Oilfield Equipment Market Report Scope & Overview:

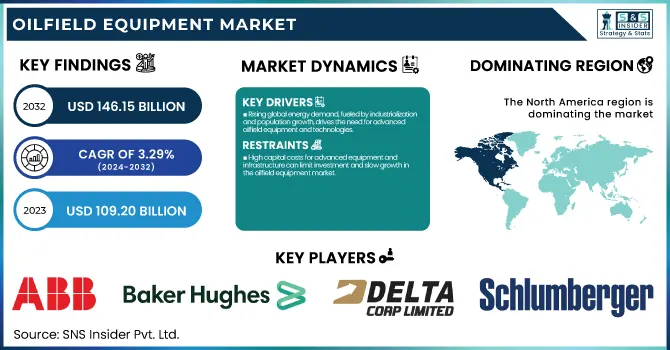

The Oilfield Equipment Market Size was esteemed at USD 109.20 billion in 2023 and is supposed to arrive at USD 146.15 billion by 2032 with a growing CAGR of 3.29% over the forecast period 2024-2032. This report offers unique insights into the oilfield equipment market by analysing production output, rig utilization rates, and maintenance metrics. It delves into the adoption of new technologies by region, reflecting how innovations are influencing operational efficiency. Export and import data is also covered, offering a snapshot of global trade patterns. Additionally, the report highlights downtime metrics, providing a clear picture of how maintenance strategies impact overall equipment performance. These insights help stakeholders understand the evolving trends and challenges in the oilfield equipment sector.

To get more information on Oilfield Equipment Market - Request Free Sample Report

Oilfield Equipment Market Dynamics

DRIVERS

-

Rising global energy demand, fueled by industrialization and population growth, drives the need for advanced oilfield equipment and technologies.

The increasing global energy demand is a key driver of the oilfield equipment market, fueled by rapid industrialization, urbanization, and population growth. As economies expand, the need for oil and gas as primary energy sources continues to rise, driving exploration and production (E&P) activities. With the development of economies, there remains an increasing demand for oil and gas as primary energy sources which drives both exploration and production (E&P) activities. The increase in demand spurs investments in advanced drilling methods such as automation and enhanced oil recovery (EOR) techniques for improved extraction efficiency. The growth of deepwater and ultra-deepwater exploration, particularly in the Gulf of Mexico, the North Sea, and offshore Africa, is also increasing the demand for specialized oilfield equipment. Data-driven digital oilfield solutions, AI-based predictive maintenance, and IoT-enabled monitoring systems are changing the way they operate to boost productivity, reduce downtime, and enhance performance. The move towards renewable energy is a long-term challenge but oil remains the great powerhouse of an energy source to this day, meaning that oilfield equipment that is creative, innovative, and effective in design and processing must be in demand for augmentation for the known future.

RESTRAINT

-

High capital costs for advanced equipment and infrastructure can limit investment and slow growth in the oilfield equipment market.

High capital costs are a significant restraint in the oilfield equipment market, as the investment required for advanced machinery, infrastructure, and technology is substantial. Drilling rigs, production platforms, and specialized equipment, potentially restrict market entry for smaller companies and prevent growth for existing players. Furthermore, there are expenses related to maintaining and upgrading equipment to industry-standard specifications. With oil and gas discovery works being increasingly more complex, specifically deepwater and unconventional fields, the demand for state-of-the-art equipment increases and so do the costs. The level of capital expenditure (capex) that these projects will require can dissuade development, particularly in times of volatile oil prices. When oil prices go down, it could take longer to see a return, providing less incentive to invest and take the market further. That is why high capital costs constitute a vital hurdle for oilfield equipment companies.

OPPORTUNITIES

-

Emerging markets like India, China, and Brazil offer significant growth opportunities for the oilfield equipment market due to rising energy demand and untapped reserves.

Emerging markets such as India, China, and Brazil represent significant growth opportunities for the oilfield equipment market. These nations are also experiencing rapid industrialization, urbanization, and increasing energy demand and the drive to explore and produce oil and gas reserves. Advanced oilfield equipment demand is highly driven by India's rising energy consumption and India's government support initiatives to increase domestic production. Likewise, China’s energy needs and its continued investment in deepwater and unconventional oil exploration also enlarge the marketplace. Brazil, which has some of the most lucrative offshore oilfields in the world especially those in the pre-salt layer represents South America’s second-largest oilfield equipment market. These countries also possess large untapped reserves, and as investments grow in exploration and production technologies, the need for state-of-the-art oilfield equipment is predicted to increase substantially in these regions. The growing markets provide a significant opportunity for global oil field equipment suppliers, enabling them to gain a sizable share of the domain.

CHALLENGES

-

Workforce shortages and the skills gap in oilfield operations hinder efficiency, increase costs, and limit the adoption of advanced technologies.

Workforce shortages and the skills gap are significant challenges facing the oilfield equipment market. As the oil and gas exploration process increases in complexity, the industry has experienced a sharp rise in demand for highly skilled workers in specialized areas like drilling, maintenance, and equipment operation. Yet many areas experience a lack of skilled labor, often due to an aging workforce, absence of technical training opportunities, and competitors luring workers away to other sectors. The lack of skilled workers results in high labor costs, delays in projects, and lesser operational efficiency. The time and money it take to train new employees only compounds the problem. In reality, this long-standing skills gap inhibits the transition to next-gen technologies since expertise in automation, digitalization, and data analytics is still limited and expertise is critical to maximizing investment in new oilfield equipment. To tackle these challenges and ensure the sustainability of the market in the long run it will be imperative for companies to work around workforce development, skill-based training programs, and recruitment modules.

Oilfield Equipment Market Segmentation Analysis

By Type

The Production Equipment segment dominated with a market share of over 44% in 2023, as it involves the necessary tools and machinery used in the extraction and processing of oil and gas. The other important aspects of production operations include wellheads, pumps, valves, and separators. These types of devices are essential components of flow control oil and gas for well parameters and also keep pressure and separate various impurities with crude oil or gas. With oil and gas production still on the rise in old and new fields alike, the need for efficient and high-performance production equipment is still there. Given the continuous demands from mature and new oil fields, the production equipment segment holds the highest market share.

By Application

The onshore applications segment dominated with a market share of over 62% in 2023, owing to the large number of onshore oil and gas reserves globally. The onshore fields are less expensive to discover and create than their offshore counterparts and represent more than half of worldwide results. That includes increased demand for oilfield machinery like drilling rigs, pumps, and safety mechanisms in onshore operations. Many of the existing oil and gas companies are already working onshore, which creates steady demand for maintenance and repairs, including upgrades and new equipment. For exploration and production activities, maritime drilling is considered less favourable than onshore projects which combined with being more economical, given logistical challenges are much lower than offshore thrive in such conditions. This leads to the onshore segment capturing the highest market share in the global oilfield equipment market.

Oilfield Equipment Market Regional Outlook

North America region dominated with a market share of over 40% in 2023, attributed to widespread oil and gas exploration operations, especially in the U.S. and Canada. With considerable investment in both technology and infrastructure, these nations have risen to become world leaders in oil production. There is a strong demand for advanced oilfield equipment due to several factors, including the development of unconventional resources such as shale gas and the increasing requirement for Offshore drilling solutions. Moreover, it has a developed supply chain, skilled labor force, and technologically advanced drilling solutions that enable efficient extraction and production processes. This allows North America to maintain its market leader position in the global oilfield equipment demand.

The Asia-Pacific region is experiencing rapid growth in the oilfield equipment market, primarily driven by surging oil and gas exploration activities in key countries like China, India, and Australia. As these countries keep growing their energy industries to satisfy the demand for oil and gas, advanced oilfield equipment becomes more pressing. China and India (in particular) are investing in onshore and offshore oil, and Australia is betting on gas extraction. The increasing demand for energy and notable investments in energy infrastructure have driven the need for advanced equipment which is expected to offer lucrative opportunities for the oilfield equipment market in the Asia Pacific region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Oilfield Equipment Market key players are:

-

ABB (Drilling Control Systems, Power Solutions)

-

Baker Hughes (Drilling Equipment, Well Completion Tools)

-

Delta Corporation (Pressure Control Equipment, Wellhead Solutions)

-

EthosEnergy Group Limited (Turbomachinery, Rotating Equipment)

-

Integrated Equipment (Blowout Preventers, Valves, Wellhead Equipment)

-

Jereh Oilfield Equipment (Fracturing Units, Cementing Equipment)

-

MSP/Drilex, Inc. (Mud Pumps, Drill String Components)

-

Sunnda Corporation (Wellhead Equipment, Flow Control Products)

-

Uztel S.A (Well Control Equipment, Valves)

-

Weir Group (Pumps, Pressure Control Equipment)

-

Halliburton (Drilling Tools, Production Equipment)

-

SLB (Schlumberger) (Well Services, Logging Equipment)

-

National Oilwell Varco (NOV) (Drilling Rigs, Pipe Handling Equipment)

-

Weatherford International (Artificial Lift Systems, Well Construction)

-

Cameron (a Schlumberger company) (Blowout Preventers, Wellheads)

-

TechnipFMC (Subsea Production Systems, Drilling Systems)

-

Aker Solutions (Subsea Equipment, Flow Assurance Solutions)

-

Dril-Quip, Inc. (Wellheads, Subsea Equipment)

-

Expro Group (Well Flow Management, Wireline Services)

-

Tenaris (OCTG Pipes, Premium Connections)

Suppliers for (oilfield equipment, digital solutions, and energy transition technologies) in Oilfield Equipment Market

-

Schlumberger Limited (SLB)

-

Halliburton

-

Baker Hughes Company

-

Weatherford International

-

National Oilwell Varco (NOV)

-

TechnipFMC plc

-

Aker Solutions

-

Cameron International (a Schlumberger company)

-

Helmerich & Payne

-

Sinopec Oilfield Equipment Corporation

RECENT DEVELOPMENT

In January 2024: Schlumberger (SLB) and Nabors Industries announced a partnership aimed at accelerating the adoption of automated drilling solutions. This collaboration seeks to integrate SLB’s drilling automation technologies with Nabors’ rig operating systems, providing oil and gas operators and drilling contractors with improved well construction performance and operational efficiency.

In April 2024: SLB also reached an agreement to acquire ChampionX, a Texas-based company specializing in pumps and pumping equipment. The acquisition is intended to strengthen SLB’s position in the production sector by combining ChampionX's expertise in production chemicals and artificial lift technologies with SLB's global reach and advanced technological capabilities.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 109.20 Billion |

| Market Size by 2032 | USD 146.15 Billion |

| CAGR | CAGR of 3.29% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Drilling Equipment, Production Equipment, Other Equipment Types) • By Application (Onshore, Offshore) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB, Baker Hughes, Delta Corporation, EthosEnergy Group Limited, Integrated Equipment, Jereh Oilfield Equipment, MSP/Drilex, Inc., Sunnda Corporation, Uztel S.A, Weir Group, Halliburton, SLB (Schlumberger), National Oilwell Varco (NOV), Weatherford International, Cameron (a Schlumberger company), TechnipFMC, Aker Solutions, Dril-Quip, Inc., Expro Group, Tenaris |

Frequently Asked Questions

Ans: North America dominated the Oilfield Equipment Market in 2023

Ans: The “Production Equipment” segment dominated the Oilfield Equipment Market.

Ans: Rising global energy demand, fueled by industrialization and population growth, drives the need for advanced oilfield equipment and technologies.

Ans: The Oilfield Equipment Market was USD 109.20 billion in 2023 and is expected to Reach USD 146.15 billion by 2032.

Ans: The Oilfield Equipment Market is expected to grow at a CAGR of 3.29% during 2024-2032.

Get in Touch