Oil and Gas Refining Industry Market Report Scope & Overview:

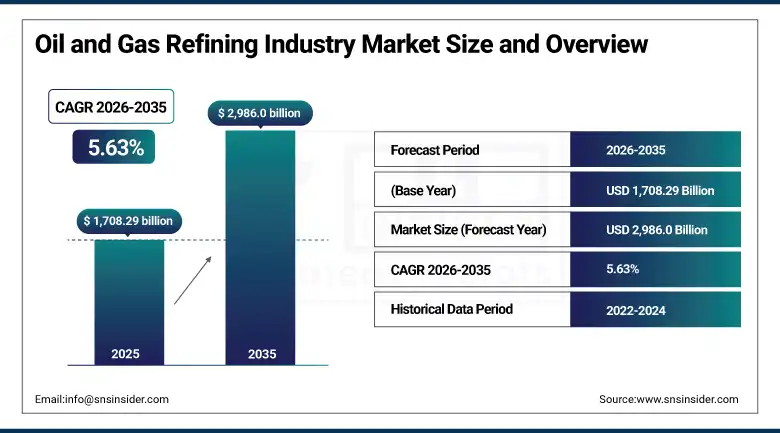

The Oil and Gas Refining Industry market was valued at USD 1,708.29 billion in 2025 and is expected to reach USD 2,986.0 billion by 2035, growing at a CAGR of 5.63% from 2026–2035.

The oil and gas refining industry performs the critical transformation of crude petroleum, natural gas liquids, and other hydrocarbon feedstocks into the spectrum of refined products that power the global economy, serve as the raw material feedstock for the petrochemical industry, lubricate the world's machinery, and provide the aviation fuel, marine fuel, heating oil, and liquefied petroleum gas that modern civilization depends upon in quantities that no alternative energy source currently approaches at comparable scale and energy density. Petroleum refineries are among the most complex and capital-intensive industrial facilities in existence, where thousands of kilometers of piping, hundreds of process vessels, heat exchangers, compressors, and reaction vessels operating at extreme temperatures and pressures are coordinated by sophisticated process control systems to continuously transform a stream of crude petroleum into dozens of precisely specified product streams whose properties must meet exact regulatory and commercial quality specifications.

The International Energy Agency's 2025 Oil Market Report confirming that global liquid fuels demand reached 103 million barrels per day in 2024, sustained by the continued growth of aviation, petrochemical, and marine fuel demand that offsets modest displacement in road transport from electric vehicle adoption, provides the fundamental demand driver that sustains refinery capacity utilization and throughput investment across all major refining regions through the 2026 to 2035 forecast period.

Market Size and Forecast

-

Market Size in 2026E: USD 1,804.48 Billion

-

Market Size by 2035: USD 2,986.0 Billion

-

CAGR: 5.63% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Oil and Gas Refining Industry Market - Request Free Sample Report

Oil and Gas Refining Industry Market Trends

-

Growing refinery digitalization and AI-based process optimization are improving operational efficiency and product yields.

-

Increasing refinery-petrochemical integration is supporting higher production of chemical feedstocks over transportation fuels.

-

Rising adoption of residue upgrading and deep conversion technologies is enabling efficient processing of heavy crude oils.

-

Expanding investments in sustainable aviation fuel and renewable diesel production are supporting refinery decarbonization efforts.

-

Advanced catalyst technologies are improving refining efficiency, product quality, and energy optimization across refining operations.

The U.S. Oil and Gas Refining Industry Market Outlook

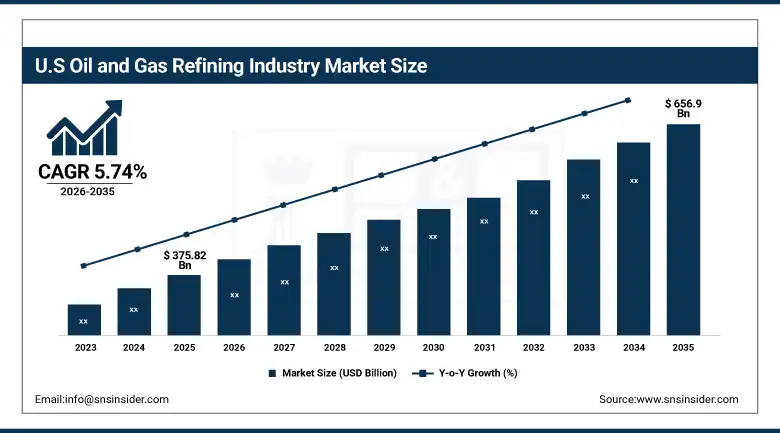

The U.S. Oil and Gas Refining Industry Market was valued at approximately USD 375.82 billion in 2025 and is expected to reach approximately USD 656.9 billion by 2035, growing at a CAGR of 5.74%, driven by the world's largest installed refinery distillation capacity, sustained domestic fuel demand underpinning refinery throughput. The Gulf Coast's extraordinary concentration of complex integrated refinery operations, and growing renewable feedstock co-processing investment positioning U.S. refineries for the energy transition.

The United States maintains the world's largest petroleum refining capacity at approximately 18 million barrels per day of atmospheric distillation capacity across its Gulf Coast, Midwest, East Coast, and West Coast refinery clusters, operated by major integrated oil companies including ExxonMobil, Phillips 66, Valero, Marathon Petroleum, and PBF Energy whose collective refinery systems represent the most complex, high-conversion, and efficient national refinery fleet in the world. U.S. refineries' high complexity as measured by the Nelson Complexity Index, averaging approximately 11 to 12 versus the global average of 8 to 9, reflects decades of investment in upgrading units that enable processing of the heavy, high-sulphur Canadian and Latin American crude oil grades alongside the lighter domestic shale crude production that together supply the world's most diverse crude slate. The Inflation Reduction Act's renewable diesel and sustainable aviation fuel production incentives are driving substantial co-processing and dedicated renewable fuel investment at U.S. refinery sites.

The U.S. Energy Information Administration's 2025 Petroleum Supply Monthly confirming that U.S. refineries processed an average of 16.4 million barrels per day of crude oil and feedstocks in 2024, representing approximately 16% of global refinery throughput, demonstrates the sustained scale of U.S. refinery operations that sustains the largest national market contribution to the global oil and gas refining industry market by revenue.

Oil and Gas Refining Industry Market Segment Analysis

-

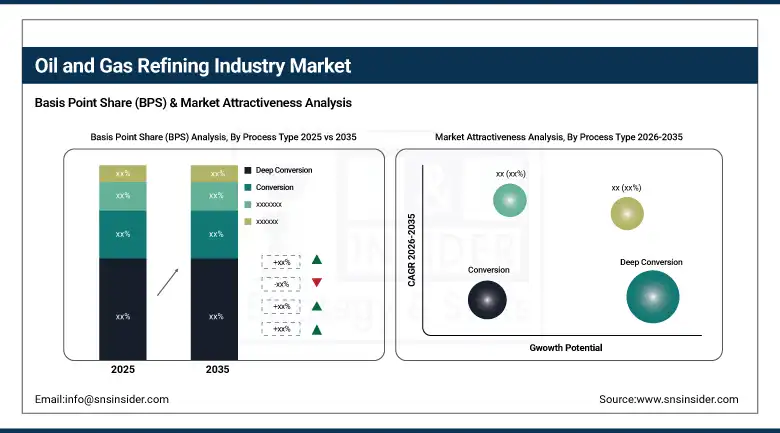

By Process Type, deep conversion dominated with approximately 45% revenue share in 2025 driven by rising crude quality challenges and the need for maximum residue upgrading to heavy fuel oil quality specifications post-IMO 2020. Conversion is the fastest-growing process type at a CAGR of 9.78%.

-

By Product Type, middle distillates dominated with approximately 53% revenue share in 2025 driven by growing demand for diesel, kerosene, and jet fuel across transportation, aviation, and heating applications. Petrochemicals are the fastest-growing product type as crude-to-chemicals integration maximizes the proportion of barrel value captured through chemical rather than fuel product yields.

-

By Application, transportation dominated with approximately 36% revenue share in 2025 through vehicular fuel consumption and growing urban mobility trends. Aviation is the fastest-growing application at a CAGR of 10.99%.

By Process Type, deep conversion dominates, conversion is expected to grow fastest

Deep Conversion retained the dominant process position with approximately 45% of oil and gas refining industry market revenues in 2025, as the combination of the progressive global trend toward heavier, higher-sulphur crude oil feedstocks whose production is growing faster than lighter sweet crude supply. The IMO 2020 marine fuel sulphur cap creating a structural demand shift away from high-sulphur fuel oil that had historically been the residue barrel's primary disposition, and the continuing spread of low-sulphur transportation fuel regulations that require refineries to process greater quantities of sulphur from their crude intake collectively create an inexorable commercial motivation for deep conversion capacity investment. Hydrocracking, delayed coking, and residue fluid catalytic cracking collectively constitute the deep conversion process technologies whose capital investment at refineries worldwide has accelerated following IMO 2020's commercial transformation of the residue barrel's value.

Conversion is the fastest-growing process type at a CAGR of 9.78% through 2035, reflecting the investment being made by semi-complex refineries in developing economies that currently lack comprehensive conversion capability to upgrade from the simple distillation operations that limit their crude flexibility and product yield value to integrated conversion facilities. That can process the full range of crude oils including heavy and sour grades while maximizing distillate yield and minimizing residue production. The Asia-Pacific and Middle Eastern refinery expansion programme is characterized by new-build complex refineries incorporating full conversion capability from inception rather than the incremental upgrading trajectory that characterized the development of Western refinery complexity over decades.

By Application, transportation dominates, aviation is expected to grow fastest

Transportation retained the dominant application position with approximately 36% of the oil and gas refining industry market in 2025, as the global light and heavy-duty vehicle fleet's petroleum fuel consumption continues to represent the largest single category of refined product demand despite the progressive electric vehicle adoption that is beginning to reduce gasoline demand growth in developed markets. Road transportation fuel demand is sustained by the continuing growth of commercial road freight, where the absence of battery technology at practical payload and range for heavy trucking applications means diesel continues to power the vast majority of the world's freight tonne-kilometre demand, and by personal vehicle fleet growth in developing economy markets where rising incomes are enabling first-time vehicle ownership at rates that exceed electric vehicle displacement of existing ICE vehicles in developed markets.

Aviation is the fastest-growing application at a CAGR of 10.99% through 2035, driven by the extraordinary recovery and continued expansion of global air travel following the COVID-19 disruption. Where the International Air Transport Association's projections of passenger traffic returning to pre-pandemic levels and continuing to grow by 3 to 4% annually through the forecast period represent the most significant demand growth opportunity available to the refining industry. The sustainable aviation fuel mandate that European Commission regulations, U.S. Inflation Reduction Act incentives, and airline net-zero commitments are collectively creating is transforming refinery investment priorities toward both petroleum-to-SAF hydro processing investments and bio-feedstock co-processing at existing hydrotreater units, creating the fastest-growing new refinery process investment category of the current decade.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.7% |

|

Europe |

Russia |

28.4% |

|

Asia Pacific |

China |

52.3% |

|

Middle East & Africa |

Saudi Arabia |

36.8% |

|

Latin America |

Brazil |

38.6% |

North America Oil and Gas Refining Industry Market Insights

North America is the world's second-largest oil and gas refining market, with the United States accounting for approximately 85.7% of North American revenues as the largest national refinery capacity holder globally. The region's sophisticated refinery fleet, characterized by the world's highest average Nelson Complexity Index, enables processing flexibility that accommodates the full range of available crude qualities from ultra-light shale condensates through heavy Canadian oil sands bitumen blends. The Gulf Coast refinery cluster's unique combination of deep-water port access for crude imports and product exports, pipeline connectivity to the U.S. crude production heartland, and proximity to the world's largest petrochemical complex sustains its position as the most commercially strategic refining location in the Western Hemisphere.

Europe Oil and Gas Refining Industry Market Insights

Europe is a mature and transitioning oil and gas refining market where the energy transition pressure toward renewable energy, carbon pricing through the EU Emissions Trading System, and progressive transportation electrification are creating structural demand reduction pressure on petroleum fuel products that motivates refinery rationalization, complexity investment, and renewable feedstock conversion to sustain commercial viability through the transition period. Russia accounts for approximately 28.4% of European refining revenues through its enormous national refinery system that serves both domestic consumption and export markets. Though geopolitical sanctions following the 2022 Ukraine invasion have fundamentally restructured Russian crude oil and refined product trade flows in ways that continue to reshape European refining competitive dynamics.

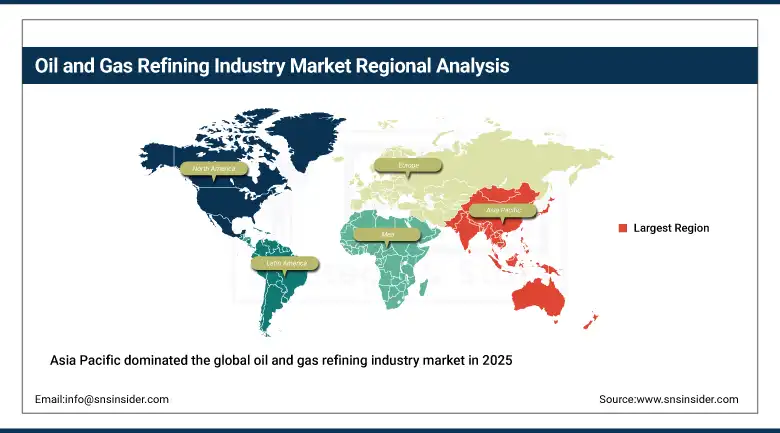

Asia Pacific Oil and Gas Refining Industry Market Insights

Asia Pacific dominated the global oil and gas refining industry market in 2025 as both the largest and fastest-growing region, anchored by China's position as the world's most rapidly expanding national refinery system. India's ambitious refinery capacity expansion programme serving the world's fastest-growing major economy fuel demand, and the Middle Eastern producers' downstream integration investments in refinery assets serving Asian fuel demand. China accounts for approximately 52.3% of Asia Pacific revenues through its combination of the world's second-largest total refinery capacity, the most rapid new complex refinery construction programme of any country, and the deepening integration of refinery and petrochemical operations in coastal industrial complexes that are achieving world-scale production efficiency.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Oil and Gas Refining Industry Market Insights

Middle East and Africa and Latin America are important and growing oil and gas refining markets where the producing nations' strategic downstream integration ambitions, growing domestic fuel demand, and access to competitive feedstocks create conditions for refinery capacity investment. Saudi Arabia leads MEA refining revenues at approximately 36.8% of regional revenues through Saudi Aramco's integrated refining and petrochemical operations at Ras Tanura, Jazan, and the SATORP and SAMREF joint ventures that together represent one of the world's largest individual refinery complexes. Brazil leads Latin American revenues at approximately 38.6% through Petrobras's national refinery system and the progressive commercialization of Brazil's presalt deepwater crude production that supplies the domestic refinery system.

Market Dynamics

Growth Drivers: Rising global liquid fuel demand driven by aviation recovery, petrochemical growth, and developing economy transportation expansion

The primary structural growth drivers for the oil and gas refining industry market are the sustained global liquid fuel demand growth driven by the three most commercially important demand categories that are each growing at above-average rates. Aviation fuel whose demand is recovering and growing from the extraordinary COVID-19 disruption through the structural growth of air travel in developing economies. Petrochemical feedstock demand whose growth is driven by the expanding production of plastics, synthetic fibres, and chemical intermediates that underpin the manufactured goods economy. Road transportation fuel in developing Asia, Africa, and Latin America whose vehicle fleet growth is outpacing the impact of electric vehicle adoption in mature markets. Simultaneously, the progressive tightening of environmental regulations governing refinery emissions, product sulphur content, and carbon intensity is driving capital investment in process technology upgrades and equipment modernization that expands the market's capital expenditure component.

Restraints: Energy transition long-term demand uncertainty creating capital investment hesitation, carbon pricing mechanisms increasing refinery operating cost in regulated markets

A significant restraint on the oil and gas refining industry market is the capital investment hesitation that long-term energy transition uncertainty creates among refinery operators and their financial backers. Where the genuine uncertainty about the pace of transportation electrification, the timeline for sustainable aviation fuel cost reduction to commercial competitiveness, and the ultimate trajectory of global petroleum product demand creates portfolio allocation challenges that cause refiners to prefer shorter payback period operational improvements over the long-term capital commitments that large refinery expansion or conversion projects require.

Opportunities: Sustainable aviation fuel production integration leveraging existing hydro processing assets, crude-to-chemicals integration maximizing chemical feedstock yield from crude

The sustainable aviation fuel production opportunity represents the most commercially aligned growth investment available to existing petroleum refineries. As the co-processing of bio-based feedstocks including used cooking oil, animal fats, and agricultural residues in existing hydrotreater and hydrocracker units requires modest capital modification to process up to 5 to 10% bio-feedstock blends without dedicated facility investment. While the IRA production tax credits for SAF produced at U.S. refineries and the European SAF mandate creating minimum blending obligations generate the revenue premium that justifies bio-feedstock procurement at above-fossil fuel cost parity.

Recent Developments:

-

2025: Saudi Aramco advanced construction of its Jizan Integrated Gasification and Liquids-to-Chemicals complex, the world's largest crude-to-chemicals refinery project designed to maximize petrochemical feedstock production from Arabian Heavy crude and minimize transportation fuel production, demonstrating the downstream integration strategy that is reshaping the economics of oil producing nation refinery investment.

-

2025: Valero Energy Corporation expanded its sustainable aviation fuel co-processing operations at multiple U.S. Gulf Coast refineries following the Inflation Reduction Act's production tax credit framework for SAF, making Valero the leading U.S. producer of renewable diesel and SAF from its existing hydrocracker infrastructure adapted for bio-feedstock co-processing.

-

2025: Shell completed major turnaround maintenance at its Pernis Rotterdam refinery incorporating AI-assisted process optimization systems and advanced emission monitoring infrastructure as part of its commitment to reduce refinery CO2 intensity by 30% by 2035 while maintaining competitive refinery margins through the efficiency improvements that digital optimization enables.

Oil and Gas Refining Industry Market Key Players are:

-

Saudi Aramco

-

Sinopec Group

-

China National Petroleum Corporation (CNPC)

-

ExxonMobil Corporation

-

Shell plc

-

BP plc

-

Valero Energy Corporation

-

Marathon Petroleum Corporation

-

Phillips 66 Company

-

TotalEnergies SE

-

Chevron Corporation

-

Indian Oil Corporation Ltd.

-

Reliance Industries Limited

-

Petrobras (Petróleo Brasileiro S.A.)

-

Rosneft Oil Company

-

Kuwait Petroleum Corporation

-

Abu Dhabi National Oil Company (ADNOC)

-

PBF Energy Inc.

-

HF Sinclair Corporation

-

LyondellBasell Industries

Oil and Gas Refining Industry Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,708.29 Billion |

| Market Size by 2035 | USD 2,986.0 Billion |

| CAGR | CAGR of 5.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Process Type (Deep Conversion, Conversion, Separation) •By Product Type (Middle Distillates, Light Distillates, Heavy Fuel Oil, Lubricants, Petrochemicals, Others) •By Application (Transportation, Chemicals & Petrochemicals, Aviation, Marine, Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Saudi Aramco, Sinopec Group, China National Petroleum Corporation (CNPC), ExxonMobil Corporation, Shell plc, BP plc, Valero Energy Corporation, Marathon Petroleum Corporation, Phillips 66 Company, TotalEnergies SE, Chevron Corporation, Indian Oil Corporation Ltd., Reliance Industries Limited, Petrobras (Petróleo Brasileiro S.A.), Rosneft Oil Company, Kuwait Petroleum Corporation, Abu Dhabi National Oil Company (ADNOC), PBF Energy Inc., HF Sinclair Corporation, LyondellBasell Industries |

Frequently Asked Questions

Asia Pacific dominated the oil and gas refining industry Market in 2025.

Deep conversion dominated with approximately 45% of revenues in 2025.

Rising global liquid fuel demand driven by aviation traffic recovery, petrochemical feedstock growth, and developing economy transportation expansion.

The oil and gas refining industry market was valued at USD 1,708.29 billion in 2025.

The oil and gas refining industry market is expected to grow at a CAGR of 5.63% from 2026 to 2035.

Get in Touch