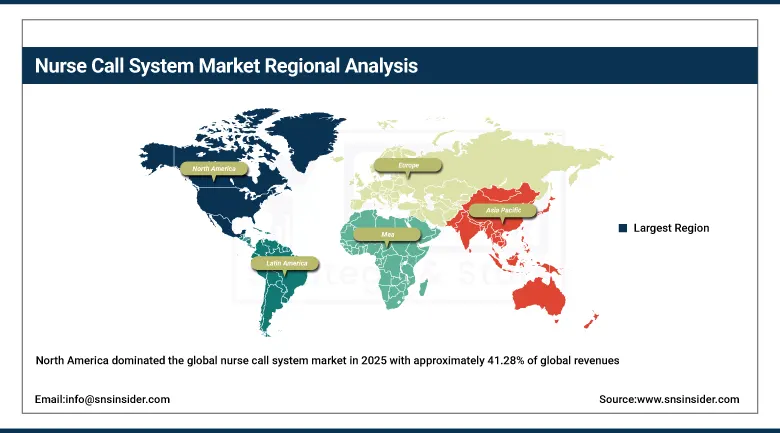

North America dominated the global nurse call system market in 2025 with approximately 41.28% of global revenues, driven by the United States’ combination of the world’s highest per-capita healthcare capital expenditure, the most comprehensive patient safety regulatory framework for clinical communication systems, and the largest installed base of hospital nurse call infrastructure undergoing active technology refresh cycles toward modern IP-networked and mobile-integrated platforms. The U.S. accounts for approximately 87.4% of North American nurse call revenues through its approximately 6,120 registered hospitals, 15,600 nursing homes, and thousands of assisted living and ambulatory care facilities whose collectively substantial nurse call system procurement and replacement activity sustains the world’s largest national nurse call market. Canada contributes approximately 12.6% of North American revenues through a provincial health system whose hospital technology investment is supported by Canada Health Infoway’s digital health infrastructure funding and whose growing long-term care sector, serving Canada’s above-average elderly population proportion, generates increasing nurse call system demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Nurse Call System Market Insights

Europe is the world’s second-largest nurse call system market where the combination of universal healthcare systems with substantial hospital infrastructure investment capacity, strong patient safety regulatory frameworks under the EU Medical Device Regulation and national hospital accreditation standards, and particularly advanced long-term care sector development driven by Europe’s ageing population demographics are collectively creating sustained nurse call system procurement demand across both acute and long-term care facility categories. Germany accounts for approximately 22.3% of European nurse call revenues as the region’s largest national market, driven by the country’s extraordinary hospital density with approximately 1,700 acute care hospitals, its leading position in healthcare technology adoption and medical device innovation, and the strong domestic industrial base of nurse call system manufacturers and integrators including Ascom’s European operations and regional specialists. The EU’s Directive on work-life balance for parents and carers and national strategies for elderly care in Germany, France, and the Nordic countries are creating institutional investment in the assisted living and residential care facility sector that generates growing nurse call system procurement alongside the acute hospital market.

Asia Pacific Nurse Call System Market Insights

Asia Pacific is the fastest-growing regional nurse call system market at a CAGR of approximately 11.07% through 2035, driven by the region’s extraordinary combination of the world’s largest and most rapidly ageing populations in Japan, China, South Korea, and India, the largest healthcare infrastructure construction programme occurring across the region as governments invest in hospital and elderly care facility capacity to serve growing healthcare demand, and the accelerating adoption of advanced clinical communication technology as Asian healthcare systems progressively align their patient safety and hospital operation standards with international best practice frameworks. China accounts for approximately 61.7% of Asia Pacific nurse call revenues through the combination of the world’s most ambitious hospital construction programme, the rapid development of senior care facility infrastructure serving China’s ageing population, and the government’s Healthy China 2030 initiative directing substantial healthcare infrastructure investment toward the technology standards that modern clinical communication systems represent. Japan and South Korea represent the most technologically sophisticated secondary markets within Asia Pacific whose advanced nurse call system procurement reflects both their elderly population demographics creating long-term care facility demand and their healthcare system technology leadership in mobile clinical communication and intelligent alerting.

MEA & Latin America Nurse Call System Market Insights

The Middle East and Africa and Latin America are growing nurse call system markets where significant healthcare infrastructure investment programmes, rising patient safety standards, and growing private hospital sector development are creating expanding nurse call system procurement across both new hospital construction and facility technology upgrade projects. Saudi Arabia leads Middle East and Africa nurse call revenues at approximately 38.4% of the regional total through Vision 2030’s extraordinary healthcare infrastructure investment, whose new hospital construction programme and existing facility upgrade initiatives are incorporating modern nurse call system requirements as standard specifications. Brazil leads Latin American nurse call revenues at approximately 44.2% of the regional total through its combination of the region’s largest hospital network, growing private healthcare sector investment in patient safety and clinical quality infrastructure, and a rapidly expanding elderly care facility sector serving Brazil’s ageing population whose nurse call system requirements are increasing proportionally with demographic growth in the elderly care consumer segment.

Market Dynamics

Growth Drivers: Demographic ageing expanding patient populations in both acute and long-term care settings, patient safety regulatory requirements elevating nurse call system capability standards, and hospital digitalization creating demand for integrated clinical communication platforms

The primary structural growth drivers for the nurse call system market are the demographic inevitability of ageing populations in high-income countries and the rapidly growing elderly care facility sectors they generate, combined with the progressive strengthening of patient safety regulatory requirements that are mandating higher nurse call system capabilities across acute, long-term, and ambulatory care settings globally. The global nursing shortage, whose severity is documented by the WHO’s estimate of a 5.9 million nurse deficit worldwide, creates an operational imperative for nurse call system technology investment that maximises the clinical communication efficiency of the available nursing workforce by reducing alert management overhead, eliminating unnecessary physical movement for alert receipt and response, and providing clinical decision support that improves care triage quality per nursing staff member.

Restraints: High capital cost of modern integrated nurse call system deployment, healthcare facility IT infrastructure complexity limiting system integration depth, and interoperability gaps between nurse call platforms and clinical information systems

A significant restraint on the nurse call system market is the substantial capital investment requirement of modern integrated nurse call system deployment, whose combined hardware, software, network infrastructure, integration, and staff training costs can represent multi-million dollar investments for large hospital facilities whose capital budget competition with medical equipment, facility renovation, and electronic health record system investments creates procurement prioritisation pressure that extends nurse call refresh cycle timelines beyond the technology lifecycle that optimal operational performance would ideally dictate.

Opportunities: AI-integrated passive fall detection creating preventive alerting capability beyond traditional reactive call systems, homecare and hospital-at-home programme expansion creating new installation markets, and unified clinical communication platform integration creating higher-value nurse call system propositions

The AI-integrated passive monitoring and fall prevention opportunity represents the most commercially significant technology evolution in the nurse call system market, as the demonstrated clinical and financial value of preventing falls in elderly care settings, whose average cost per patient fall event exceeds USD 30,000 in direct and indirect healthcare system expense, creates a compelling return on investment rationale for the nurse call system technology investment that AI-integrated passive monitoring represents. The hospital-at-home programme expansion across the United States, United Kingdom, and Australia is creating a new installation market for nurse call equivalent patient monitoring and emergency alerting systems in residential settings that represent the market’s most commercially novel frontier, with consumer-grade and clinical-grade personal emergency response system solutions competing to establish the technical and commercial standard for this emerging care delivery model’s communication infrastructure.

Recent Developments:

-

2025: Sensio announced a long-term strategic agreement with Lovett Care in January 2025 to facilitate the development of sensor technology RoomMate and a digital nurse call system for integration across Lovett Care’s UK care home network, combining AI-based fall detection, passive infrared monitoring, and nurse call alerting in an integrated platform designed specifically for the long-term care setting’s distinctive patient monitoring requirements.

-

2025: Ascom Holdings expanded its Telligence nurse call platform with new AI-powered alarm prioritisation and mobile alert routing capabilities, enabling acute care hospitals to implement intelligent clinical alarm management that reduces alarm fatigue by automatically prioritising alerts by clinical urgency and routing them to the most appropriate available staff member based on location and role.

-

2025: STANLEY Healthcare launched an enhanced version of its nurse call and patient flow platform with expanded real-time location system integration, enabling hospitals to correlate nurse call alert data with staff and patient location information for automated response routing, compliance monitoring against response time standards, and operational analytics that support quality improvement programme development.

-

2025: Hill-Rom (Baxter International) introduced expanded integration between its nurse call system platform and the Welch Allyn patient monitoring portfolio, enabling vital sign alarm data from bedside monitoring equipment to be routed through the nurse call system infrastructure for centralised clinical alert management that reduces nursing station complexity and improves care team alert awareness.

-

2025: Rauland-Borg launched a new cloud-based nurse call management platform providing hospital systems with centralised visibility across multi-facility nurse call deployments, enabling health system operations teams to monitor alert response performance, manage system configuration, and identify operational improvement opportunities across their entire installed base through a unified cloud-hosted management interface.

Nurse Call System Market Key Players

-

Rauland-Borg Corporation

-

Ascom Holding AG

-

Hill-Rom Holdings Inc. (Baxter International)

-

STANLEY Healthcare (Securitas Technology)

-

Philips Healthcare

-

Honeywell Life Safety

-

Azure Healthcare Ltd.

-

Critical Alert Systems LLC

-

Telequip Labs Inc.

-

Austco Healthcare

-

Intercall Systems Inc.

-

Ametek Inc.

-

Jeron Electronic Systems Inc.

-

Cornell Communications

-

Vs Systems

-

Nurse Call Corporation

-

Aiphone Corporation

-

Wandsworth Group

-

Curbell Medical Products

-

Sensio AS

Nurse Call System Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.24 Billion |

| Market Size by 2035 | USD 5.95 Billion |

| CAGR | CAGR of 10.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By System Type (Wired Systems, Wireless Systems, Hybrid Systems) • By Component (Button Systems, Mobile Systems, Intercom Systems, Others) • By Application (Emergency Medical Alarms, Nurse Call & Response, Workflow Support, Others) • By End User (Hospitals & Clinics, Nursing Homes & Assisted Living, Homecare Settings, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Rauland-Borg Corporation, Ascom Holding AG, Hill-Rom Holdings Inc. (Baxter International), STANLEY Healthcare (Securitas Technology), Philips Healthcare, Honeywell Life Safety, Azure Healthcare Ltd., Critical Alert Systems LLC, Telequip Labs Inc., Austco Healthcare, Intercall Systems Inc., Ametek Inc., Jeron Electronic Systems Inc., Cornell Communications, Vs Systems, Nurse Call Corporation, Aiphone Corporation, Wandsworth Group, Curbell Medical Productsl, Sensio AS |

Frequently Asked Questions

The Nurse Call System Market is expected to grow at a CAGR of 10.26% from 2026 to 2035.

The Nurse Call System Market was valued at USD 2.24 Billion in 2025.

Demographic ageing expanding patient populations in both acute and long-term care settings generating structural demand for patient communication infrastructure, combined with patient safety regulatory requirements mandating advanced nurse call system capabilities.

Wired Systems dominated with approximately 58.40% of revenues in 2025.

North America dominated the Nurse Call System Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch